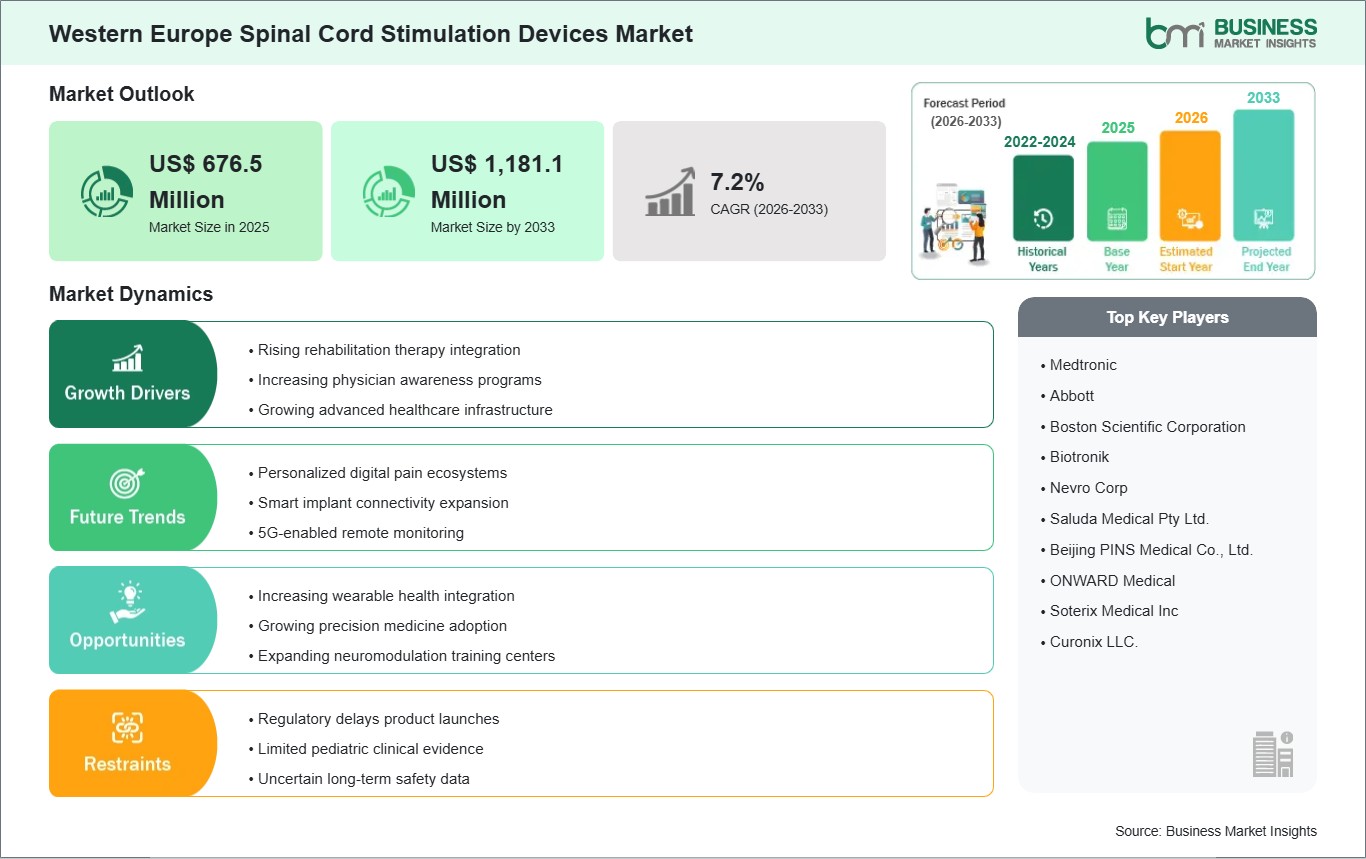

The Western Europe spinal cord stimulation devices market size is expected to reach US$ 1,181.1 million by 2033 from US$ 676.5 million in 2025. The market is estimated to register a CAGR of 7.2% from 2026 to 2033.

Executive Summary and Western Europe Spinal Cord Stimulation Devices Market Analysis:

The Western Europe spinal cord stimulation (SCS) device market is rapidly evolving within a highly developed and strictly regulated healthcare environment, where clinical decision-making is strongly guided by scientific evidence and patient outcome data. SCS therapy is increasingly being accepted as a preferred treatment option for patients with chronic neuropathic pain, failed back syndrome, and degenerative spine diseases, conditions that are becoming more prevalent in the aging population due to age-related musculoskeletal disorders. At the same time, physicians are gradually shifting away from long-term pharmacological pain management approaches toward neuromodulation-based therapies.

Market growth is further supported by advanced and efficient public healthcare systems that encourage interdisciplinary care involving neurology, orthopedics, and pain medicine. Innovative SCS technologies such as burst stimulation, high-frequency stimulation, and closed-loop feedback systems are being actively introduced across hospitals in Western Europe. In addition, strong clinical training programs and participation in neuromodulation research studies are promoting wider adoption of advanced SCS techniques. The availability of specialized pain management clinics within hospital settings also contributes significantly to market expansion.

Growth is moderated by strict regulatory approval processes and conservative reimbursement frameworks that require extensive clinical validation before widespread adoption. Budget constraints within public healthcare systems also limit the rapid uptake of high-cost implantable pain therapies. In some cases, physician reluctance toward non-traditional pain management approaches may further slow adoption. Despite these challenges, strong demand for non-opioid pain relief solutions continues to support a positive long-term outlook for the spinal cord stimulation market in Western Europe.

Western Europe Spinal Cord Stimulation Devices Market - Strategic Insights:

Get more information on this report

Western Europe Spinal Cord Stimulation Devices Market Segmentation Analysis:

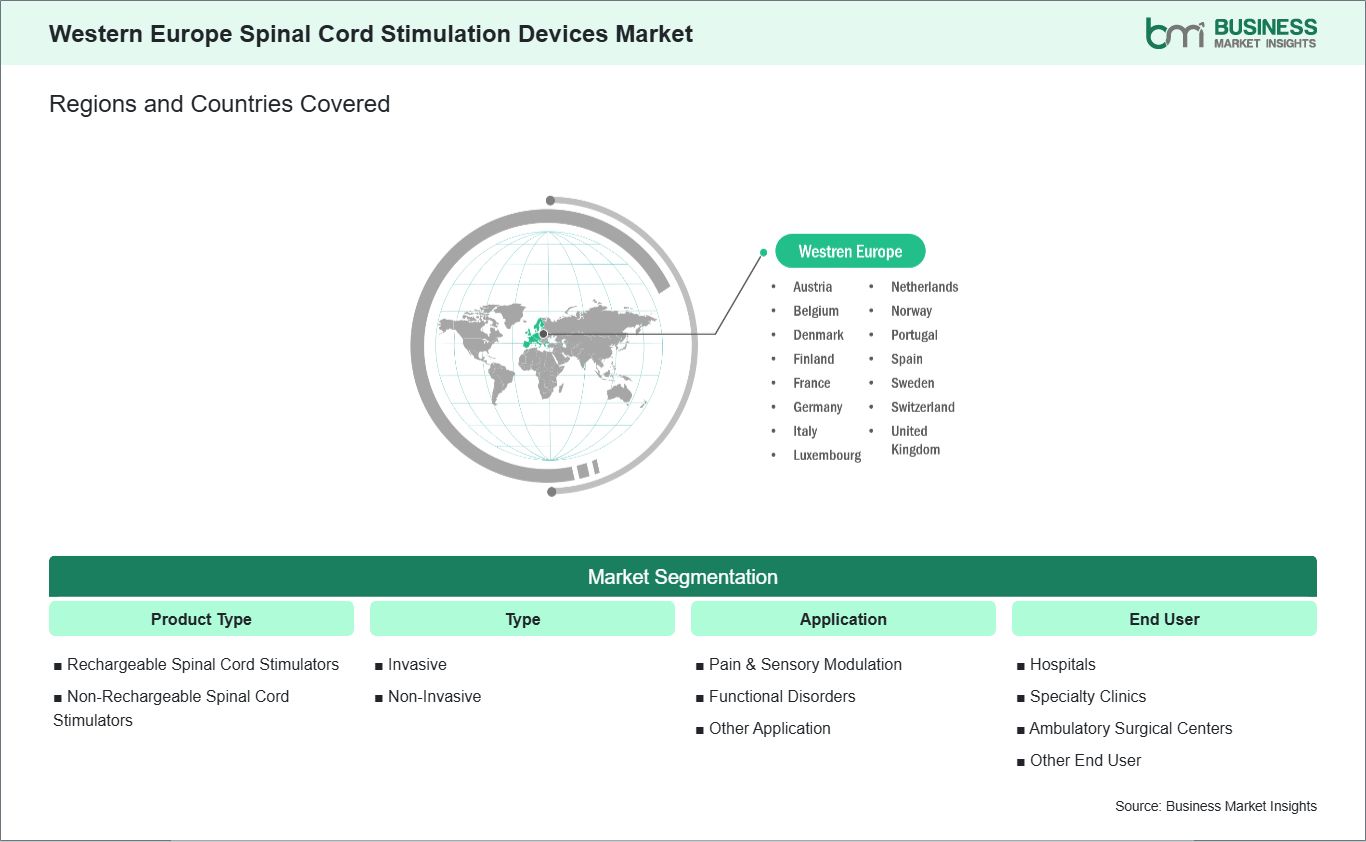

Key segments that contributed to the derivation of the Western Europe spinal cord stimulation devices market analysis are product type, type, application, and end user.

By product type, the spinal cord stimulation devices market is segmented into rechargeable spinal cord stimulators and non-rechargeable spinal cord stimulators. The rechargeable spinal cord stimulators segment dominated the market in 2025.

Based on type, the spinal cord stimulation devices market is segmented into invasive and non-invasive. The invasive segment dominated the market in 2025.

On the basis of application, the spinal cord stimulation devices market is classified into pain and sensory modulation, functional disorders, and other application. The pain and sensory modulation segment dominated the market in 2025.

In terms of end user, the spinal cord stimulation devices market is categorized into hospitals, specialty clinics, ambulatory surgical centers, and other end user. The hospitals segment dominated the market in 2025.

Western Europe Spinal Cord Stimulation Devices Market Drivers and Opportunities:

Rising Integration of Rehabilitation Therapies

The SCS market in Western Europe will increasingly be shaped by the integration of rehabilitation therapy into post-implant treatment regimens. In countries such as Germany, France, the UK, and the Netherlands, pain management teams are adopting a holistic approach to chronic neuropathic pain and failed back surgery syndrome, where spinal cord stimulation is viewed as one component of a broader functional recovery strategy. Neuromodulation is being combined with physiotherapy, occupational therapy, and cognitive pain rehabilitation to improve mobility and long-term outcomes, with this model being particularly prominent in Germany and France, especially in university hospitals and rehabilitation clinics.

Rehabilitation centers across Western Europe are also incorporating advanced physiotherapy technologies to support spinal cord stimulation outcomes. Robotic rehabilitation systems, gait training devices, and motion analysis tools are being used to improve treatment effectiveness. In Sweden and Denmark, rehabilitation units are closely linked to national pain registries, allowing clinicians to monitor long-term outcomes and adjust rehabilitation intensity based on real-world data.

There is also a clear shift toward outpatient and home-based rehabilitation programs. Healthcare systems across the region are working to reduce hospital dependence while maintaining continuous follow-up through remote monitoring and digital care platforms. Patients receiving spinal cord stimulation are increasingly enrolled in structured rehabilitation programs aimed at improving self-care, mobility, and social functioning. This model is already well established in the UK and the Netherlands.

Increasing Wearable Health Integration

In countries such as Germany, France, and the UK, wearable devices that track posture, motor activity, and physiological indicators of pain are being used in chronic pain management to provide clinicians with real-time insights into patient mobility and to optimize SCS therapy settings. There is also growing demand for wearable technologies that support outpatient and home-based care models, which are expanding across Western Europe. Patients receiving spinal cord stimulation therapy can be monitored through devices that track physical activity, sleep patterns, and stress levels, with this data increasingly used in rehabilitation programs in countries such as the Netherlands and Sweden to support clinical decision-making.

Digital health ecosystems are enabling wider integration of wearable data through smartphone-linked platforms and cloud-based remote monitoring systems. Spinal cord stimulation devices are increasingly being paired with mobile applications that allow pain tracking and, in some cases, remote parameter adjustments by clinicians. In the UK and Germany, wearable-derived data is also being incorporated into electronic health records, strengthening evidence-based treatment and improving overall patient outcomes.

Western Europe Spinal Cord Stimulation Devices Market Size and Share Analysis:

The Western Europe spinal cord stimulation devices market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within product type, type, application, and end user, highlighting their respective contributions to overall market performance.

By product type, the rechargeable spinal cord Stimulators subsegment dominated the market in 2025, because long-term chronic pain treatment requires devices that can operate continuously for several years without frequent replacement. Patients increasingly preferred rechargeable systems as they reduce the likelihood of repeat surgeries and lower overall treatment interruption.

Based on type, the invasive subsegment dominated the market in 2025 because implanted spinal cord stimulators deliver more stable and accurate nerve stimulation compared to external therapies. These systems are widely used for severe chronic pain conditions where medication and physiotherapy provide limited relief.

On the basis of application, the pain and sensory modulation subsegment dominated the market in 2025, because spinal cord stimulation is primarily designed to manage chronic neuropathic and musculoskeletal pain. The growing number of patients suffering from lower back pain, diabetic nerve pain, and post-surgical pain significantly increased demand for neuromodulation therapies.

In terms of end user, the hospitals subsegment dominated the market in 2025 because most spinal cord stimulator procedures require specialized surgical facilities, imaging equipment, and multidisciplinary pain management teams. Patients generally prefer hospitals for implantation procedures due to better emergency support and post-operative monitoring capabilities.

Western Europe Spinal Cord Stimulation Devices Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 676.5 Million

Market Size by 2033

US$ 1,181.1 Million

CAGR (2026 - 2033)

7.2%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product Type

Rechargeable Spinal Cord Stimulators

Non-Rechargeable Spinal Cord Stimulators

By Type

Invasive

Non-Invasive

By Application

Pain & Sensory Modulation

Functional Disorders

Other Application

By End User

Hospitals

Specialty Clinics

Ambulatory Surgical Centers

Other End User

Regions and Countries Covered

Western Europe

Belgium, Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, United Kingdom, Denmark, Portugal, Norway, Finland

Market leaders and key company profiles

Medtronic

Abbott

Boston Scientific Corporation

Biotronik

Nevro Corp

Saluda Medical Pty Ltd.

Beijing PINS Medical Co., Ltd.

ONWARD Medical

Soterix Medical Inc

Curonix LLC.

Get more information on this report

Western Europe Spinal Cord Stimulation Devices Market Report Coverage and Deliverables:

The "Western Europe Spinal Cord Stimulation Devices Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at regional and country levels for all market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Market concentration, heat map analysis, prominent players, and recent developments for the Market

Detailed company profiles, including SWOT analysis

Western Europe Spinal Cord Stimulation Devices Market Geographic Insights:

The geographical scope of the Western Europe spinal cord stimulation devices market report is divided into: Belgium, the Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, the UK, Denmark, Portugal, Norway, and Finland. Germany held the largest share in 2025.

Germany dominates the Western Europe spinal cord stimulation (SCS) market due to its advanced hospital infrastructure, strong neurosurgical expertise, and rapid adoption of emerging technologies. The country has a well-established network of university hospitals and specialized pain clinics where SCS is routinely integrated into the treatment of chronic neuropathic pain, spinal cord injuries, and postoperative pain conditions. Germany's healthcare system places strong emphasis on precision medicine, enabling the use of personalized and programmable neuromodulation therapies. Its robust clinical research ecosystem, supported by active collaboration between hospitals and universities, has also contributed to early adoption of next-generation SCS technologies, including closed-loop systems. Physicians in Germany have extensive experience in interventional pain management, which supports better procedural outcomes and higher confidence in implantable devices. In addition, a structured and well-defined reimbursement system provides consistent support for clinically validated SCS treatments, while large hospital networks and specialized spine centers ensure standardized patient selection, implantation, and aftercare processes. Although adoption is moderated by strict cost-effectiveness assessments and cautious introduction of new technologies, Germany continues to lead, driven by strong clinical capability, high patient awareness, and a growing shift toward non-opioid pain management strategies.

Get more information on this report

Western Europe Spinal Cord Stimulation Devices Market Research Report Guidance:

The report includes qualitative and quantitative data in the Western Europe spinal cord stimulation devices market across product type, type, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Western Europe spinal cord stimulation devices market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Western Europe spinal cord stimulation devices market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Western Europe spinal cord stimulation devices market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover the Western Europe spinal cord stimulation devices market segments by product type, type, application, end user, and geography across Belgium, the Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, the UK, Denmark, Portugal, Norway, and Finland. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Western Europe spinal cord stimulation devices market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Western Europe Spinal Cord Stimulation Devices Market News and Key Development:

The Western Europe spinal cord stimulation devices market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Western Europe spinal cord stimulation devices market are:

In May 2024, Abbott received regulatory approval in Europe for its expanded spinal cord stimulation portfolio, including the Proclaim and Eterna SCS systems, supporting broader commercial availability of advanced implantable neuromodulation devices across Western Europe for chronic pain management.

In August 2023, Medtronic received CE Mark approval for its Inceptiv closed-loop spinal cord stimulation system, enabling real-time adaptive pain therapy and strengthening its neuromodulation portfolio across Western European markets, including Germany, France, Italy, and Spain.

Key Sources Referred:

The World BankWorld Health Organization (WHO)Center for Disease Control and Prevention (CDC)Food and Drug Administration (FDA)Centers for Medicare and Medicaid Services (CMS)European CommissionMedicines and Healthcare products Regulatory Agency (MHRA)Company WebsitesCompany Annual ReportsCompany Investor Presentation

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Western Europe Spinal Cord Stimulation Devices Market?

The Western Europe Spinal Cord Stimulation Devices Market is valued at US$ 676.5 Million in 2025, it is projected to reach US$ 1,181.1 Million by 2033.

What is the CAGR for Western Europe Spinal Cord Stimulation Devices Market by (2026 - 2033)?

As per our report Western Europe Spinal Cord Stimulation Devices Market, the market size is valued at US$ 676.5 Million in 2025, projecting it to reach US$ 1,181.1 Million by 2033. This translates to a CAGR of approximately 7.2% during the forecast period.

What segments are covered in this report?

The Western Europe Spinal Cord Stimulation Devices Market report typically cover these key segments-

Product Type (Rechargeable Spinal Cord Stimulators, Non-Rechargeable Spinal Cord Stimulators)

Type (Invasive, Non-Invasive)

Application (Pain & Sensory Modulation, Functional Disorders, Other Application)

End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Other End User)

What is the historic period, base year, and forecast period taken for Western Europe Spinal Cord Stimulation Devices Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Western Europe Spinal Cord Stimulation Devices Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Western Europe Spinal Cord Stimulation Devices Market?

The Western Europe Spinal Cord Stimulation Devices Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic

Abbott

Boston Scientific Corporation

Biotronik

Nevro Corp

Saluda Medical Pty Ltd.

Beijing PINS Medical Co., Ltd.

ONWARD Medical

Soterix Medical Inc

Curonix LLC.

Who should buy this report?

The Western Europe Spinal Cord Stimulation Devices Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Western Europe Spinal Cord Stimulation Devices Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Western Europe Spinal Cord Stimulation Devices Market

Get Free Sample For Western Europe Spinal Cord Stimulation Devices Market