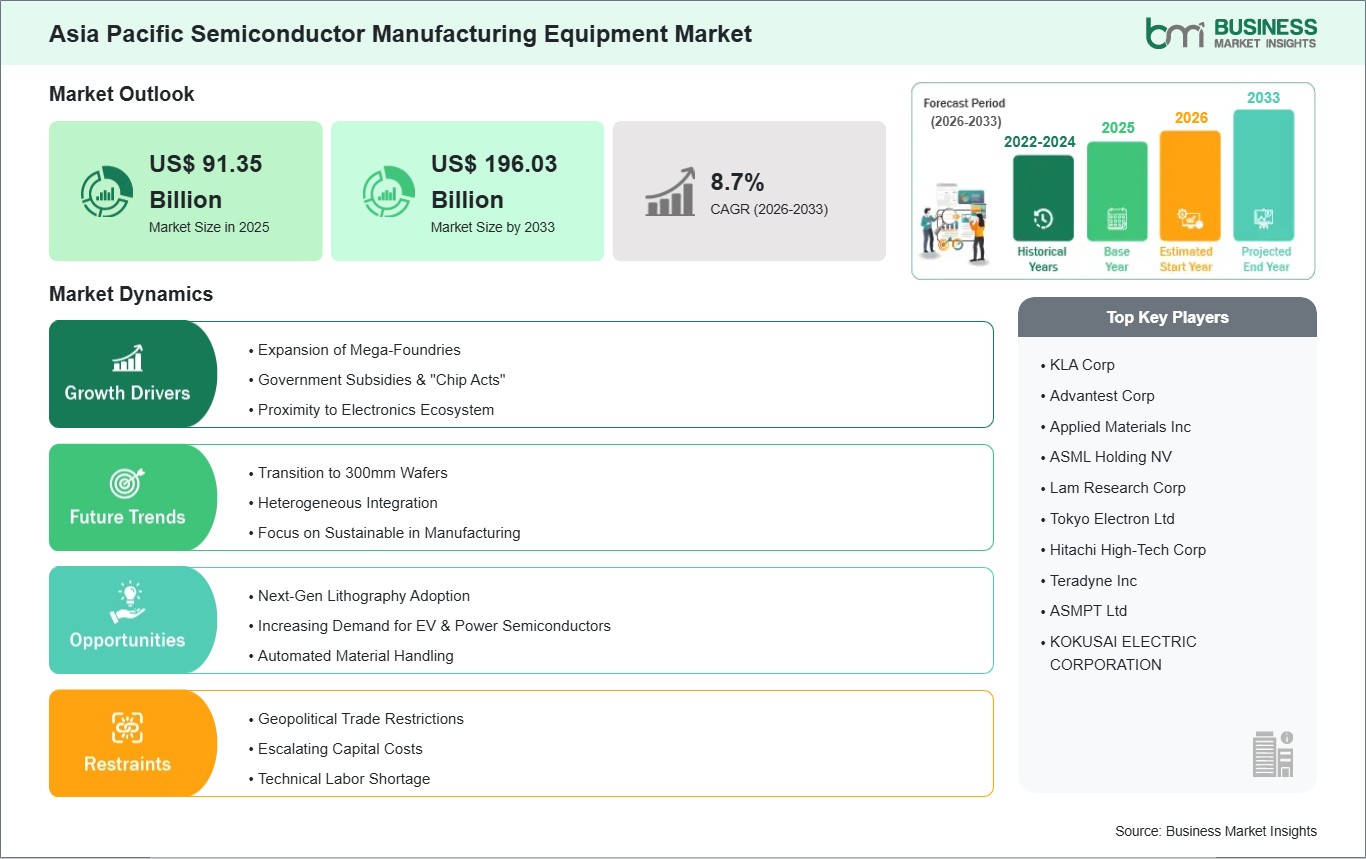

The Asia Pacific semiconductor manufacturing equipment market size is expected to reach US$ 196.03 billion by 2033 from US$ 91.35 billion in 2025. The market is estimated to record a CAGR of 8.7% from 2026 to 2033.

Executive Summary and Asia Pacific Semiconductor Manufacturing Equipment Market Analysis:

The Asia Pacific semiconductor manufacturing equipment market has witnessed robust growth, driven by rising demand for advanced semiconductor devices and significant investments in fabrication facilities across key economies such as China, Taiwan, South Korea, and Japan. Strong government initiatives and strategic incentives aimed at strengthening domestic chip production capabilities have accelerated capacity expansions and technology upgrades within the region. The surge in demand for consumer electronics, automotive applications, and edge computing has further bolstered the need for cutting‑edge manufacturing equipment. Notably, the shift toward next‑generation process nodes and the adoption of EUV lithography and advanced packaging technologies are reshaping competitive dynamics, with major global and regional players intensifying R&D to capture market share. However, supply chain disruptions and geopolitical uncertainties pose challenges to sustained growth. Overall, the Asia Pacific semiconductor manufacturing equipment market is poised for continued expansion, underpinned by strong structural demand, policy support, and technological innovation, positioning the region as a central hub in the global semiconductor value chain.

Asia Pacific Semiconductor Manufacturing Equipment Market - Strategic Insights:

Get more information on this report

Asia Pacific Semiconductor Manufacturing Equipment Market Segmentation Analysis:

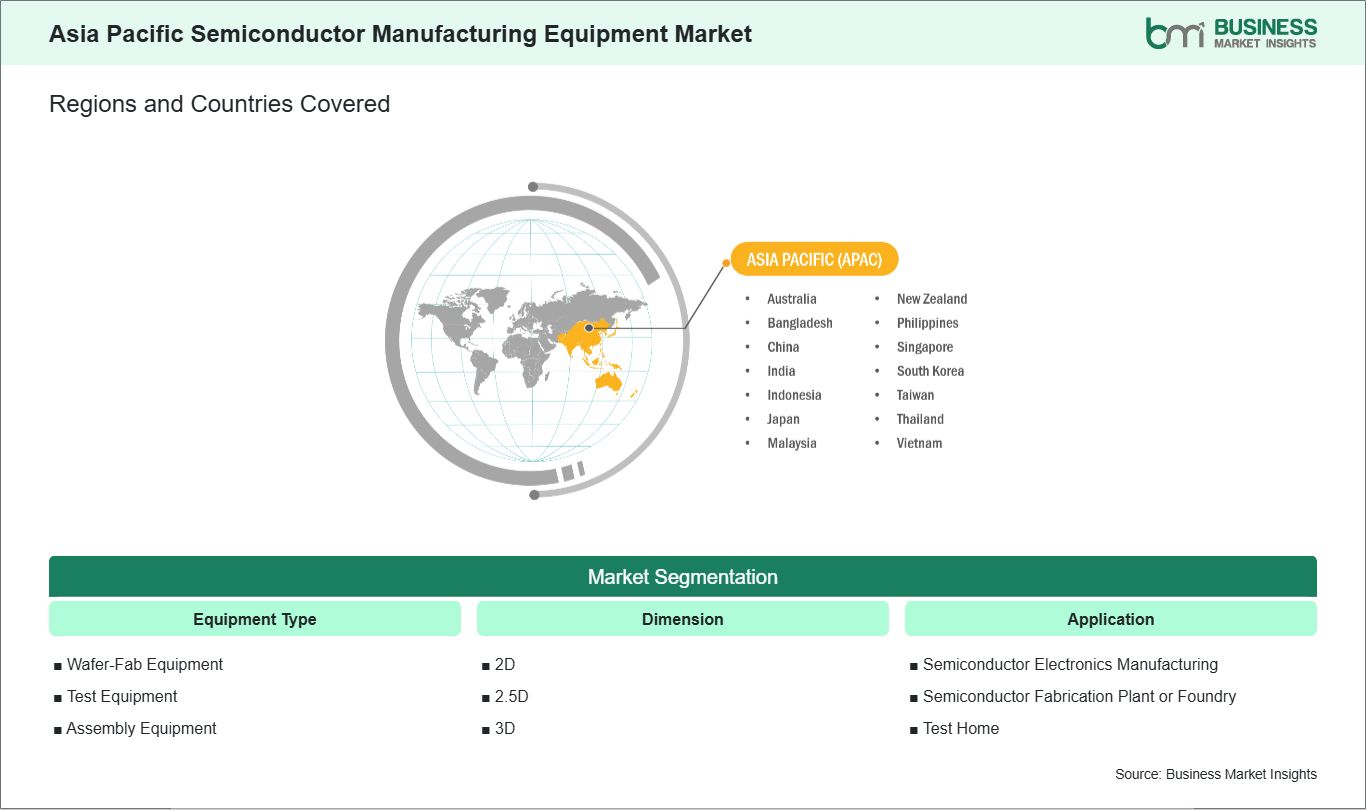

Key segments that contributed to the derivation of the Asia Pacific semiconductor manufacturing equipment market analysis are equipment type, dimension, and application.

By equipment type, the Asia Pacific semiconductor manufacturing equipment market is bifurcated into wafer-fab equipment, test equipment, and assembly equipment. The wafer-fab equipment segment dominated the market in 2025.

By dimension, the market is segmented into 2D, 2.5D, and 3D. The 2D segment held the largest share of the market in 2025.

By application, the market is segmented into semiconductor electronics manufacturing, semiconductor fabrication plant/foundry, and test home. The semiconductor electronics manufacturing segment held the largest share of the market in 2025.

Asia Pacific Semiconductor Manufacturing Equipment Market Drivers and Opportunities:

Expansion of Mega Foundries

The expansion of mega‑foundries across Asia Pacific is a pivotal driver of growth in the semiconductor manufacturing equipment market. Countries such as China, Taiwan, South Korea, and increasingly Japan and Singapore, are aggressively investing in large‑scale fabrication facilities to meet booming global demand for advanced chips in AI, 5G, automotive, and IoT applications. This expansion requires substantial capital expenditure on cutting‑edge equipment—from lithography systems to etchers, deposition tools, and metrology solutions—creating sustained demand for OEMs. Government incentives, strategic national policies, and supply chain localization efforts further accelerate capacity build‑outs. Additionally, competition among regional players to achieve technology leadership encourages frequent equipment upgrades and new facility construction. As these mega‑foundries scale up production nodes at 7 nm, 5 nm and beyond, equipment manufacturers benefit from increased orders, long‑term service contracts, and opportunities to co‑innovate with fabricators on specialized tooling and automation, reinforcing Asia Pacific’s centrality in the semiconductor ecosystem.

Next-Gen Lithography Adoption

The adoption of next‑generation lithography technologies—particularly extreme ultraviolet (EUV) and high‑NA EUV—is a key opportunity shaping the semiconductor manufacturing equipment market in Asia Pacific. As global demand shifts toward smaller, more efficient, and powerful integrated circuits, foundries and logic fabs in the region must deploy advanced lithography systems to remain competitive. EUV’s ability to pattern sub‑7 nm structures with high precision unlocks performance gains critical for AI accelerators, high‑performance computing, and mobile processors. Asia Pacific’s robust ecosystem of semiconductor manufacturers, combined with government and private investments in R&D, positions the region as an early adopter of these next‑gen tools. This transition stimulates demand not only for the lithography machines themselves—largely supplied by a few specialized vendors—but also for supporting equipment and software, such as mask inspection, pellicles, and process control solutions. Consequently, suppliers aligned with next‑gen lithography benefit from long growth cycles, premium pricing, and strategic partnerships that embed them deeply into future technology roadmaps.

Asia Pacific Semiconductor Manufacturing Equipment Market Size and Share Analysis:

By equipment type, the Asia Pacific semiconductor manufacturing equipment market is divided into wafer-fab equipment, assembly equipment, and test equipment. The wafer-fab equipment segment dominated the market in 2025. Asia Pacific shows strong wafer-fab equipment adoption, driven by China, South Korea, Taiwan, and Japan. Heavy investments in advanced lithography, etching, and deposition tools support high-volume production for global semiconductor supply chains, while emerging economies are scaling local capacities.

By dimension, the market is segmented into 2D, 2.5D, and 3D. The 2D segment held the largest share of the market in 2025. Asia Pacific leads global 2D adoption due to large-scale manufacturing, smart cities, and rapid digitalization. 2D technologies are critical in electronics, healthcare imaging, logistics automation, and consumer services across both developed and emerging economies.

By application, the market is segmented semiconductor electronics manufacturing, semiconductor fabrication plant/foundry, and test home. The semiconductor electronics manufacturing segment held the largest share of the market in 2025. Asia Pacific dominates semiconductor electronics manufacturing with extensive fabrication, packaging, and supply-chain integration. Strong demand from consumer electronics, 5G, automotive, and AI technologies, supported by government incentives, positions the region as the global manufacturing powerhouse.

Asia Pacific Semiconductor Manufacturing Equipment Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 91.35 Billion

Market Size by 2033

US$ 196.03 Billion

CAGR (2026 - 2033)

8.7%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Equipment Type

Wafer-Fab Equipment

Test Equipment

Assembly Equipment

By Dimension

2D

2.5D

3D

By Application

Semiconductor Electronics Manufacturing

Semiconductor Fabrication Plant or Foundry

Test Home

Regions and Countries Covered

Asia Pacific

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

Market leaders and key company profiles

KLA Corp

Advantest Corp

Applied Materials Inc

ASML Holding NV

Lam Research Corp

Tokyo Electron Ltd

Hitachi High-Tech Corp

Teradyne Inc

ASMPT Ltd

KOKUSAI ELECTRIC CORPORATION

Get more information on this report

Asia Pacific Semiconductor Manufacturing Equipment Market Report Coverage and Deliverables:

The "Asia Pacific Semiconductor Manufacturing Equipment Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Asia Pacific semiconductor manufacturing equipment market size and forecast at regional, and country levels for all the key market segments covered under the scope

Asia Pacific semiconductor manufacturing equipment market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Asia Pacific semiconductor manufacturing equipment market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the air circuit breaker market

Detailed company profiles, including SWOT analysis

Asia Pacific Semiconductor Manufacturing Equipment Market Geographic Insights:

The geographical scope of the Asia Pacific semiconductor manufacturing equipment market report is expected to grow significantly during the forecast period.

The demand for semiconductor manufacturing equipment in the Asia Pacific region has been rapidly increasing due to several interrelated factors. First, the region is home to some of the world’s largest semiconductor producers, such as Taiwan, South Korea, and China, which continuously invest in advanced fabrication facilities to meet global chip demand. Second, the growing adoption of emerging technologies—including 5G, artificial intelligence, Internet of Things (IoT), and electric vehicles—has significantly amplified the need for high-performance semiconductors, driving expansion in production capacity. Third, government initiatives and incentives in countries like China, Japan, and South Korea to boost domestic semiconductor manufacturing have encouraged investments in state-of-the-art equipment. Additionally, the ongoing global chip shortage has highlighted the strategic importance of localizing semiconductor production, prompting companies to modernize and expand their fabs. Collectively, these factors are fueling robust growth in the semiconductor manufacturing equipment market across Asia Pacific, making it a critical hub for global chip production.

Get more information on this report

Asia Pacific Semiconductor Manufacturing Equipment Market Research Report Guidance:

The report includes qualitative and quantitative data in the Asia Pacific semiconductor manufacturing equipment market across equipment type, dimension, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the semiconductor manufacturing equipment market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Asia Pacific semiconductor manufacturing equipment market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Asia Pacific semiconductor manufacturing equipment market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover Asia Pacific semiconductor manufacturing equipment market segments by equipment type, dimension, application, and geography. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Semiconductor manufacturing equipment market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Asia Pacific Semiconductor Manufacturing Equipment Market News and Key Development:

The Asia Pacific semiconductor manufacturing equipment market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Asia Pacific semiconductor manufacturing equipment market are:

For instance, on October, 2025, Applied Materials, Inc. introduced new semiconductor manufacturing systems that enhance the performance of advanced logic and memory chips, which are foundational to AI computing. The new products target three critical areas in the race to deliver ever more powerful AI chips: leading-edge logic including Gate-All-Around (GAA) transistors, high-performance DRAM including high-bandwidth memory (HBM), and advanced packaging to create highly integrated systems-in-a-package that optimize chip performance, power consumption and cost.

For instance, in February 2025, Advantest Corporation announced that it had entered into a partnership agreement with Micronics Japan Co., Ltd. (“MJC”). As semiconductors are expected to become increasingly advanced and complex, close collaboration within the semiconductor supply chain is essential to meet future market demands. Under this agreement, MJC and Advantest will leverage their respective expertise to provide innovative semiconductor test solutions, contributing to the optimization of customers' test processes and test costs. Additionally, Advantest plans to acquire a minority stake in MJC as part of this agreement.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

Identical Market Reports with other Region/Countries

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Asia Pacific Semiconductor Manufacturing Equipment Market?

The Asia Pacific Semiconductor Manufacturing Equipment Market is valued at US$ 91.35 Billion in 2025, it is projected to reach US$ 196.03 Billion by 2033.

What is the CAGR for Asia Pacific Semiconductor Manufacturing Equipment Market by (2026 - 2033)?

As per our report Asia Pacific Semiconductor Manufacturing Equipment Market, the market size is valued at US$ 91.35 Billion in 2025, projecting it to reach US$ 196.03 Billion by 2033. This translates to a CAGR of approximately 8.7% during the forecast period.

What segments are covered in this report?

The Asia Pacific Semiconductor Manufacturing Equipment Market report typically cover these key segments-

Equipment Type (Wafer-Fab Equipment, Test Equipment, Assembly Equipment)

Dimension (2D, 2.5D, 3D)

Application (Semiconductor Electronics Manufacturing, Semiconductor Fabrication Plant or Foundry, Test Home)

What is the historic period, base year, and forecast period taken for Asia Pacific Semiconductor Manufacturing Equipment Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Semiconductor Manufacturing Equipment Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Asia Pacific Semiconductor Manufacturing Equipment Market?

The Asia Pacific Semiconductor Manufacturing Equipment Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

KLA Corp

Advantest Corp

Applied Materials Inc

ASML Holding NV

Lam Research Corp

Tokyo Electron Ltd

Hitachi High-Tech Corp

Teradyne Inc

ASMPT Ltd

KOKUSAI ELECTRIC CORPORATION

Who should buy this report?

The Asia Pacific Semiconductor Manufacturing Equipment Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Asia Pacific Semiconductor Manufacturing Equipment Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Asia Pacific Semiconductor Manufacturing Equipment Market

Get Free Sample For Asia Pacific Semiconductor Manufacturing Equipment Market