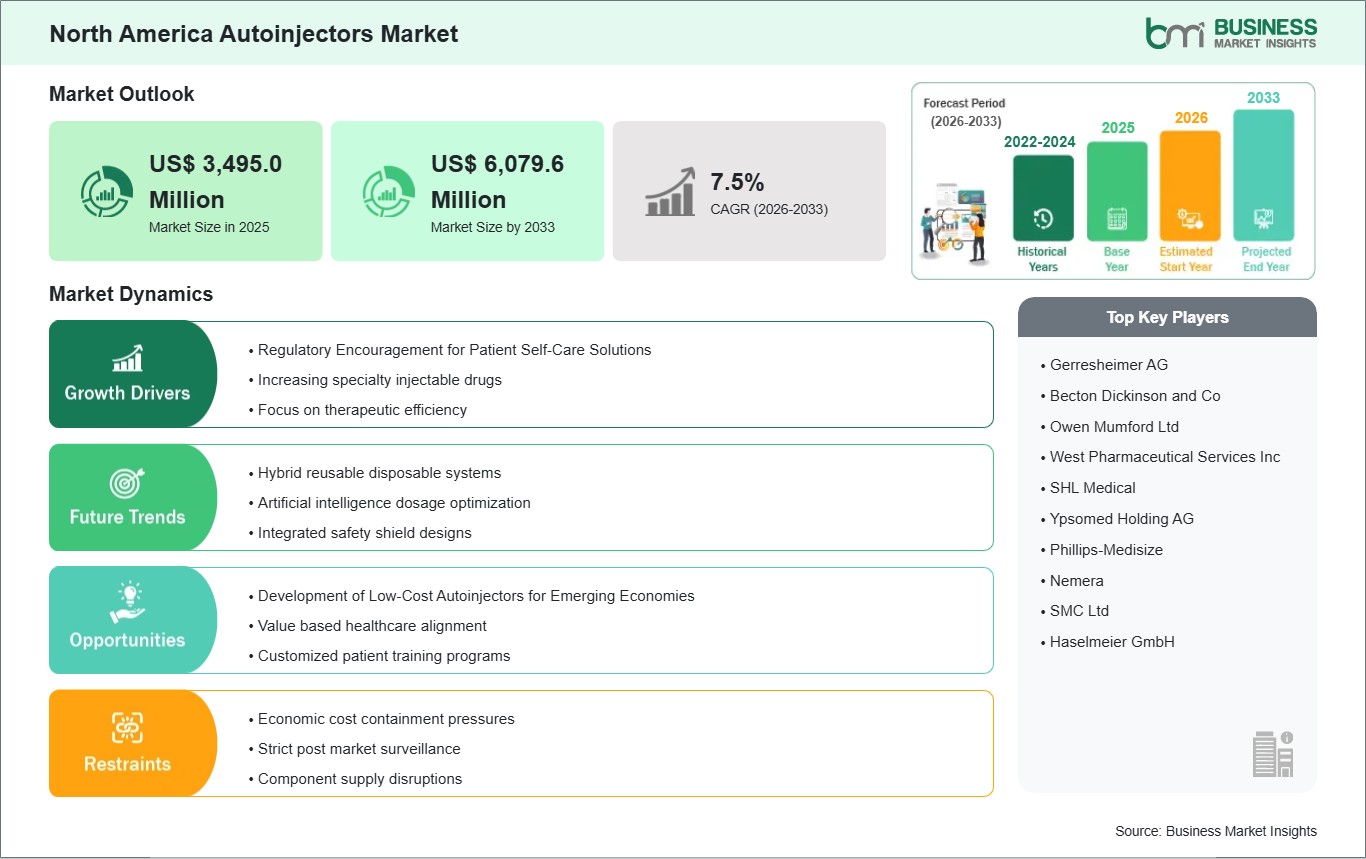

The North America Autoinjectors Market size is expected to reach US$ 6,079.6 million by 2033 from US$ 3,495.0 million in 2025. The market is estimated to record a CAGR of 7.5% from 2026 to 2033.

Executive Summary and North America Autoinjectors Market Analysis:

The North America autoinjectors market demonstrates a structurally strong growth trajectory driven by rising chronic disease prevalence, increasing biologics adoption, and expanding patient-centric drug delivery models. Autoinjectors are becoming integral to therapeutic areas such as autoimmune disorders, anaphylaxis, multiple sclerosis, and rheumatoid arthritis, where self-administration improves adherence and clinical outcomes. Regulatory support from agencies such as the U.S. Food and Drug Administration has accelerated approvals for combination products, encouraging pharmaceutical manufacturers to integrate device innovation early in drug development pipelines. Market competition is intensifying as established medical device companies and specialty drug manufacturers pursue differentiation through ergonomic design, safety mechanisms, and connectivity-enabled smart autoinjectors. Strategic collaborations between biotechnology firms and device engineering companies are reshaping commercialization models, emphasizing lifecycle management and value-added services. Additionally, payer pressure across the region is influencing product positioning, with emphasis on cost-efficient drug delivery systems that reduce hospital visits and nursing dependency. Supply chain resilience and localized manufacturing investments are emerging as strategic priorities, particularly in response to geopolitical volatility and raw material constraints. Sustainability considerations, including recyclable components and reduced plastic content, are increasingly influencing procurement decisions among institutional buyers. Overall, the market is transitioning from volume-driven expansion to value-driven innovation, where device reliability, patient usability, and digital integration form key competitive differentiators.

North America Autoinjectors Market - Strategic Insights:

Get more information on this report

North America Autoinjectors Market Segmentation Analysis:

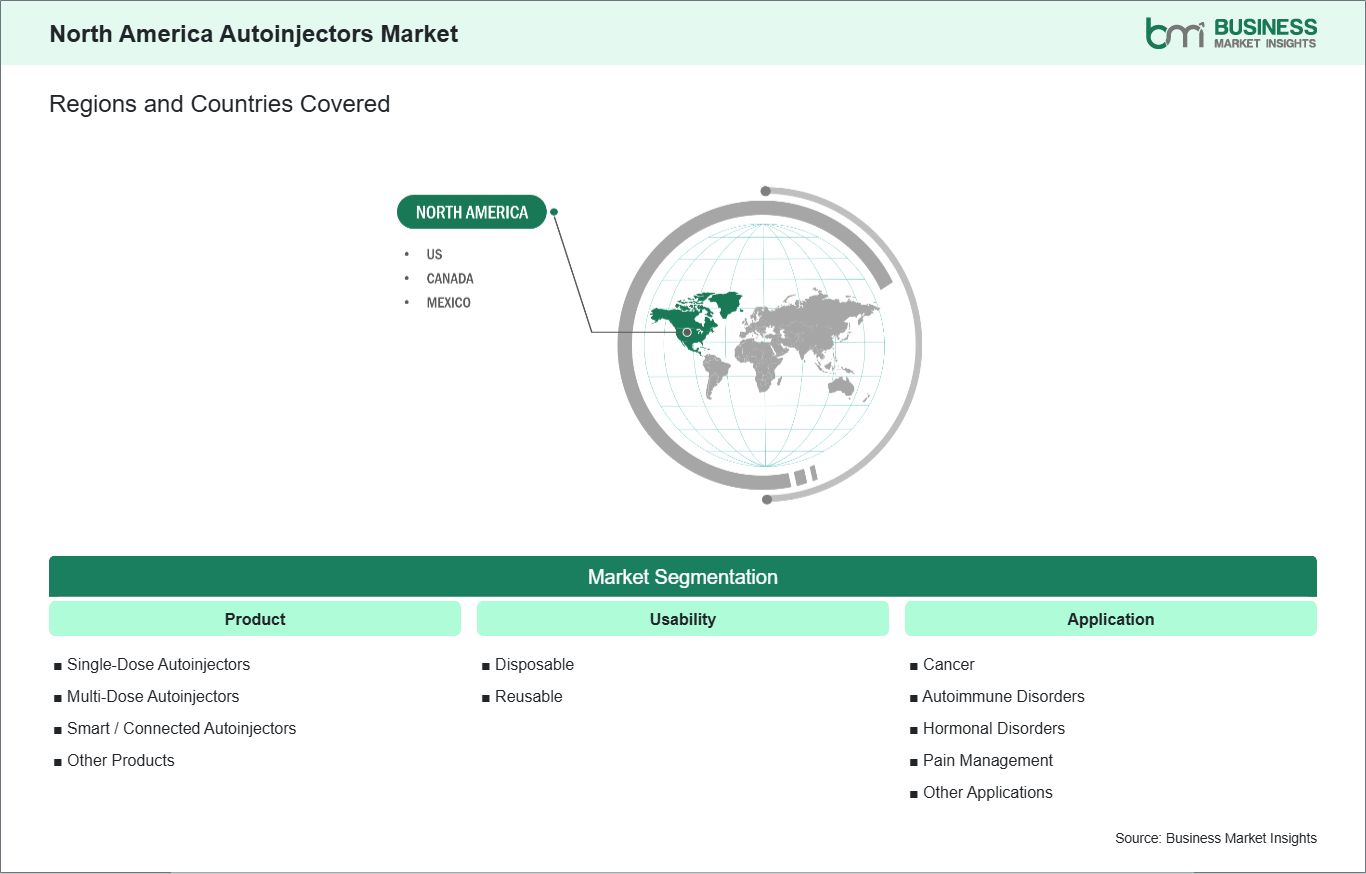

Key segments that contributed to the derivation of the North America autoinjectors market analysis are product, usability, and application.

By product, the autoinjectors market is segmented into single-dose autoinjectors, multi-dose autoinjectors, smart / connected autoinjectors, and others. The single-dose autoinjectors segment dominated the market in 2025.

Based on usability, the autoinjectors market is categorized into disposable and reusable. The disposable segment dominated the market in 2025.

In terms of application, the market is classified into cancer, autoimmune disorders, hormonal disorders, pain management, and other applications. The autoimmune disorders segment dominated the market in 2025.

North America Autoinjectors Market Drivers and Opportunities:

Regulatory Encouragement for Patient Self-Care Solutions

North America’s autoinjectors market has been significantly shaped by proactive regulatory frameworks that encourage self-care and at-home administration of injectable therapies. In the United States, the U.S. Food and Drug Administration (FDA) has clarified regulatory pathways for combination drug-device products that include autoinjectors, making it easier for developers to bring user-centric designs to market. Guidance documents emphasize human factors engineering and ease-of-use for lay users, reflecting a broader policy goal of reducing burden on healthcare facilities and empowering patients to self-manage chronic conditions like rheumatoid arthritis and multiple sclerosis. This regulatory clarity has influenced nearly all major product launches in the U.S. over the past five years, leading to a growing portfolio of FDA-cleared autoinjectors capable of supporting self-administration outside of clinical settings. Parallel to FDA efforts, payer policies in the U.S. including Medicare and major private insurers — have adapted coverage to support at-home autoinjector use. Recent reimbursement updates now include specific billing codes for patient education and remote training on autoinjector use, which helps clinicians justify prescribing home-use devices instead of clinic-administered injections. These reimbursement shifts directly affect adoption rates: a 2025 payer report highlighted a double-digit increase in claims for autoinjector devices across self-administered biologics compared with 2020, underscoring how aligned policy and reimbursement can drive market expansion within North America. In Canada, Health Canada and provincial health authorities have taken complementary steps to expand self-care solutions. Federal regulatory reviews have streamlined reviews of injection device modifications, enabling faster entry for improved autoinjector designs for conditions such as severe allergies and chronic inflammatory diseases. Provincial formularies in Ontario and Alberta increasingly list autoinjectors as preferred devices for first-line biologic therapies, encouraging use outside hospitals and clinics. Across North America, including Mexico, there is growing alignment between regulatory encouragement and health system priorities, such as reducing hospital congestion and supporting remote or rural patient populations with safe, self-administered solutions.

Development of Low-Cost Autoinjectors for Emerging Economies

Even within the high-income context of North America, there is focused innovation around lower-cost autoinjector solutions, driven by rising healthcare costs, insurance coverage variability, and equity concerns among underserved populations. In the United States, out-of-pocket costs for branded autoinjectors — particularly emergency epinephrine devices — have become a significant barrier for many patients. As a result, major device manufacturers are developing simplified, disposable autoinjector platforms that reduce manufacturing complexity and offer lower list prices while maintaining safety. For example, competitive bidding and value-based contracting with pharmacy benefit managers have led to generic epinephrine autoinjectors entering U.S. distribution at substantially reduced prices compared to legacy products, increasing accessibility for patients without comprehensive coverage. Beyond epinephrine, biologic therapies administered via autoinjectors for conditions like psoriasis and Crohn’s disease are also seeing cost-focused innovation. Several North American medtech companies have redesigned components — such as reducing the number of precision parts and adopting injection-assist technologies — to bring overall device costs down without sacrificing performance. These initiatives are targeted specifically at segments of the U.S. population where high copays and tiered formularies have previously limited adoption. Clinical advisors report that simpler, lower-cost autoinjector options have improved adherence rates in underinsured patient groups, demonstrating how cost reduction within the North American market itself is a key growth driver. In Canada and Mexico, cost considerations also influence procurement decisions for provincial health systems and national insurers. Canadian provinces with publicly funded healthcare increasingly negotiate bulk pricing for autoinjectors, including generics and simplified designs, to manage budget pressures while maintaining broad patient access. In Mexico, where private insurance penetration is lower and out-of-pocket spend is higher, manufacturers with lower-cost autoinjector offerings have seen faster uptake among hospital systems and outpatient clinics, especially for chronic disease management. These market pressures in North America — from high cost burdens in the U.S. to public procurement strategies in Canada and Mexico — ensure that low-cost autoinjector development remains a priority not for emerging markets abroad, but for addressing affordability and access within the region itself.

North America Autoinjectors Market Size and Share Analysis:

The North America Autoinjectors Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, usability, and application, offering insights into their contribution to overall market performance.

By product, the single-dose autoinjectors subsegment dominated the market in 2025, driven by strong patient preference for ready-to-use, pre-filled delivery formats that simplify self-administration and reduce dosing errors, particularly in chronic and emergency therapies where convenience and accuracy are critical.

Based on usability, the disposable subsegment dominated the market in 2025, driven by the widespread adoption of pre-filled, single-use devices that enhance safety (reducing cross-contamination and infection risk), require no maintenance, and align with home-care and chronic disease management needs.

In terms of application, the autoimmune disorders subsegment dominated the market in 2025, driven by the rising prevalence of autoimmune conditions (such as rheumatoid arthritis and multiple sclerosis) that rely on biologic therapies optimally delivered via autoinjectors for precise dosing and improved patient compliance.

North America Autoinjectors Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 3,495.0 Million

Market Size by 2033

US$ 6,079.6 Million

CAGR (2026 - 2033)

7.5%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Single-Dose Autoinjectors

Multi-Dose Autoinjectors

Smart / Connected Autoinjectors

Other Products

By Usability

Disposable

Reusable

By Application

Cancer

Autoimmune Disorders

Hormonal Disorders

Pain Management

Other Applications

Regions and Countries Covered

North America

US, Canada, Mexico

Market leaders and key company profiles

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd

West Pharmaceutical Services Inc

SHL Medical

Ypsomed Holding AG

Phillips-Medisize

Nemera

SMC Ltd

Haselmeier GmbH

Get more information on this report

North America Autoinjectors Market Report Coverage and Deliverables:

The "North America Autoinjectors Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

North America Autoinjectors Market size and forecast at regional and country levels for all market segments covered under the scope

North America Autoinjectors Market trends, as well as drivers, restraints, and opportunities

North America Autoinjectors Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the North America Autoinjectors Market

Detailed company profiles, including SWOT analysis

North America Autoinjectors Market Geographic Insights:

The geographical scope of the North America Autoinjectors Market report is divided into United States, Canada, and Mexico. US held the largest share in 2025.

Country-level dynamics within North America reveal differentiated growth drivers and regulatory environments. The United States remains the most innovation-intensive market, supported by a strong biotechnology ecosystem and advanced healthcare infrastructure. Institutional procurement through hospital systems and specialty clinics contributes significantly to demand, while direct-to-consumer awareness campaigns amplify adoption of emergency-use autoinjectors. Canada presents a distinct reimbursement landscape shaped by provincial healthcare systems, fostering structured formulary evaluations and price negotiations. Health technology assessment agencies emphasize cost-effectiveness and long-term therapeutic value, influencing device selection criteria. Meanwhile, Mexico is emerging as a developing opportunity market, driven by expanding private healthcare investments and improving biologics penetration. Regulatory oversight by entities such as Health Canada and Federal Commission for the Protection against Sanitary Risk ensures compliance with safety and quality standards, though approval timelines and documentation requirements vary across jurisdictions. Cross-border trade agreements and regional manufacturing partnerships are supporting supply continuity and reducing dependency on overseas imports. Additionally, demographic variations—such as aging populations in the United States and Canada versus a younger but increasingly urbanized population in Mexico—shape disease prevalence patterns and product demand profiles. Collectively, these country-specific factors create a heterogeneous yet strategically interconnected regional market landscape.

Get more information on this report

North America Autoinjectors Market Research Report Guidance:

The report includes qualitative and quantitative data in the North America Autoinjectors Market across product, usability, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the North America Autoinjectors Market.

Chapter 3 focuses on the research smethodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the North America Autoinjectors Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the North America Autoinjectors Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover North America Autoinjectors Market segments by product, usability, application, and geography across United States, Canada, and Mexico. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the North America Autoinjectors Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

North America Autoinjectors Market News and Key Development:

The North America Autoinjectors Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the North America autoinjectors market are:

In June 2025, The U.S. Food and Drug Administration (FDA) granted approval for a 200 mg/mL belimumab autoinjector (Benlysta) for pediatric lupus nephritis patients aged ≥5 years. This approval allows at-home subcutaneous administration of belimumab, reducing the need for clinic infusions and improving accessibility for families.

In May 2025, The FDA approved Brekiya’s DHE autoinjector formulation for acute migraine and cluster headache, marking the first autoinjector option for this indication. This regulatory milestone enables broader patient self-administration for severe headache episodes and supports expanded therapeutic uses of autoinjector devices in North America.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - North America Autoinjectors Market

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd

West Pharmaceutical Services Inc

SHL Medical

Ypsomed Holding AG

Phillips-Medisize

Nemera

SMC Ltd

Haselmeier GmbH

Frequently Asked Questions

How big is the North America Autoinjectors Market?

The North America Autoinjectors Market is valued at US$ 3,495.0 Million in 2025, it is projected to reach US$ 6,079.6 Million by 2033.

What is the CAGR for North America Autoinjectors Market by (2026 - 2033)?

As per our report North America Autoinjectors Market, the market size is valued at US$ 3,495.0 Million in 2025, projecting it to reach US$ 6,079.6 Million by 2033. This translates to a CAGR of approximately 7.5% during the forecast period.

What segments are covered in this report?

The North America Autoinjectors Market report typically cover these key segments-

Application (Cancer, Autoimmune Disorders, Hormonal Disorders, Pain Management, Other Applications)

What is the historic period, base year, and forecast period taken for North America Autoinjectors Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Autoinjectors Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in North America Autoinjectors Market?

The North America Autoinjectors Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd

West Pharmaceutical Services Inc

SHL Medical

Ypsomed Holding AG

Phillips-Medisize

Nemera

SMC Ltd

Haselmeier GmbH

Who should buy this report?

The North America Autoinjectors Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the North America Autoinjectors Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For North America Autoinjectors Market

Get Free Sample For North America Autoinjectors Market