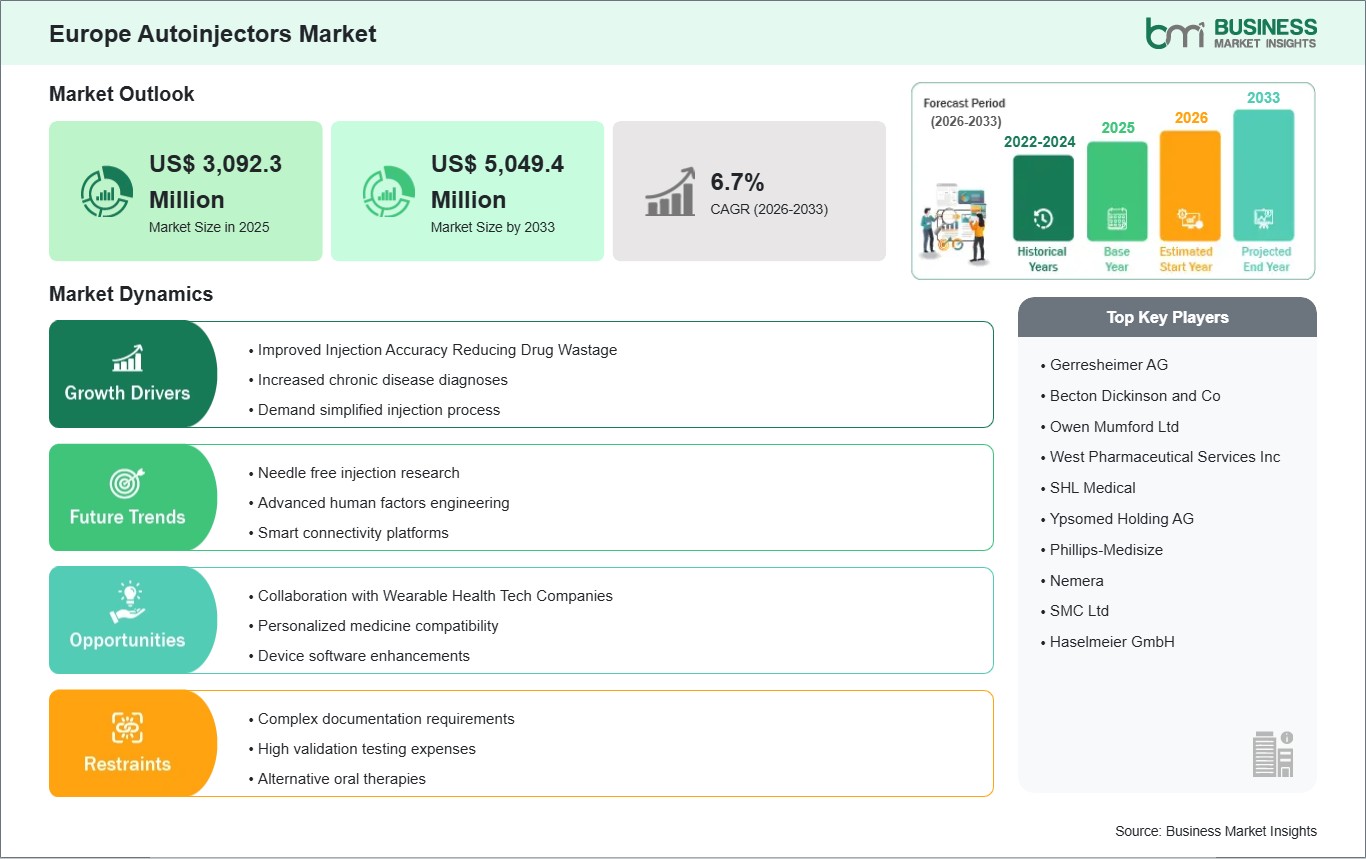

The Europe Autoinjectors Market size is expected to reach US$ 5,049.4 million by 2033 from US$ 3,092.3 million in 2025. The market is estimated to record a CAGR of 6.7% from 2026 to 2033.

Executive Summary and Europe Autoinjectors Market Analysis:

The Europe autoinjectors market is experiencing steady growth, underpinned by the region’s advanced healthcare infrastructure, high patient awareness, and strong reimbursement frameworks. The market spans Western, Central, and Eastern Europe, with countries such as Germany, France, Italy, and the UK, alongside emerging Eastern European nations, collectively driving adoption. Increasing prevalence of chronic diseases, autoimmune disorders, severe allergies, and the widespread use of biologics has accentuated the need for convenient and accurate drug delivery systems. Autoinjectors are increasingly preferred due to their ability to enhance patient adherence, reduce injection errors, and offer the convenience of self-administration in homecare settings. The competitive landscape is dominated by global medical device manufacturers, though regional players are entering through licensing, co-development, or localized assembly partnerships. Product innovation remains a key differentiator, with focus areas including ergonomic designs, dual-chamber systems, prefilled formulations, and connected devices enabling digital adherence monitoring. Regulatory compliance under the European Union’s Medical Device Regulation (MDR) ensures high safety and quality standards, although market entry requires robust clinical validation and extensive documentation, particularly for novel devices. Distribution channels are shifting from hospital-centric models toward a more diversified approach, incorporating retail pharmacies, specialty clinics, and digital platforms. Health insurers and national reimbursement programs play a pivotal role in accelerating adoption, particularly for high-cost biologics requiring autoinjector delivery. In addition, patient education and training initiatives have strengthened acceptance, allowing a wider demographic—including pediatric and geriatric populations—to adopt self-injection therapies. Overall, the Europe autoinjectors market demonstrates a strong alignment between technological innovation, regulatory rigor, and patient-centric care, creating a conducive environment for sustainable growth across multiple therapeutic areas.

Europe Autoinjectors Market - Strategic Insights:

Get more information on this report

Europe Autoinjectors Market Segmentation Analysis:

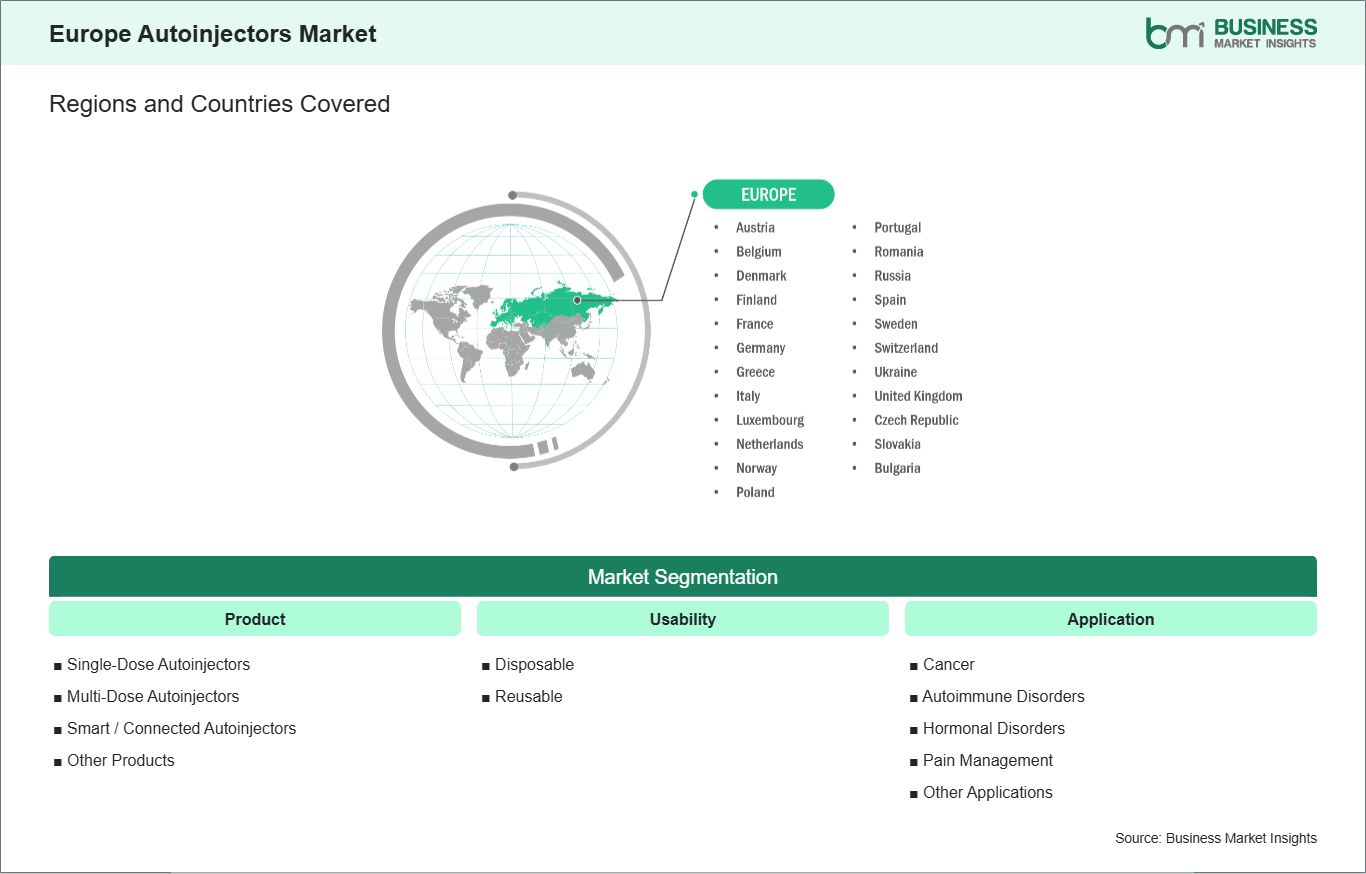

Key segments that contributed to the derivation of the Europe autoinjectors market analysis are product, usability, and application.

By product, the autoinjectors market is segmented into single-dose autoinjectors, multi-dose autoinjectors, smart / connected autoinjectors, and others. The single-dose autoinjectors segment dominated the market in 2025.

Based on usability, the autoinjectors market is categorized into disposable and reusable. The disposable segment dominated the market in 2025.

In terms of application, the market is classified into cancer, autoimmune disorders, hormonal disorders, pain management, and other applications. The autoimmune disorders segment dominated the market in 2025.

Europe Autoinjectors Market Drivers and Opportunities:

Improved Injection Accuracy Reducing Drug Wastage

Across Europe, rising pharmaceutical costs and tighter reimbursement frameworks are driving demand for autoinjector technologies that improve injection accuracy and minimize drug wastage. In high‑cost healthcare systems such as those in Western Europe, biologic therapies for conditions like rheumatoid arthritis, multiple sclerosis, and Crohn’s disease represent substantial per‑dose expenditure. Clinics in major metropolitan centers from Paris to Frankfurt increasingly prefer autoinjectors with precise dose delivery mechanisms because they ensure the full therapeutic load is administered, reducing waste and lowering both payer and patient costs. This trend aligns closely with hospital pharmacy initiatives aimed at optimizing drug utilization and lowering overall supply spend without compromising outcomes. In Northern European countries where stringent hospital budgeting frameworks are common, improved accuracy features — such as spring‑assisted delivery and integrated dose confirmation — are helping healthcare providers meet both economic and clinical objectives. Pharmacies in cities like Stockholm and Copenhagen report that devices with audible or visual delivery indicators reduce accidental partial doses, which historically have led to reduced efficacy and increased repeat visits. As reimbursement authorities increasingly tie coverage to demonstrable cost‑effectiveness, the ability of autoinjectors to mitigate wastage strengthens their value proposition in formulary decisions. Central European markets are also recognizing the economic impact of accurate delivery systems. Clinics in Vienna and Munich are transitioning away from manual syringe systems toward engineered autoinjectors for high‑price biologics, citing lower liability risk and fewer adverse events linked to dosing errors. Educational programs for nurse specialists emphasize how consistent dose administration drives better long‑term management of chronic diseases and aligns with broader EU health policy goals of resource optimization. Together, these dynamics indicate that enhanced injection accuracy — and the associated reduction in drug wastage is a growing decision criterion shaping autoinjector procurement across Europe.

Collaboration with Wearable Health Tech Companies

In Europe’s increasingly digital health ecosystem, collaboration between autoinjector manufacturers and wearable health technology companies is gaining momentum as stakeholders seek to integrate medication delivery with real‑time monitoring and data analytics. Multi‑disciplinary pilot programs in cities like Amsterdam and Barcelona are linking autoinjectors to smartphone applications and wearable sensors that track activity, vitals, and dosing history. These combined systems provide clinicians with a comprehensive view of patient adherence and therapeutic response, enabling more informed treatment adjustments and improving chronic disease management outcomes. Healthcare providers in Scandinavia are early adopters of these integrated solutions. Through partnerships with local wearable health tech companies, Danish and Finnish health networks are offering autoinjector users companion devices that sync injection events with biometric data such as heart rate variability and sleep patterns. Patients managing autoimmune conditions have responded positively to platforms that contextualize dosing within their broader health profile, reducing uncertainty and enhancing engagement. These developments are also supported by national health registries that promote interoperability and standardized data sharing across digital health tools. Central and Eastern European healthcare systems are beginning to pilot connected autoinjector ecosystems that link wearable devices with electronic medical records (EMRs). Clinics in Prague and Warsaw are exploring solutions where data from wearable patches and autoinjector logs are automatically uploaded to EMRs, enabling multidisciplinary care teams to review adherence trends during routine consultations. Integration with telehealth platforms further allows remote monitoring, a capability that has proven valuable in regions with dispersed populations. As European healthcare funders increasingly emphasize digital health as a pathway to improved efficiency and patient outcomes, collaboration between autoinjector providers and wearable tech companies is poised to become a defining feature of the continent’s evolving autoinjector market.

Europe Autoinjectors Market Size and Share Analysis:

The Europe Autoinjectors Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, usability, and application, offering insights into their contribution to overall market performance.

By product, the single-dose autoinjectors subsegment dominated the market in 2025, driven by preference for ready‑to‑use, pre‑filled devices that reduce contamination risks and improve dosing accuracy for patients and healthcare providers.

Based on usability, the disposable subsegment dominated the market in 2025, driven by strong demand for simple, single‑use delivery systems that enhance safety, eliminate maintenance, and support home‑based treatment models.

In terms of application, the autoimmune disorders subsegment dominated the market in 2025, driven by rising prevalence of chronic immune‑mediated conditions (e.g., rheumatoid arthritis, multiple sclerosis) requiring long‑term biologic therapies optimally administered via autoinjectors.

Europe Autoinjectors Market Report Coverage and Deliverables:

The "Europe Autoinjectors Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Europe Autoinjectors Market size and forecast at regional and country levels for all market segments covered under the scope

Europe Autoinjectors Market trends, as well as drivers, restraints, and opportunities

Europe Autoinjectors Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Europe Autoinjectors Market

Detailed company profiles, including SWOT analysis

Europe Autoinjectors Market Geographic Insights:

The geographical scope of the Europe Autoinjectors Market report is divided into Belgium, Austria, Finland, Denmark, Greece, Poland, Romania, Russia, Ukraine, the Czech Republic, Slovakia, Bulgaria, Italy, Luxembourg, Germany, Switzerland, France, the Netherlands, Norway, Portugal, Spain, Sweden, and the UK. Germany held the largest share in 2025.

Country-specific dynamics across Europe reveal diverse adoption patterns and strategic opportunities. Germany is a mature, innovation-driven market with strong hospital networks, high insurance coverage, and early adoption of smart autoinjectors for chronic disease management. The market is characterized by rigorous regulatory oversight, which ensures high-quality standards for both local and imported devices. In France, patient-centric care models and government-supported reimbursement schemes drive the adoption of self-administered biologics, with hospitals and specialty clinics serving as primary distribution points. Italy demonstrates a similar trend, with growing urban adoption of autoinjectors complemented by private healthcare expansion and patient training programs. Emerging Eastern European markets, including Poland, Czech Republic, and Romania, are characterized by gradual uptake influenced by public reimbursement policies, urban-rural healthcare disparities, and increasing private sector involvement. Pricing sensitivity remains a key factor, requiring affordable, user-friendly devices alongside patient education campaigns. Spain reflects a mixed market where private hospital adoption of advanced autoinjectors coexists with cost-conscious public sector procurement, highlighting opportunities for both premium and economy product segments. Collectively, these country-specific insights emphasize the need for differentiated strategies, adaptive pricing frameworks, and digital integration to effectively capture growth opportunities across the European autoinjectors market.

Get more information on this report

Europe Autoinjectors Market Research Report Guidance:

The report includes qualitative and quantitative data in the Europe Autoinjectors Market across product, usability, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Europe Autoinjectors Market.

Chapter 3 focuses on the research smethodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Europe Autoinjectors Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Europe Autoinjectors Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Europe Autoinjectors Market segments by product, usability, application, and geography across Belgium, Austria, Finland, Denmark, Greece, Poland, Romania, Russia, Ukraine, the Czech Republic, Slovakia, Bulgaria, Italy, Luxembourg, Germany, Switzerland, France, the Netherlands, Norway, Portugal, Spain, Sweden, and the UK. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Europe Autoinjectors Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Europe Autoinjectors Market News and Key Development:

The Europe Autoinjectors Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Europe autoinjectors market are:

In January 2026, SHL Medical showcased new autoinjector technologies (including its Reunite and an upcoming autoinjector) at Pharmapack Europe 2026 alongside partners such as SCHOTT Pharma and Team Consulting, highlighting strategic collaboration in combination product innovation. The event spotlighted co‑presentations that emphasised how partnerships advance self‑injection device development and patient usability. This collaboration underscores shared industry efforts to broaden Europe’s device portfolio and accelerate innovation. It also reinforces cross‑company synergy in advancing autoinjector technologies for future launches.

In December 2025, Celltrion received a positive CHMP opinion from the European Medicines Agency (EMA) for its SteQeyma ustekinumab biosimilar autoinjector, expanding the Europe portfolio of autoinjector‑delivered biologics. This positive opinion covers multiple dosage strengths and supports ease of self‑administration for chronic inflammatory diseases, signalling likely upcoming EU authorisation. The development broadens treatment options and offers an alternative delivery format that improves patient choice and adherence. This regulatory milestone strengthens competition and innovation in Europe’s self‑injection device market.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - Europe Autoinjectors Market

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd

West Pharmaceutical Services Inc

SHL Medical

Ypsomed Holding AG

Phillips-Medisize

Nemera

SMC Ltd

Haselmeier GmbH

Frequently Asked Questions

How big is the Europe Autoinjectors Market?

The Europe Autoinjectors Market is valued at US$ 3,092.3 Million in 2025, it is projected to reach US$ 5,049.4 Million by 2033.

What is the CAGR for Europe Autoinjectors Market by (2026 - 2033)?

As per our report Europe Autoinjectors Market, the market size is valued at US$ 3,092.3 Million in 2025, projecting it to reach US$ 5,049.4 Million by 2033. This translates to a CAGR of approximately 6.7% during the forecast period.

What segments are covered in this report?

The Europe Autoinjectors Market report typically cover these key segments-

Application (Cancer, Autoimmune Disorders, Hormonal Disorders, Pain Management, Other Applications)

What is the historic period, base year, and forecast period taken for Europe Autoinjectors Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Autoinjectors Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Europe Autoinjectors Market?

The Europe Autoinjectors Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd

West Pharmaceutical Services Inc

SHL Medical

Ypsomed Holding AG

Phillips-Medisize

Nemera

SMC Ltd

Haselmeier GmbH

Who should buy this report?

The Europe Autoinjectors Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Europe Autoinjectors Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Europe Autoinjectors Market

Get Free Sample For Europe Autoinjectors Market