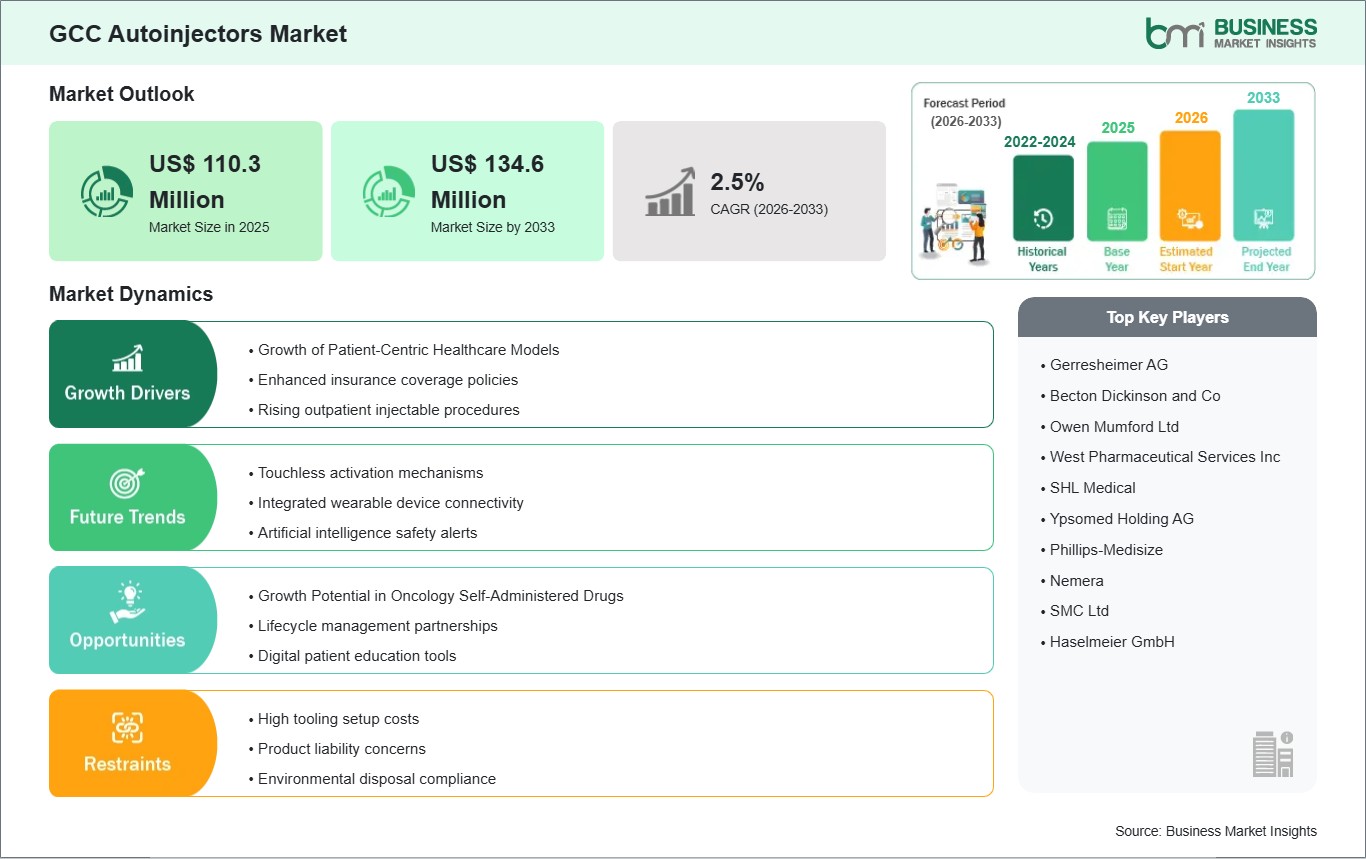

The GCC Autoinjectors Market size is expected to reach US$ 134.6 million by 2033 from US$ 110.3 million in 2025. The market is estimated to record a CAGR of 2.5% from 2026 to 2033.

Executive Summary and GCC Autoinjectors Market Analysis:

The GCC autoinjectors market, covering Saudi Arabia, United Arab Emirates, Kuwait, Qatar, Bahrain, and Oman, is witnessing steady growth, driven by rising prevalence of chronic diseases, increased patient awareness, and government-led healthcare modernization initiatives. The region has seen a surge in cases of diabetes, autoimmune disorders, and severe allergies, which has escalated demand for patient-friendly, prefilled autoinjector devices. Self-administration is increasingly recognized for its benefits, including reduced hospital visits, improved adherence, and enhanced patient autonomy. The competitive landscape is dominated by global medical device manufacturers, though regional pharmaceutical companies are entering via strategic partnerships, co-development agreements, and technology transfer programs. Market differentiation is achieved through innovation in ergonomics, safety features, dual-chamber systems, and digital connectivity, enabling adherence monitoring and remote patient support. Regulatory frameworks in the GCC, while harmonizing gradually under Gulf Cooperation Council Health Regulations, require market entrants to navigate country-specific approval procedures and local clinical validation protocols. Distribution channels are evolving from hospital-centric models toward hybrid approaches that include retail pharmacies, specialty clinics, and emerging e-commerce platforms. Health insurance coverage in countries like Saudi Arabia and the UAE is improving, supporting wider patient access to high-cost biologics delivered via autoinjectors. Furthermore, public awareness campaigns and patient training programs are facilitating adoption, particularly among pediatric and geriatric populations. The GCC autoinjectors market demonstrates a combination of high adoption potential, strong government support, and increasing patient preference for self-care, making it an attractive region for device manufacturers seeking sustainable growth.

GCC Autoinjectors Market - Strategic Insights:

Get more information on this report

GCC Autoinjectors Market Segmentation Analysis:

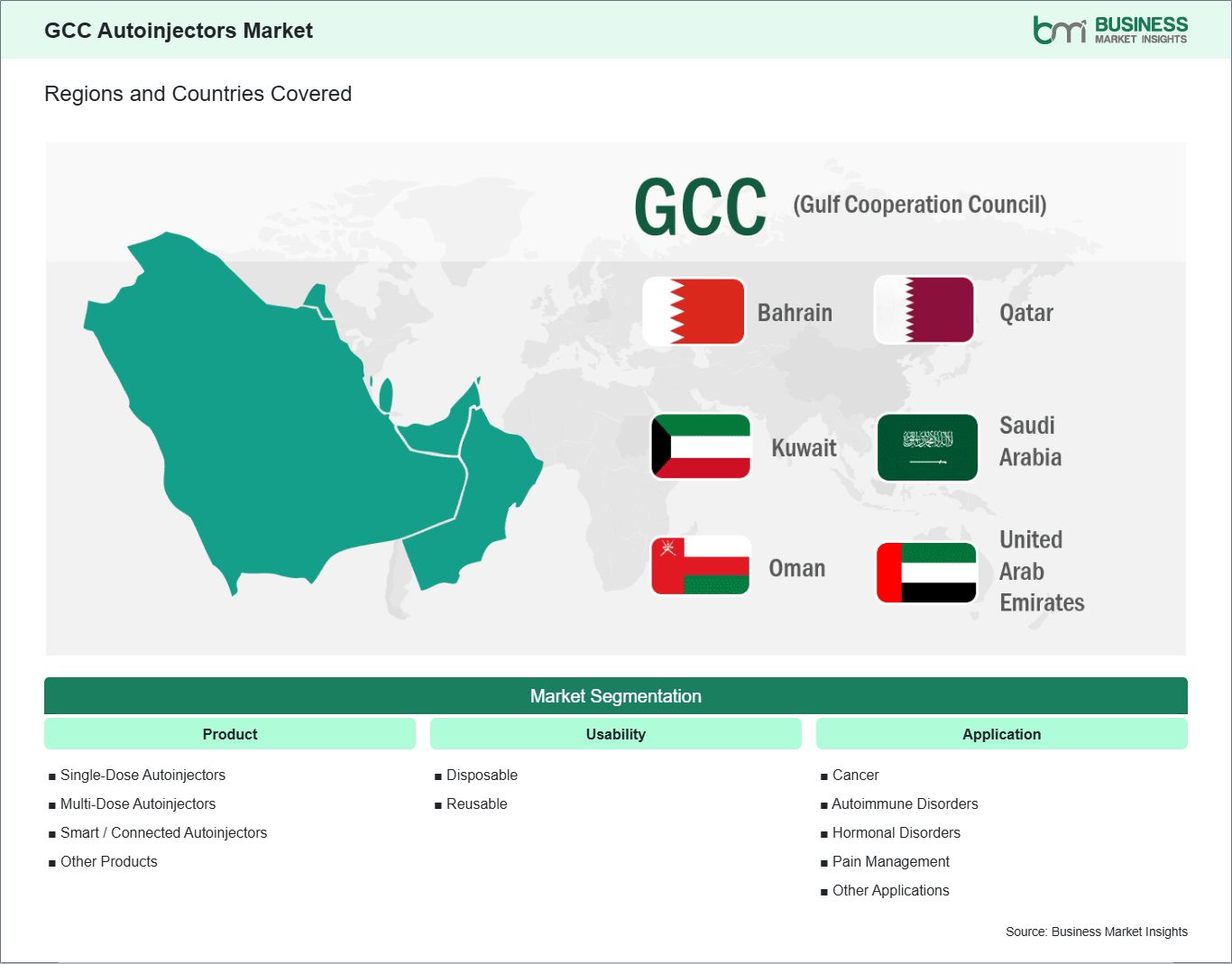

Key segments that contributed to the derivation of the GCC autoinjectors market analysis are product, usability, and application.

By product, the autoinjectors market is segmented into single-dose autoinjectors, multi-dose autoinjectors, smart / connected autoinjectors, and others. The single-dose autoinjectors segment dominated the market in 2025.

Based on usability, the autoinjectors market is categorized into disposable and reusable. The disposable segment dominated the market in 2025.

In terms of application, the market is classified into cancer, autoimmune disorders, hormonal disorders, pain management, and other applications. The autoimmune disorders segment dominated the market in 2025.

GCC Autoinjectors Market Drivers and Opportunities:

Growth of Patient-Centric Healthcare Models

The GCC region is undergoing a significant transformation toward patient‑centric healthcare models, driven by government strategies to diversify healthcare delivery and improve quality of care. In Saudi Arabia’s Vision 2030 health sector reforms, chronic disease management is a priority, and autoinjectors are increasingly recognized as tools that enable patients to administer treatment at home with greater convenience. In Riyadh and Jeddah, outpatient clinics and diabetes centers report rising uptake of autoinjectors for chronic conditions such as rheumatoid arthritis and multiple sclerosis, as physicians seek to empower patients and reduce hospital visit frequency. This shift reflects a broader move toward care models that emphasize autonomy, convenience, and long‑term adherence. In the UAE, patient‑centric models are supported by advanced digital health infrastructures that integrate electronic health records (EHRs) with patient education programs. Clinics in Dubai and Abu Dhabi have implemented initiatives where healthcare providers work closely with patients to select devices that fit individual lifestyles, particularly for self‑injectable biologics. Autoinjectors with features such as intuitive actuation and dose feedback are preferred for their ability to enhance confidence in self‑administration, especially among working adults managing complex treatment regimens. These device choices are increasingly reflected in prescription patterns across private and government health facilities. Furthermore, Qatar’s national health strategy emphasizes personalized care pathways for chronic illnesses, driving adoption of autoinjectors in both urban and semi‑urban settings. Education campaigns coordinated by public health authorities and clinic networks train patients to self‑inject safely, thereby reducing pressure on specialty care units. In Kuwait and Bahrain, enhanced patient support programs — including mobile nurse visits and telehealth follow‑ups — further reinforce the shift to patient‑centric care. Across the GCC, these healthcare models are creating fertile ground for autoinjector market growth, as stakeholders prioritize accessible, comfortable, and safe self‑administration options that improve treatment outcomes.

Growth Potential in Oncology Self-Administered Drugs

The oncology landscape in the GCC is rapidly evolving, with an increasing focus on early detection programs and expansion of cancer care beyond major hospital centers. As biologic therapies and supportive oncology drugs with self‑administration potential become more broadly available, autoinjectors are emerging as enablers of home‑based cancer care. In Saudi Arabia, oncology centers in Riyadh and Dammam are piloting autoinjector formats for supportive medications such as growth factors used to manage chemotherapy‑induced neutropenia. Patients and care teams alike report that these devices reduce hospital dependency and improve quality of life during treatment cycles. In the UAE, integrated cancer care networks are preparing for broader use of autoinjectors in oncology maintenance regimens that are suitable for home administration. Oncology specialists in Dubai and Abu Dhabi have begun recommending autoinjector delivery formats for subcutaneous monoclonal antibodies used in targeted cancer therapies, citing improved patient comfort and reduced clinic congestion. These developments align with national goals of shifting appropriate care from inpatient settings to community and home environments, particularly as the population ages and demand for chronic cancer therapies increases. Other GCC countries including Qatar, Kuwait, and Bahrain are expanding screening and early‑detection infrastructure, which is leading to higher volumes of patients entering long‑term oncology care. Regional cancer institutes are evaluating connected autoinjector technologies with digital adherence tracking, enabling clinicians to monitor self‑administered oncology drugs remotely. In Oman, oncology outpatient programs are incorporating autoinjectors into treatment plans for supportive care, reducing travel costs and time burdens for patients in remote governorates. Collectively, these region‑specific patterns indicate significant growth potential for autoinjectors in oncology self‑administered drugs across the GCC as clinical practice shifts toward home‑based, patient‑empowered therapeutic models.

GCC Autoinjectors Market Size and Share Analysis:

The GCC Autoinjectors Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, usability, and application, offering insights into their contribution to overall market performance.

By product, the single-dose autoinjectors subsegment dominated the market in 2025, driven by strong regional preference for ready‑to‑use, pre‑filled devices that enhance patient convenience and reduce dosing errors in chronic and emergency care.

Based on usability, the disposable subsegment dominated the market in 2025, driven by widespread adoption of single‑use autoinjectors due to their convenience, sterility, and minimal risk of cross‑contamination in both home and clinical settings.

In terms of application, the autoimmune disorders subsegment dominated the market in 2025, driven by rising prevalence of chronic immune‑mediated conditions in GCC countries that require frequent biologic therapies optimally delivered through autoinjectors.

GCC Autoinjectors Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 110.3 Million

Market Size by 2033

US$ 134.6 Million

CAGR (2026 - 2033)

2.5%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Single-Dose Autoinjectors

Multi-Dose Autoinjectors

Smart / Connected Autoinjectors

Other Products

By Usability

Disposable

Reusable

By Application

Cancer

Autoimmune Disorders

Hormonal Disorders

Pain Management

Other Applications

Regions and Countries Covered

GCC

UAE, Bahrain, Saudi Arabia, Oman, Qatar, Kuwait

Market leaders and key company profiles

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd

West Pharmaceutical Services Inc

SHL Medical

Ypsomed Holding AG

Phillips-Medisize

Nemera

SMC Ltd

Haselmeier GmbH

Get more information on this report

GCC Autoinjectors Market Report Coverage and Deliverables:

The "GCC Autoinjectors Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

GCC Autoinjectors Market size and forecast at regional and country levels for all market segments covered under the scope

GCC Autoinjectors Market trends, as well as drivers, restraints, and opportunities

GCC Autoinjectors Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the GCC Autoinjectors Market

Detailed company profiles, including SWOT analysis

GCC Autoinjectors Market Geographic Insights:

The geographical scope of the GCC Autoinjectors Market report is divided into UAE, Bahrain, Saudi Arabia, Oman, Qatar, and Kuwait. Saudi Arabia held the largest share in 2025.

Country-specific dynamics highlight unique adoption patterns across the GCC. Saudi Arabia dominates the region due to its large patient base, government-driven healthcare modernization, and expanding hospital and specialty clinic networks. Adoption of autoinjectors is particularly strong in urban centers, with local manufacturing partnerships and public reimbursement schemes facilitating growth. In the United Arab Emirates, digital health integration is driving uptake of connected autoinjectors, coupled with mobile app-based adherence monitoring, patient training programs, and private sector engagement. Kuwait and Qatar are characterized by smaller but affluent populations, with strong public healthcare investment and high adoption of premium autoinjector devices for chronic and emergency therapies. Bahrain shows growing uptake in private clinics and hospital networks, driven by patient awareness campaigns and gradual expansion of health insurance coverage. Meanwhile, Oman emphasizes affordability and accessibility, with demand concentrated in urban areas supported by government subsidies and localized distribution networks. Overall, these country-specific dynamics indicate that while Saudi Arabia leads the GCC in volume and influence, other member states present differentiated opportunities that require tailored strategies, including premium product positioning, digital integration, and targeted awareness programs to maximize autoinjector adoption across the region.

Get more information on this report

GCC Autoinjectors Market Research Report Guidance:

The report includes qualitative and quantitative data in the GCC Autoinjectors Market across product, usability, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the GCC Autoinjectors Market.

Chapter 3 focuses on the research smethodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the GCC Autoinjectors Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the GCC Autoinjectors Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover GCC Autoinjectors Market segments by product, usability, application, and geography across UAE, Bahrain, Saudi Arabia, Oman, Qatar, and Kuwait. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the GCC Autoinjectors Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

GCC Autoinjectors Market News and Key Development:

The GCC Autoinjectors Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the GCC autoinjectors market are:

In May 2025, Pfizer introduced a novel once‑weekly prefilled autoinjector therapy for hemophilia in the UAE, marking a key product launch that improves treatment convenience and patient independence for a rare chronic condition. The autoinjector enables subcutaneous self‑administration of a targeted therapy for bleeding reduction, broadening injectable care options in the region. This launch underscores increasing adoption of advanced autoinjector delivery formats. It highlights the GCC’s push toward patient‑centric therapeutic innovations.

In June 2024, BD launched an educational collaboration with Saudi medical associations to train healthcare professionals on proper autoinjector use, especially for emergency allergy and chronic disease applications. This partnership focused on building local competency in device handling and correct administration techniques. It aimed to increase adoption and improve clinical outcomes from self‑administration devices. The initiative represents a key regional effort to strengthen autoinjector competence among care providers.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The GCC Autoinjectors Market is valued at US$ 110.3 Million in 2025, it is projected to reach US$ 134.6 Million by 2033.

What is the CAGR for GCC Autoinjectors Market by (2026 - 2033)?

As per our report GCC Autoinjectors Market, the market size is valued at US$ 110.3 Million in 2025, projecting it to reach US$ 134.6 Million by 2033. This translates to a CAGR of approximately 2.5% during the forecast period.

What segments are covered in this report?

The GCC Autoinjectors Market report typically cover these key segments-

Application (Cancer, Autoimmune Disorders, Hormonal Disorders, Pain Management, Other Applications)

What is the historic period, base year, and forecast period taken for GCC Autoinjectors Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the GCC Autoinjectors Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in GCC Autoinjectors Market?

The GCC Autoinjectors Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd

West Pharmaceutical Services Inc

SHL Medical

Ypsomed Holding AG

Phillips-Medisize

Nemera

SMC Ltd

Haselmeier GmbH

Who should buy this report?

The GCC Autoinjectors Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the GCC Autoinjectors Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For GCC Autoinjectors Market

Get Free Sample For GCC Autoinjectors Market