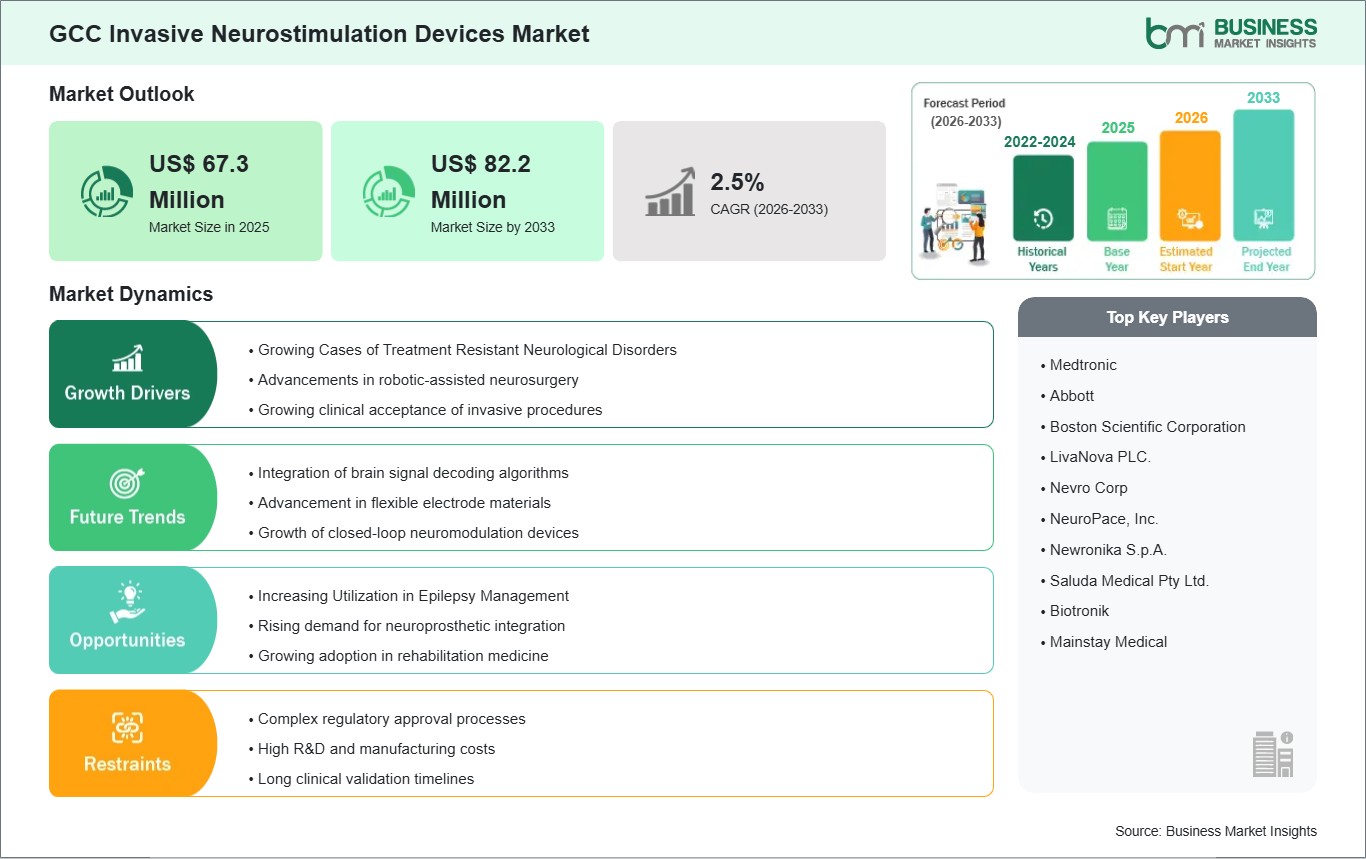

The GCC invasive neurostimulation devices market size is expected to reach US$ 82.2 million by 2033 from US$ 67.3 million in 2025. The market is estimated to register a CAGR of 2.5% from 2026 to 2033.

Executive Summary and GCC Invasive Neurostimulation Devices Market Analysis:

The GCC market for invasive neurostimulation devices has been significantly influenced by an increased reliance of the clinical sector on neurostimulation therapy options in order to treat various neurological and chronic pain disorders that are unresponsive to conventional treatment modalities, especially in view of the expanding neurosurgical skills base of tertiary care facilities in the region. Increasing incidences of epilepsy, Parkinsonian syndromes, and neuropathic pains associated with diabetes and spinal disorders have made clinicians more receptive to the application of invasive techniques involving implantation of devices such as deep-brain stimulation devices, spinal cord stimulators, and vagus nerve stimulators. The major factors influencing the GCC market include rapid healthcare infrastructure development driven by the national diversification strategy of governments, leading to an enhancement of neurological surgery and neurology units at hospitals in the UAE, Saudi Arabia, and other GCC countries. Nonetheless, the industry does face a key challenge in the form of exorbitant procedure and equipment expenses, coupled with inconsistency in reimbursement and an absence of skilled neurosurgeons specialized in device implantation and subsequent management. This will not only affect its adoption rate but could also hamper the accessibility of such treatments for more patients. Nonetheless, private sector growth and demand for minimally invasive and precise neurological treatment solutions are continuously affecting the adoption and upgrading of devices and equipment by the region‘s hospitals. Furthermore, the integration of image-guided navigation tools, AI-supported surgical planning, and collaboration across borders can help improve procedure precision and reinforce the region's positioning as a center of advanced neuromodulation therapy delivery services.

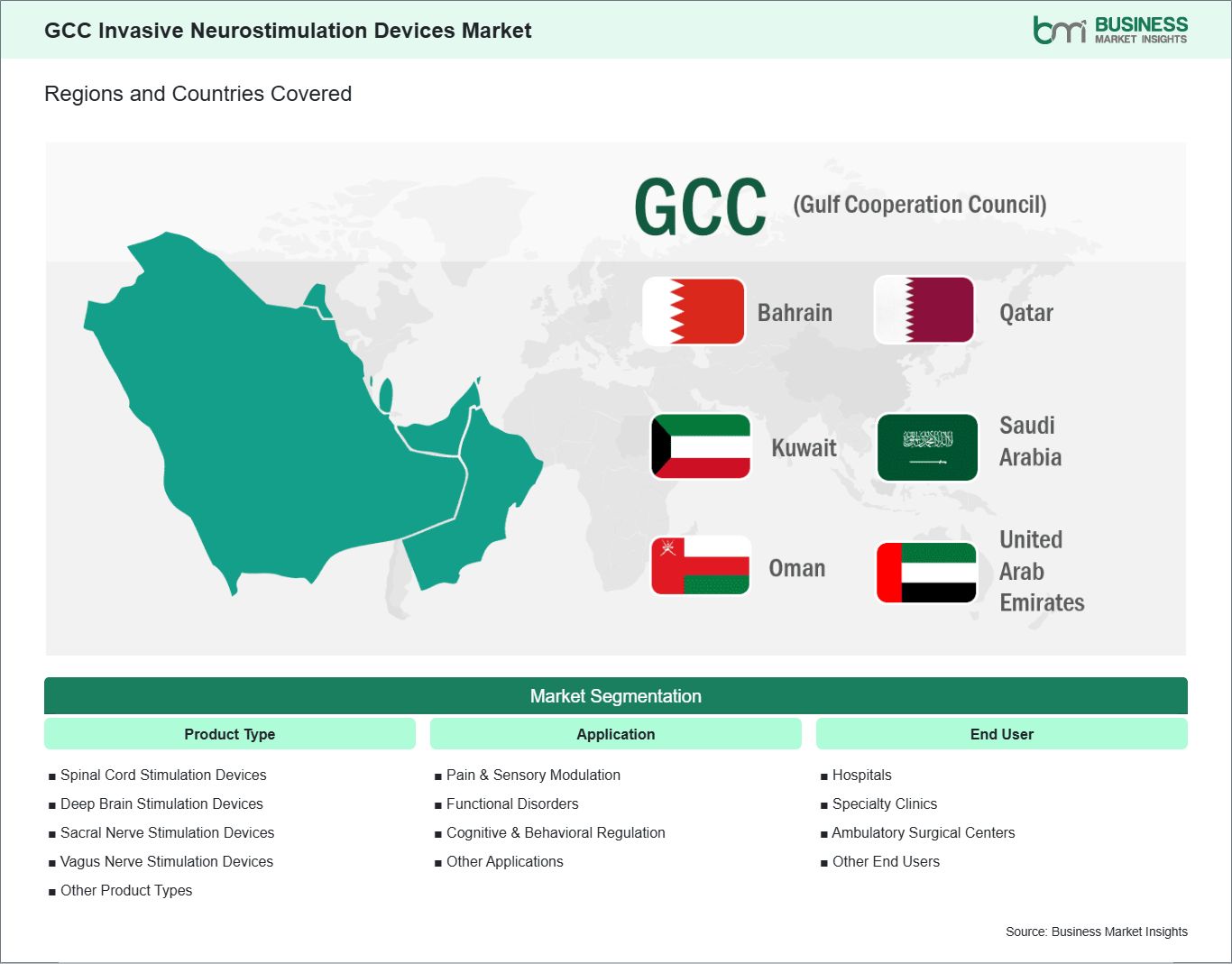

Key segments that contributed to the derivation of the GCC invasive neurostimulation devices market analysis are product type, application and end user.

By product type, the invasive neurostimulation devices market is segmented into spinal cord stimulation devices, deep brain stimulation devices, sacral nerve stimulation devices, vagus nerve stimulation devices, and other product types. The spinal cord stimulation devices segment dominated the market in 2025.

Based on application, the invasive neurostimulation devices market is categorized into pain & sensory modulation, functional disorders, cognitive & behavioral regulation, and other applications. The pain & sensory modulation segment dominated the market in 2025.

In terms of end user, the invasive neurostimulation devices market is categorized into hospitals, specialty clinics, ambulatory surgical centers, and other end users. The hospitals segment dominated the market in 2025.

GCC Invasive Neurostimulation Devices Market Drivers and Opportunities:

Growing Cases of Treatment Resistant Neurological Disorders

Another notable change taking place in the clinical landscape in the GCC countries includes the increasing prevalence of treatment-resistant patients with various neurological conditions among those admitted to different health care facilities. Such patients do not respond sufficiently well to traditional treatment methods; therefore, neurostimulation devices are increasingly considered to be one of the special means available to treat such conditions and fill an obvious therapy gap.

It seems like specialists working in GCC countries are starting to modify their clinical paths to accommodate the increased prevalence of neurostimulation devices. For instance, instead of relying on conventional methods for treating resistant patients until no other options are left, some health care institutions opt to apply neurostimulation in a more timely fashion after identifying patients' resistance patterns. The described situation is characteristic of the general industry trend towards personalized medicine and treatment.

In terms of market behavior, suppliers of devices for neurostimulation seem to be adjusting their strategies according to changing market demands. In particular, professionals, including neurosurgeons and neurologists, play an increasingly important role in the procurement process; hence, such suppliers pay more attention to training their staff, providing technical support, and offering long-term service packages.

Increasing Utilization in Epilepsy Management

Epilepsy management in the GCC is undergoing a transformation as invasive neurostimulation devices gain traction among tertiary care centers. Hospitals are recognizing the limitations of pharmacotherapy in controlling refractory seizures, and neurostimulation is being positioned as a viable adjunct to surgical interventions. This shift is evident in procurement cycles, where epilepsy-focused programs are increasingly allocating budgets toward device acquisition and integration into specialized units.

The clinical adoption pattern reveals a layered utilization strategy. Physicians are not merely deploying neurostimulation for seizure suppression but are also exploring its role in reducing comorbidities such as cognitive decline and mood disturbances. This expanded scope of application is influencing how devices are evaluated, with emphasis placed on multi-dimensional patient outcomes rather than seizure frequency alone.

On the commercial front, manufacturers are leveraging epilepsy management as a key entry point into the GCC market. By aligning product portfolios with epilepsy-focused research initiatives and collaborating with regional neurology associations, companies are embedding themselves into the clinical discourse. This strategy reflects a recognition that epilepsy care serves as a gateway for broader neurostimulation adoption, creating a ripple effect across other neurological domains once trust and efficacy are established.

GCC Invasive Neurostimulation Devices Market Size and Share Analysis:

The GCC invasive neurostimulation devices market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within product type, application and end user, highlighting their respective contributions to market performance.

By product type, the spinal cord stimulation devices subsegment dominated the market in 2025, driven by its widespread adoption for chronic pain management, particularly for failed back surgery syndrome and neuropathic pain conditions.

Based on application, the pain & sensory modulation subsegment dominated the market in 2025, driven by the rising global prevalence of chronic pain disorders and the growing preference for neuromodulation as an alternative to long-term drug therapy.

In terms of end user, the hospitals subsegment dominated the market in 2025, driven by their advanced neurosurgical infrastructure, availability of specialized healthcare professionals, and high volume of neurostimulation implantation procedures.

GCC Invasive Neurostimulation Devices Market Report Coverage and Deliverables:

The "GCC Invasive Neurostimulation Devices Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at regional and country levels for all market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Market concentration, heat map analysis, prominent players, and recent developments for the Market

Detailed company profiles, including SWOT analysis

The geographical scope of the GCC Invasive Neurostimulation Devices Market report is divided into UAE, Bahrain, Saudi Arabia, Oman, Qatar, Kuwait. UAE held the largest share in 2025.

The UAE is clearly leading the market for the GCC Invasive Neurostimulation Devices owing to its highly developed tertiary care system, fast incorporation of advanced technologies in neurosurgery and availability of dedicated neurology care centers for chronic pain management and movement disorders. The Bahraini market has seen moderate growth in its market owing to its efforts towards health-care reforms and use of foreign expertise for treatment, which has resulted in demand for advanced neurostimulator implants. There have been signs of considerable growth for the Saudi market in recent times, thanks to their hospital capacity building efforts, growing investments in neurological rehabilitation services and increased demand for advanced neurological treatment techniques for lifestyle-related disorders. Qatar represents the path of an innovative nature due to the significant focus on providing quality health care services and adopting advanced medical equipment, which leads to the incorporation of invasive neurostimulation at certain high-risk health institutions. On the other hand, Kuwait can be regarded as having progressive growth with regards to advancements driven by renovations made in its hospital system, coupled with an increasingly careful implementation of modern implantable procedures in its neurology units. In the region as a whole, market development trends are characterized by increased awareness of neurological disorders, professional training programs, and collaboration between public and private health institutions, all of which promote innovation and implementation of new neuroimplants.

Get more information on this report

GCC Invasive Neurostimulation Devices Market Research Report Guidance:

The report includes qualitative and quantitative data in the GCC Invasive Neurostimulation Devices Market across product type, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the GCC Invasive Neurostimulation Devices Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the GCC Invasive Neurostimulation Devices Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the GCC Invasive Neurostimulation Devices Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the GCC Invasive Neurostimulation Devices Market segments by product type, application, end user, and geography across UAE, Bahrain, Saudi Arabia, Oman, Qatar, Kuwait. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the GCC Invasive Neurostimulation Devices Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and a disclaimer.

GCC Invasive Neurostimulation Devices Market News and Key Development:

The GCC Invasive Neurostimulation Devices Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the GCC invasive neurostimulation devices market are:

In October 2025, Boston Scientific announced it had entered into a definitive agreement to acquire Nalu Medical, Inc., expanding its neuromodulation portfolio with the Nalu Neurostimulation System. This system delivers peripheral nerve stimulation (PNS) for chronic pain and is expected to broaden Boston Scientific‘s offerings in global markets recognizing FDA-cleared and CE-marked devices.

In November 2024, Nevro announced CE Mark certification for its HFX iQ spinal cord stimulation system with AI technology, paving the way for expansion into global markets that recognize CE-marked devices. This system integrates high-frequency therapy with cloud-based data insights for personalized pain management.

Key Sources Referred:

U.S. Food and Drug Administration (FDA)National Institutes of Health (NIH)National Institute of Neurological Disorders and Stroke (NINDS)Centers for Medicare & Medicaid Services (CMS)Medical Device Innovation Consortium (MDIC)World Health Organization (WHO)International Organization for Standardization (ISO)International Neuromodulation Society (INS)North American Neuromodulation Society (NANS)Company WebsitesCompany Annual ReportsCompany Investor Presentations

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the GCC Invasive Neurostimulation Devices Market?

The GCC Invasive Neurostimulation Devices Market is valued at US$ 67.3 Million in 2025, it is projected to reach US$ 82.2 Million by 2033.

What is the CAGR for GCC Invasive Neurostimulation Devices Market by (2026 - 2033)?

As per our report GCC Invasive Neurostimulation Devices Market, the market size is valued at US$ 67.3 Million in 2025, projecting it to reach US$ 82.2 Million by 2033. This translates to a CAGR of approximately 2.5% during the forecast period.

What segments are covered in this report?

The GCC Invasive Neurostimulation Devices Market report typically cover these key segments-

Product Type (Spinal Cord Stimulation Devices, Deep Brain Stimulation Devices, Sacral Nerve Stimulation Devices, Vagus Nerve Stimulation Devices, and Other Product Types)

Application (Pain & Sensory Modulation, Functional Disorders, Cognitive & Behavioral Regulation, and Other Applications)

End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, and Other End Users)

What is the historic period, base year, and forecast period taken for GCC Invasive Neurostimulation Devices Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the GCC Invasive Neurostimulation Devices Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in GCC Invasive Neurostimulation Devices Market?

The GCC Invasive Neurostimulation Devices Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic

Abbott

Boston Scientific Corporation

LivaNova PLC.

Nevro Corp

NeuroPace, Inc.

Newronika S.p.A.

Saluda Medical Pty Ltd.

Biotronik

Mainstay Medical

Who should buy this report?

The GCC Invasive Neurostimulation Devices Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the GCC Invasive Neurostimulation Devices Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For GCC Invasive Neurostimulation Devices Market

Get Free Sample For GCC Invasive Neurostimulation Devices Market