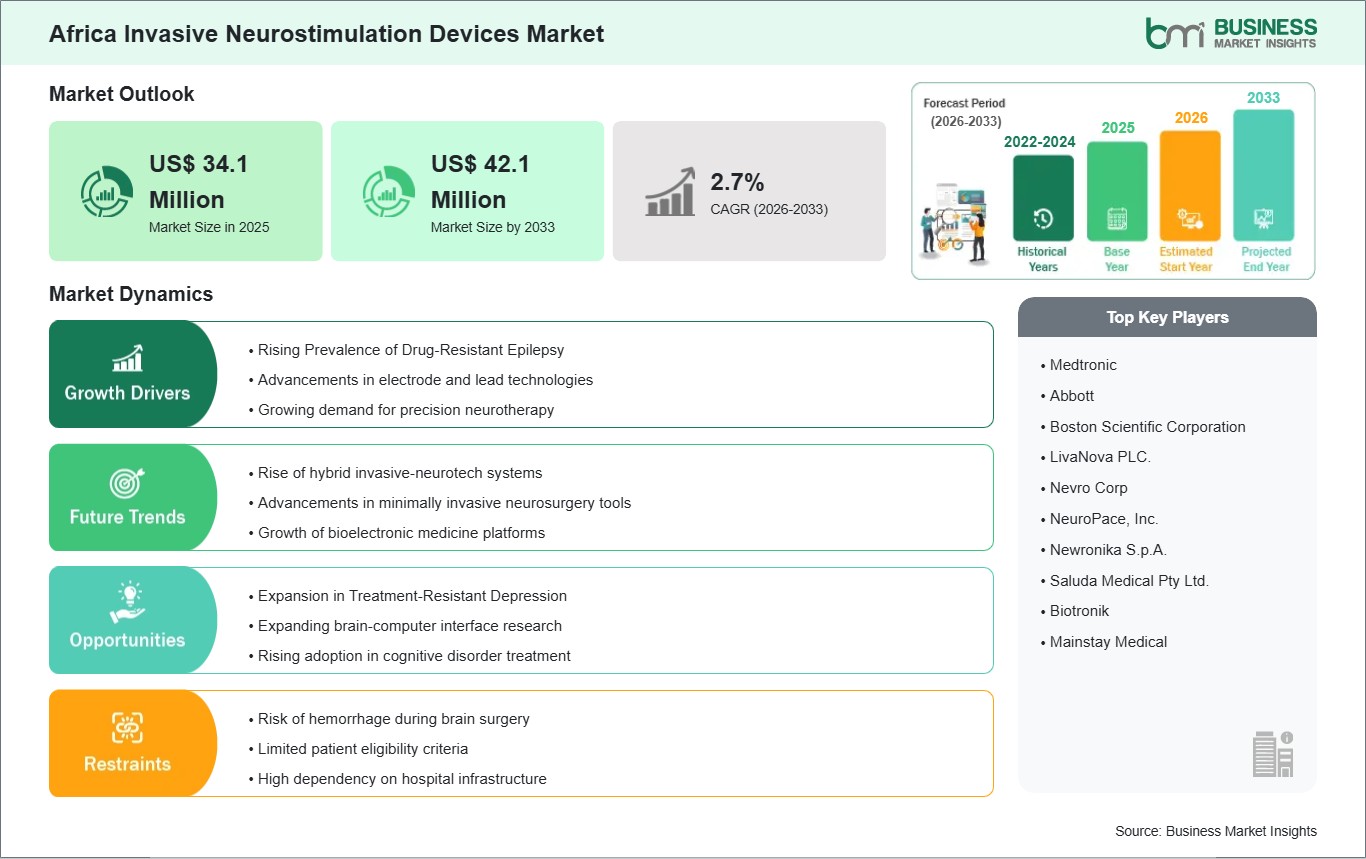

The Africa invasive neurostimulation devices market size is expected to reach US$ 42.1 million by 2033 from US$ 34.1 million in 2025. The market is estimated to register a CAGR of 2.7% from 2026 to 2033.

Executive Summary and Africa Invasive Neurostimulation Devices Market Analysis:

The landscape of Africa's invasive neurostimulation devices is shaped by changing requirements of neurology services and the gradual adoption of high-tech neurosurgical devices in major healthcare centers. The rising incidence of complex neurological disorders—including Parkinsonian syndromes, refractory seizures, and neuropathic pain—is prompting clinicians to increasingly rely on neuromodulation interventions such as deep brain stimulation and spinal cord stimulation, particularly in cases where pharmacological treatments are insufficient. A major contributing factor is the emergence of dedicated neurosurgery centers within tertiary medical institutions in urban areas, supported by improved training expertise and stronger interaction with foreign manufacturers of medical devices. The increasing demand for effective long-term pain management solutions is driving greater interest among pain specialists toward invasive neuromodulation techniques.

Private investments in the health sector and the gradual development of advanced surgical facilities act as key enablers for the adoption of neurostimulation procedures and the improvement of post-procedure patient management capacity. However, a major barrier persists in the region, particularly issues of affordability and limited financing channels, which restrict access to costly neurostimulation implants. Another significant challenge is the uneven distribution of neurosurgical expertise and the shortage of specialized facilities outside major metropolitan hubs, resulting in the use of these devices being concentrated among a limited number of industry players and centers. Despite these constraints, there have been gradual advancements in the adoption of neurostimulation implants in the region, supported by increasing clinical awareness and improving technical capability.

Africa Invasive Neurostimulation Devices Market - Strategic Insights:

Get more information on this report

Africa Invasive Neurostimulation Devices Market Segmentation Analysis:

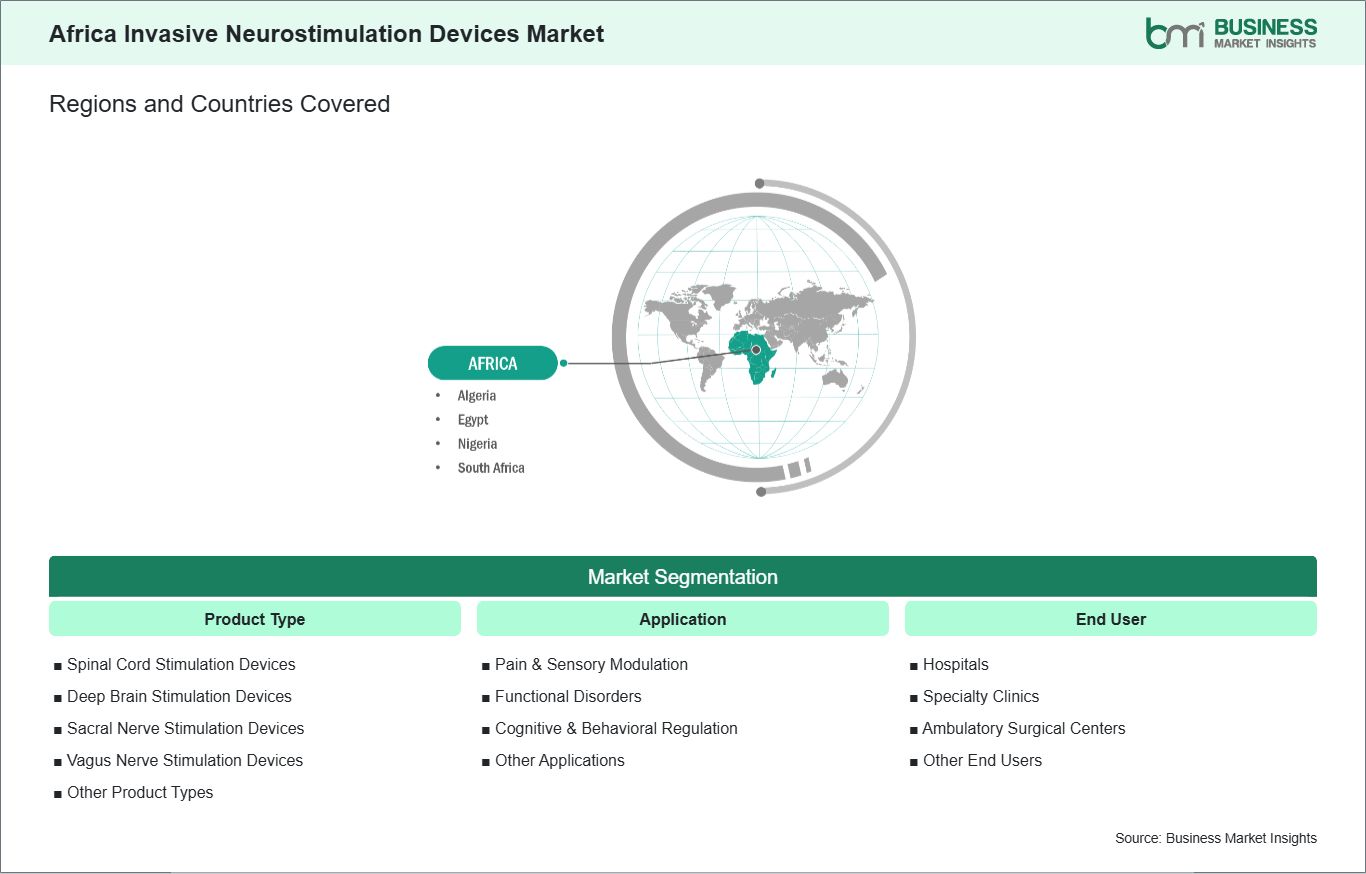

Key segments that contributed to the derivation of the Africa invasive neurostimulation devices market analysis are product type, application, and end user.

By product type, the invasive neurostimulation devices market is segmented into spinal cord stimulation devices, deep brain stimulation devices, sacral nerve stimulation devices, vagus nerve stimulation devices, and other product types. The spinal cord stimulation devices segment dominated the market in 2025.

Based on application, the invasive neurostimulation devices market is categorized into pain & sensory modulation, functional disorders, cognitive & behavioral regulation, and other applications. The pain & sensory modulation segment dominated the market in 2025.

In terms of end user, the invasive neurostimulation devices market is categorized into hospitals, specialty clinics, ambulatory surgical centers, and other end users. The hospitals segment dominated the market in 2025.

Africa Invasive Neurostimulation Devices Market Drivers and Opportunities:

Rising Prevalence of Drug-Resistant Epilepsy

In African neurology practices, drug-resistant epilepsy cases are frequently recognized after numerous rounds of anticonvulsant medication optimization that have taken place in routine neurology or even general practice environments. The referral process for surgery or neuromodulation often occurs at a late stage, largely due to fragmented referral pathways and limited access to dedicated epilepsy monitoring units.

In this context, decisions become more multidisciplinary once pharmacologic management fails, but in most African tertiary care centers, neuromodulation approaches are discussed only after exhausting all medication attempts and managing comorbidities. Consequently, device-based therapy is often positioned as a late-stage, advanced option within a constrained neurosurgical workflow, heavily influenced by available resources and operating theater prioritization.

On the other hand, the use of invasive neurostimulation devices is becoming increasingly concentrated in private neurology clinics and selected teaching hospitals, where clinicians gain familiarity with these technologies through gradual clinical exposure and overseas training opportunities. In parallel, device manufacturers often engage hospitals through a demonstration-led adoption model rather than broad, system-wide distribution.

Expansion in Treatment-Resistant Depression

Within psychiatric care pathways in African urban centers, treatment-resistant depression is managed through layered escalation frameworks, where pharmacological switching is followed by structured intensification of psychotherapy before any consideration of device-based neuromodulation. Clinical teams typically depend on longitudinal observation within outpatient psychiatry units to assess suitability for interventions beyond medication-based strategies.

Driven by the growing acceptance of neuromodulation in psychiatric practice, clinicians in selected African referral hospitals are beginning to integrate noninvasive and invasive stimulation techniques into stepwise treatment plans, particularly for patients with recurrent non-response to antidepressant regimens. However, adoption remains influenced by protocol conservatism and the requirement for multidisciplinary psychiatric and neurological consensus before proceeding.

In private mental health networks and specialized neurology-psychiatry crossover clinics, device-based interventions for treatment-resistant depression are being introduced through carefully selected patient cohorts, often prioritizing individuals with stable clinical histories and documented pharmacotherapy resistance. Follow-up structures emphasize programming adjustments, side-effect monitoring, and caregiver engagement, while manufacturers support adoption through clinician training workshops and limited-site pilot implementations that emphasize procedural familiarity over scale.

Africa Invasive Neurostimulation Devices Market Size and Share Analysis:

The Africa invasive neurostimulation devices market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within product type, application, and end user, highlighting their respective contributions to market performance.

By product type, the spinal cord stimulation devices subsegment dominated the market in 2025, driven by its widespread adoption for chronic pain management, particularly for failed back surgery syndrome and neuropathic pain conditions.

Based on application, the pain & sensory modulation subsegment dominated the market in 2025, driven by the rising global prevalence of chronic pain disorders and the growing preference for neuromodulation as an alternative to long-term drug therapy.

In terms of end user, the hospitals subsegment dominated the market in 2025, driven by their advanced neurosurgical infrastructure, availability of specialized healthcare professionals, and high volume of neurostimulation implantation procedures.

Africa Invasive Neurostimulation Devices Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 34.1 Million

Market Size by 2033

US$ 42.1 Million

CAGR (2026 - 2033)

2.7%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product Type

Spinal Cord Stimulation Devices

Deep Brain Stimulation Devices

Sacral Nerve Stimulation Devices

Vagus Nerve Stimulation Devices

Other Product Types

By Application

Pain & Sensory Modulation

Functional Disorders

Cognitive & Behavioral Regulation

Other Applications

By End User

Hospitals

Specialty Clinics

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

Africa

Egypt, South Africa, Nigeria, Algeria

Market leaders and key company profiles

Medtronic

Abbott

Boston Scientific Corporation

LivaNova PLC.

Nevro Corp

NeuroPace, Inc.

Newronika S.p.A.

Saluda Medical Pty Ltd.

Biotronik

Mainstay Medical

Get more information on this report

Africa Invasive Neurostimulation Devices Market Report Coverage and Deliverables:

The "Africa Invasive Neurostimulation Devices Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at regional and country levels for all market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Market concentration, heat map analysis, prominent players, and recent developments for the Market

Detailed company profiles, including SWOT analysis

Africa Invasive Neurostimulation Devices Market Geographic Insights:

The geographical scope of the Africa Invasive Neurostimulation Devices Market report is divided into Nigeria, Egypt, South Africa, and Algeria. South Africa held the largest share in 2025.

In terms of adoption trends, the African invasive neurostimulation devices market has shown an uneven yet progressively dynamic performance trajectory, particularly across key national healthcare systems. South Africa continues to perform strongly due to a relatively developed neurosurgical infrastructure, high levels of practitioner specialization, and effective integration between private and public tertiary hospitals, enabling earlier incorporation of implantable neurostimulation treatments for chronic neurological disorders. In addition, active clinician training programs and reliable servicing capabilities have contributed to sustained treatment delivery. Nigeria is driven by the rising burden of neurological diseases, increased patient referrals to urban specialty hospitals, and growing investment in private healthcare facilities that support selective importation of neuromodulation devices.

Egypt reflects steady growth supported by government-led modernization of tertiary hospitals, the establishment of specialized neurology and pain management units, and its positioning as a regional medical tourism hub. Algeria is also slowly gaining traction through the upgradation of health infrastructure funded by energy revenues, improvements in neurology units within hospitals, and increasing openness to foreign neurostimulation technologies. This growth is further reinforced by the rising incidence of chronic pain and movement disorders, alongside interclinic collaboration across North Africa that supports gradual acceptance of neurostimulators in public hospitals and training centers within urban regions.

Get more information on this report

Africa Invasive Neurostimulation Devices Market Research Report Guidance:

The report includes qualitative and quantitative data in the Africa Invasive Neurostimulation Devices Market across product type, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Africa Invasive Neurostimulation Devices Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Africa Invasive Neurostimulation Devices Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Africa Invasive Neurostimulation Devices Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Africa Invasive Neurostimulation Devices Market segments by product type, application, end user, and geography across Nigeria, Egypt, South Africa, and Algeria. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Africa Invasive Neurostimulation Devices Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and a disclaimer.

Africa Invasive Neurostimulation Devices Market News and Key Development:

The Africa invasive neurostimulation devices market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Africa invasive neurostimulation devices market are:

In July 2025, Abbott launched its Liberta RC Deep Brain Stimulation (DBS) system in Japan, expanding its rechargeable implantable neurostimulation portfolio designed to treat movement disorders such as Parkinson's disease, essential tremor, and dystonia, and supporting remote programming via NeuroSphere Virtual Clinic.

In April 2024, Medtronic announced FDA approval of its Inceptiv closed-loop spinal cord stimulator, the first implantable spinal cord stimulation system capable of sensing and automatically adjusting therapy in real time for chronic pain management.

Key Sources Referred:

U.S. Food and Drug Administration (FDA)National Institutes of Health (NIH)National Institute of Neurological Disorders and Stroke (NINDS)Centers for Medicare & Medicaid Services (CMS)Medical Device Innovation Consortium (MDIC)World Health Organization (WHO)International Organization for Standardization (ISO)International Neuromodulation Society (INS)North American Neuromodulation Society (NANS)Company WebsitesCompany Annual ReportsCompany Investor Presentations

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Africa Invasive Neurostimulation Devices Market?

The Africa Invasive Neurostimulation Devices Market is valued at US$ 34.1 Million in 2025, it is projected to reach US$ 42.1 Million by 2033.

What is the CAGR for Africa Invasive Neurostimulation Devices Market by (2026 - 2033)?

As per our report Africa Invasive Neurostimulation Devices Market, the market size is valued at US$ 34.1 Million in 2025, projecting it to reach US$ 42.1 Million by 2033. This translates to a CAGR of approximately 2.7% during the forecast period.

What segments are covered in this report?

The Africa Invasive Neurostimulation Devices Market report typically cover these key segments-

Product Type (Spinal Cord Stimulation Devices, Deep Brain Stimulation Devices, Sacral Nerve Stimulation Devices, Vagus Nerve Stimulation Devices, and Other Product Types)

Application (Pain & Sensory Modulation, Functional Disorders, Cognitive & Behavioral Regulation, and Other Applications)

End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, and Other End Users)

What is the historic period, base year, and forecast period taken for Africa Invasive Neurostimulation Devices Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Africa Invasive Neurostimulation Devices Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Africa Invasive Neurostimulation Devices Market?

The Africa Invasive Neurostimulation Devices Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic

Abbott

Boston Scientific Corporation

LivaNova PLC.

Nevro Corp

NeuroPace, Inc.

Newronika S.p.A.

Saluda Medical Pty Ltd.

Biotronik

Mainstay Medical

Who should buy this report?

The Africa Invasive Neurostimulation Devices Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Africa Invasive Neurostimulation Devices Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Africa Invasive Neurostimulation Devices Market

Get Free Sample For Africa Invasive Neurostimulation Devices Market