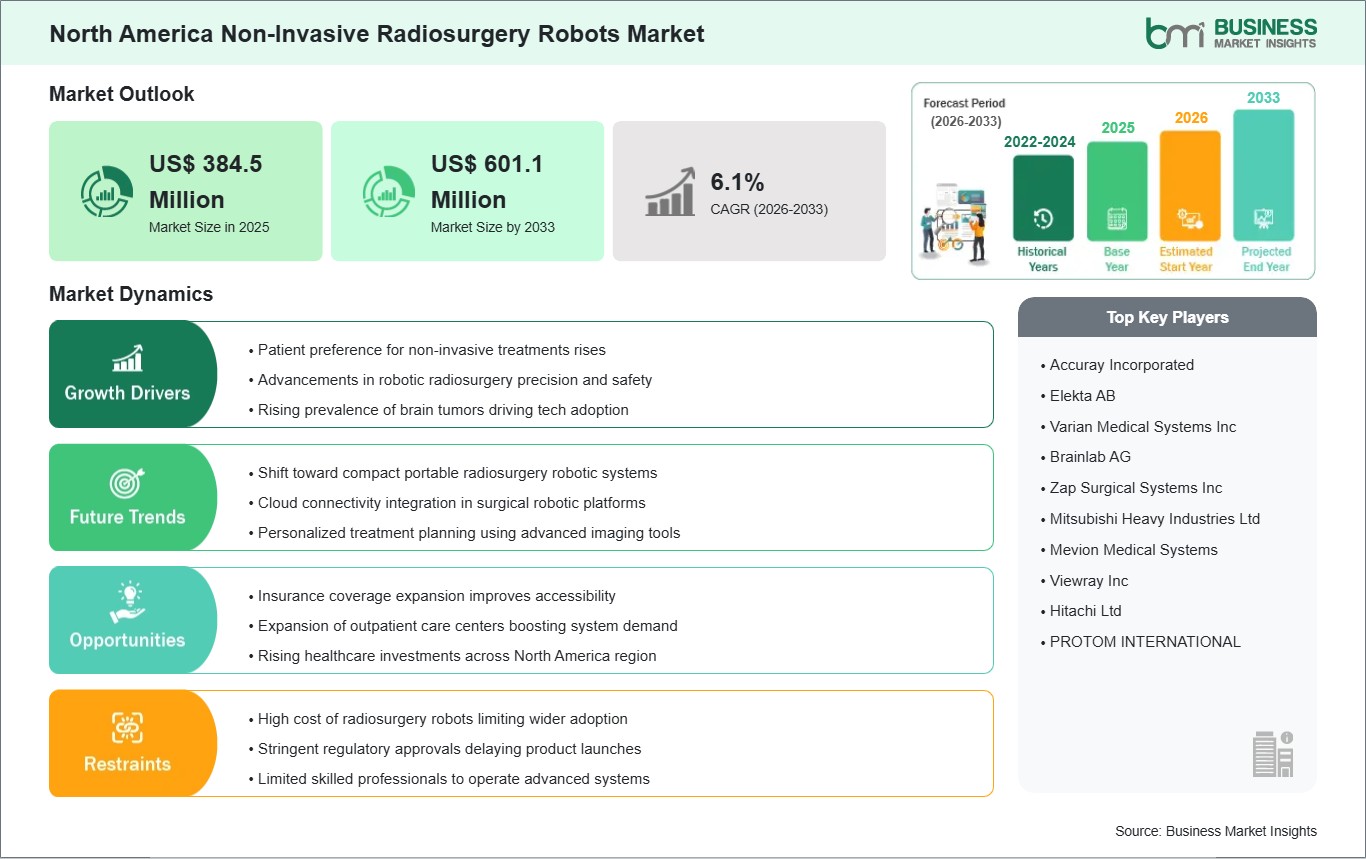

The North America non-invasive radiosurgery robots market size is expected to reach US$601.1 million by 2033 from US$384.5 million in 2025. The market is estimated to record a CAGR of 6.1% from 2026 to 2033.

Executive Summary and North America Non-Invasive Radiosurgery Robots Market Analysis:

The North America Non-Invasive Radiosurgery Robots market is characterized by rapid technological adoption, driven by the region’s strong healthcare infrastructure, high awareness of precision medicine, and increasing prevalence of complex oncological and neurological disorders. Hospitals and specialized treatment centers are integrating robotic radiosurgery systems to enhance procedural accuracy, reduce patient risk, and improve recovery times, particularly in the treatment of brain tumors, spinal lesions, and other complex neurosurgical conditions. The market is shaped by a combination of global robotics manufacturers and regional healthcare technology providers, with competition focused on system precision, integration with advanced imaging modalities, AI-assisted treatment planning, and automated patient motion management. Adoption is concentrated in urban tertiary hospitals and high-volume oncology centers with established imaging capabilities and highly trained clinical personnel. Private hospitals often lead deployment initiatives to differentiate services, attract medical tourists, and establish centers of excellence, while public hospitals adopt robotic systems through structured procurement programs and government-supported modernization initiatives. The market faces challenges, including high capital expenditure, a limited pool of skilled operators, and regulatory considerations that require compliance with both federal and state standards. However, the advantages of robotic radiosurgery—such as improved clinical outcomes, reduced procedural complications, and operational efficiency—position it as a strategic investment for hospitals. Overall, North America represents a highly mature and competitive market where early adopters set clinical and operational benchmarks, and technological innovation continues to drive market differentiation.

North America Non-Invasive Radiosurgery Robots Market - Strategic Insights:

Get more information on this report

North America Non-Invasive Radiosurgery Robots Market Segmentation Analysis:

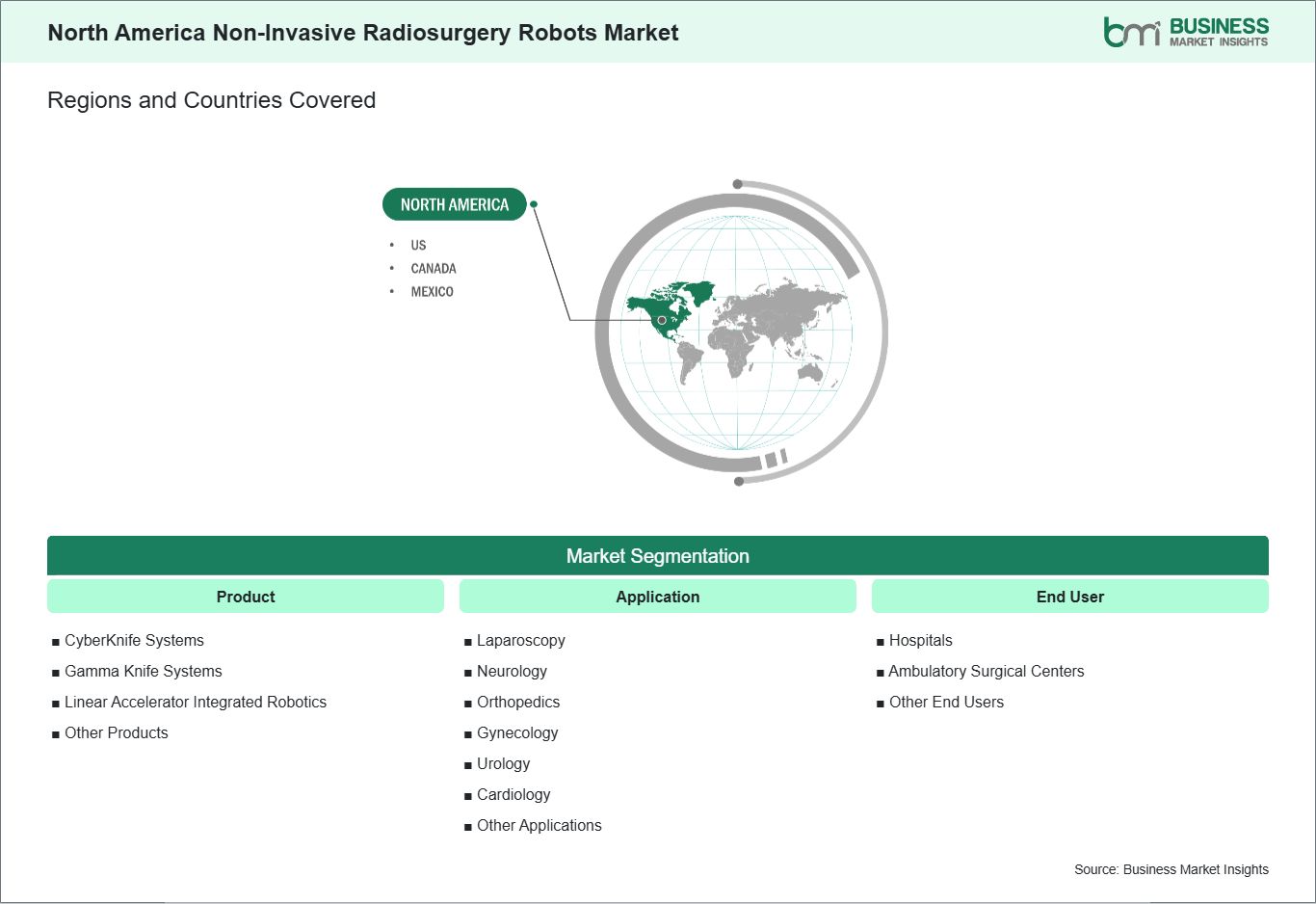

Key segments that contributed to the derivation of the North America non-invasive radiosurgery robots market analysis are product, application, and end user.

By product, the non-invasive radiosurgery robots market is segmented into cyberknife systems, gamma knife systems, linear accelerator (linac) integrated robotics and other products. The medication cyberknife systems segment dominated the market in 2025.

In terms of application, the non-invasive radiosurgery robots market is categorized into laparoscopy, neurology, orthopedics, gynecology, urology, cardiology and other applications. The laparoscopy segment dominated the market in 2025.

Based on end user, the market is classified into hospitals, ambulatory surgical centers and other end users. The hospitals segment dominated the market in 2025.

North America Non-Invasive Radiosurgery Robots Market Drivers and Opportunities:

Patient preference for non-invasive treatments rises

The North America non-invasive radiosurgery robots market is witnessing robust growth driven by increasing patient preference for non-invasive cancer treatments. Patients across the United States and Canada are becoming more aware of minimally invasive options that reduce recovery times, minimize surgical trauma, and limit post-operative complications. Non-invasive radiosurgery robots enable precise radiation delivery to tumors without requiring traditional surgical incisions, which appeals to patients seeking treatment options that are less physically taxing. This trend is particularly prominent among older adults, individuals with comorbidities, and those concerned with quality-of-life considerations during cancer therapy. Healthcare providers are responding to this preference by incorporating robotic radiosurgery systems into multidisciplinary oncology programs. Hospitals and cancer centers are highlighting the advantages of non-invasive procedures, including shorter hospital stays and outpatient treatment capabilities, to attract patients who prioritize comfort and convenience. Patient-centric marketing and educational campaigns are also reinforcing awareness about the benefits of robotic radiosurgery, encouraging more individuals to choose this treatment modality over conventional surgery or extended radiation therapy regimens. As a result, patient demand is increasingly influencing investment decisions in robotic systems across North American healthcare facilities. In addition to influencing hospital adoption, patient preference is shaping clinical workflows and care pathways. Physicians are integrating non-invasive radiosurgery into standard treatment protocols, offering alternatives for tumors in sensitive or hard-to-reach locations. The focus on patient comfort and reduced recovery time also aligns with broader healthcare goals of improving patient satisfaction and outcomes. By responding to the growing demand for minimally invasive treatment options, North American healthcare providers are expanding access to robotic radiosurgery while reinforcing its role as a preferred treatment choice for modern oncology care.

The expansion of insurance coverage for non-invasive radiosurgery procedures is a key factor driving market growth in North America. Public and private insurers are increasingly recognizing robotic radiosurgery as an effective and safe treatment for a variety of cancers, which has improved reimbursement policies and reduced out-of-pocket costs for patients. This coverage expansion makes advanced robotic treatments more accessible to a wider population, including those who may have previously opted for conventional therapies due to financial constraints. Hospitals and clinics are leveraging these insurance improvements to promote broader adoption and ensure that more patients can benefit from precision radiation therapy. Insurance coverage also supports hospitals in justifying investments in robotic radiosurgery systems. With reimbursement policies in place, healthcare facilities can anticipate a return on investment while providing cutting-edge treatment services. The availability of insurance-backed treatment reduces the financial barrier for patients and encourages them to seek earlier intervention, improving overall clinical outcomes. In addition, insurance coverage often extends to outpatient procedures, which aligns with the minimally invasive nature of robotic radiosurgery and supports efficient hospital operations. Furthermore, expanded insurance coverage promotes regional adoption by enabling healthcare providers to offer radiosurgery services in both metropolitan and smaller urban centers. Hospitals in diverse geographic locations can implement robotic systems knowing that patients will have access to reimbursement, enhancing equitable access to advanced oncology care across North America. Coverage expansion also incentivizes collaboration between hospitals, insurers, and technology providers to optimize treatment protocols and cost-effectiveness. Overall, the combination of insurance support and patient demand is strengthening the North American non-invasive radiosurgery robots market, improving accessibility, affordability, and adoption of these advanced cancer treatments.

North America Non-Invasive Radiosurgery Robots Market Size and Share Analysis:

The North America non-invasive radiosurgery robots market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

By product, the medication cyberknife systems segment dominated the market in 2025, driven by widespread clinical adoption due to high precision and real‑time image‑guided capabilities that enhance treatment outcomes and reduce damage to healthy tissue.

In terms of application, the laparoscopy subsegment dominated the market in 2025, driven by strong demand for minimally invasive procedures that offer faster recovery, fewer complications, and improved patient satisfaction.

Based on end user, the hospitals subsegment dominated the market in 2025, driven by extensive healthcare infrastructure and high investments in advanced oncology technologies to meet growing patient volume and complex treatment needs.

North America Non-Invasive Radiosurgery Robots Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 384.5 Million

Market Size by 2033

US$ 601.1 Million

CAGR (2026 - 2033)

6.1%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

CyberKnife Systems

Gamma Knife Systems

Linear Accelerator Integrated Robotics

Other Products

By Application

Laparoscopy

Neurology

Orthopedics

Gynecology

Urology

Cardiology

Other Applications

By End User

Hospitals

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

North America

US, Canada, Mexico

Market leaders and key company profiles

Accuray Incorporated

Elekta AB

Varian Medical Systems Inc

Brainlab AG

Zap Surgical Systems Inc

Mitsubishi Heavy Industries Ltd

Mevion Medical Systems

Viewray Inc

Hitachi Ltd

PROTOM INTERNATIONAL

Get more information on this report

North America Non-Invasive Radiosurgery Robots Market Report Coverage and Deliverables:

The "North America Non-Invasive Radiosurgery Robots Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

North America Non-Invasive Radiosurgery Robots Market size and forecast at regional and country levels for all segments covered under the scope

North America Non-Invasive Radiosurgery Robots Market trends, as well as drivers, restraints, and opportunities

North America Non-Invasive Radiosurgery Robots Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the North America Non-Invasive Radiosurgery Robots Market

Detailed company profiles, including SWOT analysis

North America Non-Invasive Radiosurgery Robots Market Geographic Insights:

The geographical scope of the North America Non-Invasive Radiosurgery Robots Market report is divided into US, Canada, and Mexico. The US held the largest share in 2025.

The North America Non-Invasive Radiosurgery Robots market exhibits varied adoption across the U.S., Canada, and Mexico, reflecting differences in healthcare infrastructure, investment capacity, and clinical specialization. The U.S. emerges as the dominant market, with leading hospitals in metropolitan areas such as New York, Los Angeles, Boston, and Chicago actively deploying robotic radiosurgery systems to enhance treatment precision, optimize workflow efficiency, and expand access to minimally invasive procedures. Adoption in the U.S. is driven by a combination of private and public investments, advanced tertiary hospitals, well-established oncology and neurosurgery centers, and comprehensive training programs for radiation oncologists and neurosurgeons. Hospitals leverage robotic systems to improve clinical outcomes, reduce procedural risks, and strengthen institutional reputation, particularly in centers of excellence and high-volume tertiary care facilities. Canada represents a secondary growth market, with adoption concentrated in urban tertiary hospitals and specialized cancer centers in Toronto, Montreal, and Vancouver. Canadian hospitals prioritize clinical accuracy, patient safety, and operational efficiency, often deploying systems through public-private partnerships, pilot programs, and structured government-supported funding initiatives. Mexico is an emerging market, with deployment focused on major urban hospitals in Mexico City, Monterrey, and Guadalajara, where infrastructure and specialized personnel are sufficient to manage advanced radiosurgery technology. Adoption in Mexico often relies on referral networks or shared-service models, allowing hospitals to provide patient access to high-precision treatments while managing resource limitations. Across all three countries, successful adoption is supported by vendor strategies offering flexible financing, structured clinical training, and ongoing technical support. High-volume hospitals and specialized centers act as primary adoption hubs, while smaller institutions often rely on networked access to robotic systems. The U.S.’s dominance reflects its larger healthcare infrastructure, higher investment capacity, and concentration of advanced tertiary hospitals, positioning it as the key driver of growth in North America. Canada and Mexico provide incremental opportunities for market expansion as awareness, healthcare modernization, and minimally invasive treatment adoption continue to grow across the region.

Get more information on this report

North America Non-Invasive Radiosurgery Robots Market Research Report Guidance:

The report includes qualitative and quantitative data in the North America Non-Invasive Radiosurgery Robots Market across product, application, end user and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the North America Non-Invasive Radiosurgery Robots Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the North America Non-Invasive Radiosurgery Robots Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the North America Non-Invasive Radiosurgery Robots Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover North America Non-Invasive Radiosurgery Robots Market segments by product, application, end user, and geography across US, Canada, and Mexico. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the North America Non-Invasive Radiosurgery Robots Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

North America Non-Invasive Radiosurgery Robots Market News and Key Development:

The North America Non-Invasive Radiosurgery Robots Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the North America non-invasive radiosurgery robots market are:

In November 2025, ZAP Surgical’s ZAP‑Axon Radiosurgery Planning System achieved U.S. FDA 510(k) clearance (and parallel EU CE certification), authorizing its clinical use across the United States and EU as a dedicated cranial radiosurgery planning platform. This regulatory approval is critical for enabling efficient treatment planning for ZAP‑X systems at North American centres. It delivers a streamlined interface built specifically for stereotactic radiosurgery case workflows, enhancing precision and usability. The dual approvals mark an important expansion in regulatory recognition of next‑generation radiosurgery tooling.

In January 2024, Westchester Medical Center in New York announced it would become the first hospital in New York State to install the ZAP‑X Gyroscopic Radiosurgery system, bringing this non‑invasive robotic radiosurgery technology to the Hudson Valley region. The installation, slated for mid‑2024, represents a regional product launch of the ZAP‑X platform to serve patients needing high‑precision radiosurgery without open surgery. This initiative positions the medical centre as an advanced radiosurgery provider in the northeastern U.S., complementing existing treatment modalities.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the North America Non-Invasive Radiosurgery Robots Market?

The North America Non-Invasive Radiosurgery Robots Market is valued at US$ 384.5 Million in 2025, it is projected to reach US$ 601.1 Million by 2033.

What is the CAGR for North America Non-Invasive Radiosurgery Robots Market by (2026 - 2033)?

As per our report North America Non-Invasive Radiosurgery Robots Market, the market size is valued at US$ 384.5 Million in 2025, projecting it to reach US$ 601.1 Million by 2033. This translates to a CAGR of approximately 6.1% during the forecast period.

What segments are covered in this report?

The North America Non-Invasive Radiosurgery Robots Market report typically cover these key segments-

Product (CyberKnife Systems, Gamma Knife Systems, Linear Accelerator (LINAC) Integrated Robotics, Other Products)

Application (Laparoscopy, Neurology, Orthopedics, Gynecology, Urology, Cardiology, Other Applications)

End User (Hospitals, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for North America Non-Invasive Radiosurgery Robots Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Non-Invasive Radiosurgery Robots Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in North America Non-Invasive Radiosurgery Robots Market?

The North America Non-Invasive Radiosurgery Robots Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Accuray Incorporated

Elekta AB

Varian Medical Systems Inc

Brainlab AG

Zap Surgical Systems Inc

Mitsubishi Heavy Industries Ltd

Mevion Medical Systems

Viewray Inc

Hitachi Ltd

PROTOM INTERNATIONAL

Who should buy this report?

The North America Non-Invasive Radiosurgery Robots Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the North America Non-Invasive Radiosurgery Robots Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For North America Non-Invasive Radiosurgery Robots Market

Get Free Sample For North America Non-Invasive Radiosurgery Robots Market