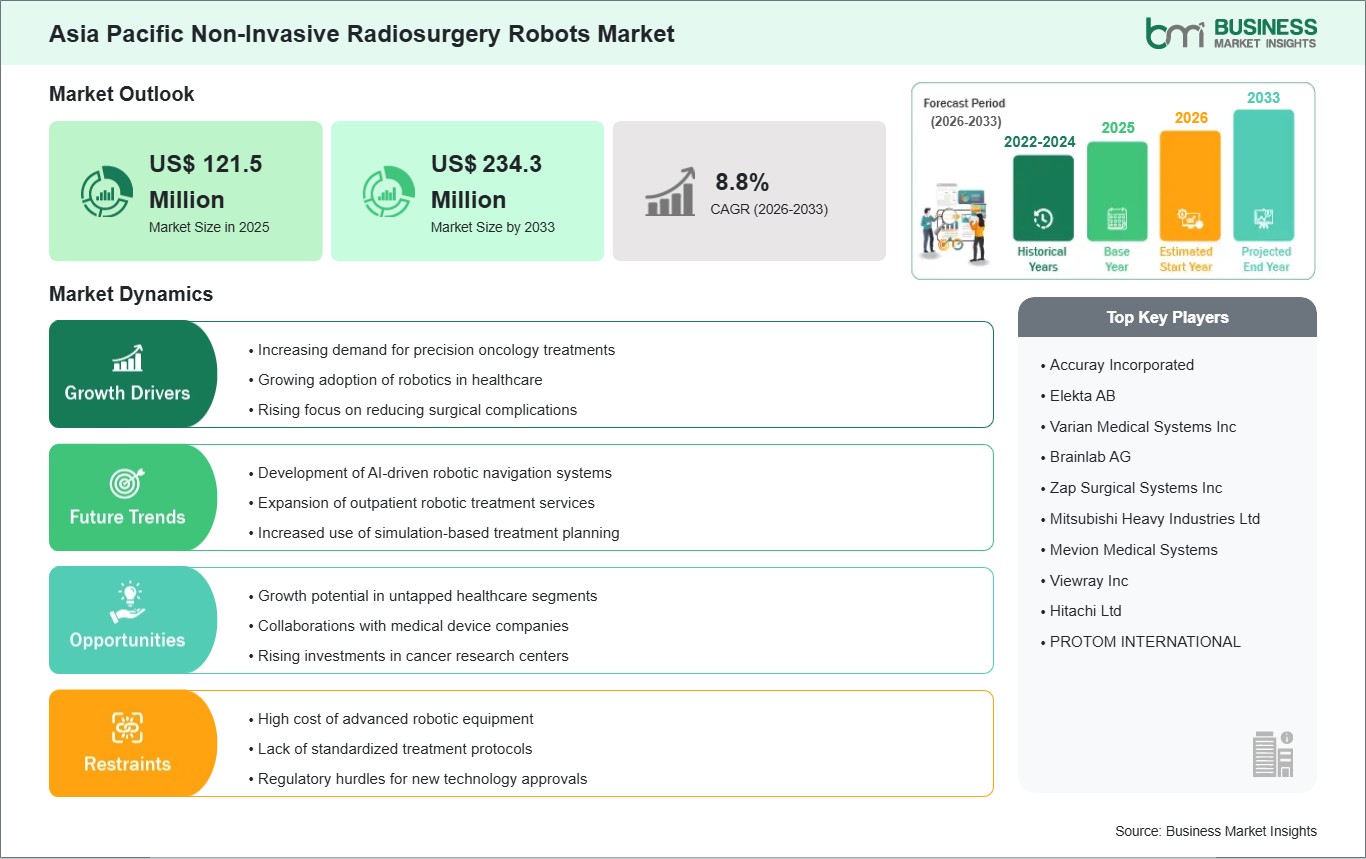

The Asia Pacific non-invasive radiosurgery robots market size is expected to reach US$234.3 million by 2033 from US$121.5 million in 2025. The market is estimated to record a CAGR of 8.8% from 2026 to 2033.

Executive Summary and Asia Pacific Non-Invasive Radiosurgery Robots Market Analysis:

The Asia Pacific Non‑Invasive Radiosurgery Robots market represents a strategic frontier in precision oncology and neurosurgery, driven by escalating demand for minimally invasive therapies and improved clinical outcomes. This market segment is shaped by the increasing prevalence of cancer, neurological disorders, and vascular anomalies, coupled with a growing patient preference for treatments that minimize hospitalization and recovery times. Hospitals and specialty centers across Asia Pacific are exploring robotic radiosurgery systems to address these demands, emphasizing high-precision radiation delivery, workflow efficiency, and integration with advanced imaging modalities. The competitive environment is dominated by a combination of global robotics OEMs and regional technology integrators, with differentiation focused on system accuracy, treatment versatility, and service reliability. Early adoption has been concentrated in developed healthcare hubs such as Japan, South Korea, and Australia, where tertiary hospitals possess the technical infrastructure and skilled workforce necessary to operate advanced radiosurgery systems. Meanwhile, emerging markets in India, China, and Southeast Asia are witnessing growing interest as private and public healthcare institutions seek to enhance service offerings and attract inbound medical tourism. Key drivers include technological advances in AI-assisted treatment planning, automated motion compensation, and precision targeting that expand the clinical scope of radiosurgery beyond conventional tumor sites. Adoption challenges remain significant, particularly in terms of high upfront investment, the need for specialized training, and varying regulatory frameworks across Asia Pacific nations. Nevertheless, the market is gaining momentum as healthcare providers recognize the potential to improve patient throughput, reduce procedural risk, and achieve cost efficiencies over the long term. For investors and hospital administrators, this market presents a compelling opportunity to deploy high-value medical technology while simultaneously strengthening institutional reputation and competitive positioning in regional oncology services.

Asia Pacific Non-Invasive Radiosurgery Robots Market - Strategic Insights:

Get more information on this report

Asia Pacific Non-Invasive Radiosurgery Robots Market Segmentation Analysis:

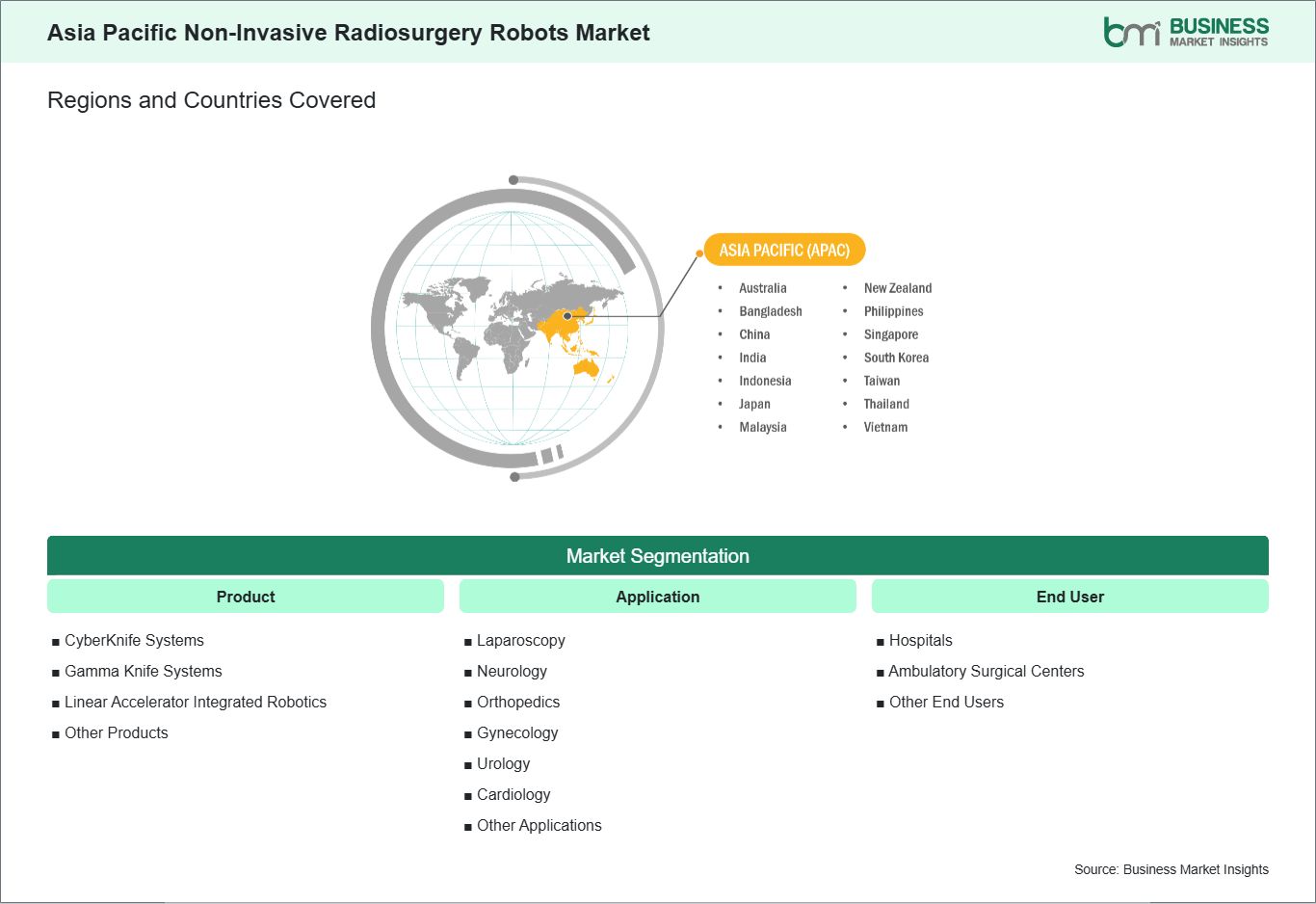

Key segments that contributed to the derivation of the Asia Pacific non-invasive radiosurgery robots market analysis are product, application, and end user.

By product, the non-invasive radiosurgery robots market is segmented into cyberknife systems, gamma knife systems, linear accelerator (linac) integrated robotics and other products. The medication cyberknife systems segment dominated the market in 2025.

In terms of application, the non-invasive radiosurgery robots market is categorized into laparoscopy, neurology, orthopedics, gynecology, urology, cardiology and other applications. The laparoscopy segment dominated the market in 2025.

Based on end user, the market is classified into hospitals, ambulatory surgical centers and other end users. The hospitals segment dominated the market in 2025.

Asia Pacific Non-Invasive Radiosurgery Robots Market Drivers and Opportunities:

Rising adoption of robotic-assisted surgeries

The Asia Pacific healthcare landscape is experiencing a significant shift toward robotic‑assisted medical procedures, driven by the need to improve clinical precision, reduce patient recovery times, and expand access to advanced treatment modalities. Non‑invasive radiosurgery robots, as part of this broader trend, are gaining recognition among hospitals and oncology centers as instruments that can deliver focused radiation with high accuracy. Healthcare providers in the region are increasingly investing in technologies that support minimally invasive and image‑guided treatments, reflecting a broader strategic emphasis on reducing surgical trauma and enhancing patient outcomes. The shift toward robotic‑assisted solutions aligns with efforts to modernize care delivery and integrate sophisticated tools into existing clinical infrastructures. In major metropolitan medical hubs, healthcare institutions are positioning non‑invasive radiosurgery robots as central elements of multidisciplinary cancer care programs. Oncology specialists and surgical teams are collaborating to explore use cases where robotic precision can address tumors located in anatomically challenging regions or in cases where conventional surgery presents increased risk. This clinical enthusiasm is also reflected in institutional investment strategies, where healthcare providers allocate resources toward technologies that can support both diagnostic accuracy and therapeutic effectiveness. By integrating radiosurgery robots into surgical suites and imaging departments, hospitals demonstrate a commitment to leveraging automation and robotics to achieve better clinical performance. Patient demand and referral patterns are also influencing the adoption trajectory of radiosurgery robots across Asia Pacific. Increasing awareness of robotic‑assisted procedures among patients and referring clinicians has generated greater interest in technologies that can offer targeted treatment with fewer side effects. Healthcare facilities that adopt these systems often communicate their availability as a differentiator, positioning themselves to attract patients seeking advanced oncology care. As a result, there is a growing ecosystem of early adopters, technology vendors, and clinical advocates fueling market momentum, which collectively contributes to a broader integration of robotic‑assisted modalities within regional healthcare frameworks.

Collaboration with academic research institutions

Collaboration between healthcare providers, technology developers, and academic research institutions is a defining feature of the Asia Pacific non‑invasive radiosurgery robots market. Universities and medical research centers in the region are playing a pivotal role in advancing the scientific foundations of radiosurgery robotics by conducting clinical studies, validation trials, and technology assessments. These partnerships help bridge clinical needs with engineering innovation, driving the refinement of treatment protocols and the development of next‑generation systems. By fostering environments where clinicians and researchers can exchange insights, the Asia Pacific market is nurturing evidence‑based adoption of radiosurgery robots, which contributes to greater confidence among end users. Research collaborations are also enabling region‑specific enhancements that address unique clinical and operational considerations within local healthcare systems. Academic partners contribute to the customization of software algorithms, imaging interfaces, and workflow integrations that align with regional treatment patterns. Through pilot programs and institutional partnerships, technology providers gain access to real‑world clinical data that inform ongoing product development. These activities not only support the regulatory approval process but also help build robust clinical evidence highlighting the safety, accuracy, and operational benefits of non‑invasive radiosurgery systems in diverse care settings. Moreover, academic research institutions are serving as hubs for training and professional development that support wider market growth. Medical schools and specialized research centers are offering education programs and competency‑building initiatives focused on robotics, imaging integration, and precision treatment planning. This emphasis on workforce readiness is critical for successful implementation of radiosurgery robots, as clinical teams require familiarity with both the technological capabilities and the clinical applications of these systems. By investing in collaborative research and training ecosystems, stakeholders across Asia Pacific are positioning the non‑invasive radiosurgery robots market to expand sustainably, supported by evidence‑based practice and a well‑prepared clinical workforce.

Asia Pacific Non-Invasive Radiosurgery Robots Market Size and Share Analysis:

The Asia Pacific non-invasive radiosurgery robots market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

By product, the medication cyberknife systems segment dominated the market in 2025, driven by their capability to deliver precise, real-time image-guided treatment for complex tumors with minimal damage to surrounding healthy tissue.

In terms of application, the laparoscopy subsegment dominated the market in 2025, driven by the growing adoption of minimally invasive procedures that reduce recovery time, complications, and hospital stays.

Based on end user, the hospitals subsegment dominated the market in 2025, driven by high patient volumes, advanced infrastructure, and multidisciplinary teams that support adoption of robotic radiosurgery technologies.

Asia Pacific Non-Invasive Radiosurgery Robots Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 121.5 Million

Market Size by 2033

US$ 234.3 Million

CAGR (2026 - 2033)

8.8%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

CyberKnife Systems

Gamma Knife Systems

Linear Accelerator Integrated Robotics

Other Products

By Application

Laparoscopy

Neurology

Orthopedics

Gynecology

Urology

Cardiology

Other Applications

By End User

Hospitals

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

Asia Pacific

China, India, Japan, Australia, Bangladesh, Indonesia, Malaysia, New Zealand, Philippines, Singapore, South Korea, Taiwan, Thailand, Vietnam

Market leaders and key company profiles

Accuray Incorporated

Elekta AB

Varian Medical Systems Inc

Brainlab AG

Zap Surgical Systems Inc

Mitsubishi Heavy Industries Ltd

Mevion Medical Systems

Viewray Inc

Hitachi Ltd

PROTOM INTERNATIONAL

Get more information on this report

Asia Pacific Non-Invasive Radiosurgery Robots Market Report Coverage and Deliverables:

The "Asia Pacific Non-Invasive Radiosurgery Robots Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Asia Pacific Non-Invasive Radiosurgery Robots Market size and forecast at regional and country levels for all segments covered under the scope

Asia Pacific Non-Invasive Radiosurgery Robots Market trends, as well as drivers, restraints, and opportunities

Asia Pacific Non-Invasive Radiosurgery Robots Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Asia Pacific Non-Invasive Radiosurgery Robots Market

Detailed company profiles, including SWOT analysis

Asia Pacific Non-Invasive Radiosurgery Robots Market Geographic Insights:

The geographical scope of the Asia Pacific Non-Invasive Radiosurgery Robots Market report is divided into China, India, Japan, Australia, Bangladesh, Indonesia, Malaysia, New Zealand, Philippines, Singapore, South Korea, Taiwan, Thailand, and Vietnam. China held the largest share in 2025.

Within the Asia Pacific region, the market for non-invasive radiosurgery robots displays significant diversity, reflecting differences in healthcare infrastructure, economic capacity, and technology adoption readiness. India emerges as the dominant market, driven by a combination of a large and growing patient population, rising incidence of cancer and neurological disorders, and expanding private and public tertiary hospitals investing in precision oncology solutions. Major urban centers such as Mumbai, Delhi, Bangalore, and Hyderabad are increasingly prioritizing robotic radiosurgery systems to improve patient outcomes, reduce treatment times, and establish specialized treatment centers capable of serving both domestic and regional patient inflows. China is another high-growth market, with adoption concentrated in metropolitan hospitals in Beijing, Shanghai, and Guangzhou, driven by government initiatives to modernize cancer care infrastructure and growing private hospital networks. Japan and South Korea represent mature markets with early adoption, supported by sophisticated imaging infrastructure, experienced oncology teams, and advanced regulatory frameworks that facilitate integration of cutting-edge technologies. Australia and New Zealand are moderate-growth markets where robotic radiosurgery systems are deployed in tertiary hospitals to expand oncology and neurology services and enhance regional medical tourism offerings. Singapore, Malaysia, and Thailand are gradually expanding adoption, particularly in flagship private hospitals that aim to attract international patients and improve competitive positioning. Indonesia, Philippines, Vietnam, Bangladesh, and Taiwan remain in early-stage adoption, constrained by limited infrastructure, workforce skill gaps, and capital availability, though pilot programs and regional partnerships are beginning to introduce robotic systems in key hospitals. Across all these markets, commercial success hinges on flexible financing models, robust operator training programs, and strong service networks. India’s dominance reflects not only market size but also the strategic prioritization of advanced treatment technologies in major urban centers, making it the central hub for vendor focus and regional growth, while other countries represent both opportunities for expansion and benchmarks for adoption best practices.

Get more information on this report

Asia Pacific Non-Invasive Radiosurgery Robots Market Research Report Guidance:

The report includes qualitative and quantitative data in the Asia Pacific Non-Invasive Radiosurgery Robots Market across product, application, end user and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Asia Pacific Non-Invasive Radiosurgery Robots Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Asia Pacific Non-Invasive Radiosurgery Robots Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Asia Pacific Non-Invasive Radiosurgery Robots Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Asia Pacific Non-Invasive Radiosurgery Robots Market segments by product, application, end user, and geography across China, India, Japan, Australia, Bangladesh, Indonesia, Malaysia, New Zealand, Philippines, Singapore, South Korea, Taiwan, Thailand, and Vietnam. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Asia Pacific Non-Invasive Radiosurgery Robots Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Asia Pacific Non-Invasive Radiosurgery Robots Market News and Key Development:

The Asia Pacific Non-Invasive Radiosurgery Robots Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Asia Pacific non-invasive radiosurgery robots market are:

In October 2025, Peking University International Hospital entered a strategic partnership with Baheal Medical to establish a precision radiosurgery centre equipped with the ZAP‑X Gyroscopic Radiosurgery platform, a cutting‑edge non‑invasive system focused on brain and cranial tumour treatments. This centre will also serve as a training and research hub to support broader clinical adoption across China and neighboring countries.

In June 2024, Apollo Cancer Centres launched India’s first robotic & stereotactic radiosurgery education programme in collaboration with Accuray to train clinicians in advanced CyberKnife systems, strengthening knowledge and clinical skills for non‑invasive radiosurgery across India and the sub‑

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Asia Pacific Non-Invasive Radiosurgery Robots Market?

The Asia Pacific Non-Invasive Radiosurgery Robots Market is valued at US$ 121.5 Million in 2025, it is projected to reach US$ 234.3 Million by 2033.

What is the CAGR for Asia Pacific Non-Invasive Radiosurgery Robots Market by (2026 - 2033)?

As per our report Asia Pacific Non-Invasive Radiosurgery Robots Market, the market size is valued at US$ 121.5 Million in 2025, projecting it to reach US$ 234.3 Million by 2033. This translates to a CAGR of approximately 8.8% during the forecast period.

What segments are covered in this report?

The Asia Pacific Non-Invasive Radiosurgery Robots Market report typically cover these key segments-

Product (CyberKnife Systems, Gamma Knife Systems, Linear Accelerator (LINAC) Integrated Robotics, Other Products)

Application (Laparoscopy, Neurology, Orthopedics, Gynecology, Urology, Cardiology, Other Applications)

End User (Hospitals, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for Asia Pacific Non-Invasive Radiosurgery Robots Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Non-Invasive Radiosurgery Robots Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Asia Pacific Non-Invasive Radiosurgery Robots Market?

The Asia Pacific Non-Invasive Radiosurgery Robots Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Accuray Incorporated

Elekta AB

Varian Medical Systems Inc

Brainlab AG

Zap Surgical Systems Inc

Mitsubishi Heavy Industries Ltd

Mevion Medical Systems

Viewray Inc

Hitachi Ltd

PROTOM INTERNATIONAL

Who should buy this report?

The Asia Pacific Non-Invasive Radiosurgery Robots Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Asia Pacific Non-Invasive Radiosurgery Robots Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Asia Pacific Non-Invasive Radiosurgery Robots Market

Get Free Sample For Asia Pacific Non-Invasive Radiosurgery Robots Market