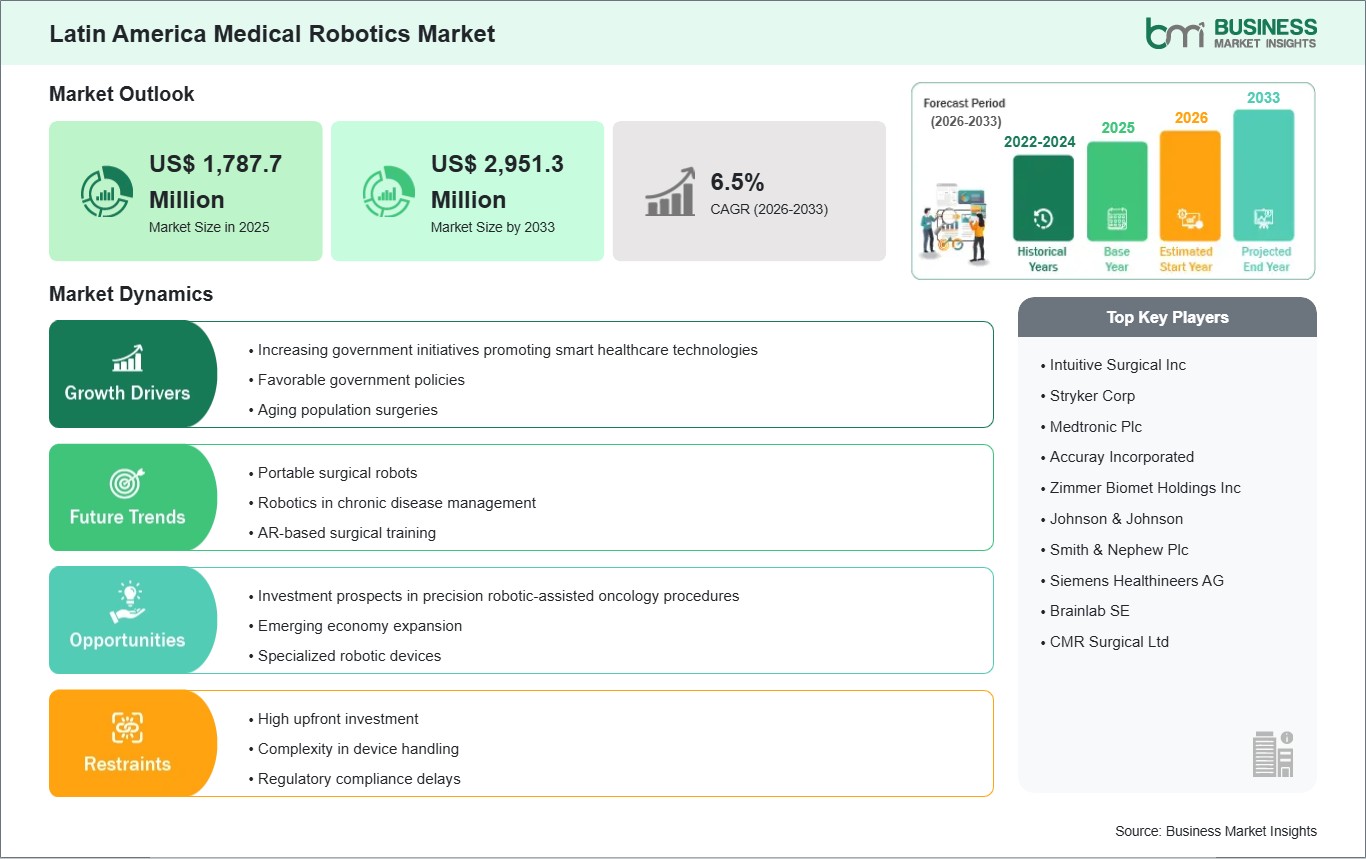

The Latin America medical robotics market size is expected to reach US$ 2,951.3 million by 2033 from US$ 1,787.7 million in 2025. The market is estimated to record a CAGR of 6.5% from 2026 to 2033./p>

Executive Summary and Latin America Medical Robotics Market Analysis:

The Latin America medical robotics market is advancing steadily as healthcare systems across the region prioritize quality enhancement, procedural precision, and technological modernization. Key markets such as Brazil, Mexico, Argentina, and Chile are increasingly investing in robotic-assisted solutions particularly for minimally invasive surgery and complex care pathways to address mounting clinical demands and growing expectations for patient outcomes comparable to developed markets. The adoption landscape is marked by a clear bifurcation: private healthcare networks in major urban centers are leading investments, driven by competitive differentiation and a strategic focus on premium care delivery, while public institutions, constrained by budgetary pressures, are adopting robotics more selectively, often through government pilot programs or international collaborations. Brazil stands out as a strategic hub, hosting a significant share of surgical robotics programs in the region and attracting multinational robotics providers seeking market traction. This leadership reflects not only robust clinical adoption in metropolitan hospitals but also an expanding medical tourism segment where advanced procedural technologies bolster institutional reputation. Mexico, similarly, has seen progressive uptake of robotic systems in high‑volume private hospital networks, with an emphasis on urology and gynecological specialties that align with regional disease burden patterns. Meanwhile, Argentina and Chile are gaining momentum through academic‑industry partnerships that support localized clinical trials and evidence generation, helping to mitigate skepticism around efficacy and cost justification. Despite this positive trajectory, adoption challenges persist. High upfront costs, limited reimbursement frameworks, and disparities in healthcare infrastructure across urban and rural areas temper market expansion. Regulatory environments although improving remain heterogenous across countries, requiring vendors to adopt tailored entry strategies that account for local compliance nuances. Workforce readiness is another critical factor; the availability of trained robotic surgeons and technical support personnel directly influences adoption rates and integration success. Overall, the Latin America Medical Robotics Market is characterized by strategic investments in technology‑enabled care, growing clinical acceptance of robotics, and a competitive landscape shaped by public‑private participation and regional clinical priorities.

Latin America Medical Robotics Market - Strategic Insights:

Get more information on this report

Latin America Medical Robotics Market Segmentation Analysis:

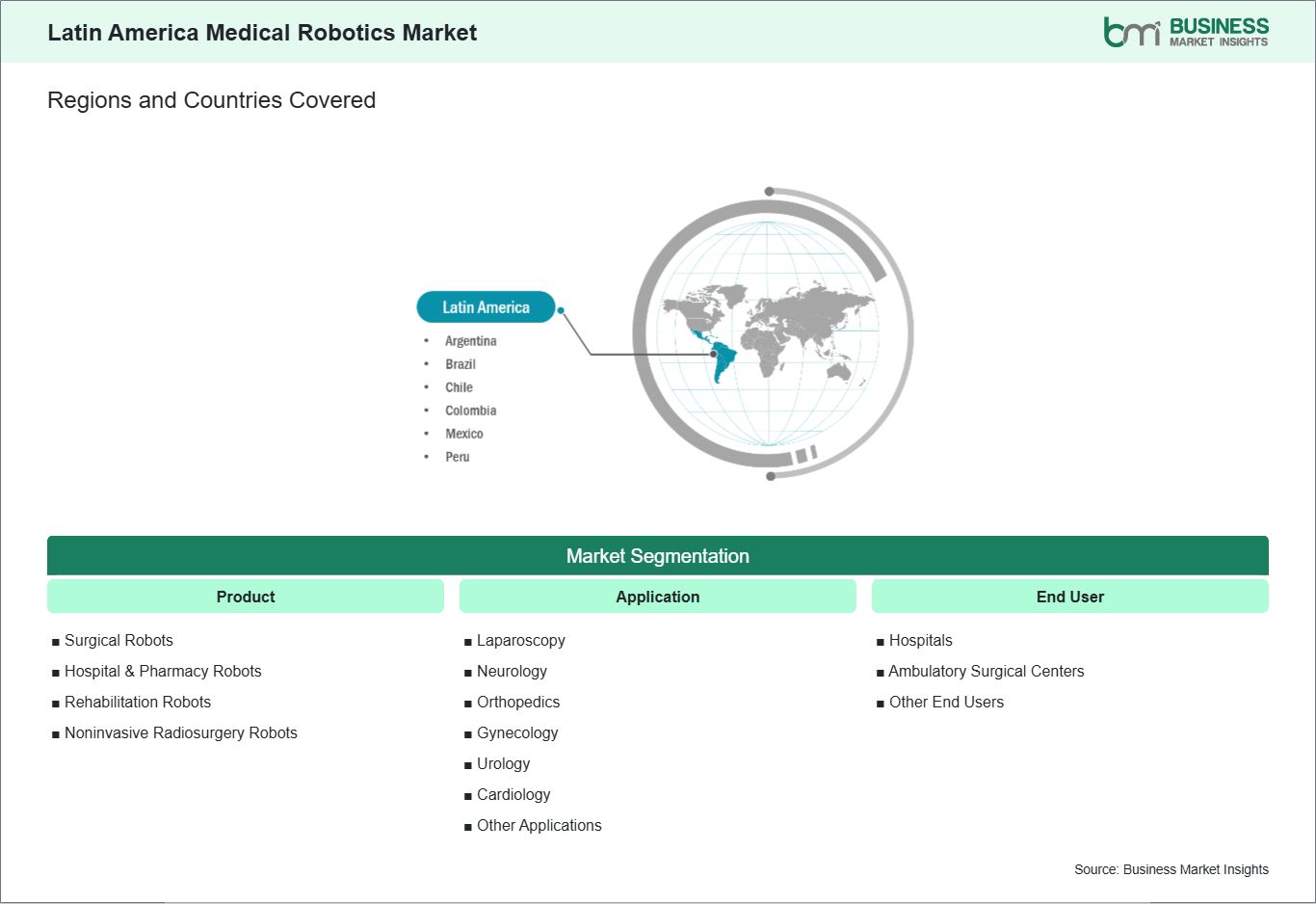

Key segments that contributed to the derivation of the Latin America Medical Robotics Market analysis are product, application, and end user.

By product, the medical robotics market is segmented into surgical robots, hospital & pharmacy robots, rehabilitation robots, and non-invasive radiosurgery robots. The surgical robots segment dominated the market in 2025.

In terms of application, the medical robotics market is categorized into laparoscopy, neurology, orthopedics, gynecology, urology, cardiology, and other applications. The laparoscopy segment dominated the market in 2025.

Based on end user, the medical robotics market is classified into hospitals, ambulatory surgical centers, and other end users. The hospitals segment dominated the market in 2025.

Latin America Medical Robotics Market Drivers and Opportunities:

Increasing government initiatives promoting smart healthcare technologies

Government initiatives in Latin America are playing a key role in promoting smart healthcare technologies, creating favorable conditions for the adoption of medical robotics. Policymakers are increasingly prioritizing digital transformation in healthcare systems, emphasizing the integration of advanced technologies to improve patient care, operational efficiency, and overall clinical outcomes. These initiatives encourage hospitals and healthcare providers to explore robotics as a means to modernize surgical procedures and streamline workflows. The focus on smart healthcare encompasses the deployment of robotic systems that enhance surgical precision, assist in patient monitoring, and support data-driven decision-making. Healthcare authorities are promoting programs that provide guidance, funding, and training for the adoption of these technologies. This fosters an environment where healthcare institutions can implement robotic systems with greater confidence, ensuring that staff are prepared to leverage the full potential of automation in both surgical and clinical care settings. In addition, government support is encouraging the expansion of technology infrastructure, such as digital operating rooms, integrated imaging systems, and connected devices that complement robotic platforms. By aligning healthcare modernization with regulatory frameworks and strategic investment plans, Latin American countries are creating a foundation for sustainable adoption of robotics. These initiatives help accelerate the integration of advanced technologies across both urban and regional healthcare facilities, enabling improved service delivery, enhanced patient safety, and the broader realization of smart healthcare goals throughout the region.

Investment prospects in precision robotic-assisted oncology procedures

Precision robotic-assisted oncology procedures are emerging as a significant investment opportunity in Latin America, driven by the growing demand for minimally invasive cancer treatments. Robotic systems provide enhanced accuracy, improved visualization, and stable instrument control during complex oncological surgeries. This enables surgeons to perform delicate tumor resections and reconstructive procedures with greater confidence, reducing complications and supporting better patient outcomes. The adoption of robotics in oncology also allows hospitals to expand the range of surgical options available to patients, particularly for cancers that require high-precision intervention. By incorporating robotic platforms, healthcare providers can offer less invasive procedures, faster recovery, and improved post-operative care. This focus on precision and efficiency makes robotic-assisted oncology an attractive area for investment, as institutions seek to differentiate their services and deliver high-quality treatment options in a competitive healthcare landscape. Moreover, the growth of robotic-assisted oncology procedures is encouraging collaborations and partnerships within the healthcare sector. Investments are being directed not only toward acquiring advanced robotic systems but also toward training surgeons and integrating technology with hospital workflows. As Latin American healthcare systems continue to prioritize cancer care and precision surgery, the prospects for investment in robotic-assisted oncology are expected to expand steadily. This presents opportunities for both technology providers and healthcare institutions to drive innovation while improving outcomes for patients across the region.

Latin America Medical Robotics Market Size and Share Analysis:

The Latin America medical robotics market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

By product, the surgical robots segment dominated the market in 2025, driven by the rising adoption of technologically advanced robotic systems for precision surgeries.

In terms of application, the laparoscopy segment dominated the market in 2025, driven by the increasing preference for minimally invasive procedures with faster recovery.

Based on end user, the hospitals segment dominated the market in 2025, driven by growing investments in healthcare infrastructure and advanced surgical technologies.

Latin America Medical Robotics Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 1,787.7 Million

Market Size by 2033

US$ 2,951.3 Million

CAGR (2026 - 2033)

6.5%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Surgical Robots

Hospital & Pharmacy Robots

Rehabilitation Robots

Noninvasive Radiosurgery Robots

By Application

Laparoscopy

Neurology

Orthopedics

Gynecology

Urology

Cardiology

Other Applications

By End User

Hospitals

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

Latin America

Mexico, Brazil, Argentina, Peru, Chile, Colombia

Market leaders and key company profiles

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Get more information on this report

Latin America Medical Robotics Market Report Coverage and Deliverables:

The "Latin America Medical Robotics Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Latin America Medical Robotics Market size and forecast at regional and country levels for all market segments covered under the scope

Latin America Medical Robotics Market trends, as well as drivers, restraints, and opportunities

Latin America Medical Robotics Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Latin America Medical Robotics Market

Detailed company profiles, including SWOT analysis

Latin America Medical Robotics Market Geographic Insights:

The geographical scope of the Latin America Medical Robotics Market report is divided into Mexico, Brazil, Argentina, Peru, Chile, and Colombia. Brazil held the largest share in 2025.

Country‑level insights into the Latin America Medical Robotics Market illustrate differentiated adoption patterns shaped by national healthcare priorities, infrastructure maturity, and investment landscapes across Brazil, Mexico, Argentina, Chile, and Colombia. Brazil serves as the dominant market in the region, with tertiary hospitals in Sao Paulo and Rio de Janeiro leading the deployment of advanced robotic systems, particularly in high‑volume specialties such as urology, oncology, and orthopedics. Brazil’s extensive private healthcare network, alongside government‑supported pilot initiatives, has created a robust clinical ecosystem for robotics adoption, establishing the country as a regional hub for procedural innovation and medical tourism. In Mexico, robotics integration is likewise advancing within major private hospital networks, where institutions leverage technology to elevate procedural quality and attract international patients. Mexico’s larger healthcare providers are conducting clinical evidence programs to demonstrate the value of robotics in reducing recovery times and improving long‑term outcomes, which is key to engaging payers and expanding adoption beyond flagship facilities. Argentina exhibits a growing focus on academic‑industry collaborations. Centers of excellence are partnering with robotics manufacturers to conduct localized clinical studies and training programs, which help build clinician confidence and generate region‑specific efficacy data. Similarly, Chile is advancing adoption through strategic investments in metropolitan hospitals, supported by government funding mechanisms aimed at modernizing healthcare infrastructure and improving care quality metrics. Colombia represents an emerging frontier where robotics uptake is gaining traction among private and hybrid public‑private institutions. These facilities are selectively investing in surgical robots for high‑impact procedures as part of broader care quality initiatives, despite budgetary constraints that limit rapid scale. Collectively, these country insights underscore that while Brazil leads in scale and ecosystem maturity, each market presents unique opportunities shaped by clinical priorities, regulatory evolution, and strategic investment choices that influence robotics adoption across the Latin American healthcare landscape.

Get more information on this report

Latin America Medical Robotics Market Research Report Guidance:

The report includes qualitative and quantitative data in the Latin America Medical Robotics Market across product, application, end user and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Latin America Medical Robotics Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Latin America Medical Robotics Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Latin America Medical Robotics Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Latin America Medical Robotics Market segments by product, application, end user and geography across Mexico, Brazil, Argentina, Peru, Chile, and Colombia. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Latin America Medical Robotics Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Latin America Medical Robotics Market News and Key Development:

The Latin America Medical Robotics Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Latin America Medical Robotics Market are:

In December 2024, MicroPort MedBot’s Toumai endoscopic surgical robot received market approval from Brazil’s National Health Surveillance Agency (ANVISA), clearing its commercial use throughout the country. This regulatory milestone marks one of the first dedicated laparoscopic surgical robots authorised in Latin America, expanding access to advanced minimally invasive procedures. The launch event in São Paulo included demonstrations and a remote animal surgery highlighting robotics and telesurgery potential. The approval is expected to drive greater adoption of robot‑assisted surgery across Brazilian hospitals.

In October 2025, the Toumai surgical robot achieved a global rollout milestone with significant orders and deliveries, including installations in Latin America, where hospitals such as Hospital Nove de Julho in Brazil completed the region’s first commercial remote human surgery. This marks an evolution in deploying advanced robotic platforms capable of telesurgery functions across continents. Hospitals in the region are now better positioned to integrate robotics with remote surgical support and training networks. The milestone reflects rising demand and broader acceptance of robotic‑assisted procedures throughout Latin American healthcare systems.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - Latin America Medical Robotics Market

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Frequently Asked Questions

How big is the Latin America Medical Robotics Market?

The Latin America Medical Robotics Market is valued at US$ 1,787.7 Million in 2025, it is projected to reach US$ 2,951.3 Million by 2033.

What is the CAGR for Latin America Medical Robotics Market by (2026 - 2033)?

As per our report Latin America Medical Robotics Market, the market size is valued at US$ 1,787.7 Million in 2025, projecting it to reach US$ 2,951.3 Million by 2033. This translates to a CAGR of approximately 6.5% during the forecast period.

What segments are covered in this report?

The Latin America Medical Robotics Market report typically cover these key segments-

Application (Laparoscopy, Neurology, Orthopedics, Gynecology, Urology, Cardiology, Other Applications)

End User (Hospitals, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for Latin America Medical Robotics Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Latin America Medical Robotics Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Latin America Medical Robotics Market?

The Latin America Medical Robotics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Who should buy this report?

The Latin America Medical Robotics Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Latin America Medical Robotics Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Latin America Medical Robotics Market

Get Free Sample For Latin America Medical Robotics Market