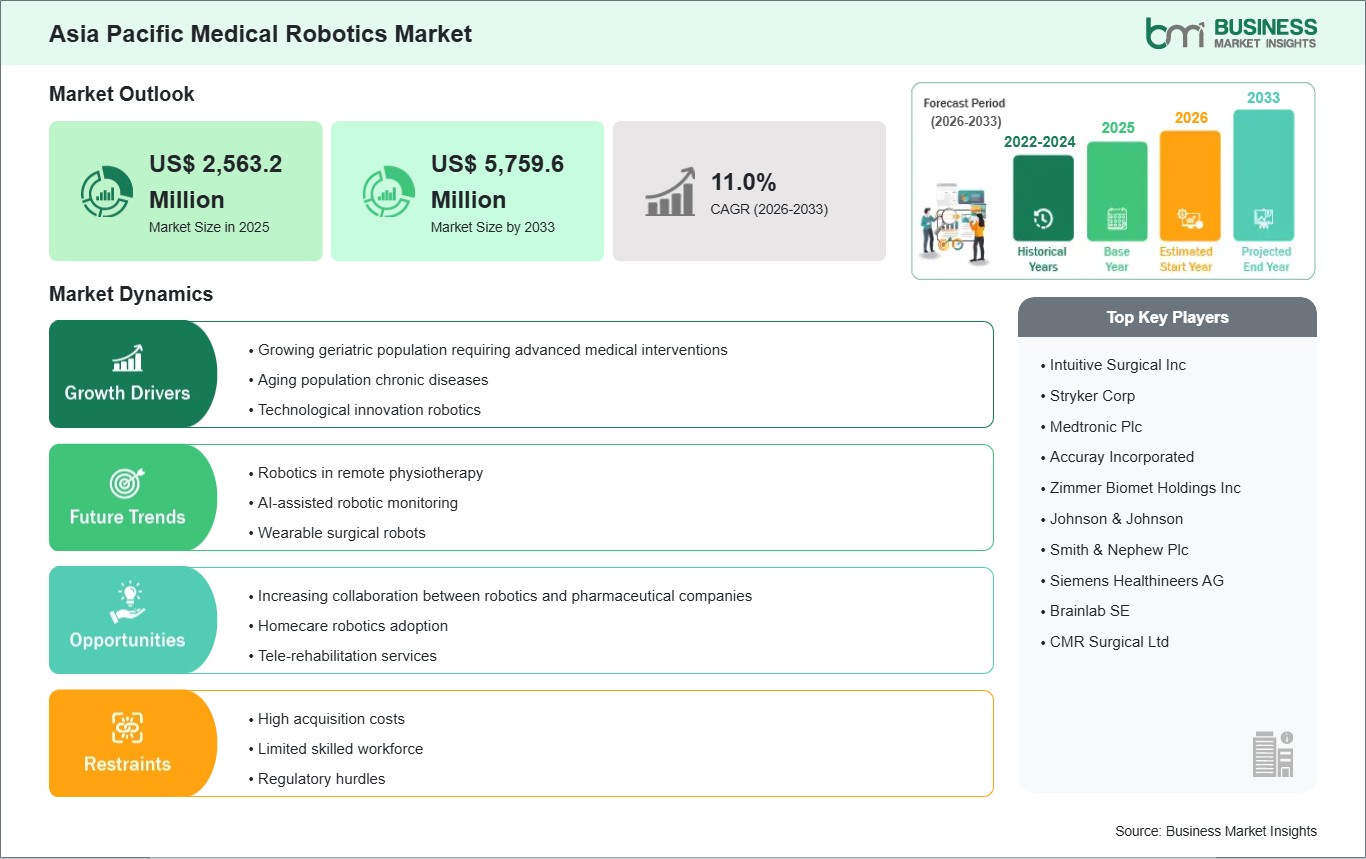

The Asia Pacific medical robotics market size is expected to reach US$ 5,759.6 million by 2033 from US$ 2,563.2 million in 2025. The market is estimated to record a CAGR of 11.0% from 2026 to 2033.

Executive Summary and Asia Pacific Medical Robotics Market Analysis:

The Asia Pacific medical robotics market is transitioning into a core component of the region’s healthcare modernization strategies, driven by rapid integration of precision automation across clinical environments. Healthcare providers in key markets such as China, Japan, and South Korea are increasingly incorporating robotic platforms across surgical, diagnostic, and rehabilitation workflows to improve clinical outcomes while managing rising procedure volumes and workforce shortages. Strategic investments in artificial intelligence, enhanced imaging, and robotic engineering are expanding the application spectrum of medical robots beyond traditional surgical suites into areas such as non‑invasive neurosurgery, elderly care, and hospital automation. Surgical robotic systems, in particular, dominate regional innovation due to their ability to reduce procedural complications, improve dexterity, and enhance patient recovery pathways in complex interventions like urology and oncology. These systems are being increasingly deployed in tertiary hospitals where quality benchmarks and clinical differentiation are critical. However, market growth dynamics exhibit notable asymmetry. Developed APAC healthcare systems benefit from more structured reimbursement frameworks, rigorous regulatory pathways, and clinician training programs that accelerate adoption, whereas emerging markets face challenges associated with infrastructure constraints, funding limitations, and variable regulatory clarity. These differences are prompting stakeholders to pursue differentiated strategies, including tailored financing solutions, local training collaborations, and ecosystem partnerships to build clinical confidence in robotics‑augmented care. Cross‑sector collaborations between healthcare institutions and MedTech innovators are also catalyzing technology transfer and support frameworks essential for integration at scale. As healthcare systems increasingly prioritize patient‑centric outcomes and operational resilience, medical robotics is being positioned as a strategic enabler of long‑term system efficiency and quality care delivery.

Asia Pacific Medical Robotics Market - Strategic Insights:

Get more information on this report

Asia Pacific Medical Robotics Market Segmentation Analysis:

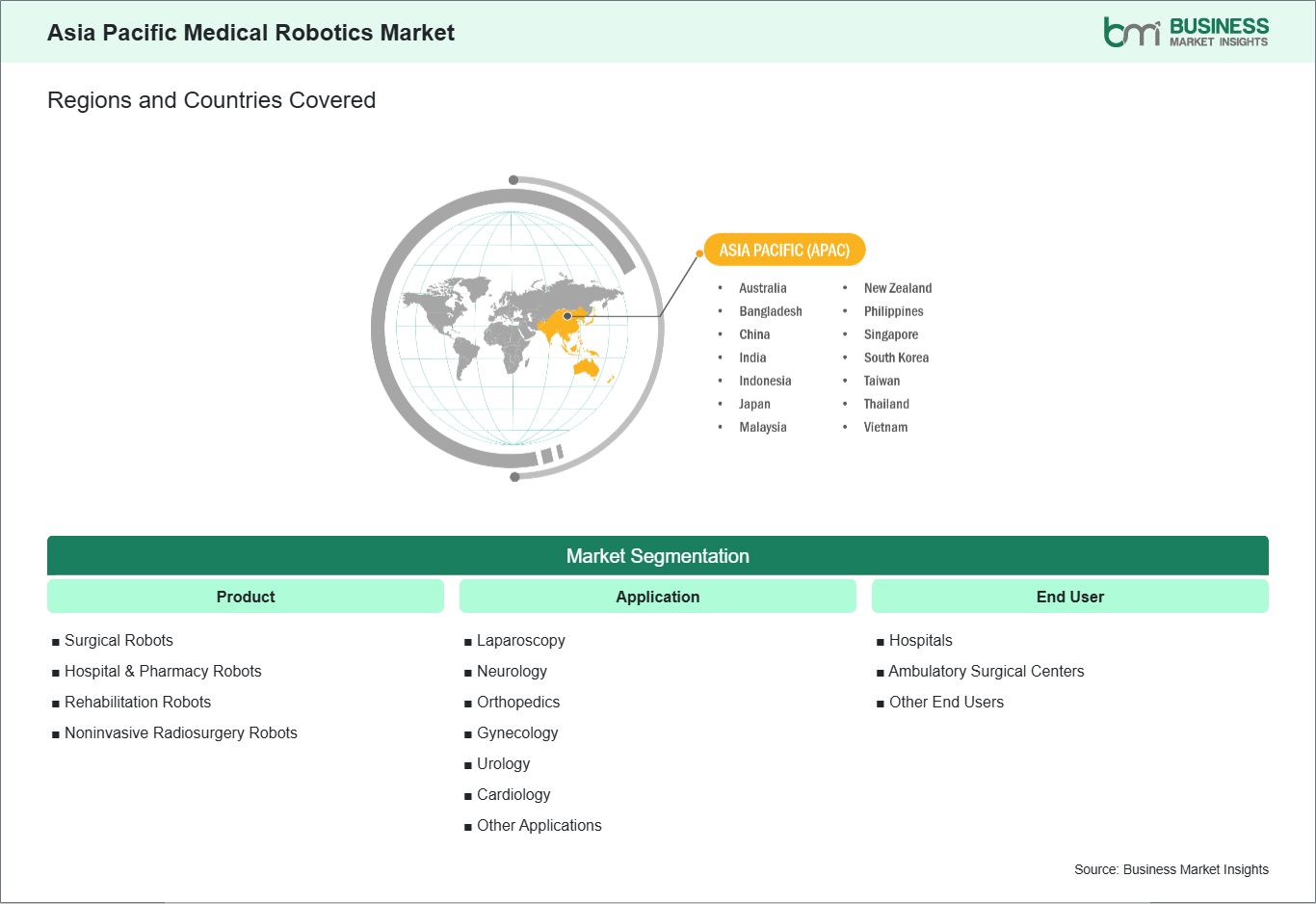

Key segments that contributed to the derivation of the Asia Pacific Medical Robotics Market analysis are product, application, and end user.

By product, the medical robotics market is segmented into surgical robots, hospital & pharmacy robots, rehabilitation robots, and non-invasive radiosurgery robots. The surgical robots segment dominated the market in 2025.

In terms of application, the medical robotics market is categorized into laparoscopy, neurology, orthopedics, gynecology, urology, cardiology, and other applications. The laparoscopy segment dominated the market in 2025.

Based on end user, the medical robotics market is classified into hospitals, ambulatory surgical centers, and other end users. The hospitals segment dominated the market in 2025.

Asia Pacific Medical Robotics Market Drivers and Opportunities:

Growing geriatric population requiring advanced medical interventions

The Asia Pacific region is experiencing a significant demographic transition marked by a rapidly increasing elderly population, which directly influences the demand for sophisticated healthcare services, including medical robotics. Projections suggest that by 2050, about one in four people in the Asia Pacific will be over 60 years old, representing more than 1.3 billion older adults. This shift is particularly pronounced in countries such as Japan, China, and South Korea, where the proportion of citizens aged 65 + is high and continuing to rise. In Japan, the elderly segment has expanded substantially, leading to higher surgical volumes for age‑associated conditions like prostate cancer and gastrointestinal disorders that benefit from robotic precision and minimally invasive approaches. Similarly, China’s population segments above 60 are expected to exceed 300 million by 2030, increasing the need for advanced interventions across cardiac, urological, and oncological care where robot‑assisted systems can enhance outcomes. Hospitals across the Asia Pacific are responding to these demographic changes by incorporating more robotic systems into surgical and rehabilitative care pathways. In India, for example, facilities like CK Birla Hospital have installed fourth‑generation robotic surgery platforms to support complex procedures, demonstrating how aging‑related healthcare needs are shaping technology adoption. Other nations such as Singapore and Australia are investing in robotics not only for surgery but also for elderly care, including autonomous delivery and assistive robots to support nursing workflows. These investments help manage the increased procedural demand from older patients while also addressing workforce shortages in caregiving and acute care settings—a dual challenge in aging communities. The demand for robotics in the Asia Pacific is also reinforced by rising chronic diseases that disproportionately affect older adults, such as cardiovascular disease and diabetes, which often require repeat or complex surgeries. As minimally invasive and robot‑assisted techniques become more established, they are increasingly preferred by both clinicians and patients due to benefits like smaller incisions, reduced recovery times, and higher precision. In countries like China and Japan, surgical robots are now routinely used in urology and oncologic procedures, reflecting how demographic trends correlate with technology adoption. With governments and healthcare systems emphasizing improved quality of care for aging populations, investments in both robotic infrastructure and surgeon training are expected to grow throughout the region.

Increasing collaboration between robotics and pharmaceutical companies

In the Asia Pacific, collaboration between medical robotics developers and pharmaceutical companies is emerging as a transformative trend that enhances capabilities across drug discovery, manufacturing, and clinical care pathways. Pharmaceutical firms and robotics technology providers are partnering to bring automation to complex laboratory and production tasks that were previously labor‑intensive and error‑prone. For instance, collaborations involving automated robotic systems for drug formulation and preparation are increasingly visible in China’s pharmaceutical manufacturing sector, where robots are programmed to mix and prepare chemotherapy drugs with high precision. These joint efforts improve efficiency, boost quality control, and reduce risks associated with manual handling in sterile environments, addressing critical needs in high‑volume drug manufacturing. Robotics collaborations are not limited to production lines; they extend into pharmaceutical R&D workflows. Across the region, there is a growing emphasis on integrating robotic automation and data analytics in laboratories to accelerate compound screening, sample handling, and chemical synthesis. This is particularly relevant in nations such as Japan and South Korea, where pharmaceutical research institutions and robotics firms jointly develop advanced lab‑automation platforms to shorten drug discovery cycles. These collaborations leverage robotics for repetitive tasks, freeing researchers to focus on experiment design and interpretation while improving throughput and reproducibility—a key factor in competitive drug development. Beyond manufacturing and R&D, Asia Pacific collaborations also extend into clinical and pharmaceutical service delivery. Robotics is increasingly utilized in pharmacy automation, with robotics‑assisted prescription filling and AI‑enabled drug interaction alerts enhancing medication safety and operational efficiency in busy pharmacies in China, Indonesia, and the Philippines. These integrated solutions, combining pharmaceutical expertise with robotics precision, help decentralize pharmacy services and support high patient volumes while reducing errors. Additionally, robotics partnerships that focus on hospital logistics, inspection, and quality assurance further demonstrate how multidisciplinary collaboration can streamline the entire lifecycle of pharmaceutical products—from development and production to patient delivery.

Asia Pacific Medical Robotics Market Size and Share Analysis:

The Asia Pacific medical robotics market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

By product, the surgical robots segment dominated the market in 2025, driven by strong adoption of robotic systems for minimally invasive and complex surgeries across major Asia Pacific healthcare facilities.

In terms of application, the laparoscopy segment dominated the market in 2025, driven by increasing use of robotic‑assisted laparoscopic procedures that offer better precision, reduced trauma, and faster recovery in high‑volume surgical applications.

Based on end user, the hospitals segment dominated the market in 2025, driven by their advanced infrastructure, high surgical workloads and ability to absorb investment in costly robotic technologies.

Asia Pacific Medical Robotics Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 2,563.2 Million

Market Size by 2033

US$ 5,759.6 Million

CAGR (2026 - 2033)

11.0%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Surgical Robots

Hospital & Pharmacy Robots

Rehabilitation Robots

Noninvasive Radiosurgery Robots

By Application

Laparoscopy

Neurology

Orthopedics

Gynecology

Urology

Cardiology

Other Applications

By End User

Hospitals

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

Asia Pacific

China, India, Japan, Australia, Bangladesh, Indonesia, Malaysia, New Zealand, Philippines, Singapore, South Korea, Taiwan, Thailand, Vietnam

Market leaders and key company profiles

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Get more information on this report

Asia Pacific Medical Robotics Market Report Coverage and Deliverables:

The "Asia Pacific Medical Robotics Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Asia Pacific Medical Robotics Market size and forecast at regional and country levels for all market segments covered under the scope

Asia Pacific Medical Robotics Market trends, as well as drivers, restraints, and opportunities

Asia Pacific Medical Robotics Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Asia Pacific Medical Robotics Market

Detailed company profiles, including SWOT analysis

Asia Pacific Medical Robotics Market Geographic Insights:

The geographical scope of the Asia Pacific Medical Robotics Market report is divided into China, India, Japan, Australia, Bangladesh, Indonesia, Malaysia, New Zealand, Philippines, Singapore, South Korea, Taiwan, Thailand, and Vietnam. China held the largest share in 2025.

Country‑level insights into the Asia Pacific Medical Robotics Market reflect heterogeneous adoption patterns shaped by healthcare infrastructure maturity, regulatory ecosystems, and strategic priorities across key economies including China, Japan, India, South Korea, and Australia. China stands out as the dominant market in the region, driven by aggressive hospital modernization initiatives, expansive middle‑class healthcare demand, and strong government incentives that support advanced medical equipment deployment. China’s robust domestic manufacturing ecosystem and strategic collaborations with multinational robotics innovators have also accelerated clinical utilization of medical robotic systems in major tertiary care centers, particularly for oncology, laparoscopy, and minimally invasive procedures. In Japan, high healthcare quality standards, a well‑established insurance framework, and an aging demographic have driven early and sustained adoption of robotic-assisted surgery, especially in specialties like urology, orthopedics, and cardiovascular interventions. Japan’s strategic focus on integrating precision technologies has fostered a mature clinical environment for robotics testing and refinement, which in turn attracts supplementary R&D investments. India is emerging as one of the fastest growing markets for medical robotics in APAC, supported by rising healthcare expenditure, medical tourism growth, and hospital investments in surgical automation. While adoption varies by region due to differing regulatory and reimbursement landscapes, leading hospital chains in metropolitan centers are pioneering integration of robotic systems to improve quality and competitiveness. South Korea and Australia also exhibit progressive adoption trends. South Korea’s innovation ecosystem, combined with structured public health initiatives, is enabling earlier integration of robotics amplified by technology export synergies. Australia’s advanced healthcare infrastructure supports strategic deployment in major hospital networks, with a growing focus on robotic rehabilitation and clinical support applications. Across these markets, strategic priorities include clinician training, interoperability standards, and scalable deployment frameworks that align robotics adoption with national health outcomes and long‑term healthcare sustainability goals.

Get more information on this report

Asia Pacific Medical Robotics Market Research Report Guidance:

The report includes qualitative and quantitative data in the Asia Pacific Medical Robotics Market across product, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Asia Pacific Medical Robotics Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Asia Pacific Medical Robotics Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Asia Pacific Medical Robotics Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Asia Pacific Medical Robotics Market segments by product, application, end user, and geography across China, India, Japan, Australia, Bangladesh, Indonesia, Malaysia, New Zealand, Philippines, Singapore, South Korea, Taiwan, Thailand, and Vietnam. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Asia Pacific Medical Robotics Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Asia Pacific Medical Robotics Market News and Key Development:

The Asia Pacific Medical Robotics Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Asia Pacific Medical Robotics Market are:

In September 2025, Indian company Meril unveiled the Mizzo Endo 4000, a next‑generation soft‑tissue robotic surgical system designed to enhance precision in minimally invasive procedures across specialties like general surgery, gynecology and urology. This represents a major Asia‑Pacific launch of an indigenously developed robotic platform aimed at improving surgical accuracy and widening patient access to advanced robotic care. The system’s advanced capabilities are seen as elevating India’s role in global medical robotics innovation. Its introduction underscores rising regional competition in surgical robotics technology deployment.

In September 2025, HMI Medical Group introduced Japan’s Hinotori robotic‑assisted surgery systems in Malaysia at hospitals including Regency Specialist Hospital and Mahkota Medical Centre, making this the first Japanese RAS launch in the private healthcare sector in Southeast Asia. The platform enhances surgical precision and control for complex procedures and underscores growing regional adoption of advanced robotics. This launch positioned Malaysia as a key ASEAN hub for high‑end surgical robotics.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - Asia Pacific Medical Robotics Market

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Frequently Asked Questions

How big is the Asia Pacific Medical Robotics Market?

The Asia Pacific Medical Robotics Market is valued at US$ 2,563.2 Million in 2025, it is projected to reach US$ 5,759.6 Million by 2033.

What is the CAGR for Asia Pacific Medical Robotics Market by (2026 - 2033)?

As per our report Asia Pacific Medical Robotics Market, the market size is valued at US$ 2,563.2 Million in 2025, projecting it to reach US$ 5,759.6 Million by 2033. This translates to a CAGR of approximately 11.0% during the forecast period.

What segments are covered in this report?

The Asia Pacific Medical Robotics Market report typically cover these key segments-

Application (Laparoscopy, Neurology, Orthopedics, Gynecology, Urology, Cardiology, Other Applications)

End User (Hospitals, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for Asia Pacific Medical Robotics Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Medical Robotics Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Asia Pacific Medical Robotics Market?

The Asia Pacific Medical Robotics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Who should buy this report?

The Asia Pacific Medical Robotics Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Asia Pacific Medical Robotics Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Asia Pacific Medical Robotics Market

Get Free Sample For Asia Pacific Medical Robotics Market