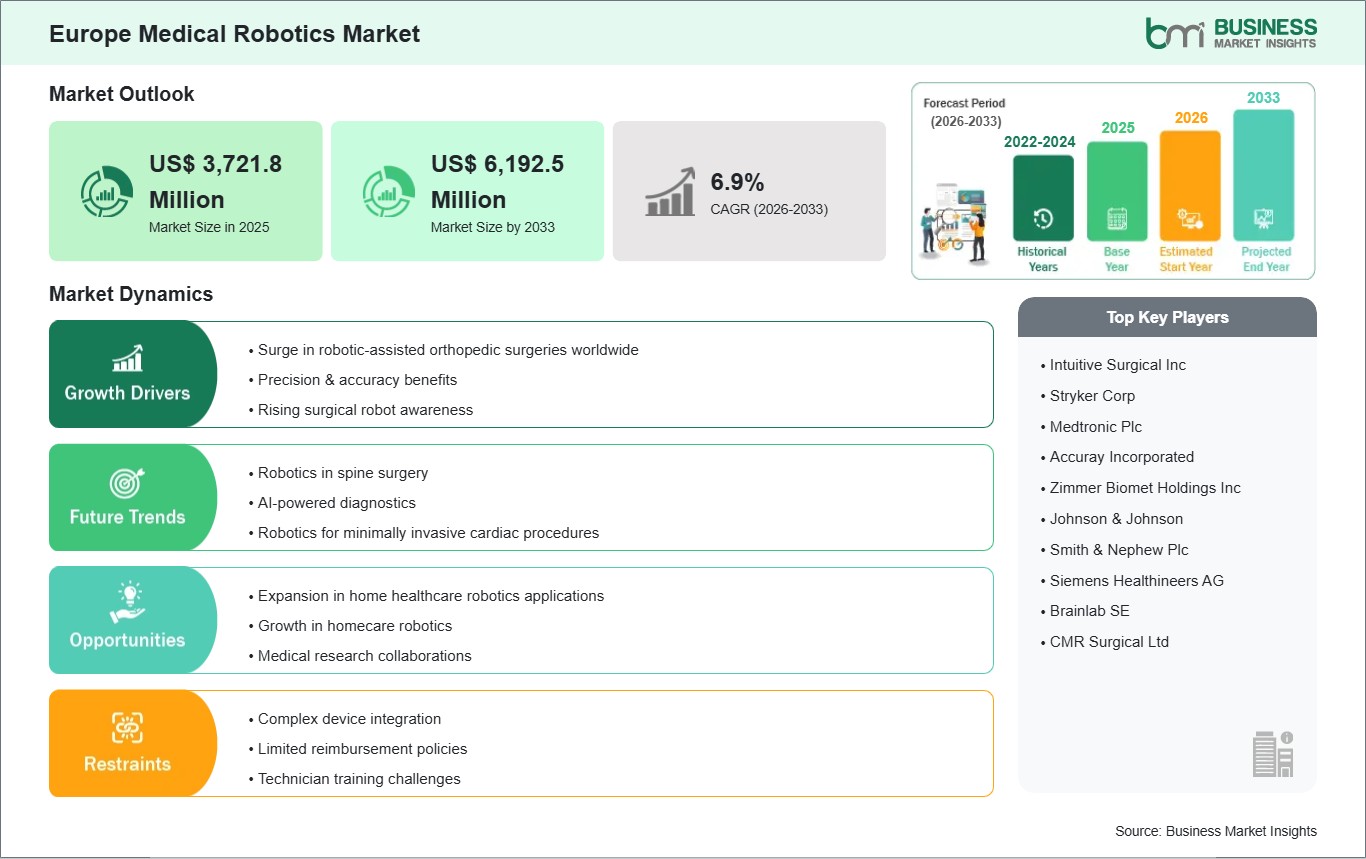

The Europe medical robotics market size is expected to reach US$ 6,192.5 million by 2033 from US$ 3,721.8 million in 2025. The market is estimated to record a CAGR of 6.9% from 2026 to 2033.

Executive Summary and Europe Medical Robotics Market Analysis:

The Europe medical robotics market is witnessing a period of accelerated evolution driven by advanced healthcare infrastructure, rising patient demand for minimally invasive procedures, and growing emphasis on precision medicine. Across Western and Central Europe, hospitals and specialty clinics are increasingly integrating robotic-assisted systems to enhance surgical accuracy, reduce procedure times, and improve post-operative recovery. Surgical robotics, particularly in urology, cardiothoracic surgery, and orthopedics, remains the primary adoption area, while ancillary domains such as rehabilitation and hospital logistics are emerging. These trends reflect a broader strategy to improve operational efficiency, enhance patient satisfaction, and maintain competitive differentiation among private and public healthcare providers. Market growth is further propelled by strong collaborations between global robotics manufacturers, European research institutions, and clinical centers, fostering innovation in AI-enabled surgical planning, robotic navigation, and haptic feedback systems. Regulatory frameworks harmonized under EU medical device directives facilitate smoother market entry, ensuring safety and interoperability across multiple countries. Moreover, healthcare payers and insurance providers increasingly evaluate robotics adoption based on demonstrated improvements in clinical outcomes, driving hospitals to invest in systems that provide measurable benefits in efficiency and quality of care. Challenges persist, including high capital investment requirements, the need for extensive clinician training, and integration complexities with legacy hospital IT systems. To mitigate these challenges, healthcare providers are exploring flexible procurement strategies, such as leasing models, outcome-based contracts, and shared-service platforms. Additionally, the adoption of digital twins and simulation-based training is enhancing workforce readiness, ensuring that surgeons and support staff can effectively utilize robotic systems. Overall, Europe’s medical robotics market reflects a mature ecosystem focused on innovation, operational efficiency, and patient-centric care, with sustained growth anticipated as technology integration deepens across surgical and clinical workflows.

Europe Medical Robotics Market - Strategic Insights:

Get more information on this report

Europe Medical Robotics Market Segmentation Analysis:

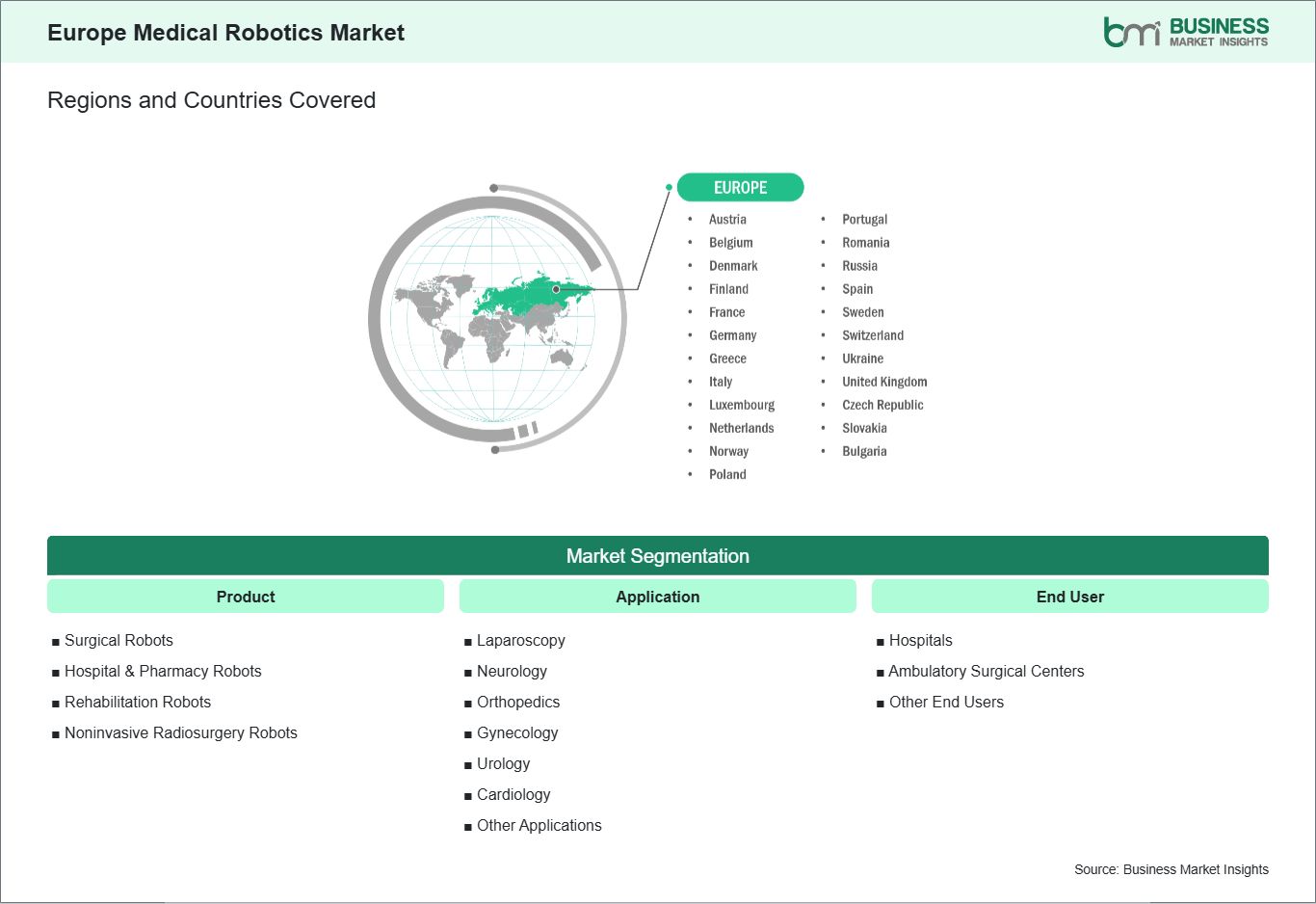

Key segments that contributed to the derivation of the Europe Medical Robotics Market analysis are product, application, and end user.

By product, the medical robotics market is segmented into surgical robots, hospital & pharmacy robots, rehabilitation robots, and non-invasive radiosurgery robots. The surgical robots segment dominated the market in 2025.

In terms of application, the medical robotics market is categorized into laparoscopy, neurology, orthopedics, gynecology, urology, cardiology, and other applications. The laparoscopy segment dominated the market in 2025.

Based on end user, the medical robotics market is classified into hospitals, ambulatory surgical centers, and other end users. The hospitals segment dominated the market in 2025.

Europe Medical Robotics Market Drivers and Opportunities:

Surge in robotic-assisted orthopedic surgeries worldwide

Robotic-assisted orthopedic surgeries are becoming an integral part of healthcare systems in Europe. Hospitals and surgical centers are increasingly recognizing the value of robotic technology in improving surgical precision and enhancing patient outcomes. Robotic systems allow surgeons to perform complex procedures with higher accuracy, reducing the risk of errors and supporting consistent results. The integration of robotics in orthopedic surgery provides greater control over instrument movements and improves alignment during procedures, which contributes to faster patient recovery and a more efficient surgical workflow. The adoption of robotic systems is also transforming the role of orthopedic surgeons. With the assistance of robotics, surgeons can plan procedures more effectively, simulate surgical steps, and execute operations with minimal variability. This enables them to focus on critical decisions while relying on robotic precision for routine aspects of surgery. As a result, surgical teams can improve overall efficiency and reduce fatigue, allowing healthcare facilities to maintain high-quality care even under increasing patient demand. The emphasis on precision and reliability is gradually reshaping surgical practices in Europe. Furthermore, robotic-assisted orthopedic surgery is supporting the move toward minimally invasive techniques. These systems allow for smaller incisions and more controlled movements, reducing tissue damage and accelerating patient recovery. Hospitals are increasingly viewing robotic surgery as a strategic investment that not only enhances clinical outcomes but also improves patient satisfaction. As technology continues to advance and surgical teams become more familiar with robotic workflows, the use of robotics in orthopedic procedures is expected to expand further, setting a new standard for care in the region.

Expansion in home healthcare robotics applications

Home healthcare robotics is emerging as a key growth area in Europe, driven by the need to support patients outside traditional hospital settings. Robotics can assist individuals with daily activities, provide basic medical monitoring, and support mobility, creating a safer and more comfortable environment for home care. These systems are increasingly being integrated with healthcare services to offer practical solutions that reduce the reliance on caregivers while maintaining a high level of patient independence and well-being. The expansion of home healthcare robotics also reflects a broader trend toward personalized care. Robots can be tailored to the needs of individuals, providing support for rehabilitation exercises, medication reminders, or routine health checks. This personalized approach enables patients to maintain a higher level of engagement with their care plans and encourages consistent adherence to treatment recommendations. By combining assistance with monitoring capabilities, home robotics helps bridge the gap between professional healthcare oversight and daily patient needs. In addition, home healthcare robotics supports the efficiency of healthcare systems by reducing unnecessary hospital visits and enabling care to be delivered remotely. Robots can assist patients while allowing healthcare providers to track progress and intervene when necessary, improving the continuity of care. The integration of robotics into home care services also strengthens the overall patient experience by promoting independence, safety, and convenience. As technology develops, home healthcare robotics is expected to become a standard component of care delivery in Europe, complementing traditional healthcare services and supporting patients in living healthier, more independent lives.

Europe Medical Robotics Market Size and Share Analysis:

The Europe medical robotics market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

By product, the surgical robots segment dominated the market in 2025, driven by increasing adoption of advanced robotic systems that enhance precision, safety and efficiency across minimally invasive procedures throughout Europe.

In terms of application, the laparoscopy segment dominated the market in 2025, driven by strong preference for robot‑assisted minimally invasive laparoscopic surgeries that deliver better clinical outcomes and faster patient recovery.

Based on end user, the hospitals segment dominated the market in 2025, driven by their advanced infrastructure, high surgical volumes and capacity to invest in costly robotic technologies for improved patient care.

Europe Medical Robotics Market Report Coverage and Deliverables:

The "Europe Medical Robotics Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Europe Medical Robotics Market size and forecast at regional and country levels for all market segments covered under the scope

Europe Medical Robotics Market trends, as well as drivers, restraints, and opportunities

Europe Medical Robotics Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Europe Medical Robotics Market

Detailed company profiles, including SWOT analysis

Europe Medical Robotics Market Geographic Insights:

The geographical scope of the Europe Medical Robotics Market report is divided into Belgium, Austria, Finland, Denmark, Greece, Poland, Romania, Russia, Ukraine, the Czech Republic, Slovakia, Bulgaria, Italy, Luxembourg, Germany, Switzerland, France, the Netherlands, Norway, Portugal, Spain, Sweden, and the UK. Germany held the largest share in 2025.

Country-level insights into the Europe Medical Robotics Market reveal diverse adoption dynamics across Germany, France, the United Kingdom, Italy, and Spain, shaped by healthcare infrastructure, regulatory frameworks, and investment priorities. Germany is a leading market, with tertiary hospitals and specialized centers deploying advanced robotic systems for urology, orthopedic, and cardiothoracic surgeries. The country’s strong focus on precision medicine and high R&D expenditure supports the development of AI-integrated surgical platforms and continuous innovation. In France, robotics adoption is supported by a well-structured healthcare system and national strategies for hospital modernization. French hospitals are increasingly utilizing robotic systems to enhance surgical efficiency, improve clinical outcomes, and reduce hospital stays, particularly in urban academic centers. The United Kingdom has seen rapid integration of robotics, particularly in private hospital networks and teaching hospitals. Emphasis is placed on minimally invasive surgery and tele-mentoring platforms, aligning with broader NHS goals of improving care quality while optimizing resource utilization. In Italy, adoption is concentrated in major metropolitan hospitals, focusing on high-complexity surgical procedures such as oncology and cardiovascular interventions. Investments are guided by regional health authorities and university hospital collaborations. Spain demonstrates a balanced approach, combining public and private adoption to expand minimally invasive surgical capabilities while piloting robotics-assisted rehabilitation programs. Collaborative initiatives between hospitals, universities, and robotics manufacturers are enhancing workforce readiness and accelerating clinical integration. Overall, Europe’s country-level landscape reflects a mature, innovation-driven market where adoption strategies are tailored to national healthcare priorities, infrastructure capabilities, and patient demand. Germany and the United Kingdom emerge as leading hubs for robotics deployment, while France, Italy, and Spain are scaling integration through targeted investments, clinical collaborations, and digital health alignment, collectively driving regional growth and technological leadership.

Get more information on this report

Europe Medical Robotics Market Research Report Guidance:

The report includes qualitative and quantitative data in the Europe Medical Robotics Market across product, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Europe Medical Robotics Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Europe Medical Robotics Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Europe Medical Robotics Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Europe Medical Robotics Market segments by product, application, end user, and geography across into Belgium, Austria, Finland, Denmark, Greece, Poland, Romania, Russia, Ukraine, the Czech Republic, Slovakia, Bulgaria, Italy, Luxembourg, Germany, Switzerland, France, the Netherlands, Norway, Portugal, Spain, Sweden, and the UK. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Europe Medical Robotics Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Europe Medical Robotics Market News and Key Development:

The Europe Medical Robotics Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Europe Medical Robotics Market are:

In July 2025, Intuitive Surgical’s da Vinci 5 robotic surgical system received CE mark approval for use across Europe in a broad range of adult and pediatric minimally invasive procedures, including urology, gynecology, and general laparoscopic surgery. This regulatory milestone allows hospitals throughout the EU to begin clinical deployment of the latest generation surgical robot with enhanced precision and controls. The clearance underscores continued adoption of advanced surgical robotics in European healthcare. With wider roll‑out planned, the system aims to expand access to next‑gen robotic‑assisted surgery.

In September 2025, Surgerii Robotics’ Shurui single‑port surgical robot secured CE certification for the European market, marking one of the first single‑port robotic platforms approved for clinical use in Europe. The system’s compact single‑incision design supports complex laparoscopic procedures with reduced invasiveness and has already been used in hundreds of surgeries globally. This milestone enhances the portfolio of minimally invasive surgical robots available to European hospitals. Its approval is expected to stimulate broader adoption of single‑port robotic surgery across the continent.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - Europe Medical Robotics Market

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Frequently Asked Questions

How big is the Europe Medical Robotics Market?

The Europe Medical Robotics Market is valued at US$ 3,721.8 Million in 2025, it is projected to reach US$ 6,192.5 Million by 2033.

What is the CAGR for Europe Medical Robotics Market by (2026 - 2033)?

As per our report Europe Medical Robotics Market, the market size is valued at US$ 3,721.8 Million in 2025, projecting it to reach US$ 6,192.5 Million by 2033. This translates to a CAGR of approximately 6.9% during the forecast period.

What segments are covered in this report?

The Europe Medical Robotics Market report typically cover these key segments-

Application (Laparoscopy, Neurology, Orthopedics, Gynecology, Urology, Cardiology, Other Applications)

End User (Hospitals, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for Europe Medical Robotics Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Medical Robotics Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Europe Medical Robotics Market?

The Europe Medical Robotics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Who should buy this report?

The Europe Medical Robotics Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Europe Medical Robotics Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Europe Medical Robotics Market

Get Free Sample For Europe Medical Robotics Market