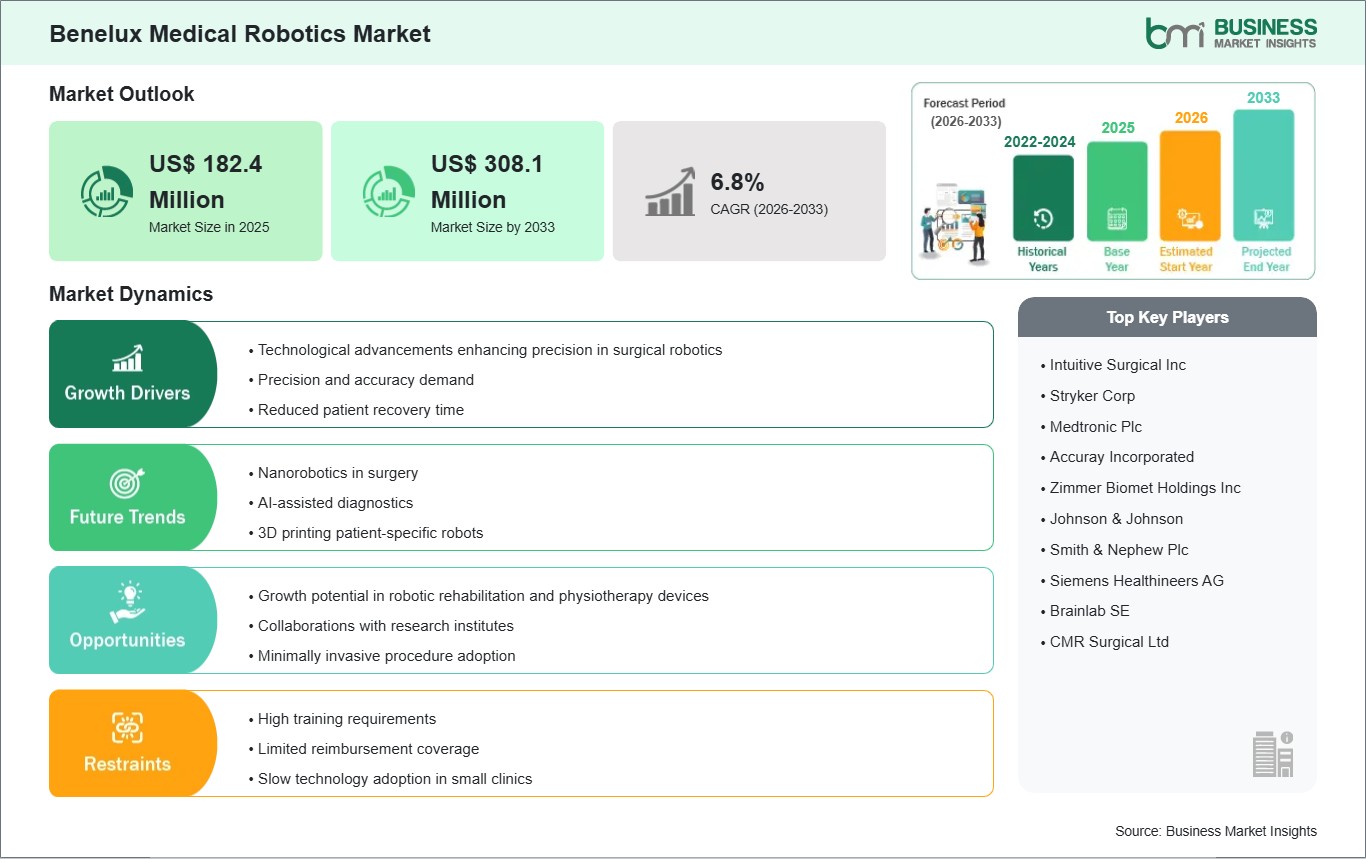

The Benelux medical robotics market size is expected to reach US$ 308.1 million by 2033 from US$ 182.4 million in 2025. The market is estimated to record a CAGR of 6.8% from 2026 to 2033.

Executive Summary and Benelux Medical Robotics Market Analysis:

The Benelux medical robotics market is evolving within a broader European context where advanced healthcare systems and an innovation-centric approach are accelerating the adoption of robotic technologies across clinical settings. Hospitals and specialty care centers in Belgium, the Netherlands, and Luxembourg are increasingly investing in robotic platforms especially in precision surgical systems, minimally invasive robotic assistance, and procedural automation that enhance clinical accuracy and operational performance. This trend is supported by well-established healthcare structures, robust digital infrastructure, and a high degree of integration between public and private healthcare provision, which collectively create a conducive environment for sophisticated robotics deployments. Belgium, for example, has seen the introduction of next-generation surgical systems in multispecialty programs, underscoring a regional commitment to value-based care and patient outcomes improvement through robotics integration. From a strategic standpoint, regional stakeholders are pursuing differentiated growth paths: private hospitals prioritize adoption for competitive differentiation and clinical quality enhancement, while public healthcare networks focus on cost-efficiency, staff optimization, and reducing inpatient recovery times a prime driver for robotics in high-volume surgical workflows. The Benelux market also benefits from strong academic-industry linkages that support pilot programs and clinical validation initiatives, providing early exposure to emerging robotics technologies and data-driven performance analysis. Regulatory alignment with EU medical device directives further facilitates smoother pathways for introduction and evaluation of new robotic platforms. However, the market faces constraints common to advanced robotics adoption: high upfront capital requirements, the need for workforce training in robotics operation and maintenance, and interoperability challenges with legacy hospital IT systems. To balance these challenges, healthcare providers are exploring hybrid financing models such as outcome-based payments and shared services agreements to distribute risk. In aggregate, the market’s strategic emphasis on clinical efficacy, quality assurance, and integrated care delivery positions Benelux as a significant contributor to Europe’s medical robotics innovation landscape, even as adoption remains calibrated to long-term institutional value and system sustainability.

Benelux Medical Robotics Market - Strategic Insights:

Get more information on this report

Benelux Medical Robotics Market Segmentation Analysis:

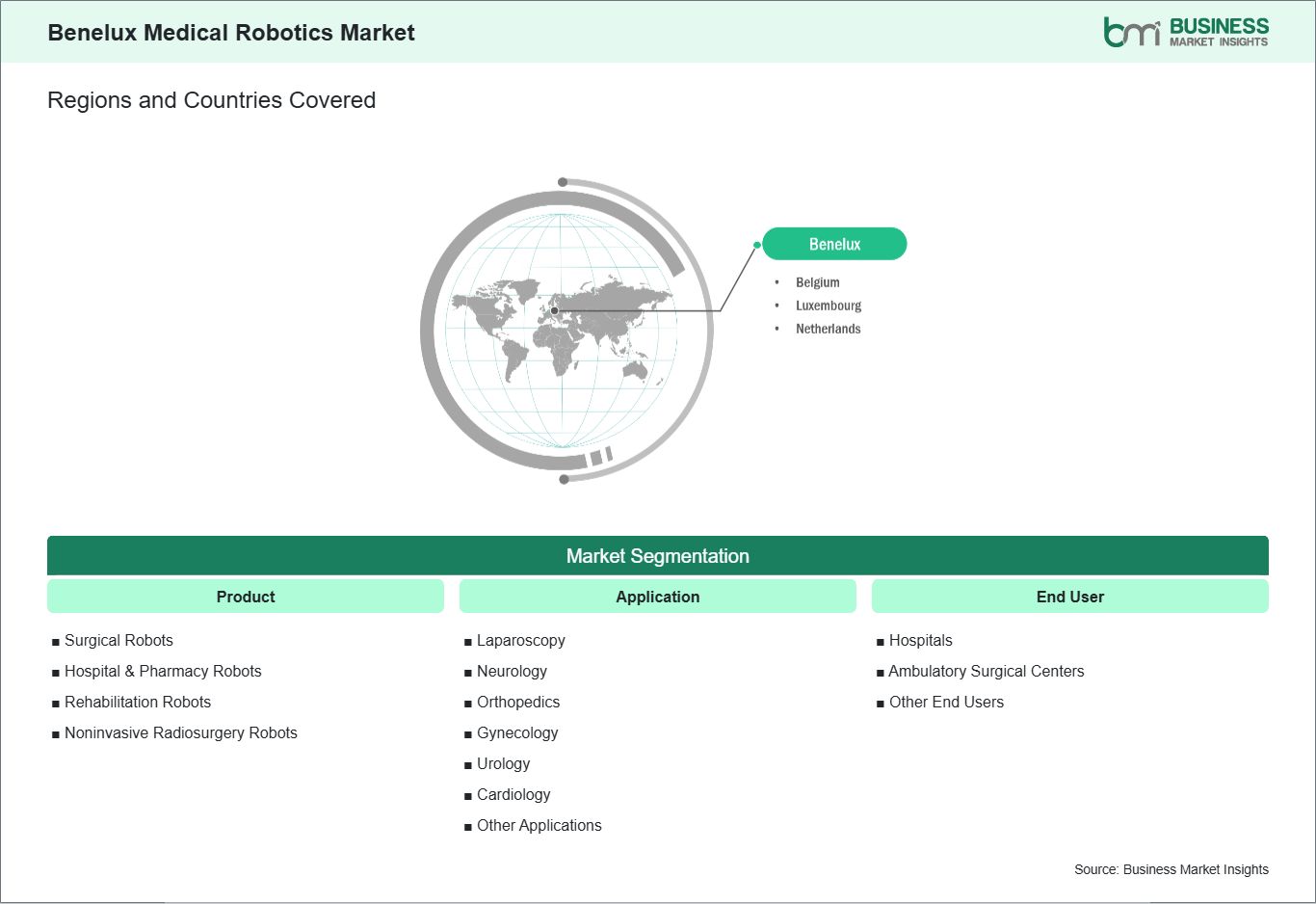

Key segments that contributed to the derivation of the Benelux Medical Robotics Market analysis are product, application, and end user.

By product, the medical robotics market is segmented into surgical robots, hospital & pharmacy robots, rehabilitation robots, and non-invasive radiosurgery robots. The surgical robots segment dominated the market in 2025.

In terms of application, the medical robotics market is categorized into laparoscopy, neurology, orthopedics, gynecology, urology, cardiology, and other applications. The laparoscopy segment dominated the market in 2025.

Based on end user, the medical robotics market is classified into hospitals, ambulatory surgical centers, and other end users. The hospitals segment dominated the market in 2025.

Benelux Medical Robotics Market Drivers and Opportunities:

Technological advancements enhancing precision in surgical robotics

In the Asia Pacific medical robotics market, recent technological advancements are significantly improving the precision and capabilities of surgical robotic systems used in hospitals and specialty clinics. Innovations such as enhanced 3D visualization, AI-guided instrumentation, and advanced robotic arm mechanics have enabled surgeons to perform intricate procedures with greater accuracy and control than traditional methods. In Japan and China, hospitals are adopting platforms that integrate real-time imaging with robotic guidance, allowing for better identification of tissue boundaries and vital structures during operations. This increased situational awareness directly contributes to more controlled and consistent surgical outcomes, particularly in complex specialties like urology and gynecological surgery, where millimeter-level precision can influence both operative success and recovery times. Several Asia Pacific healthcare systems are also piloting next-generation surgical technologies that combine robotics with machine learning and sensor fusion. For example, hospitals in South Korea have begun trialing systems that use real-time data analytics to refine instrument movement patterns and reduce motion variability during delicate tasks. These systems help balance surgeon inputs with autonomous stabilization features that filter tremor and offer smoother instrument articulation. By integrating haptic feedback and predictive analytics, these platforms can alert surgeons in real time to potential deviations, enabling adjustments that further elevate procedural precision. Such advancements are crucial in specialties like pediatric, cardiac, and neurosurgery, where even slight deviations could increase risk or prolong recovery. Regional innovation extends beyond hardware upgrades to include enhanced training and simulation tools that prepare surgicaleams for high-precision tasks. In India and China, many leading medical universities have introduced sophisticated surgical robotics simulators that replicate real-world robotic procedures in virtual environments. These simulators immerse clinicians in varied surgical scenarios, allowing them to refine precision skills before entering the operating room. The result is a new generation of robotic surgeons trained not only on hardware mechanics but also on advanced procedure planning and execution techniques. The focus on integrated training technologies ensures that surgical precision continues to improve as robotic systems become more complex and capable.

Growth potential in robotic rehabilitation and physiotherapy devices

The Asia Pacific region is witnessing strong growth potential in robotic rehabilitation and physiotherapy devices, driven by rising healthcare investments and increasing awareness of advanced therapy options. Exoskeletons, end-effector devices, and wearable robotic systems are among the leading technologies being explored to support physical rehabilitation for patients with mobility impairments or post-surgical recovery needs. In Japan, where a combination of technological expertise and demographic shifts has accelerated development, powered exoskeletons such as the Hybrid Assistive Limb (HAL) have been used for years to assist patients with spinal injuries and stroke-related mobility issues, demonstrating how robotics can complement traditional therapy approaches. Elsewhere across the region, countries like the Philippines and South Korea are beginning to adopt rehabilitation robotics in clinical settings, though at an earlier stage than surgical robotics adoption. Clinical studies and device pilots in the Philippines have introduced robotic exoskeleton hands and upper-limb rehabilitation systems to local physiotherapy units, often aiming to help patients regain fine motor control after neurological incidents or injuries. These systems offer consistent, repeatable therapy sessions that can supplement human therapists, improving both efficiency and patient outcomes in settings where therapy resources may be limited. Another key trend is the integration of AI and sensor-based feedback into rehabilitation devices to personalize therapy and monitor patient progress. Advanced sensors can track movement patterns in real time, enabling rehabilitation robots to adjust support levels and provide targeted assistance based on patient performance. This adaptability improves therapeutic precision and engagement, particularly for patients undergoing long-term recovery from stroke or orthopedic surgery. Collaboration between robotics developers and rehabilitation centers across South Korea, Japan, and Australia is fostering innovations that merge robotics with data analytics and telehealth platforms, broadening the reach of these technologies beyond hospital walls. Combined with increasing healthcare spending across the region, these advancements suggest significant growth potential for robotic rehabilitation and physiotherapy devices in the Asia Pacific market.

Benelux Medical Robotics Market Size and Share Analysis:

The Benelux medical robotics market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

By product, the surgical robots segment dominated the market in 2025, driven by their essential role as core precision platforms enabling a wide range of robotic-assisted procedures across surgical specialties in the Benelux region.

In terms of application, the laparoscopy segment dominated the market in 2025, driven by high volumes of minimally invasive laparoscopic procedures supported by established clinical protocols and surgeon expertise in Benelux healthcare systems.

Based on end user, the hospitals segment dominated the market in 2025, driven by their advanced infrastructure, centralized surgical centers and financial capacity to invest in cutting-edge robotic technologies.

Benelux Medical Robotics Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 182.4 Million

Market Size by 2033

US$ 308.1 Million

CAGR (2026 - 2033)

6.8%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Surgical Robots

Hospital & Pharmacy Robots

Rehabilitation Robots

Noninvasive Radiosurgery Robots

By Application

Laparoscopy

Neurology

Orthopedics

Gynecology

Urology

Cardiology

Other Applications

By End User

Hospitals

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

Benelux

Belgium, Netherlands, Luxembourg

Market leaders and key company profiles

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Get more information on this report

Benelux Medical Robotics Market Report Coverage and Deliverables:

The "Benelux Medical Robotics Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Benelux Medical Robotics Market size and forecast at regional and country levels for all market segments covered under the scope

Benelux Medical Robotics Market trends, as well as drivers, restraints, and opportunities

Benelux Medical Robotics Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Benelux Medical Robotics Market

Detailed company profiles, including SWOT analysis

Benelux Medical Robotics Market Geographic Insights:

The geographical scope of the Benelux Medical Robotics Market report is divided into Belgium, the Netherlands, and Luxembourg. The Netherlands held the largest share in 2025.

Country-level insights into the benelux medical robotics market highlight differentiated adoption trends across the Netherlands, Luxembourg, and Belgium, shaped by national healthcare priorities, procurement structures, and innovation ecosystems. The Netherlands emerges as the dominant market within Benelux, supported by a highly advanced healthcare infrastructure, strong digital health integration, and proactive technology assessment frameworks. Dutch hospitals are among the region’s early adopters of robotic-assisted surgery, particularly in urology, gynecology, and cardiothoracic specialties, where outcome measurement and value-based care models drive procurement decisions. The country’s structured reimbursement environment and emphasis on clinical evidence generation further support sustained robotics integration. Additionally, the Netherlands benefits from a mature MedTech ecosystem and strong collaboration between academic medical centers and robotics manufacturers, accelerating pilot validation and scalable deployment across hospital networks. In Luxembourg, adoption remains selective yet strategically targeted. Given its relatively small healthcare system, the country focuses on high-precision surgical robotics within specialized treatment domains, often leveraging cross-border healthcare collaborations with neighboring EU states. Luxembourg’s investment approach is characterized by cautious capital allocation and partnership-driven acquisition models, ensuring alignment with long-term system efficiency goals. While deployment volume is limited compared to the Netherlands, Luxembourg demonstrates strong institutional openness to advanced technologies that enhance care quality and reduce patient referrals abroad. Belgium, meanwhile, maintains a steady but measured trajectory in medical robotics adoption. Belgian hospitals integrate robotic systems primarily to strengthen minimally invasive surgery capabilities and enhance procedural standardization across multispecialty departments. The country’s dual public-private healthcare structure influences purchasing cycles, with private hospital groups typically leading in advanced robotics procurement. Belgium also benefits from strong clinical research capabilities, supporting trials and data-driven evaluation of robotic platforms before broader roll-out. Collectively, Benelux countries share common priorities around clinical excellence, interoperability with digital hospital systems, and workforce readiness. However, the Netherlands leads in scale, ecosystem maturity, and structured integration strategies, positioning it as the central hub for medical robotics advancement within the Benelux region.

Get more information on this report

Benelux Medical Robotics Market Research Report Guidance:

The report includes qualitative and quantitative data in the Benelux Medical Robotics Market across product, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Benelux Medical Robotics Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Benelux Medical Robotics Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Benelux Medical Robotics Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Benelux Medical Robotics Market segments by product, application, end user, and geography across Belgium, the Netherlands, and Luxembourg. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Benelux Medical Robotics Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Benelux Medical Robotics Market News and Key Development:

The Benelux Medical Robotics Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Benelux Medical Robotics Market are:

In June 2023, the UK-based CMR Surgical’s Versius modular surgical robot was launched at Sint-Franciscus Hospital in Belgium, marking a significant expansion of advanced surgical robotics in the Benelux region. The compact, mobile system enabled minimally invasive robotic procedures across specialties like urology, gynecology and abdominal surgery, broadening access to robotic-assisted care for Belgian patients. Its modular design makes integration simpler for surgical teams and fits a variety of operating rooms. While not a 2025 launch, this deployment remains a cornerstone recent milestone in the Benelux medical robotics landscape.

In February 2025, AZORG Hospital in Belgium became a European pioneer by introducing the ROSA (Robotic Surgical Assistant) system for total hip prosthesis procedures, performing some of the first robot-assisted hip replacements in the region. This robotics deployment aims to enhance implant positioning precision and improve patient outcomes while reducing complications and recovery times. The introduction positions Belgium at the forefront of orthopaedic robotic surgery innovation in Europe. The technology reflects rising demand for advanced robot-assisted orthopaedics in Benelux care centers.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - Benelux Medical Robotics Market

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Frequently Asked Questions

How big is the Benelux Medical Robotics Market?

The Benelux Medical Robotics Market is valued at US$ 182.4 Million in 2025, it is projected to reach US$ 308.1 Million by 2033.

What is the CAGR for Benelux Medical Robotics Market by (2026 - 2033)?

As per our report Benelux Medical Robotics Market, the market size is valued at US$ 182.4 Million in 2025, projecting it to reach US$ 308.1 Million by 2033. This translates to a CAGR of approximately 6.8% during the forecast period.

What segments are covered in this report?

The Benelux Medical Robotics Market report typically cover these key segments-

Application (Laparoscopy, Neurology, Orthopedics, Gynecology, Urology, Cardiology, Other Applications)

End User (Hospitals, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for Benelux Medical Robotics Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Benelux Medical Robotics Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Benelux Medical Robotics Market?

The Benelux Medical Robotics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Who should buy this report?

The Benelux Medical Robotics Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Benelux Medical Robotics Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Benelux Medical Robotics Market

Get Free Sample For Benelux Medical Robotics Market