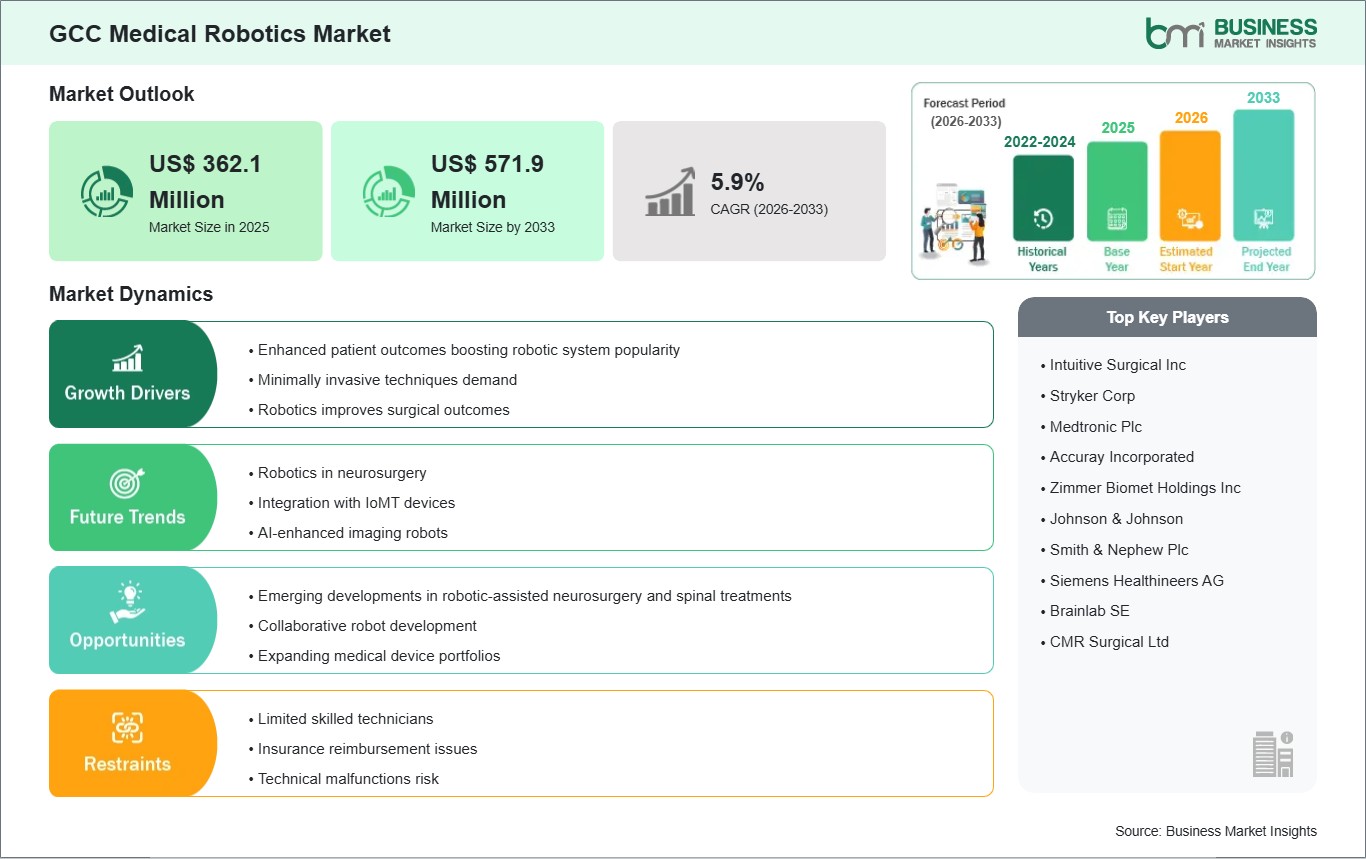

The GCC medical robotics market size is expected to reach US$ 571.9 million by 2033 from US$ 362.1 million in 2025. The market is estimated to record a CAGR of 5.9% from 2026 to 2033./p>

Executive Summary and GCC Medical Robotics Market Analysis:

The GCC medical robotics market is gaining strategic momentum as healthcare systems across the Gulf Cooperation Council (GCC) nations pursue modernization and digital transformation initiatives. Countries including Saudi Arabia, the United Arab Emirates (UAE), Qatar, Kuwait, Bahrain, and Oman are increasingly investing in advanced medical technologies to elevate clinical quality, improve procedural efficiency, and attract regional patient inflows. A notable trend is the prioritization of robotics within tertiary care centers and specialty hospitals, particularly for minimally invasive surgery, precision oncology, and rehabilitation support. Stakeholders within the GCC are positioning robotics not merely as a clinical tool but as a differentiator for high‑value care delivery that enhances institutional reputation and competitive positioning in the broader Middle Eastern healthcare landscape. Market dynamics are shaped by both public and private sector drivers. Government‑led health infrastructure development plans, particularly Saudi Vision 2030 and UAE’s healthcare innovation agendas, emphasize adoption of state‑of‑the‑art technologies to reduce reliance on overseas medical referrals and boost local service capabilities. These strategic initiatives are complemented by favorable investment environments and regulatory reforms that streamline approvals for high‑end devices. Private hospital groups are equally active, leveraging robotics to diversify service offerings, improve patient throughput, and strengthen affiliations with global centers of excellence. Despite strong impetus, adoption challenges persist. High capital expenditure requirements, scarcity of locally certified robotics specialists, and gaps in technical support infrastructure remain barriers, especially outside major metropolitan facilities. This has led stakeholders to explore alternative procurement frameworks such as shared services, leasing contracts, and managed robotics programs that distribute risk and optimize utilization. Furthermore, integration with hospital IT systems and electronic medical records is critical to unlocking full clinical and operational value, necessitating deliberate investments in interoperability and cybersecurity. Overall, the GCC Medical Robotics Market underscores a strategic shift toward technology‑enabled care delivery, with robotics playing an increasingly important role in reshaping procedural standards, enhancing clinical outcomes, and supporting broader healthcare system ambitions.

GCC Medical Robotics Market - Strategic Insights:

Get more information on this report

GCC Medical Robotics Market Segmentation Analysis:

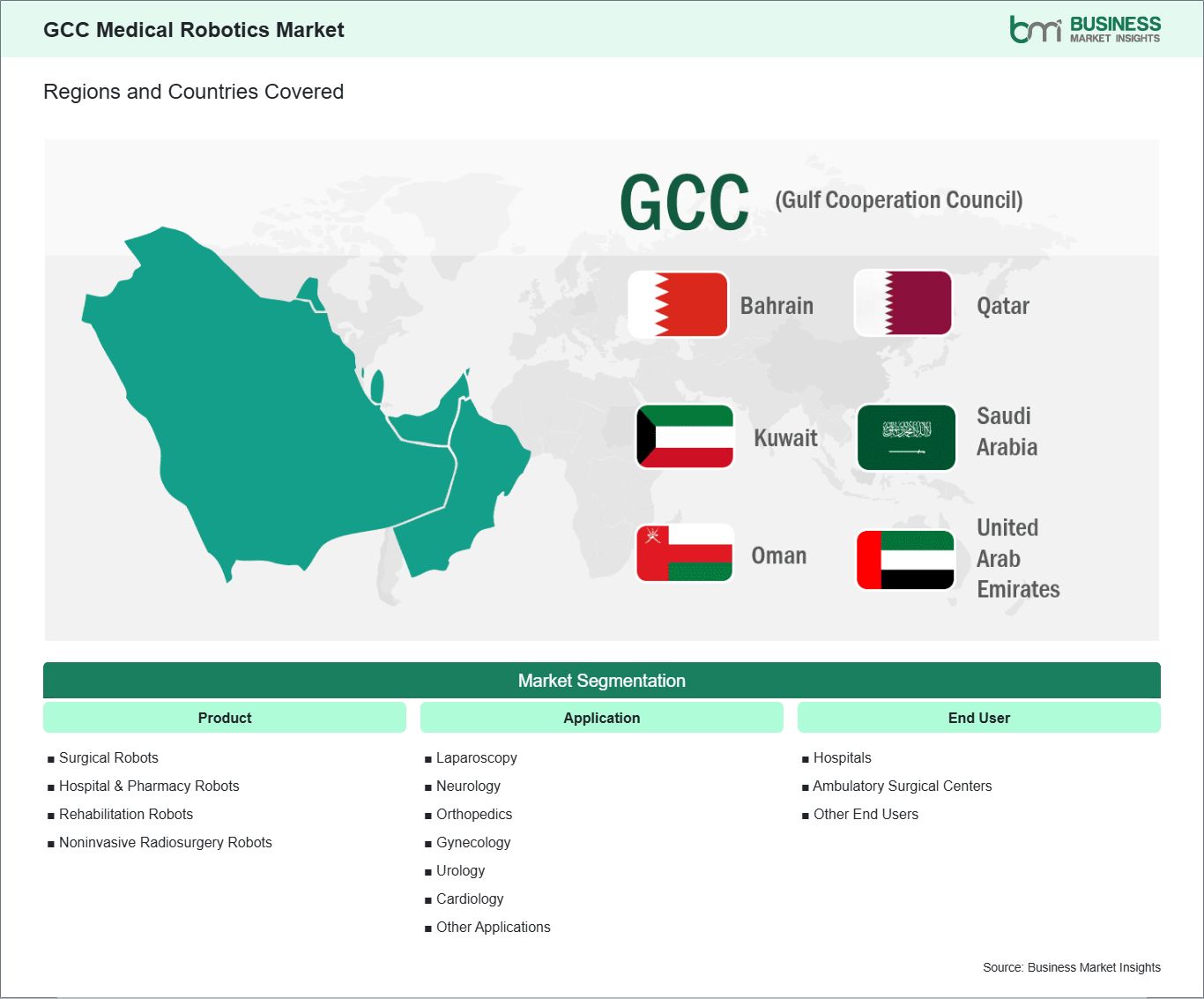

Key segments that contributed to the derivation of the GCC Medical Robotics Market analysis are product, application, and end user.

By product, the medical robotics market is segmented into surgical robots, hospital & pharmacy robots, rehabilitation robots, and non-invasive radiosurgery robots. The surgical robots segment dominated the market in 2025.

In terms of application, the medical robotics market is categorized into laparoscopy, neurology, orthopedics, gynecology, urology, cardiology, and other applications. The laparoscopy segment dominated the market in 2025.

Based on end user, the medical robotics market is classified into hospitals, ambulatory surgical centers, and other end users. The hospitals segment dominated the market in 2025.

GCC Medical Robotics Market Drivers and Opportunities:

Enhanced patient outcomes boosting robotic system popularity

Robotic systems are increasingly recognized in the GCC region for their ability to enhance patient outcomes, driving their popularity among hospitals and healthcare providers. By offering greater precision, control, and consistency, robotic-assisted procedures reduce the risk of complications and improve the quality of care across multiple surgical specialties. Patients benefit from smaller incisions, reduced tissue trauma, and faster recovery, which collectively enhance satisfaction and confidence in advanced treatment options. Healthcare providers in the GCC are adopting robotic platforms as a strategic tool to improve clinical performance. Robotic systems enable surgeons to execute complex procedures with more predictable outcomes, supporting standardization across surgical teams and improving overall efficiency. These capabilities are particularly important in areas such as urology, gynecology, and general surgery, where high accuracy and minimal invasiveness are critical for successful treatment and patient safety. The growing recognition of superior patient outcomes is also encouraging investment in robotic technologies. Hospitals are increasingly integrating robotics into surgical workflows to strengthen service offerings and demonstrate leadership in advanced care. As familiarity with robotic systems expands among clinicians and surgical teams, their adoption continues to rise, establishing robotic-assisted procedures as a preferred option for both patients and healthcare providers seeking improved results and reduced post-operative risks.

Emerging developments in robotic-assisted neurosurgery and spinal treatments

Robotic-assisted neurosurgery and spinal treatments are gaining momentum in the GCC as healthcare providers explore advanced solutions for complex neurological and spinal conditions. Robotics allows surgeons to plan and perform delicate procedures with enhanced accuracy and stability, minimizing the potential for complications and supporting better overall clinical outcomes. These capabilities are increasingly seen as critical in neurosurgical care, where precision and careful navigation of critical structures are essential. The integration of robotics in neurosurgery also supports innovation in minimally invasive techniques. Smaller surgical incisions, precise instrument control, and enhanced visualization enable patients to recover more quickly and experience reduced post-operative discomfort. Robotic-assisted spinal procedures further allow surgeons to address complex structural challenges with greater confidence and consistency, improving the reliability of surgical interventions and supporting the delivery of high-quality care across neurology and orthopedics. Emerging developments in this field also reflect a broader focus on training and technological advancement within the GCC. Robotic platforms offer opportunities for skill development, simulation-based training, and procedural standardization, helping surgeons refine their expertise in advanced neurosurgical and spinal procedures. As healthcare systems continue to invest in robotics and expand their capabilities, robotic-assisted neurosurgery and spinal treatments are poised to become increasingly prevalent, offering patients safer, more effective options while positioning the region at the forefront of surgical innovation.

GCC Medical Robotics Market Size and Share Analysis:

The GCC medical robotics market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

By product, the surgical robots segment dominated the market in 2025, driven by the growing adoption of advanced robotic systems that enhance precision and reduce surgical errors. The increasing number of complex surgical procedures in the region further fuels their demand.

In terms of application, the laparoscopy segment dominated the market in 2025, driven by the rising preference for minimally invasive procedures that shorten recovery times and reduce complications. The growing awareness of patient comfort and faster post-operative outcomes supports its widespread use.

Based on end user, the hospitals segment dominated the market in 2025, driven by substantial investments in modern healthcare infrastructure and high-end surgical technologies. The expanding number of specialized medical centers in the GCC accelerates the deployment of medical robots.

GCC Medical Robotics Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 362.1 Million

Market Size by 2033

US$ 571.9 Million

CAGR (2026 - 2033)

5.9%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Surgical Robots

Hospital & Pharmacy Robots

Rehabilitation Robots

Noninvasive Radiosurgery Robots

By Application

Laparoscopy

Neurology

Orthopedics

Gynecology

Urology

Cardiology

Other Applications

By End User

Hospitals

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

GCC

UAE, Bahrain, Saudi Arabia, Oman, Qatar, Kuwait

Market leaders and key company profiles

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Get more information on this report

GCC Medical Robotics Market Report Coverage and Deliverables:

The "GCC Medical Robotics Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

GCC Medical Robotics Market size and forecast at regional and country levels for all market segments covered under the scope

GCC Medical Robotics Market trends, as well as drivers, restraints, and opportunities

GCC Medical Robotics Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the GCC Medical Robotics Market

Detailed company profiles, including SWOT analysis

GCC Medical Robotics Market Geographic Insights:

The geographical scope of the GCC Medical Robotics Market report is divided into UAE, Bahrain, Saudi Arabia, Oman, Qatar, and Kuwait. UAE held the largest share in 2025.

Country‑level insights into the GCC Medical Robotics Market reveal distinct dynamics across Saudi Arabia, the United Arab Emirates (UAE), Qatar, Kuwait, Bahrain, and Oman each driven by unique healthcare priorities and investment trajectories. Saudi Arabia leads the region in strategic robotics adoption, buoyed by its Vision 2030 healthcare reform agenda that seeks to enhance medical infrastructure, reduce medical outbound travel, and build local capacity for high‑end care. Major tertiary hospitals in Riyadh and Jeddah are investing in robotic surgical systems across oncology, urology, and cardiovascular specialties, supported by government funding and collaborations with global technology leaders. The UAE is similarly ambitious, aligning robotics adoption with its digital health initiatives and advanced hospital networks spread across Abu Dhabi and Dubai. The UAE’s policies on innovation‑based healthcare procurement and robust private sector activity have accelerated integration of robotics, particularly in minimally invasive surgery, tele‑mentoring platforms, and rehabilitation robotics. Emirates hospitals are also integrating robotics with advanced imaging and data analytics to optimize clinical workflows. In Qatar, adoption is driven by national strategies that emphasize health system excellence and knowledge transfer. Robotics is being introduced through collaborative programs with academic centers and international medical organizations to enhance surgical precision and outcomes in subspecialty care. Kuwait and Bahrain show incremental growth characterized by targeted investments in flagship hospitals aimed at elevating care standards and retaining patients within domestic systems. These countries are selectively deploying robotic systems in high‑impact clinical areas such as oncology and orthopedics. Oman demonstrates measured adoption, primarily in referral hospitals where robotics supports specialized procedures and workforce upskilling. Across the GCC, providers are focusing on clinician training, data governance, and interoperable IT infrastructure to maximize the value of robotics investments. In summary, while Saudi Arabia and the UAE are at the forefront of market development, emerging robotics adoption in Qatar, Kuwait, Bahrain, and Oman underscores a regional shift toward technology‑enhanced, patient‑centric care delivery.

Get more information on this report

GCC Medical Robotics Market Research Report Guidance:

The report includes qualitative and quantitative data in the GCC Medical Robotics Market across product, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the GCC Medical Robotics Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the GCC Medical Robotics Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the GCC Medical Robotics Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover GCC Medical Robotics Market segments by product, application, end user, and geography across UAE, Bahrain, Saudi Arabia, Oman, Qatar, and Kuwait. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the GCC Medical Robotics Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

GCC Medical Robotics Market News and Key Development:

The GCC Medical Robotics Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the GCC Medical Robotics Market are:

In February 2026, Korean medical robotics company Curexo participated in WHX Dubai 2026 where it showcased flagship products including the CUVIS‑joint surgical robot for joint replacement and the Morning Walk gait rehabilitation robot to healthcare professionals and distributors. The exhibit focused on live demonstrations and engagement with GCC healthcare institutions to explore adoption and partnerships across the Middle East market. Curexo’s participation highlights growing demand and interest in advanced surgical and rehabilitation robotics in the GCC. This engagement also supports the company’s roadmap toward CE/MDR certification for global expansion.

In July 2025, Yas Clinic Khalifa City, in partnership with Abu Dhabi Stem Cells Centre, launched an advanced robotic spine surgery programme to support complex spinal procedures using robotic guidance technologies. This new programme aims to improve precision, reduce operative risks, and enhance recovery outcomes in spine care for patients throughout the UAE and the broader GCC. It represents a major addition to specialised robotic surgical services beyond traditional laparoscopic applications. The launch underscores the region’s expanding investment in specialised robotic surgery beyond general and orthopaedic procedures.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - GCC Medical Robotics Market

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Frequently Asked Questions

How big is the GCC Medical Robotics Market?

The GCC Medical Robotics Market is valued at US$ 362.1 Million in 2025, it is projected to reach US$ 571.9 Million by 2033.

What is the CAGR for GCC Medical Robotics Market by (2026 - 2033)?

As per our report GCC Medical Robotics Market, the market size is valued at US$ 362.1 Million in 2025, projecting it to reach US$ 571.9 Million by 2033. This translates to a CAGR of approximately 5.9% during the forecast period.

What segments are covered in this report?

The GCC Medical Robotics Market report typically cover these key segments-

Application (Laparoscopy, Neurology, Orthopedics, Gynecology, Urology, Cardiology, Other Applications)

End User (Hospitals, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for GCC Medical Robotics Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the GCC Medical Robotics Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in GCC Medical Robotics Market?

The GCC Medical Robotics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Who should buy this report?

The GCC Medical Robotics Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the GCC Medical Robotics Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For GCC Medical Robotics Market

Get Free Sample For GCC Medical Robotics Market