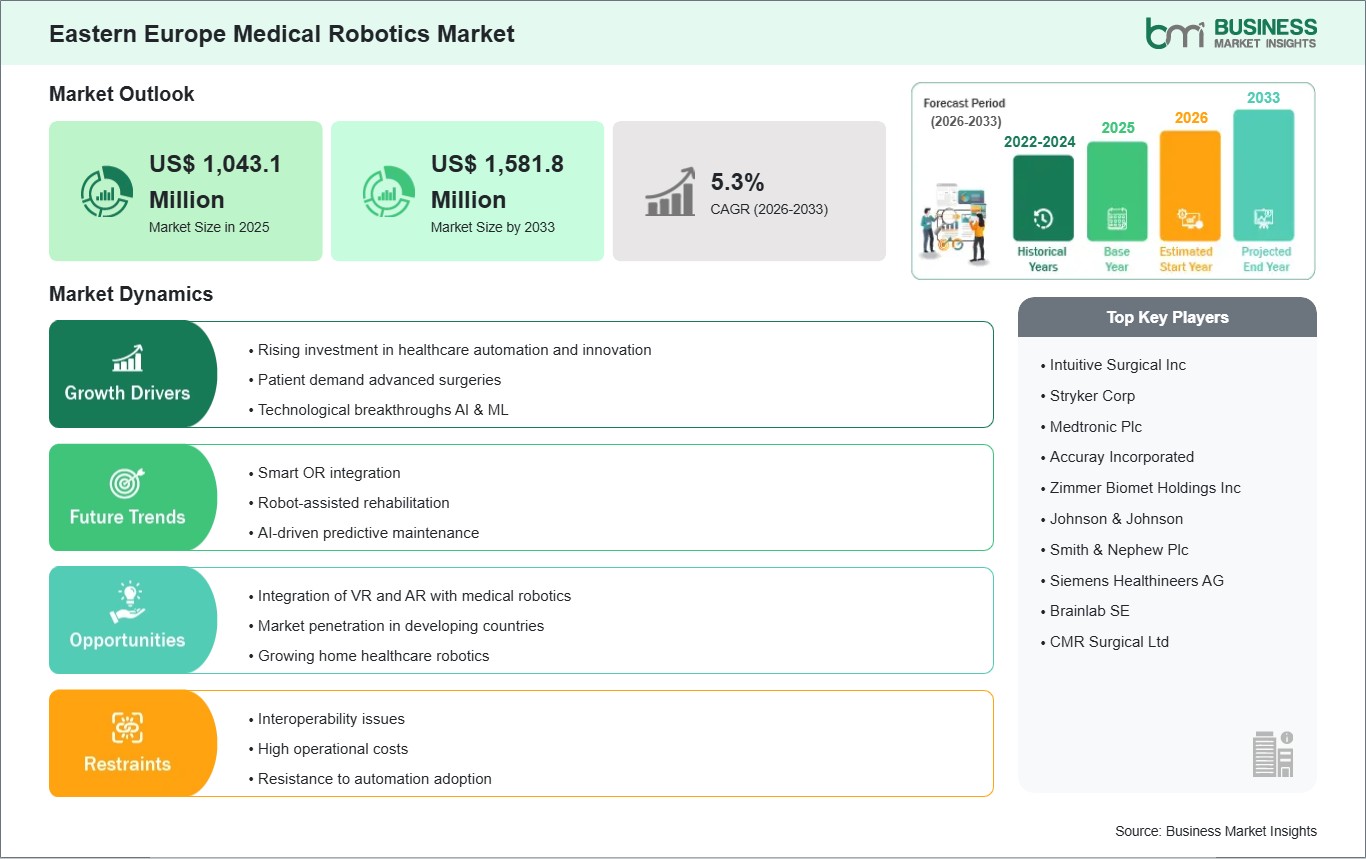

The Eastern Europe medical robotics market size is expected to reach US$ 1,581.8 million by 2033 from US$ 1,043.1 million in 2025. The market is estimated to record a CAGR of 5.3% from 2026 to 2033.

Executive Summary and Eastern Europe Medical Robotics Market Analysis:

The Eastern Europe medical robotics market is advancing against a backdrop of healthcare modernization, demographic transitions, and rising clinical demand for innovative procedural technologies. Across countries such as Poland, Czech Republic, Hungary, Romania, and Ukraine, healthcare providers are increasingly turning to robotics to enhance surgical precision, improve patient outcomes, and address workforce constraints. Investment in minimally invasive surgical systems particularly in urology, orthopedics, and gynecological procedures has emerged as a focal area, driven by hospital networks striving to align with Western European clinical standards. A key feature of the region’s market evolution is the strategic adoption of robotics as part of broader digital health initiatives, where robotics integration complements electronic health records, advanced imaging, and telemedicine platforms. Market dynamics exhibit considerable diversity within Eastern Europe. Developed healthcare systems in Poland and the Czech Republic are leading initial deployments with structured procurement frameworks and clinician training programs that support robotics utilization. These markets demonstrate an increasing preference for platforms that deliver improved dexterity and real‑time data analytics capabilities, enabling clinicians to optimize both procedural efficiency and patient safety metrics. Conversely, in markets with constrained healthcare budgets, such as Romania and Ukraine, adoption remains concentrated within leading urban medical centers and private hospital groups that are selectively investing in robotics to differentiate care quality and attract medical tourism. Regulatory complexity and budgetary pressures remain material challenges, compelling robotics vendors to adopt flexible commercialization strategies, including leasing models, shared service agreements, and outcome‑based partnerships with hospital consortia. Additionally, workforce readiness—particularly surgeon certification and technical maintenance capacity emerges as a critical determinant of successful robotics integration. Stakeholders are increasingly investing in training ecosystems and academic collaborations to bridge these gaps. Overall, the Eastern Europe Medical Robotics Market is poised for gradual expansion, with innovation‑driven demand and institutional commitment to quality care serving as primary catalysts for sustained adoption.

Eastern Europe Medical Robotics Market - Strategic Insights:

Get more information on this report

Eastern Europe Medical Robotics Market Segmentation Analysis:

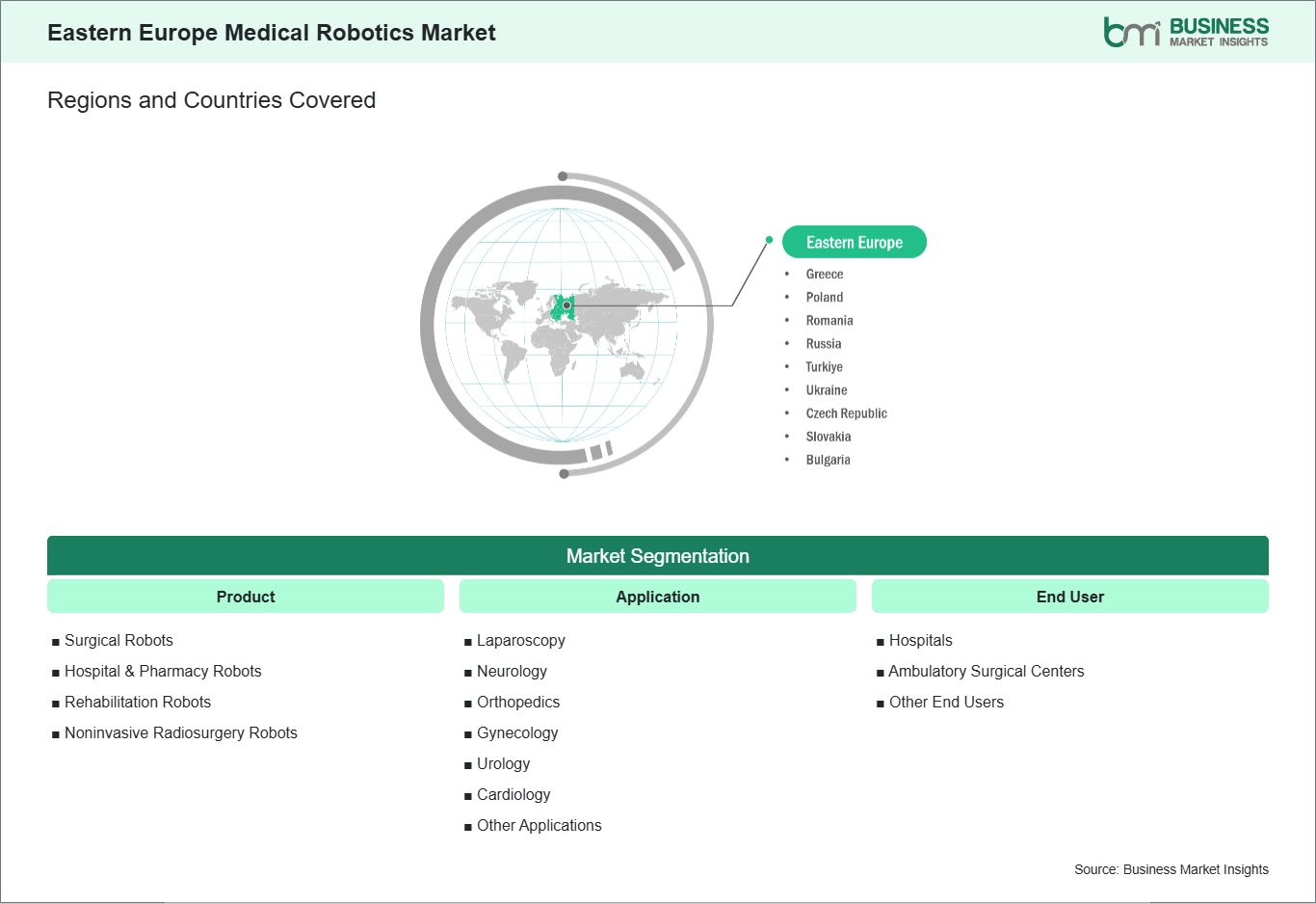

Key segments that contributed to the derivation of the Eastern Europe Medical Robotics Market analysis are product, application, and end user.

By product, the medical robotics market is segmented into surgical robots, hospital & pharmacy robots, rehabilitation robots, and non-invasive radiosurgery robots. The surgical robots segment dominated the market in 2025.

In terms of application, the medical robotics market is categorized into laparoscopy, neurology, orthopedics, gynecology, urology, cardiology, and other applications. The laparoscopy segment dominated the market in 2025.

Based on end user, the medical robotics market is classified into hospitals, ambulatory surgical centers, and other end users. The hospitals segment dominated the market in 2025.

Eastern Europe Medical Robotics Market Drivers and Opportunities:

Rising investment in healthcare automation and innovation

In Eastern Europe, investment in healthcare automation and innovation is increasingly shaping the medical robotics market as hospitals and clinics seek greater efficiency and clinical quality. Countries such as Poland, Czech Republic, Hungary, and Romania are deepening their focus on advanced healthcare technologies as part of broader national strategies to modernize care delivery. In Poland, several tertiary care centers have renewed operating theaters with robotic surgical systems that automate traditionally manual tasks, allowing surgeons to perform complex procedures with higher consistency and reduced physical strain. Public and private healthcare funds are prioritizing these automated solutions to support growing demand for minimally invasive procedures, reflecting a shift from legacy equipment toward digitally integrated robotics. Similarly, Czech Republic’s university hospitals are investing in robotics platforms alongside electronic health record systems and automated operating room workflows, aiming to create seamless, data‑driven surgical environments. Healthcare automation investments are also visible in Eastern Europe through emerging interest in robot‑assisted pharmacy automation and clinical support systems. In Romania, larger hospital networks are piloting robotics for tasks such as automated drug dispensing and supply chain management, reducing turnaround times and human error in routine processes. This shift is supported by targeted government grants and EU structural funds that earmark digital innovation within the healthcare sector, incentivizing institutions to adopt automation technologies. For example, hospitals in Bucharest and Cluj‑Napoca have received funding to upgrade clinical infrastructure with automation that improves surgical throughput and enhances perioperative coordination, illustrating how investment priorities are expanding beyond individual robotic systems into comprehensive automated ecosystems. The region’s health tech start‑up scene also contributes to expanding investment in medical automation. Several Eastern European software and robotics firms—particularly in Poland and the Baltic states—are developing adjunct technologies that integrate with surgical robots, such as automated workflow analytics and interoperability tools that connect robotics systems with hospital data networks. These innovations attract capital from both local investors and international partnerships, reinforcing a long‑term trend: investment in healthcare automation is not limited to purchasing hardware but extends to intelligent solutions that amplify the impact of medical robotics on clinical performance, operational efficiency, and patient outcomes across Eastern Europe.

Integration of VR and AR with medical robotics

The integration of virtual reality (VR) and augmented reality (AR) with medical robotics is gaining momentum in Eastern Europe as clinicians leverage immersive technologies to augment surgical precision, training, and intraoperative navigation. In Poland, leading orthopedic and neurosurgery departments at academic hospitals have adopted VR simulation platforms that allow surgeons to rehearse robot‑assisted procedures in fully interactive 3D environments before entering the operating room. These VR tools help surgical teams visualize patient anatomy in detail, anticipate procedural challenges, and refine their approach, all while reducing reliance on traditional cadaver labs. This integration is particularly valuable for complex cases such as spinal reconstruction or tumor resections, where immersive preoperative planning increases confidence and improves clinical decision‑making. Augmented reality is also transforming intraoperative experiences in Eastern Europe. In Czech Republic and Hungary, AR overlays are being used to provide real‑time visual guidance during robot‑assisted surgeries, displaying critical anatomical landmarks and instrument trajectories directly within the surgeon’s field of view. These AR systems can be integrated with surgical robots’ imaging modules to project enhanced information on monitors or wearable displays, improving hand‑eye coordination and reducing cognitive load. For example, during urological and gynecological procedures, AR‑enhanced robotics systems help surgeons merge preoperative imaging data with real‑time operative views, enabling more accurate resections while preserving surrounding tissue. This technological convergence holds particular promise in settings where surgical volumes are rising and precision is paramount. Beyond the operating room, VR and AR play a growing role in clinician training and remote mentoring across Eastern Europe. In Romania and the Baltic states, medical schools and training hospitals are adopting VR simulation labs that pair with robotic systems to train residents and specialists in coordinated robotic workflows and advanced procedural scenarios. These platforms often support remote collaboration, allowing expert surgeons to guide trainees through AR‑augmented interfaces from different locations, helping bridge expertise gaps across the region. The result is a more digitally enabled workforce capable of maximizing the benefits of medical robotics. As Eastern European healthcare systems continue to invest in immersive technologies, the integration of VR and AR with robotics is poised to enhance clinical outcomes, boost procedural efficiency, and support long‑term growth of advanced surgical capabilities throughout the region.

Eastern Europe Medical Robotics Market Size and Share Analysis:

The Eastern Europe medical robotics market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

By product, the surgical robots segment dominated the market in 2025, driven by widespread adoption of advanced robotic platforms that enable precision and minimally invasive procedures across key surgical specialties in Eastern Europe.

In terms of application, the laparoscopy segment dominated the market in 2025, driven by high volumes of robot‑assisted minimally invasive laparoscopic surgeries supported by established clinical protocols and growing surgeon expertise.

Based on end user, the hospitals segment dominated the market in 2025, driven by their comprehensive surgical infrastructure and financial capacity to invest in costly robotic systems for improved clinical outcomes and patient care.

Eastern Europe Medical Robotics Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 1,043.1 Million

Market Size by 2033

US$ 1,581.8 Million

CAGR (2026 - 2033)

5.3%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Surgical Robots

Hospital & Pharmacy Robots

Rehabilitation Robots

Noninvasive Radiosurgery Robots

By Application

Laparoscopy

Neurology

Orthopedics

Gynecology

Urology

Cardiology

Other Applications

By End User

Hospitals

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

Eastern Europe

Russia, Poland, Ukraine, Romania, the Czech Republic, Slovakia, Bulgaria, Greece

Market leaders and key company profiles

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Get more information on this report

Eastern Europe Medical Robotics Market Report Coverage and Deliverables:

The "Eastern Europe Medical Robotics Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Eastern Europe Medical Robotics Market size and forecast at regional and country levels for all market segments covered under the scope

Eastern Europe Medical Robotics Market trends, as well as drivers, restraints, and opportunities

Eastern Europe Medical Robotics Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Eastern Europe Medical Robotics Market

Detailed company profiles, including SWOT analysis

Eastern Europe Medical Robotics Market Geographic Insights:

The geographical scope of the Eastern Europe Medical Robotics Market report is divided into Russia, Poland, Ukraine, Romania, the Czech Republic, Slovakia, Bulgaria, and Greece. Russia held the largest share in 2025.

Country-level insights into the Eastern Europe medical robotics market reveal differentiated adoption trajectories shaped by national healthcare systems, policy frameworks, and capital allocation strategies. Russia emerges as the dominant market in the region, driven by substantial investments in healthcare modernization, large tertiary hospitals, and strategic initiatives to reduce dependence on imported medical technologies. Major Russian medical centers in Moscow and Saint Petersburg are deploying robotic-assisted surgical systems across specialties such as urology, oncology, and cardiothoracic surgery. Government-backed technology programs and public-private partnerships are supporting local manufacturing capabilities, clinical training, and research collaborations, enabling scalable adoption and faster integration of robotics into high-volume care pathways. The Czech Republic also demonstrates strong adoption, supported by well-funded hospitals and rigorous technology assessment protocols. Czech healthcare providers are gradually integrating robotic surgical platforms into standard practice, leveraging EU-aligned regulatory frameworks and robust clinical outcome data to justify broader deployment. Interoperability with national health IT systems and digital infrastructure is emphasized to ensure efficient integration and data-driven insights. In Hungary, adoption is moderate, primarily concentrated in metropolitan teaching hospitals and specialized care centers. Robotics is used to improve procedural standardization, reduce recovery times, and enhance surgical outcomes in high-volume operations. Budgetary constraints and structured fiscal planning cycles, however, limit rapid expansion into smaller hospitals. Romania and Ukraine are emerging markets where robotics integration is selective and concentrated within private hospitals and specialty centers. High capital costs and limited public funding lead to cautious adoption, with institutions deploying robotics strategically to enhance care quality, attract regional referrals, and differentiate their services. Across Eastern Europe, Russia leads in scale, government support, and local innovation capabilities, while other countries are advancing at varied paces depending on infrastructure, funding, and regulatory maturity. Collectively, these country-level insights highlight that the region is increasingly recognizing medical robotics as a key driver of clinical excellence, efficiency, and patient outcomes, with future growth hinging on policy alignment, workforce development, and innovative financing strategies.

Get more information on this report

Eastern Europe Medical Robotics Market Research Report Guidance:

The report includes qualitative and quantitative data in the Eastern Europe Medical Robotics Market across product, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Eastern Europe Medical Robotics Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Eastern Europe Medical Robotics Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Eastern Europe Medical Robotics Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Eastern Europe Medical Robotics Market segments by product, application, end user, and geography across Russia, Poland, Ukraine, Romania, the Czech Republic, Slovakia, Bulgaria, and Greece. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Eastern Europe Medical Robotics Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Eastern Europe Medical Robotics Market News and Key Development:

The Eastern Europe Medical Robotics Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Eastern Europe Medical Robotics Market are:

In July 2025, Intuitive Surgical’s da Vinci 5 robot received CE mark approval for use across Europe in adult and pediatric minimally invasive procedures spanning urology, gynaecology and general laparoscopic surgery. This regulatory milestone paves the way for clinical roll‑out across EU member states and increases access to the latest generation of surgical robotics with integrated force feedback and advanced systems. The CE clearance reflects Europe’s continued adoption of next‑gen robot‑assisted platforms to drive surgical precision and patient outcomes. With broader market entry planned thereafter, healthcare providers can now deploy Da Vinci 5 in operating rooms throughout Eastern and Western Europe.

In September 2025, the SHURUI Single‑Port Surgical Robot secured CE certification in the EU, marking it as one of the first single‑port robotic systems approved for a wide range of laparoscopic adult and pediatric surgeries in Europe. Its snake‑like instrument architecture enables complex operations through a single incision, potentially reducing surgical trauma and speeding recovery compared with traditional multi‑port robotics. The certification also supports expanded clinical use and training partnerships across European healthcare institutions. This milestone boosts the competitiveness of next‑generation surgical robots in European markets.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - Eastern Europe Medical Robotics Market

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Frequently Asked Questions

How big is the Eastern Europe Medical Robotics Market?

The Eastern Europe Medical Robotics Market is valued at US$ 1,043.1 Million in 2025, it is projected to reach US$ 1,581.8 Million by 2033.

What is the CAGR for Eastern Europe Medical Robotics Market by (2026 - 2033)?

As per our report Eastern Europe Medical Robotics Market, the market size is valued at US$ 1,043.1 Million in 2025, projecting it to reach US$ 1,581.8 Million by 2033. This translates to a CAGR of approximately 5.3% during the forecast period.

What segments are covered in this report?

The Eastern Europe Medical Robotics Market report typically cover these key segments-

Application (Laparoscopy, Neurology, Orthopedics, Gynecology, Urology, Cardiology, Other Applications)

End User (Hospitals, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for Eastern Europe Medical Robotics Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Eastern Europe Medical Robotics Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Eastern Europe Medical Robotics Market?

The Eastern Europe Medical Robotics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Intuitive Surgical Inc

Stryker Corp

Medtronic Plc

Accuray Incorporated

Zimmer Biomet Holdings Inc

Johnson & Johnson

Smith & Nephew Plc

Siemens Healthineers AG

Brainlab SE

CMR Surgical Ltd

Who should buy this report?

The Eastern Europe Medical Robotics Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Eastern Europe Medical Robotics Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Eastern Europe Medical Robotics Market

Get Free Sample For Eastern Europe Medical Robotics Market