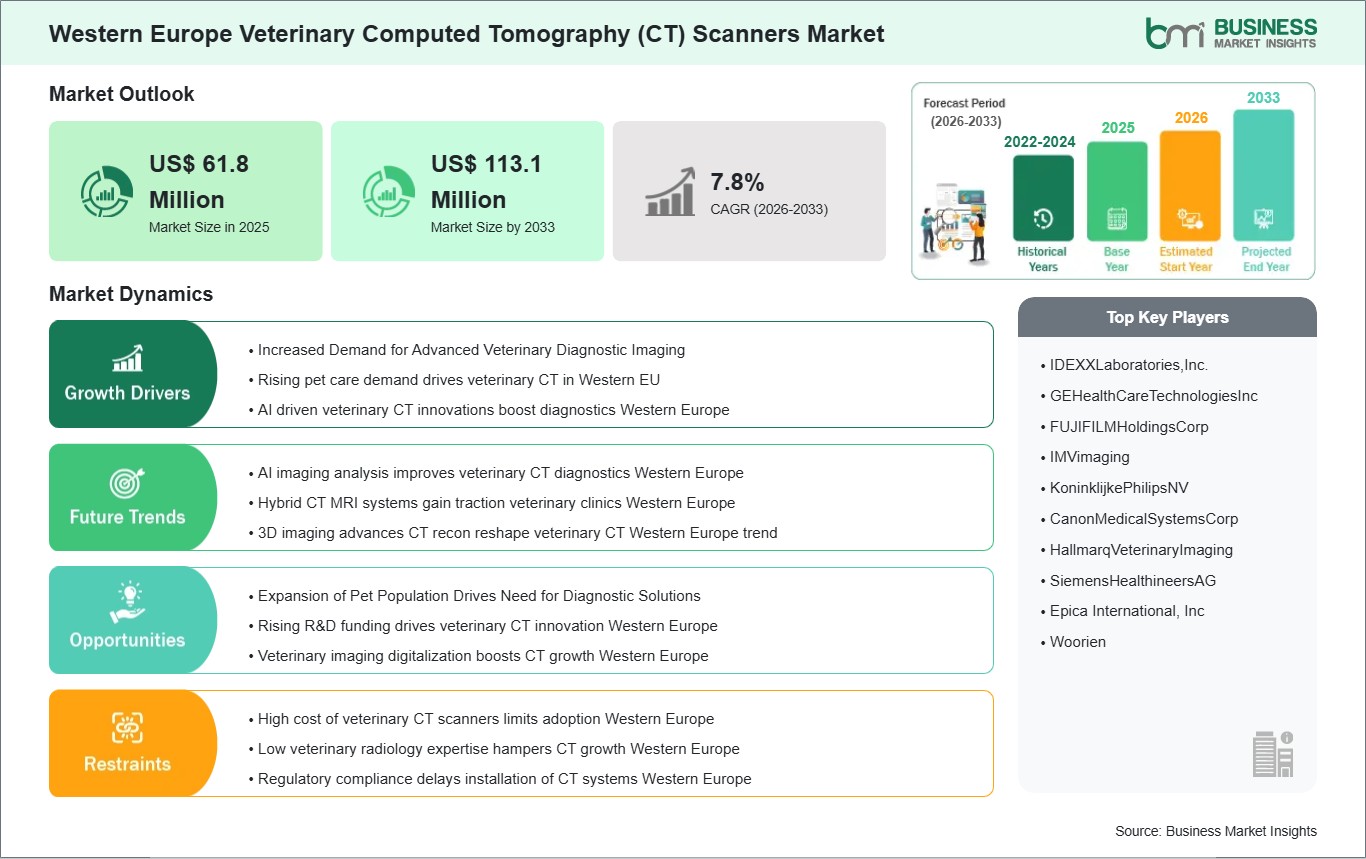

The Western Europe veterinary computed tomography (CT) scanners market size is expected to reach US$ 113.1 million by 2033 from US$ 61.8 million in 2025. The market is estimated to record a CAGR of 7.8% from 2026 to 2033.

Executive Summary and Western Europe Veterinary Computed Tomography (CT) Scanners Market Analysis:

The Western Europe veterinary CT scanner market is driven by the increasing acceptance of advanced diagnostic equipment in animal healthcare facilities. In Western Europe, increased pet ownership and expansion of specialized veterinary care centers have contributed to greater acceptance and integration of computed tomography (CT) technology. Unlike traditional imaging modalities, CT scanners provide highly detailed cross-sectional images, enabling accurate diagnosis of complex conditions in small companion animals, equine patients, and livestock. This capability has made CT systems an essential investment for progressive veterinary practices in developed markets such as Germany, the UK, France, and the Benelux countries.

One of the key factors driving the market growth in Western Europe is the strong presence of veterinary teaching hospitals and diagnostic imaging centers that prefer cutting-edge technologies for both diagnostic and research purposes. The region's strong regulatory environment, coupled with well-established animal health infrastructure, supports technology adoption. Veterinarians are increasingly relying on CT imaging to diagnose neurological disorders, orthopedic injuries, and oncological conditions, where accurate visualization is critical. Additionally, the increasing focus on preventive care and advanced therapeutics has encouraged referrals to imaging centers equipped with CT systems, increasing overall utilization rates.

Western Europe Veterinary Computed Tomography (CT) Scanners Market - Strategic Insights:

Get more information on this report

Western Europe Veterinary Computed Tomography (CT) Scanners Market Segmentation Analysis:

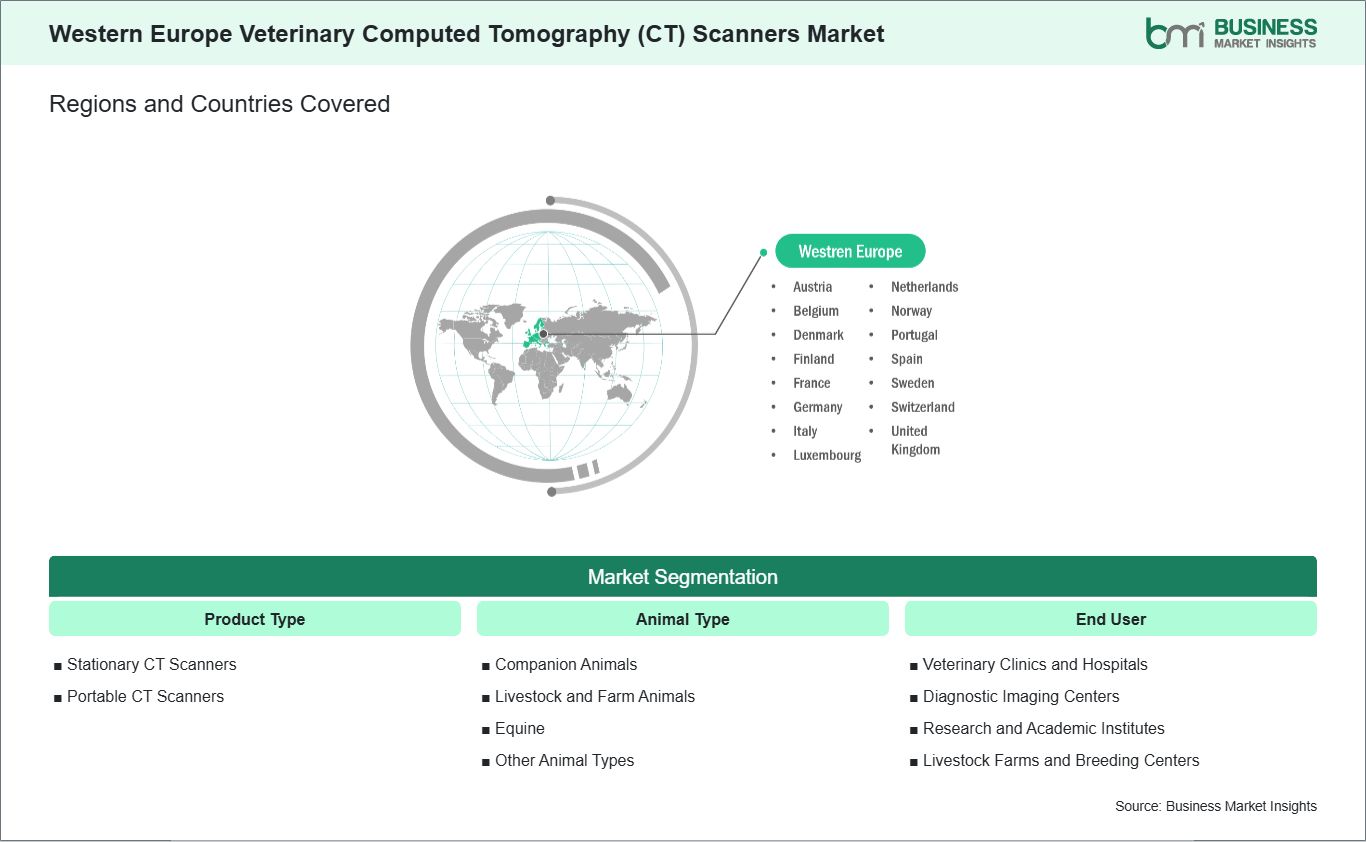

Key segments that contributed to the derivation of the Western Europe veterinary computed tomography (CT) scanners market analysis are product type, animal type, and end user.

By product type, the veterinary computed tomography (CT) scanners market is bifurcated into stationary CT scanners and portable CT scanners. The stationary CT scanners segment dominated the market in 2025.

Based on animal type, the veterinary computed tomography (CT) scanners market is categorized into companion animals, livestock and farm animals, equine, and other animal types. The companion animals segment dominated the market in 2025.

In terms of end user, the veterinary computed tomography (CT) scanners market is segmented into veterinary clinics and hospitals, diagnostic imaging centers, research and academic institutes, livestock farms, and breeding centers. The veterinary clinics and hospitals segment dominated the market in 2025.

Western Europe Veterinary Computed Tomography (CT) Scanners Market Drivers and Opportunities:

Increased Demand for Advanced Veterinary Diagnostic Imaging

In countries such as Germany, France, and the UK, pet ownership has reached record levels, prompting clinics to invest in advanced imaging for diagnosing complex conditions such as bone fractures and internal organ issues. This rising demand has also led smaller practices to partner with veterinary CT-equipped diagnostic centers, expanding overall regional adoption.

In Scandinavia - where animal welfare regulations are among the strictest in Europe - routine whistle use is becoming standard practice for cases involving pets and horses. The availability of government grants in countries such as Sweden and the Netherlands has further encouraged equipment acquisition, especially in rural areas where mobile CT units now service several clinics to meet demand.

Additionally, growing awareness among veterinary professionals about the advantages of CT imaging compared to traditional X-rays - particularly in oncology and neurology cases - is fueling purchases. This trend has been reinforced by academic collaboration in Western European veterinary research facilities focused on improving clinical outcomes.

Expansion of Pet Population Drives Need for Diagnostic Solutions

Recent reports indicate that countries such as France and Italy have the highest rates of cat and dog ownership in the region, driving demand for sophisticated diagnostic tools. As pet owners in urban centers such as Paris and Milan seek specialized care, veterinary hospitals are increasingly investing in CT solutions to provide comprehensive diagnostic services.

Additionally, horse and livestock imaging is increasing in agricultural centers in Western Europe, such as Bavaria and Andalusia. Here, advanced diagnostic imaging helps veterinarians monitor complex conditions in valuable breeding animals, strengthening the case for adopting CT beyond the care of companion animals.

Investment in veterinary health care infrastructure across Western Europe presents a measurable opportunity. Clinics are upgrading facilities and integrating CT imaging with digital record systems, particularly in the UK and the Netherlands. This integration supports quick turnaround for diagnosis and better clinical decision-making.

Western Europe Veterinary Computed Tomography (CT) Scanners Market Size and Share Analysis:

The Western Europe veterinary computed tomography (CT) scanners market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product type, animal type, and end user, offering insights into their contribution to overall market performance.

By product type, the stationary CT scanners subsegment dominated the market in 2025, driven by their higher imaging accuracy, comprehensive diagnostic capabilities, and greater demand from established veterinary facilities.

Based on animal type, the companion animals subsegment dominated the market in 2025, driven by the increasing pet ownership and growing demand for advanced diagnostic services for dogs and cats.

In terms of end user, the veterinary clinics and hospitals subsegment dominated the market in 2025, driven by the rising investment in advanced imaging equipment and expanding service offerings in clinical settings.

Western Europe Veterinary Computed Tomography (CT) Scanners Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 61.8 Million

Market Size by 2033

US$ 113.1 Million

CAGR (2026 - 2033)

7.8%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product Type

Stationary CT Scanners

Portable CT Scanners

By Animal Type

Companion Animals

Livestock and Farm Animals

Equine

Other Animal Types

By End User

Veterinary Clinics and Hospitals

Diagnostic Imaging Centers

Research and Academic Institutes

Livestock Farms and Breeding Centers

Regions and Countries Covered

Western Europe

Belgium, the Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, the United Kingdom, Denmark, Portugal, Norway, Finland

Market leaders and key company profiles

IDEXXLaboratories,Inc.

GEHealthCareTechnologiesInc

FUJIFILMHoldingsCorp

IMVimaging

KoninklijkePhilipsNV

CanonMedicalSystemsCorp

HallmarqVeterinaryImaging

SiemensHealthineersAG

Epica International, Inc

Woorien

Get more information on this report

Western Europe Veterinary Computed Tomography (CT) Scanners Market Report Coverage and Deliverables:

The "Western Europe Veterinary Computed Tomography (CT) Scanners Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Western Europe Veterinary Computed Tomography (CT) Scanners Market size and forecast at regional, and country levels for all the key market segments covered under the scope

Western Europe Veterinary Computed Tomography (CT) Scanners Market trends, as well as drivers, restraints, and opportunities

Western Europe Veterinary Computed Tomography (CT) Scanners Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Western Europe Veterinary Computed Tomography (CT) Scanners Market

Detailed company profiles, including SWOT analysis

Western Europe Veterinary Computed Tomography (CT) Scanners Market Geographic Insights:

The geographical scope of the Western Europe Veterinary Computed Tomography (CT) Scanners Market report is divided into Belgium, the Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, the UK, Denmark, Portugal, Norway, and Finland. Germany held the largest share in 2025.

In the Western Europe veterinary computed tomography (CT) scanners market, Germany serves as the dominant region, driven by its highly developed veterinary infrastructure, widespread adoption of advanced diagnostic technologies, and significant presence of specialized veterinary hospitals and research institutes. High pet ownership and a strong focus on companion animal health further strengthen Germany's leadership, making it the largest contributor to regional demand and a center for vendor investment, service networks, and training initiatives. France and the UK represent mature markets, characterized by extensive veterinary clinic networks, increasing use of CT scanners for oncology, orthopedics, and pre-surgical planning, and a growing trend toward integrated imaging services.

The Benelux countries - Belgium, the Netherlands, and Luxembourg - are demonstrating steady growth, supported by active veterinary education, regulatory frameworks favoring advanced diagnostics, and gradual adoption of CT technology in both private and academic veterinary settings. Italy and Spain are expanding, but are comparatively emerging markets, where increasing pet health care expenditures and growing awareness of CT applications are gradually driving equipment upgrades. Adoption remains slow in these countries due to budgetary constraints in smaller practices. Switzerland maintains a stable demand trajectory, reflecting high per capita veterinary spending and well-established private and specialty clinics that actively invest in advanced imaging capabilities. Scandinavian nations - Sweden, Denmark, Norway, and Finland - are notable for strong growth potential, driven by increasing pet ownership, emphasis on early detection of complex diseases, and adoption of service-providing mobile CT solutions.

Get more information on this report

Western Europe Veterinary Computed Tomography (CT) Scanners Market Research Report Guidance:

The report includes qualitative and quantitative data in the Western Europe Veterinary Computed Tomography (CT) Scanners Market across product type, animal type, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Western Europe Veterinary Computed Tomography (CT) Scanners Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Western Europe Veterinary Computed Tomography (CT) Scanners Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Western Europe Veterinary Computed Tomography (CT) Scanners Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Western Europe Veterinary Computed Tomography (CT) Scanners Market segments by product type, animal type, end user, and geography across Belgium, the Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, the UK, Denmark, Portugal, Norway, and Finland. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Western Europe Veterinary Computed Tomography (CT) Scanners Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Western Europe Veterinary Computed Tomography (CT) Scanners Market News and Key Development:

The Western Europe Veterinary Computed Tomography (CT) Scanners Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Western Europe veterinary computed tomography (CT) scanners market are:

In October 2024, WOORIEN Co., Ltd. launched the MyVet CT Plus, an advanced veterinary imaging solution designed to significantly reduce CT scan acquisition time while enhancing image quality across a wide range of animal sizes, improving diagnostic capabilities with a more efficient spiral‑linear CT technology. This launch builds on their ongoing strategy to innovate in veterinary CT equipment and expand product reach into global markets.

In September 2025, IMV Imaging and Asto CT announced a strategic partnership to advance veterinary diagnostic imaging, combining IMV's broad veterinary imaging portfolio with Asto CT's pioneering Equina weight‑bearing equine CT technology to accelerate the adoption of advanced CT imaging solutions worldwide.

Key Sources Referred:

American College of Veterinary Radiology (ACVR)World Small Animal Veterinary Association (WSAVA)British Veterinary Association (BVA)International Veterinary Radiology Association (IVRA)American Veterinary Medical Association (AVMA)European College of Veterinary Diagnostic Imaging (ECVDI)World Organisation for Animal Health (WOAH / OIE)Veterinary Imaging & Radiation Oncology Society (VIROS)

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Western Europe Veterinary Computed Tomography (CT) Scanners Market?

The Western Europe Veterinary Computed Tomography (CT) Scanners Market is valued at US$ 61.8 Million in 2025, it is projected to reach US$ 113.1 Million by 2033.

What is the CAGR for Western Europe Veterinary Computed Tomography (CT) Scanners Market by (2026 - 2033)?

As per our report Western Europe Veterinary Computed Tomography (CT) Scanners Market, the market size is valued at US$ 61.8 Million in 2025, projecting it to reach US$ 113.1 Million by 2033. This translates to a CAGR of approximately 7.8% during the forecast period.

What segments are covered in this report?

The Western Europe Veterinary Computed Tomography (CT) Scanners Market report typically cover these key segments-

Product Type (Stationary CT Scanners, Portable CT Scanners)

Animal Type (Companion Animals, Livestock and Farm Animals, Equine, Other Animal Types)

End User (Veterinary Clinics and Hospitals, Diagnostic Imaging Centers, Research and Academic Institutes, Livestock Farms and Breeding Centers)

What is the historic period, base year, and forecast period taken for Western Europe Veterinary Computed Tomography (CT) Scanners Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Western Europe Veterinary Computed Tomography (CT) Scanners Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Western Europe Veterinary Computed Tomography (CT) Scanners Market?

The Western Europe Veterinary Computed Tomography (CT) Scanners Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

IDEXXLaboratories,Inc.

GEHealthCareTechnologiesInc

FUJIFILMHoldingsCorp

IMVimaging

KoninklijkePhilipsNV

CanonMedicalSystemsCorp

HallmarqVeterinaryImaging

SiemensHealthineersAG

Epica International, Inc

Woorien

Who should buy this report?

The Western Europe Veterinary Computed Tomography (CT) Scanners Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Western Europe Veterinary Computed Tomography (CT) Scanners Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Western Europe Veterinary Computed Tomography (CT) Scanners Market

Get Free Sample For Western Europe Veterinary Computed Tomography (CT) Scanners Market