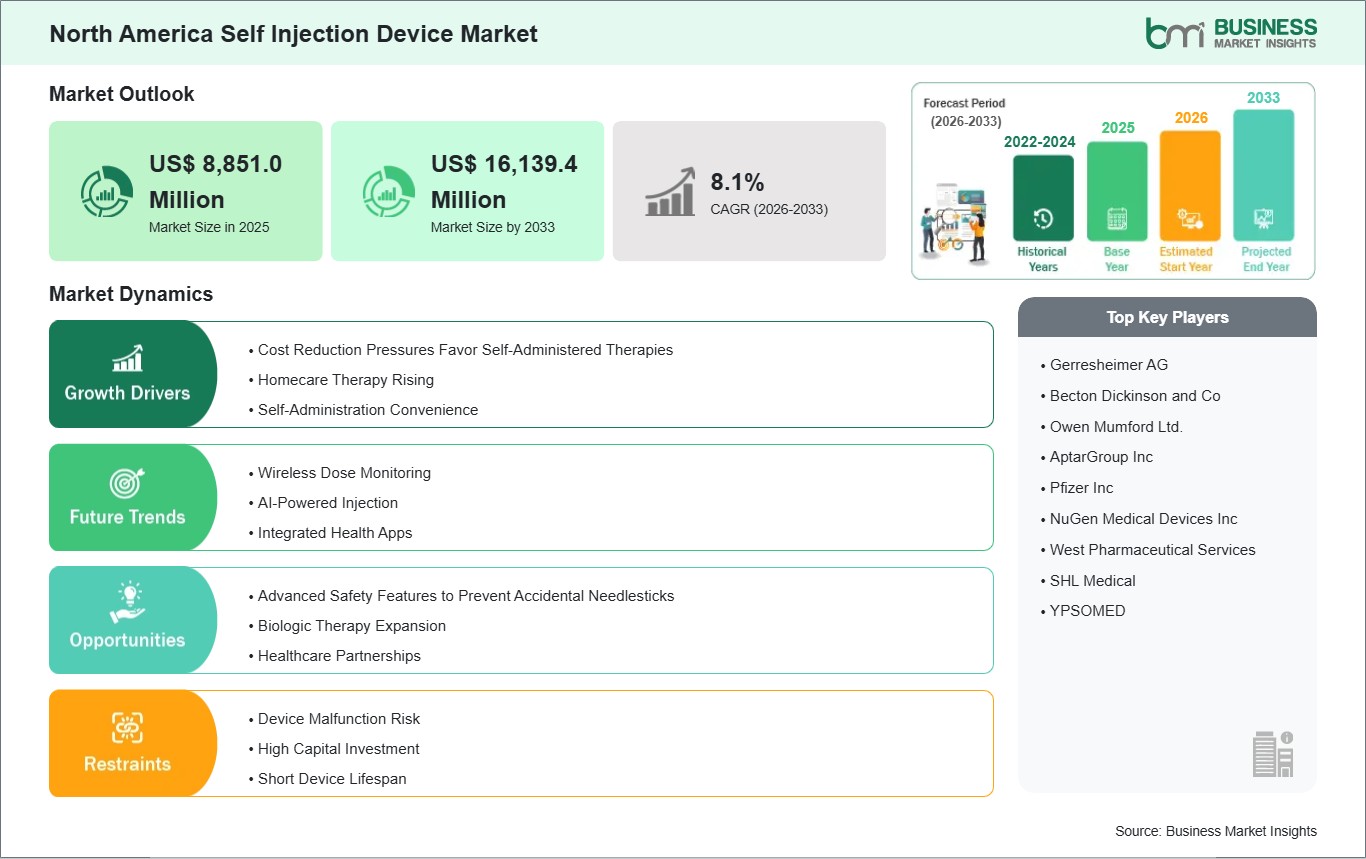

The North America Self Injection Device Market size is expected to reach US$ 16,139.4 million by 2033 from US$ 8,851.0 million in 2025. The market is estimated to record a CAGR of 8.1 % from 2026 to 2033.

Executive Summary and North America Self Injection Device Market Analysis:

The North America self-injection device market is one of the most advanced and strategically important in the global medical technology landscape, shaped by a convergence of high chronic disease prevalence, rapid adoption of biologic therapies, and integrated healthcare delivery channels. Across the US and Canada, clinicians are increasingly prescribing self-injection devices, including autoinjectors, prefilled pens, wearable systems, and connected platforms to support patient autonomy while reducing reliance on clinic-based administration. This trend is particularly evident in therapeutic areas such as diabetes, rheumatoid arthritis, multiple sclerosis, and fertility treatments. Competitive dynamics in the region are defined by robust participation from multinational device manufacturers as well as innovative startups that emphasize ease-of-use, connectivity, ergonomic design, and safety mechanisms to minimize needle injuries.

A defining characteristic of the North American market is the high penetration of digital health integration: smart injectors that pair with mobile applications, dose tracking systems, and cloud-based clinician interfaces are becoming standard offerings, enabling real-time adherence monitoring and richer longitudinal health data. The regulatory landscape in the US and Canada, while stringent, provides clear pathways for self-injection device approvals; the U.S. Food and Drug Administration (FDA) has refined guidance for combination drug-device products to reduce uncertainty in development timelines. Reimbursement environments in both countries support broad adoption, with public and private payers increasingly recognizing the long-term cost benefits of self-administration, such as reduced hospital visits and improved adherence outcomes. Distribution networks are highly diversified, spanning hospital procurement, specialty pharmacies, retail pharmacy chains, and fast-growing direct-to-patient digital channels. Challenges in the market include payer complexity, pricing pressures, and clinician hesitancy in transitioning certain patient populations to at-home self-administration. Success in this market hinges on demonstrating real-world outcomes that align patient satisfaction with clinical efficacy and health system efficiency.

North America Self Injection Device Market - Strategic Insights:

Get more information on this report

North America Self Injection Device Market Segmentation Analysis:

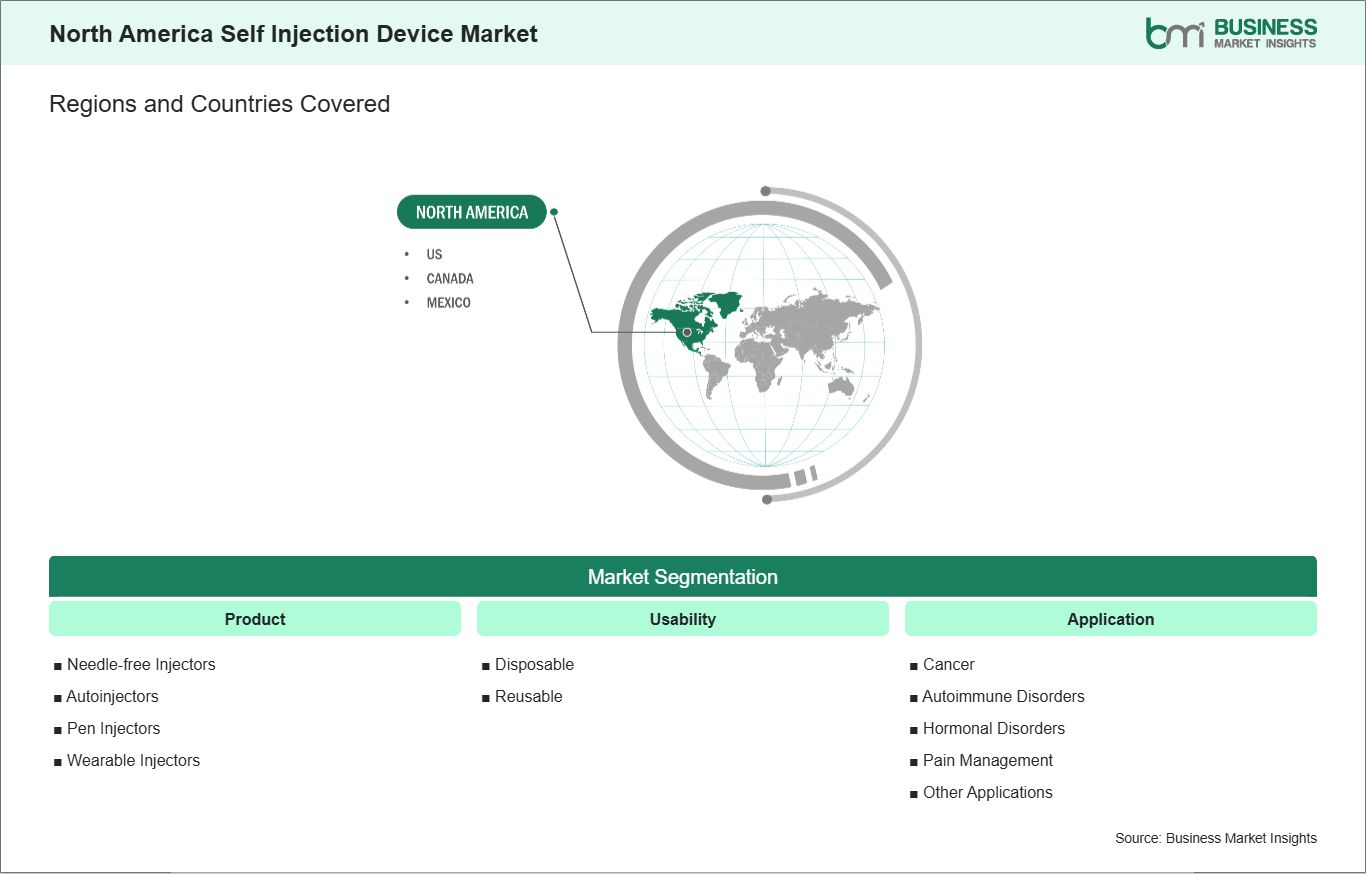

Key segments that contributed to the derivation of the North America self injection device market analysis are product, usability, and application.

By product, the self injection device market is segmented into needle-free Injectors, autoinjectors, pen Injectors, and wearable Injectors. The needle-free Injectors segment dominated the market in 2025.

Based on usability, the self injection device market is categorized into disposable and reusable. The disposable segment dominated the market in 2025.

In terms of application, the market is classified into cancer, autoimmune disorders, hormonal disorders, pain management, and other applications. The autoimmune disorders segment dominated the market in 2025.

North America Self Injection Device Market Drivers and Opportunities:

In North America, healthcare systems are under significant cost pressures driven by rising chronic disease burden, aging populations, and escalating specialty drug spending. As a result, payers and providers are increasingly encouraging self-administered therapies to reduce the need for clinic visits and hospital-based administration. Self-injection devices such as autoinjectors and prefilled pens enable patients to manage long-term treatments at home, reducing outpatient resource utilization and freeing up healthcare staff for higher-acuity care. This shift is particularly evident in chronic conditions such as diabetes and autoimmune diseases, where frequent injections are required. Cost pressures are also driving the adoption of self-injection in value-based care models. Integrated healthcare systems and insurers increasingly link reimbursement to outcomes, creating incentives for therapies that improve adherence and reduce complications. Self-injection devices support these goals by enabling more consistent dosing and reducing missed appointments.

Providers prefer devices that include adherence support features such as dose reminders and dose logging, because improved adherence can translate into fewer costly complications and hospitalizations. Another factor influencing cost reduction is the expansion of home health services and remote monitoring. Self-injection devices enable patients to stay at home while still receiving effective treatment, which is particularly important in rural areas where travel to clinics is time-consuming and expensive. Payers often cover self-injection devices because they can reduce long-term costs associated with hospital-based care and improve patient quality of life. As healthcare systems continue to focus on reducing the total cost of care, self-injected therapies are expected to become more common, supporting sustainable management of chronic diseases across North America.

Advanced Safety Features to Prevent Accidental Needlesticks

Safety concerns are a major driver of innovation in the North America self-injection device market. Needlestick injuries pose a significant risk to patients, caregivers, and waste handlers, and regulatory bodies and healthcare organizations strongly promote devices with advanced safety mechanisms. As a result, devices with automatic needle retraction, shielded needles, and tamper-proof locking systems are increasingly favored. These features are especially important for patients who self-inject at home, where proper disposal may not always be consistently practiced. In addition to preventing accidental injury, safety features are also designed to reduce the risk of dosing errors. North American patients often require complex therapies with specific dose ranges, and devices that provide clear dose confirmation and error-proof mechanisms are highly valued. For example, devices with audible clicks or tactile feedback that confirm full dose delivery help patients avoid incomplete injections.

Safety is also a key consideration for pediatric and elderly populations, who may struggle with manual dexterity and visual limitations. These groups benefit from devices that provide easier handling and built-in safety systems to prevent accidental needle exposure. Another emerging trend is the integration of safety features with disposal and waste management solutions. North American healthcare systems are increasingly concerned about the environmental and public health risks of improper sharps disposal. As a result, some self-injection devices now include built-in sharps containment, and manufacturers are developing programs for safe disposal and recycling. These developments align with broader public health campaigns aimed at reducing needlestick injuries in community settings. Overall, advanced safety features are becoming a key differentiator in the North America self-injection market, driving adoption by both patients and healthcare providers who prioritize safety and compliance.

North America Self Injection Device Market Size and Share Analysis:

The North America Self Injection Device Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, usability, and application, offering insights into their contribution to overall market performance.

By product, the needle-free Injectors subsegment dominated the market in 2025, driven by innovation in needleless technology that improves user comfort and reduces needlestick injuries.

Based on usability, the disposable subsegment dominated the market in 2025, driven by strong regulatory and patient focus on single-use safety and simplified at-home care.

In terms of application, the autoimmune disorders subsegment dominated the market in 2025, driven by growing reliance on long-term biologic therapies that patients self-administer regularly.

North America Self Injection Device Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 8,851.0 Million

Market Size by 2033

US$ 16,139.4 Million

CAGR (2026 - 2033)

8.1%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Needle-free Injectors

Autoinjectors

Pen Injectors

Wearable Injectors

By Usability

Disposable

Reusable

By Application

Cancer

Autoimmune Disorders

Hormonal Disorders

Pain Management

Other Applications

Regions and Countries Covered

North America

US, Canada, Mexico

Market leaders and key company profiles

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd.

AptarGroup Inc

Pfizer Inc

NuGen Medical Devices Inc

West Pharmaceutical Services

SHL Medical

YPSOMED

Get more information on this report

North America Self Injection Device Market Report Coverage and Deliverables:

The "North America Self Injection Device Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

North America Self Injection Device Market size and forecast at regional and country levels for all market segments covered under the scope

North America Self Injection Device Market trends, as well as drivers, restraints, and opportunities

North America Self Injection Device Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the North America Self Injection Device Market

Detailed company profiles, including SWOT analysis

North America Self Injection Device Market Geographic Insights:

The geographical scope of the North America Self Injection Device Market report is divided into the US, Canada, and Mexico. The US held the largest share in 2025.

Country-level dynamics within the North America self-injection device market reveal distinct regulatory, clinical, and payer environments that shape adoption and commercialization strategies. The US remains the dominant innovation hub and largest adoption center, supported by a mature healthcare infrastructure, integrated electronic health records, and proactive payer systems. The FDA's increasingly clear guidance on combination drug-device products facilitates streamlined development pathways for advanced autoinjectors and smart wearable injectors. High prevalence of diabetes and autoimmune conditions drives sustained demand for ergonomic pens and connected delivery systems. Payers in the US are progressively adopting value-based reimbursement models that reward improved patient outcomes and reduced hospitalization metrics, enabling broader formulary access for innovative devices.

The single-payer provincial systems in Canada influence device adoption through health technology assessments that emphasize cost-effectiveness and population health outcomes. Self-injection devices are widely adopted in urban centers with strong specialist networks, and digital health integration is supported by national interoperability initiatives. However, provincial differences in coverage criteria mean manufacturers must engage with multiple health authorities to ensure broad access. While both the US and Canada align with international safety and quality standards, the US system animates more rapid device iteration cycles due to its larger private sector investment in research and development. In contrast, Canada's emphasis on health economics prompts deeper clinical validation and post-market evidence generation. Cross-border clinical and payer collaborations are emerging to standardize best practices, particularly for connected self-injection solutions that generate real-world adherence data. Despite nuanced differences, both markets share high patient expectations for usability, digital features, and clinician-supported device training, making localized strategies critical for long-term market penetration and sustained competitive advantage.

Get more information on this report

North America Self Injection Device Market Research Report Guidance:

The report includes qualitative and quantitative data in the North America Self Injection Device Market across product, usability, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the North America Self Injection Device Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the North America Self Injection Device Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the North America Self Injection Device Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover North America Self Injection Device Market segments by product, usability, application, and geography across the US, Canada, and Mexico. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the North America Self Injection Device Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

North America Self Injection Device Market News and Key Development:

The North America Self Injection Device Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the North America self injection device market are:

In April 2025, NuGen Medical Devices expanded distribution of its InsuJet needle-free injection device across Canada, placing the device in major retail pharmacy and distributor channels, such as Shoppers Drug Mart, London Drugs, and McKesson Canada. Following its Health Canada approval and initial introduction in late 2024, this expanded availability enhanced access to a needle-free self-injection option for diabetes care in the Canadian market. The broader rollout underscores growing interest in alternative delivery systems beyond traditional needle-based pens and pumps. This distribution expansion marks a meaningful product availability milestone in the self-injection landscape of North America.

In August 2024, the FDA expanded clearance for the Omnipod 5 Automated Insulin Delivery System to include people with Type 2 diabetes in the United States, making it the first automated insulin delivery system approved for both Type 1 and Type 2 diabetes management. This approval broadened access to a wearable, tubeless self-delivery platform that integrates with continuous glucose monitoring and supports more flexible, at-home care. The expanded indication marked a significant shift in how insulin delivery devices are leveraged across chronic patient segments. The rollout reinforces the trend toward automated and connected self-injection solutions in North America.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the North America Self Injection Device Market?

The North America Self Injection Device Market is valued at US$ 8,851.0 Million in 2025, it is projected to reach US$ 16,139.4 Million by 2033.

What is the CAGR for North America Self Injection Device Market by (2026 - 2033)?

As per our report North America Self Injection Device Market, the market size is valued at US$ 8,851.0 Million in 2025, projecting it to reach US$ 16,139.4 Million by 2033. This translates to a CAGR of approximately 8.1% during the forecast period.

What segments are covered in this report?

The North America Self Injection Device Market report typically cover these key segments-

Application (Cancer, Autoimmune Disorders, Hormonal Disorders, Pain Management, Other Applications)

What is the historic period, base year, and forecast period taken for North America Self Injection Device Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Self Injection Device Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in North America Self Injection Device Market?

The North America Self Injection Device Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd.

AptarGroup Inc

Pfizer Inc

NuGen Medical Devices Inc

West Pharmaceutical Services

SHL Medical

YPSOMED

Who should buy this report?

The North America Self Injection Device Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the North America Self Injection Device Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For North America Self Injection Device Market

Get Free Sample For North America Self Injection Device Market