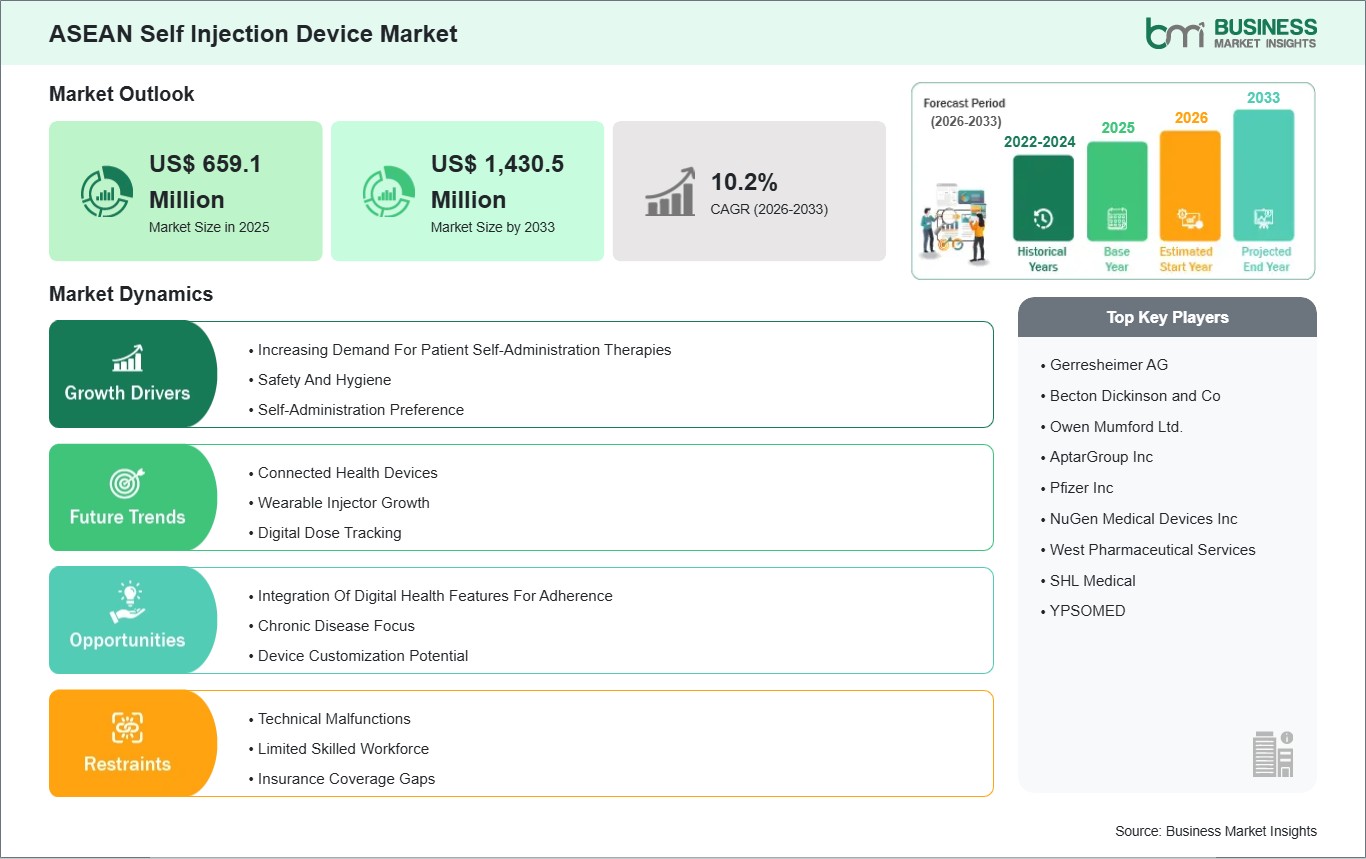

The ASEAN Self Injection Device Market size is expected to reach US$ 1,430.5 million by 2033 from US$ 659.1 million in 2025. The market is estimated to record a CAGR of 10.2 % from 2026 to 2033.

Executive Summary and ASEAN Self Injection Device Market Analysis:

The ASEAN self injection device market is characterized by robust innovation and expanding accessibility across urban and semi-urban areas. Key market drivers include the integration of smart technology into devices, such as digital dose tracking, connectivity with mobile health applications, and reminder systems that improve adherence and patient outcomes. These advancements are particularly relevant in regions with growing smartphone penetration, enabling real-time monitoring and remote patient management. Additionally, healthcare systems are increasingly adopting policies to decentralize chronic disease management, which is accelerating the demand for at-home self-injection solutions. Strategic collaborations between device manufacturers and pharmaceutical companies are expected to introduce combination offerings, integrating medication delivery with user-friendly injection platforms.

From a regulatory perspective, harmonization initiatives among ASEAN member states are gradually simplifying product approvals, which will facilitate faster market entry for new technologies. Market players are also exploring subscription-based or rental models to reduce cost barriers for patients while maintaining consistent revenue streams. Furthermore, education campaigns led by healthcare providers and patient advocacy groups are anticipated to strengthen market penetration by addressing misconceptions and improving technique proficiency. The outlook also highlights the potential for expansion in niche therapeutic areas beyond diabetes, such as growth hormone therapy, hemophilia, and immunotherapy treatments, where patient self-management can significantly reduce hospital visits.

Environmental sustainability trends are beginning to influence device design, with biodegradable components and recyclable packaging being prioritized to meet regulatory expectations and consumer preferences. Collectively, these factors indicate that the market is undergoing a quantitative and qualitative transformation, emphasizing patient empowerment, technological integration, and sustainable practices that will define competitive leadership.

Key segments that contributed to the derivation of the ASEAN self injection device market analysis are product, usability, and application.

By product, the self injection device market is segmented into needle-free Injectors, autoinjectors, pen Injectors, and wearable Injectors. The needle-free Injectors segment dominated the market in 2025.

Based on usability, the self injection device market is categorized into disposable and reusable. The disposable segment dominated the market in 2025.

In terms of application, the market is classified into cancer, autoimmune disorders, hormonal disorders, pain management, and other applications. The autoimmune disorders segment dominated the market in 2025.

ASEAN Self Injection Device Market Drivers and Opportunities:

Increasing Demand For Patient Self-Administration Therapies

Across ASEAN, there has been a rapid rise in chronic diseases, particularly diabetes and autoimmune disorders. In Indonesia—where urban lifestyles and rising obesity rates have increased Type 2 diabetes prevalence—self-injection devices are becoming more common in community pharmacies and primary care clinics. Pen injectors and prefilled syringes are preferred by patients who have to travel long distances to reach hospitals and reduce repeated clinic visits. In rural areas, local health posts increasingly rely on self-administration as a practical solution to physician shortages. Malaysia's healthcare system has shown a strong push toward outpatient chronic disease management, and self-administration devices are being adopted as part of national diabetes programs. Public clinics now frequently provide basic injection training and follow-up through nurse-led sessions, making self-administration more acceptable among older patients.

In cities such as Kuala Lumpur and Penang, pharmacies are also offering counseling on device selection and storage, which has helped reduce common user errors such as improper needle disposal or incorrect dose settings. Thailand and Vietnam represent two distinct adoption paths. Thailand's well-developed hospital network has created a strong foundation for patient education, enabling patients to transition from clinic-based injections to home use. In Bangkok and Chiang Mai, specialized diabetes centers report higher rates of pen injector use due to structured training and community support groups. Vietnam is experiencing rapid growth in the middle class and rising healthcare awareness. In Ho Chi Minh City and Hanoi, private clinics are increasingly recommending autoinjectors for chronic inflammatory conditions, and pharmacies are becoming more proactive in patient education.

Integration Of Digital Health Features For Adherence

Digital health integration is shaping the next phase of self-injection adoption across ASEAN, with countries showing varying levels of readiness based on infrastructure and smartphone penetration. Singapore is the regional leader, with widespread smartphone use and strong digital healthcare ecosystems. Self-injection devices with Bluetooth connectivity are being piloted in specialist clinics, allowing patients to automatically log dose timing and share data with their healthcare team. This is especially valuable for high-risk patients, such as those with complicated diabetes management or chronic inflammatory conditions, where missed doses can quickly lead to complications. Digital reminders, dose tracking, and clinician alerts are becoming standard expectations among urban Singaporean patients.

Malaysia and Thailand are rapidly catching up, particularly in urban centers where telehealth is increasingly used for chronic disease follow-ups. In Kuala Lumpur, digital self-injection platforms are being integrated into hospital patient portals, enabling physicians to monitor adherence trends and intervene if a patient repeatedly misses doses. Thailand's telemedicine expansion has similarly enabled remote counseling and adherence support, especially for patients living outside major cities. In provinces such as Chiang Rai and Khon Kaen, patients can attend virtual check-ins after training sessions, reducing the burden of travel while ensuring proper injection technique. Indonesia, the Philippines, and Vietnam face stronger digital adoption constraints due to uneven connectivity; however, they are still progressing rapidly through mobile-first strategies.

In the Philippines, smartphone penetration is high, and telehealth apps are widely used, creating a natural environment for connected injection devices. Patients in Metro Manila increasingly rely on digital reminders and app-based dose tracking, especially those managing diabetes while balancing demanding work schedules. In Vietnam, app-based patient communities and clinic-led digital follow-ups are emerging in major cities, supporting adherence to chronic therapies. Indonesia's fragmented healthcare system is witnessing growth in digital adherence tools through pharmacy networks and private clinics, particularly in Java and Bali, where patients use mobile apps to log injections and receive automated refill reminders. Overall, digital integration is becoming a key differentiator in ASEAN, improving adherence and transforming self-injection devices from standalone tools into connected health solutions.

ASEAN Self Injection Device Market Size and Share Analysis:

The ASEAN Self Injection Device Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, usability, and application, offering insights into their contribution to overall market performance.

By product, the needle-free Injectors subsegment dominated the market in 2025, driven by growing demand for painless, user-friendly drug delivery that reduces needle anxiety and needlestick risks.

Based on usability, the disposable subsegment dominated the market in 2025, driven by patient preference for convenience, hygiene, and lower infection risk from single-use devices.

In terms of application, the autoimmune disorders subsegment dominated the market in 2025, driven by the rising prevalence of chronic autoimmune conditions requiring frequent injectable biologics and targeted therapies.

Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam

Market leaders and key company profiles

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd.

AptarGroup Inc

Pfizer Inc

NuGen Medical Devices Inc

West Pharmaceutical Services

SHL Medical

YPSOMED

Get more information on this report

ASEAN Self Injection Device Market Report Coverage and Deliverables:

The "ASEAN Self Injection Device Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

ASEAN Self Injection Device Market size and forecast at regional and country levels for all market segments covered under the scope

ASEAN Self Injection Device Market trends, as well as drivers, restraints, and opportunities

ASEAN Self Injection Device Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the ASEAN Self Injection Device Market

Detailed company profiles, including SWOT analysis

The geographical scope of the ASEAN Self Injection Device Market report is divided into Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam. Indonesia held the largest share in 2025.

Indonesia holds the largest share of the ASEAN self injection device market, driven by its vast population base, rapidly expanding middle class, and growing prevalence of chronic diseases. The market is highly price-sensitive, prompting manufacturers to focus on cost-competitive product lines, local manufacturing, and distribution partnerships to increase affordability and reach. Malaysia exhibits strong growth potential due to its balanced public-private healthcare model, rising insurance coverage, and increasing patient preference for pen injectors and autoinjectors in diabetes and autoimmune therapy segments.

Singapore, as the most advanced market in the region, is characterized by high adoption of premium, smart-enabled devices and rigorous regulatory standards; market players often prioritize innovation, digital connectivity, and premium positioning to meet consumer expectations. In the Philippines, demand is expanding through urban healthcare modernization and telehealth adoption. Still, out-of-pocket expenditure remains high, steering consumers toward lower-cost devices and generic drug-device combinations. Thailand presents a mature hospital-based market with high device adoption in metropolitan areas; however, rural penetration is constrained by limited access and lower health literacy, encouraging companies to invest in patient education and decentralized distribution models.

Market growth in Vietnam is propelled by rising healthcare spending, expanding private clinics, and growing chronic disease awareness. However, inconsistent reimbursement and fragmented supply chains require strategic collaborations with local distributors and tiered pricing strategies. Overall, market success across these six countries depends on aligning product offerings with local affordability, regulatory requirements, and patient education levels.

Get more information on this report

ASEAN Self Injection Device Market Research Report Guidance:

The report includes qualitative and quantitative data in the ASEAN Self Injection Device Market across product, usability, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the ASEAN Self Injection Device Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the ASEAN Self Injection Device Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the ASEAN Self Injection Device Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover ASEAN Self Injection Device Market segments by product, usability, application, and geography across Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the ASEAN Self Injection Device Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

ASEAN Self Injection Device Market News and Key Development:

The ASEAN Self Injection Device Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the ASEAN Self Injection Device Market are:

In October 2025, Hyphens Pharma extended its partnership with medac to broaden the commercialisation of the Metoject subcutaneous autoinjector pen into Thailand and Cambodia, building on its existing rights across Singapore, Malaysia, the Philippines, and Vietnam. The expansion enhances access to a trusted self-injection therapy for rheumatoid arthritis across Southeast Asia.

In March 2025, Hyphens Pharma secured exclusive rights to register and commercialise the Metoject autoinjector pen in Singapore, Malaysia, the Philippines, and Vietnam. This move marked a significant step in its product launch strategy, aimed at expanding the availability of methotrexate-based self-injection treatment for rheumatoid arthritis across key ASEAN markets.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the ASEAN Self Injection Device Market?

The ASEAN Self Injection Device Market is valued at US$ 659.1 Million in 2025, it is projected to reach US$ 1,430.5 Million by 2033.

What is the CAGR for ASEAN Self Injection Device Market by (2026 - 2033)?

As per our report ASEAN Self Injection Device Market, the market size is valued at US$ 659.1 Million in 2025, projecting it to reach US$ 1,430.5 Million by 2033. This translates to a CAGR of approximately 10.2% during the forecast period.

What segments are covered in this report?

The ASEAN Self Injection Device Market report typically cover these key segments-

Application (Cancer, Autoimmune Disorders, Hormonal Disorders, Pain Management, Other Applications)

What is the historic period, base year, and forecast period taken for ASEAN Self Injection Device Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the ASEAN Self Injection Device Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in ASEAN Self Injection Device Market?

The ASEAN Self Injection Device Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd.

AptarGroup Inc

Pfizer Inc

NuGen Medical Devices Inc

West Pharmaceutical Services

SHL Medical

YPSOMED

Who should buy this report?

The ASEAN Self Injection Device Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the ASEAN Self Injection Device Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For ASEAN Self Injection Device Market

Get Free Sample For ASEAN Self Injection Device Market