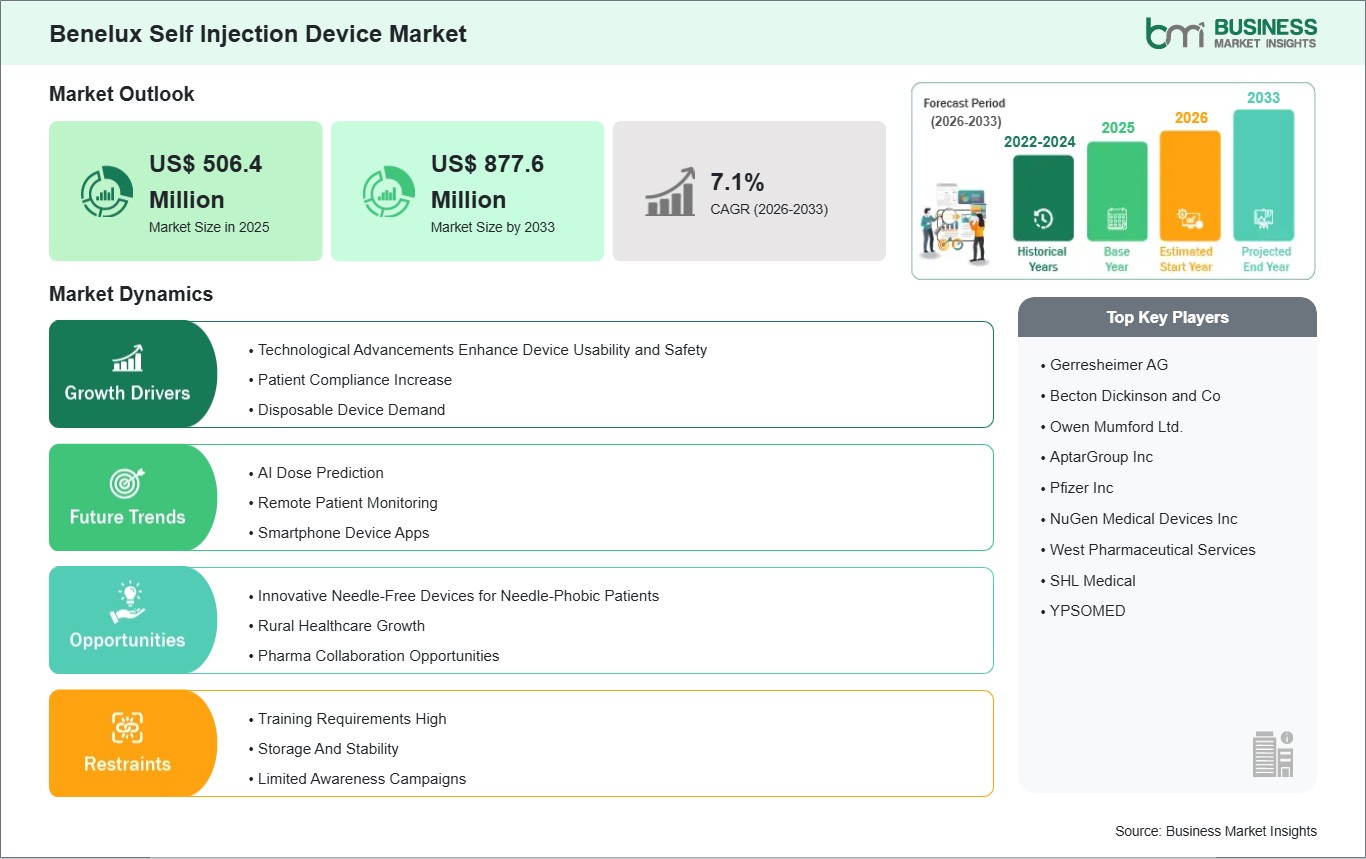

The Benelux Self Injection Device Market size is expected to reach US$ 877.6 million by 2033 from US$ 506.4 million in 2025. The market is estimated to record a CAGR of 7.1 % from 2026 to 2033.

Executive Summary and Benelux Self Injection Device Market Analysis:

The Benelux self injection device market is at a pivotal juncture as demand for patient-centric drug delivery solutions continues to grow amid rising chronic disease prevalence and expanding biologic therapy adoption. In the Benelux region, traditional healthcare delivery models are being reoriented toward outpatient and home-based care paradigms that emphasize convenience, adherence, and cost-effectiveness. This shift is supported by well-developed healthcare infrastructures and a high degree of health insurance penetration, which together facilitate broader patient access to advanced delivery technologies such as autoinjectors, pen injectors, and wearable injectors.

Subcutaneous delivery remains the dominant administration route for self-injection devices, particularly for the management of diabetes, autoimmune disorders, and hormonal therapies, while applications in autoimmune diseases are experiencing some of the fastest growth within device-use segments. The competitive landscape reflects established multinational medical device players and agile regional manufacturers leveraging localized distribution strategies and post-market support services to strengthen market positioning. Collaborative initiatives between healthcare providers, insurers, and device manufacturers are increasingly focused on structured patient education programs, which are critical to driving self-injection adoption, improving technique proficiency, and reducing adverse events. Regulatory frameworks across the three countries align with broader European Union medical device standards, emphasizing product safety, traceability, and quality management, which necessitate rigorous compliance for market entry and sustainment. Distribution channels are evolving, with digital pharmacy platforms and remote counselling services growing in relevance alongside traditional hospital and retail pharmacy outlets. Overall, the market demonstrates a dynamic interplay of patient demand, technological innovation, and regulatory rigor, suggesting that stakeholders investing in integrated care pathways and user-optimized devices are well-positioned to capture growth.

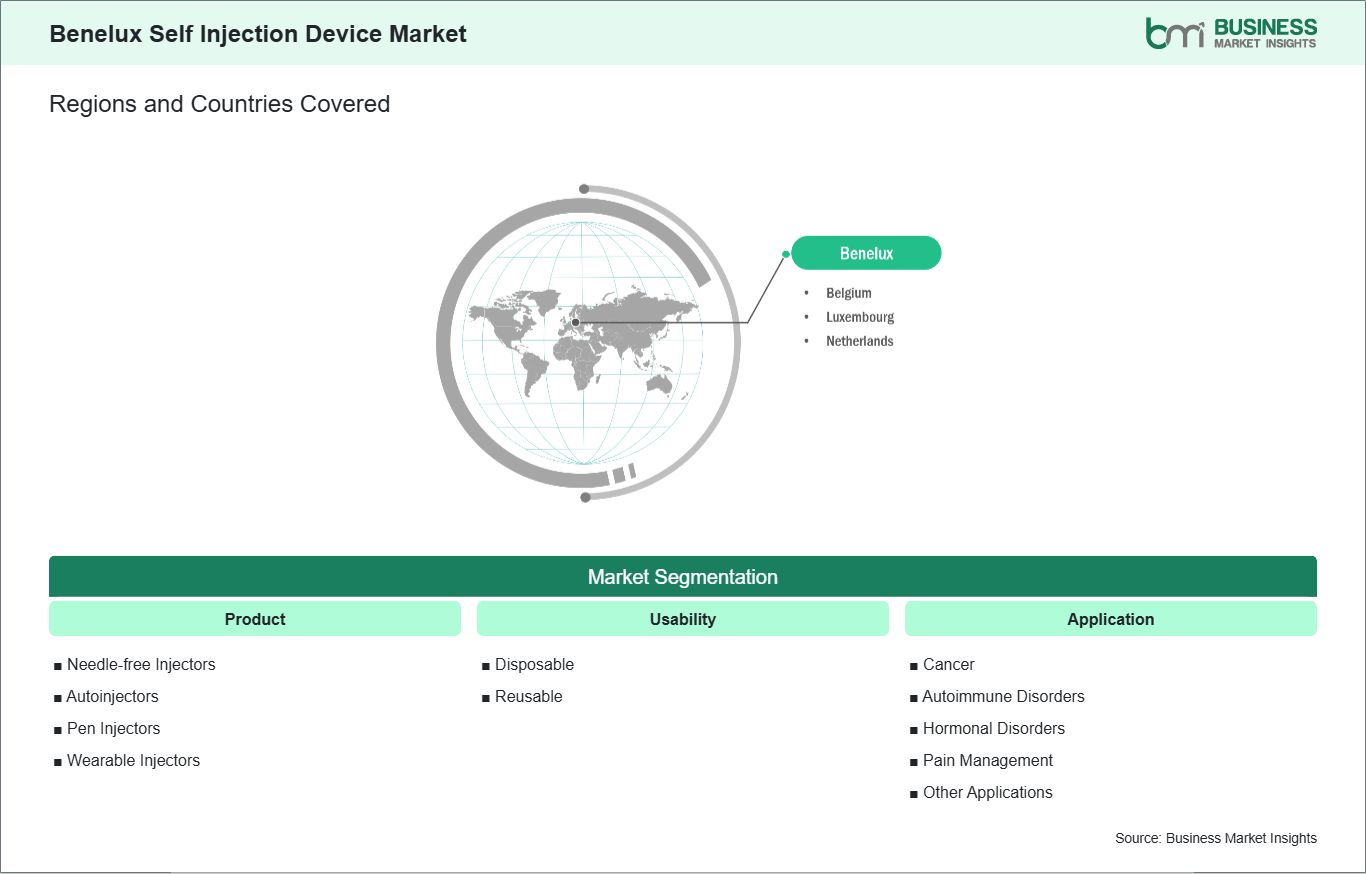

Key segments that contributed to the derivation of the Benelux self injection device market analysis are product, usability, and application.

By product, the self injection device market is segmented into needle-free Injectors, autoinjectors, pen Injectors, and wearable Injectors. The needle-free Injectors segment dominated the market in 2025.

Based on usability, the self injection device market is categorized into disposable and reusable. The disposable segment dominated the market in 2025.

In terms of application, the market is classified into cancer, autoimmune disorders, hormonal disorders, pain management, and other applications. The autoimmune disorders segment dominated the market in 2025.

Benelux Self Injection Device Market Drivers and Opportunities:

Technological Advancements Enhance Device Usability and Safety

In Belgium, technological innovation in self-injection devices is being driven by the country's strong hospital and specialist clinic networks, particularly in oncology and rheumatology. Belgian clinics have increasingly shifted toward autoinjectors and smart pen systems for chronic therapies, reducing the need for frequent clinic visits. These devices often include ergonomic designs, simplified dosing settings, and safety features such as needle shields and lock mechanisms. This trend is supported by Belgium's well-established home care system, which allows nurses to train patients on device use at home, especially for biologic therapies where correct administration is crucial to avoid dosing errors. The Netherlands is a key hub for medical device innovation in Europe. Dutch manufacturers and healthcare providers have been at the forefront of integrating advanced safety features such as automatic needle retraction, clear dose confirmation windows, and low-force injection mechanisms. In the Netherlands, patients with chronic diseases such as diabetes and multiple sclerosis increasingly use reusable pens and autoinjectors, supported by pharmacy-based training programs. The country's strong emphasis on patient autonomy and self-care has encouraged widespread adoption of devices that minimize user error and enhance safety.

Luxembourg's market is smaller but highly specialized, with high per-capita healthcare spending and strong patient support programs. Self-injection devices are commonly used for chronic conditions such as diabetes and rheumatoid arthritis, where the health system supports home-based treatment through structured patient education. Luxembourg's insurers often cover advanced devices with safety features, encouraging uptake among patients who prefer self-management. The country's focus on patient safety has also led to the adoption of devices with integrated needle disposal and reduced risk of accidental needlestick injury, reflecting broader Benelux trends toward safer and more user-friendly self-injection solutions.

Innovative Needle-Free Devices for Needle-Phobic Patients

In Belgium, needle phobia remains a barrier to treatment adherence for some patients, particularly those needing frequent injections, such as diabetics and patients on biologic therapies. To address this, clinics and hospitals in Belgium are increasingly exploring needle-free delivery systems such as jet injectors and needle-free patches. These technologies are especially appealing in pediatric care, where fear of needles can create significant compliance issues. Belgian hospitals have begun piloting needle-free systems in specialized departments, and patient advocacy groups are actively promoting alternatives that reduce anxiety and improve long-term adherence.

The Netherlands has one of the highest levels of patient engagement and healthcare digitalization in Europe, making it a fertile ground for the adoption of needle-free devices. Dutch pharmacies and diabetes care centers are beginning to offer needle-free injection alternatives as part of broader patient-centered care programs. These devices are particularly attractive for younger patients and those with needle phobia who otherwise might delay or avoid treatment. Dutch healthcare providers emphasize training and support, ensuring patients understand how needle-free systems work and feel confident using them at home.

Luxembourg's smaller population means the market for needle-free devices is niche, but demand is growing among patients seeking comfortable treatment options. Luxembourg's health insurers often cover advanced therapeutic devices, and the high-income population is more likely to adopt innovative solutions such as needle-free injectors for insulin and biologics. Patient support programs in Luxembourg are also promoting alternative delivery options for needle-phobic patients, particularly for chronic conditions requiring long-term therapy. Across Benelux, the trend toward needle-free devices reflects broader patient expectations for more comfortable, less invasive treatment options.

Benelux Self Injection Device Market Size and Share Analysis:

The Benelux Self Injection Device Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, usability, and application, offering insights into their contribution to overall market performance.

By product, the needle-free Injectors subsegment dominated the market in 2025, driven by a strong preference for pain-reducing and user-friendly administration among patients and caregivers.

Based on usability, the disposable subsegment dominated the market in 2025, driven by high demand for convenient, single-use devices that enhance safety and infection control.

In terms of application, the autoimmune disorders subsegment dominated the market in 2025, driven by rising treatment needs for chronic autoimmune conditions requiring frequent injectable therapies.

Benelux Self Injection Device Market Report Coverage and Deliverables:

The "Benelux Self Injection Device Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Benelux Self Injection Device Market size and forecast at regional and country levels for all market segments covered under the scope

Benelux Self Injection Device Market trends, as well as drivers, restraints, and opportunities

Benelux Self Injection Device Market analysis, covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Benelux Self Injection Device Market

Detailed company profiles, including SWOT analysis

The geographical scope of the Benelux Self Injection Device Market report is divided into Belgium, the Netherlands, and Luxembourg. The Netherlands held the largest share in 2025.

Country-level analysis of the Benelux self-injection device market reveals nuanced trends driven by local healthcare structures, policy environments, and patient expectations across Belgium, the Netherlands, and Luxembourg. In Belgium, self-injection devices are increasingly important in chronic disease management, particularly for autoimmune disorders where the subcutaneous route dominates usage; this reflects both established clinical protocols and growing patient preference for home-based treatments. Belgium's robust direct tender and hospital procurement channels play a central role in device distribution, complemented by emerging digital pharmacy platforms that enhance access and convenience.

The Netherlands exhibits a strong affinity for self-injection technologies across endocrinological and immunological therapies, supported by high patient literacy and proactive healthcare provider engagement. Dutch market dynamics show notable growth in segments such as autoimmune disease applications and single-dose formats, underscoring evolving patient needs and prescribing trends. In Luxembourg, high disposable incomes and comprehensive insurance coverage contribute to rapid uptake of advanced, user-friendly injectors with discreet form factors, even as the market remains comparatively smaller in scale.

Cross-country regulatory alignment within the EU ensures consistent safety expectations, but localized reimbursement criteria and healthcare reimbursement pathways can differ, necessitating tailored market access strategies for device manufacturers. Despite these differences, all three Benelux countries share a commitment to patient education, digital health integration, and quality care delivery, which collectively support increasing adoption of self-injection therapies.

Get more information on this report

Benelux Self Injection Device Market Research Report Guidance:

The report includes qualitative and quantitative data in the Benelux Self Injection Device Market across product, usability, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Benelux Self Injection Device Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Benelux Self Injection Device Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Benelux Self Injection Device Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Benelux Self Injection Device Market segments by product, usability, application, and geography across Belgium, the Netherlands, and Luxembourg. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Benelux Self Injection Device Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Benelux Self Injection Device Market News and Key Development:

The Benelux Self Injection Device Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Benelux self injection device market are:

In May 2025, Sandoz launched the PYZCHIVA autoinjector, the first commercially available ustekinumab biosimilar in an autoinjector format across Europe, including Belgium and the Netherlands, enhancing self-administration options for chronic inflammatory diseases. The device offers automatic dosing and improved comfort, directly addressing patient adherence challenges in Benelux healthcare settings. This launch underscores the region's adoption of next-generation self-injection formats for biologics as standard care and strengthens the availability of patient-centric delivery solutions within advanced European markets.

In December 2025, TempraMed expanded its distribution footprint into the Benelux through a strategic partnership with Salomo Executive, bringing temperature-controlled solutions for injectable medications to pharmacies and care providers in Belgium, the Netherlands, and Luxembourg. While not a device launch, this rollout significantly improves the storage and usability of self-injection therapies, such as insulin, supporting safer daily use by chronic patients. It reflects increasing supply-chain sophistication and support for self-administration ecosystems in Benelux markets.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Benelux Self Injection Device Market?

The Benelux Self Injection Device Market is valued at US$ 506.4 Million in 2025, it is projected to reach US$ 877.6 Million by 2033.

What is the CAGR for Benelux Self Injection Device Market by (2026 - 2033)?

As per our report Benelux Self Injection Device Market, the market size is valued at US$ 506.4 Million in 2025, projecting it to reach US$ 877.6 Million by 2033. This translates to a CAGR of approximately 7.1% during the forecast period.

What segments are covered in this report?

The Benelux Self Injection Device Market report typically cover these key segments-

Application (Cancer, Autoimmune Disorders, Hormonal Disorders, Pain Management, Other Applications)

What is the historic period, base year, and forecast period taken for Benelux Self Injection Device Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Benelux Self Injection Device Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Benelux Self Injection Device Market?

The Benelux Self Injection Device Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd.

AptarGroup Inc

Pfizer Inc

NuGen Medical Devices Inc

West Pharmaceutical Services

SHL Medical

YPSOMED

Who should buy this report?

The Benelux Self Injection Device Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Benelux Self Injection Device Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Benelux Self Injection Device Market

Get Free Sample For Benelux Self Injection Device Market