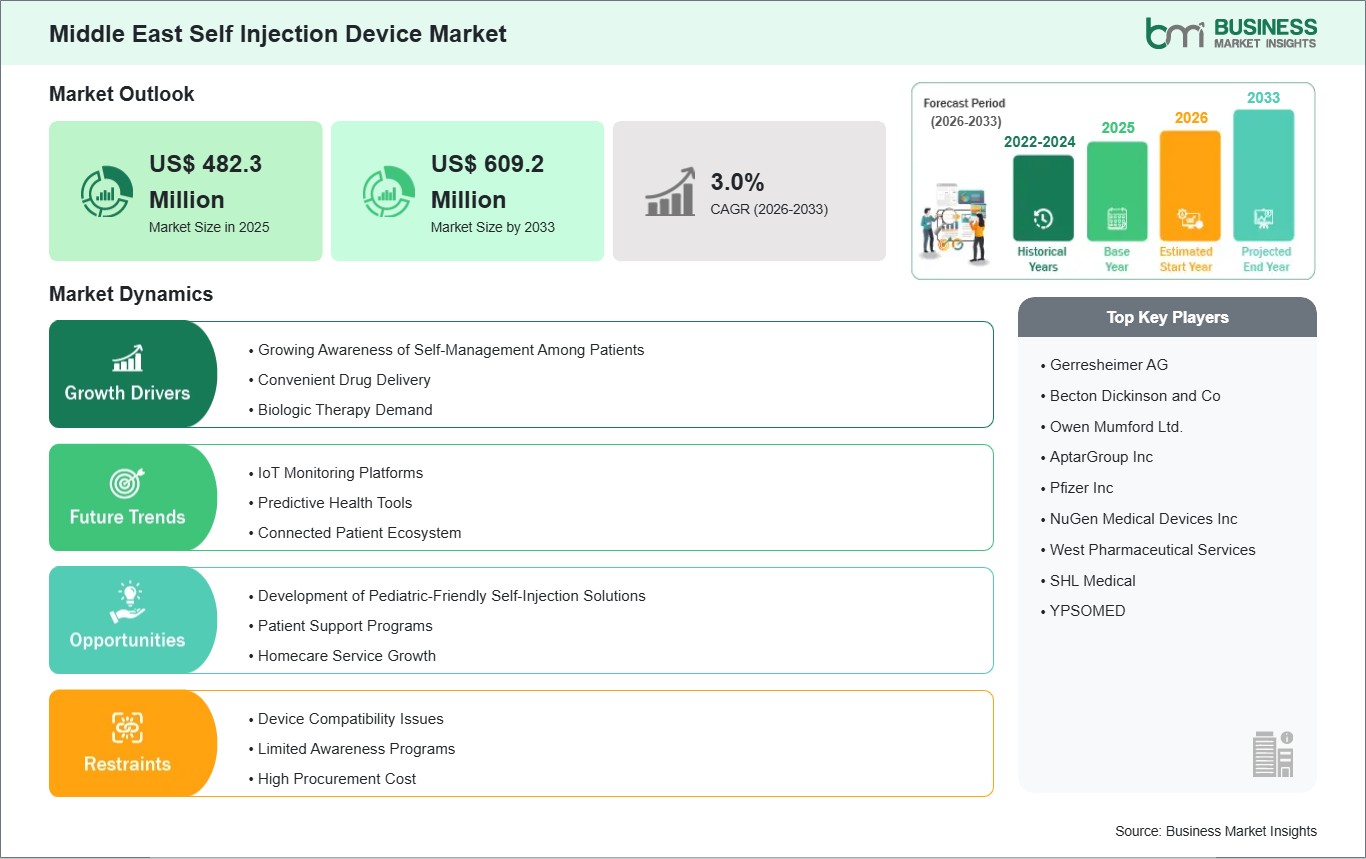

The Middle East Self Injection Device Market size is expected to reach US$ 609.2 million by 2033 from US$ 482.3 million in 2025. The market is estimated to record a CAGR of 3.0 % from 2026 to 2033.

Executive Summary and Middle East Self Injection Device Market Analysis:

The Middle East self-injection device market is evolving rapidly as regional healthcare systems prioritize decentralized care, chronic disease management, and patient autonomy. Persistently high prevalence rates of diabetes, autoimmune conditions, and growth in specialty biologic therapies have compelled healthcare providers, payers, and policymakers to integrate self-administration devices such as autoinjectors, prefilled pens, and wearable delivery systems into treatment paradigms. Governments in the Gulf Cooperation Council (GCC), notably Saudi Arabia and the UAE, are scaling investments in chronic care infrastructure and implementing regulatory reforms that streamline approval pathways for combination drug-device products, reflecting broader commitments to enhancing patient outcomes and easing clinical burdens.

Multichannel distribution frameworks are emerging, as traditional hospital tenders, retail pharmacy networks, and digital pharmacy platforms expand reach, while telemedicine platforms support remote patient education and post-prescription care. Competitive dynamics involve multinational manufacturers, regional distributors, and strategic alliances that emphasize supply continuity, clinician engagement programs, and localized training resources to build confidence in self-injection adoption. Operational challenges persist; regional heterogeneity in reimbursement frameworks means price sensitivity can impede device uptake in non-GCC and lower-coverage markets.

Countries where insurance penetration remains limited face slower adoption curves, requiring manufacturers to deploy tiered pricing strategies or co-development partnerships with public health systems. Physician and patient education efforts are increasingly regarded as key differentiators, with successful market entrants investing in technique training, adherence programs, and digital support tools to reduce administration errors and improve long-term outcomes. Market analysis indicates that sustainable adoption will depend on aligning device portfolios with regional healthcare priorities, including enhanced digital support, regulatory compliance, and value-based care outcomes.

Middle East Self Injection Device Market - Strategic Insights:

Get more information on this report

Middle East Self Injection Device Market Segmentation Analysis:

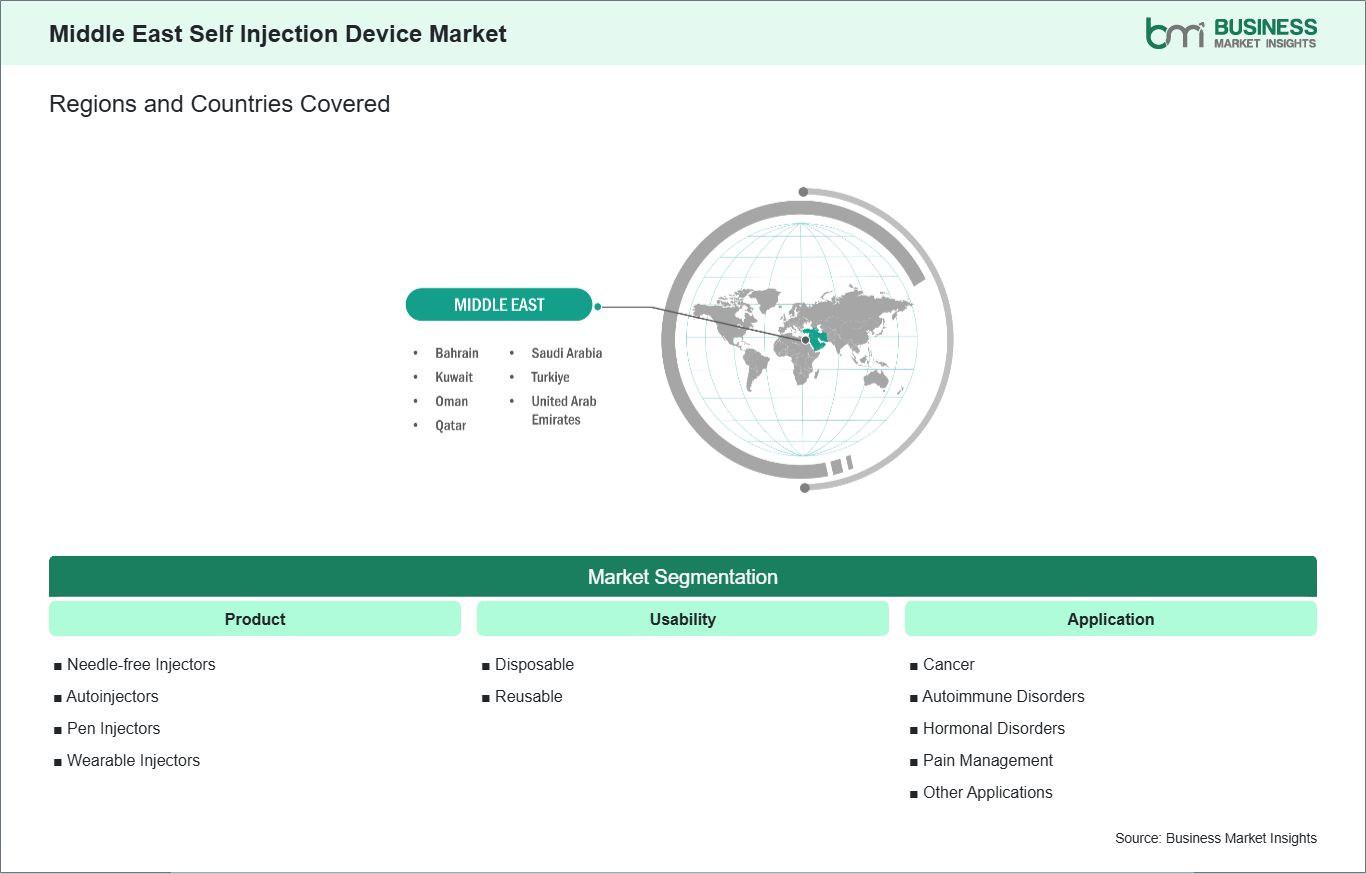

Key segments that contributed to the derivation of the Middle East self injection device market analysis are product, usability, and application.

By product, the self injection device market is segmented into needle-free Injectors, autoinjectors, pen Injectors, and wearable Injectors. The needle-free Injectors segment dominated the market in 2025.

Based on usability, the self injection device market is categorized into disposable and reusable. The disposable segment dominated the market in 2025.

In terms of application, the market is classified into cancer, autoimmune disorders, hormonal disorders, pain management, and other applications. The autoimmune disorders segment dominated the market in 2025.

Middle East Self Injection Device Market Drivers and Opportunities:

Growing Awareness of Self-Management Among Patients

Across the Middle East, patient awareness of self-management is increasing as healthcare systems place greater emphasis on chronic disease control and preventive care. The rising prevalence of diabetes, autoimmune disorders, and hormonal conditions has encouraged patients to take a more active role in managing long-term therapies. Educational campaigns led by hospitals, pharmacies, and digital health platforms are improving patient understanding of self-injection techniques, safety, and adherence. As a result, self-injection devices are increasingly viewed as empowering tools. Urbanization and high smartphone penetration in the Middle East have also played a major role in shaping patient behavior.

Patients now have greater access to online educational resources, instructional videos, and virtual consultations that reinforce correct self-injection practices. This digital exposure has reduced fear associated with injectable therapies and increased confidence in home administration. In parallel, pharmacies and outpatient clinics frequently offer structured onboarding sessions for patients initiating injectable treatments, supporting sustained adherence and correct device usage. Cultural shifts are further reinforcing self-management trends. Busy lifestyles, frequent travel, and work commitments make repeated clinic visits inconvenient for many patients. Self-injection devices enable flexible treatment schedules while maintaining clinical effectiveness.

For elderly patients and those with mobility limitations, self-administration also reduces dependence on caregivers and healthcare facilities. Overall, growing awareness of self-management in the Middle East is accelerating the adoption of self-injection devices and reshaping chronic disease care toward a more patient-centered model.

Development of Pediatric-Friendly Self-Injection Solutions

Pediatric care is emerging as an important focus area in the Middle East self-injection device market, driven by rising diagnosis rates of pediatric diabetes, growth hormone deficiencies, and autoimmune conditions. Children requiring long-term injectable therapy present unique challenges, including fear of needles, anxiety, and reliance on caregivers. To address this challenge, manufacturers are developing pediatric-friendly self-injection solutions designed to reduce pain perception and simplify administration. Devices with hidden needles, shorter injection times, and quieter mechanisms are gaining attention among pediatric specialists.

Healthcare providers in the Middle East increasingly recognize the importance of early treatment adherence in pediatric populations. Pediatric-friendly devices often feature colorful designs, smaller form factors, and intuitive operation to make injections less intimidating. These features help reduce treatment resistance and improve long-term outcomes. Training programs aimed at parents and caregivers emphasize proper technique, storage, and emotional reassurance, ensuring that home administration is both safe and stress-free. Hospitals and specialty clinics are playing a key role in introducing these devices during early treatment stages.

The development of pediatric self-injection solutions also aligns with broader healthcare goals in the Middle East, including improved quality of life and reduced hospital dependency. Devices that allow children to receive therapy at home minimize school disruptions and reduce the emotional burden of frequent clinic visits. As awareness grows among caregivers and healthcare professionals, demand for child-specific injection solutions is expected to increase

Middle East Self Injection Device Market Size and Share Analysis:

The Middle East Self Injection Device Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, usability, and application, offering insights into their contribution to overall market performance.

By product, the needle-free Injectors subsegment dominated the market in 2025, driven by increasing adoption of advanced injection technologies that improve patient comfort and adherence.

Based on usability, the disposable subsegment dominated the market in 2025, driven by healthcare systems' emphasis on infection control and reduced device handling.

In terms of application, the autoimmune disorders subsegment dominated the market in 2025, driven by expanding use of biologic therapies that require long-term, at-home administration.

Middle East Self Injection Device Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 482.3 Million

Market Size by 2033

US$ 609.2 Million

CAGR (2026 - 2033)

3.0%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Needle-free Injectors

Autoinjectors

Pen Injectors

Wearable Injectors

By Usability

Disposable

Reusable

By Application

Cancer

Autoimmune Disorders

Hormonal Disorders

Pain Management

Other Applications

Regions and Countries Covered

Middle East

UAE, Saudi Arabia, Bahrain, Oman, Kuwait, Qatar, Turkiye

Market leaders and key company profiles

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd.

AptarGroup Inc

Pfizer Inc

NuGen Medical Devices Inc

West Pharmaceutical Services

SHL Medical

YPSOMED

Get more information on this report

Middle East Self Injection Device Market Report Coverage and Deliverables:

The "Middle East Self Injection Device Market Size and Forecast (2026–2033)" report provides a detailed analysis of the market covering below areas:

Middle East Self Injection Device Market size and forecast at regional and country levels for all market segments covered under the scope

Middle East Self Injection Device Market trends, as well as drivers, restraints, and opportunities

Middle East Self Injection Device Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Middle East Self Injection Device Market

Detailed company profiles, including SWOT analysis

Middle East Self Injection Device Market Geographic Insights:

The geographical scope of the Middle East Self Injection Device Market report is divided into the UAE, Saudi Arabia, Bahrain, Oman, Kuwait, Qatar, and Turkiye. Turkiye held the largest share in 2025.

Country-specific dynamics within the Middle East self-injection device market reveal distinct healthcare system structures, regulatory environments, and adoption patterns that shape competitive strategies. Turkey stands at the forefront, combining a sophisticated healthcare infrastructure, progressive regulatory framework, and strong domestic manufacturing capabilities. The Turkish Medicines and Medical Devices Agency (TİTCK) has adopted streamlined device approval pathways that align with European standards, enabling faster commercialization of autoinjectors, prefilled pens, and connected delivery systems. Turkey's robust public and private insurance landscape further supports uptake, particularly for chronic disease therapies where self-injection devices reduce reliance on clinical administration.

In addition, Turkey's growing medtech manufacturing base positions it as both an adopter and exporter of advanced delivery formats within the wider Middle East. Saudi Arabia follows closely, where the SFDA has accelerated approvals for a range of self-injection platforms, particularly in diabetes and autoimmune therapy segments, supported by strong public health investments and clinician engagement initiatives that emphasize patient education. The UAE demonstrates high adoption of digital-enabled self-injection technologies, with health authorities in Dubai and Abu Dhabi actively promoting telehealth strategies that integrate device data for improved continuity of care.

Other GCC countries, including Qatar, Kuwait, and Bahrain, benefit from comprehensive public funding schemes and clinician outreach programs that increase access to advanced delivery systems. However, uptake is often most pronounced in urban centers. Egypt represents a growing market in North Africa, with expanding private healthcare services and increasing availability of ergonomic injectors in metropolitan pharmacies, though rural access and reimbursement limitations temper adoption rates. Across the region, physician advocacy, localized educational initiatives, and alignment with national chronic disease strategies remain critical to driving sustained device adoption, highlighting the need for tailored market approaches based on country-specific healthcare dynamics.

Get more information on this report

Middle East Self Injection Device Market Research Report Guidance:

The report includes qualitative and quantitative data in the Middle East Self Injection Device Market across product, usability, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Middle East Self Injection Device Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Middle East Self Injection Device Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Middle East Self Injection Device Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Middle East Self Injection Device Market segments by product, usability, application, and geography across the UAE, Saudi Arabia, Bahrain, Oman, Kuwait, Qatar, and Turkiye. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Middle East Self Injection Device Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Middle East Self Injection Device Market News and Key Development:

The Middle East Self Injection Device Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Middle East self injection device market are:

In October 2024, Sanofi and Saudi Arabia's Public Investment Fund (PIF), NUPCO, and Sudair Pharmaceuticals announced plans to localize production of insulin pens—specifically the SoloStar delivery device—in Saudi Arabia, marking a major move toward regional manufacture of advanced self-injection delivery tools. Under the agreement, technology transfer and assembly expertise for these pens will be developed locally at Sudair's plant. This initiative supports Vision 2030 objectives to build domestic pharmaceutical capabilities and secure reliable access to insulin pen devices. It is a strategic step that expands self-injection device availability in the Gulf beyond imports.

In February 2026, Insulet launched its Omnipod 5 Automated Insulin Delivery (AID) System and accompanying Omnipod Discover data platform across key Middle Eastern markets, including Saudi Arabia, Kuwait, Qatar, and the UAE, marking one of the first introductions of this wearable, tubeless insulin delivery technology in the region. The Omnipod 5 integrates with continuous glucose monitors such as Abbott FreeStyle Libre 2 Plus and Dexcom G7 to automate insulin delivery and improve glycemic control. Its commercial availability represents a shift toward more advanced self-administration capabilities that reduce reliance on multiple daily injections. The data platform further enhances care by giving patients and clinicians actionable insights from glucose and insulin delivery data.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Middle East Self Injection Device Market?

The Middle East Self Injection Device Market is valued at US$ 482.3 Million in 2025, it is projected to reach US$ 609.2 Million by 2033.

What is the CAGR for Middle East Self Injection Device Market by (2026 - 2033)?

As per our report Middle East Self Injection Device Market, the market size is valued at US$ 482.3 Million in 2025, projecting it to reach US$ 609.2 Million by 2033. This translates to a CAGR of approximately 3.0% during the forecast period.

What segments are covered in this report?

The Middle East Self Injection Device Market report typically cover these key segments-

Application (Cancer, Autoimmune Disorders, Hormonal Disorders, Pain Management, Other Applications)

What is the historic period, base year, and forecast period taken for Middle East Self Injection Device Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East Self Injection Device Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Middle East Self Injection Device Market?

The Middle East Self Injection Device Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Gerresheimer AG

Becton Dickinson and Co

Owen Mumford Ltd.

AptarGroup Inc

Pfizer Inc

NuGen Medical Devices Inc

West Pharmaceutical Services

SHL Medical

YPSOMED

Who should buy this report?

The Middle East Self Injection Device Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Middle East Self Injection Device Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Middle East Self Injection Device Market

Get Free Sample For Middle East Self Injection Device Market