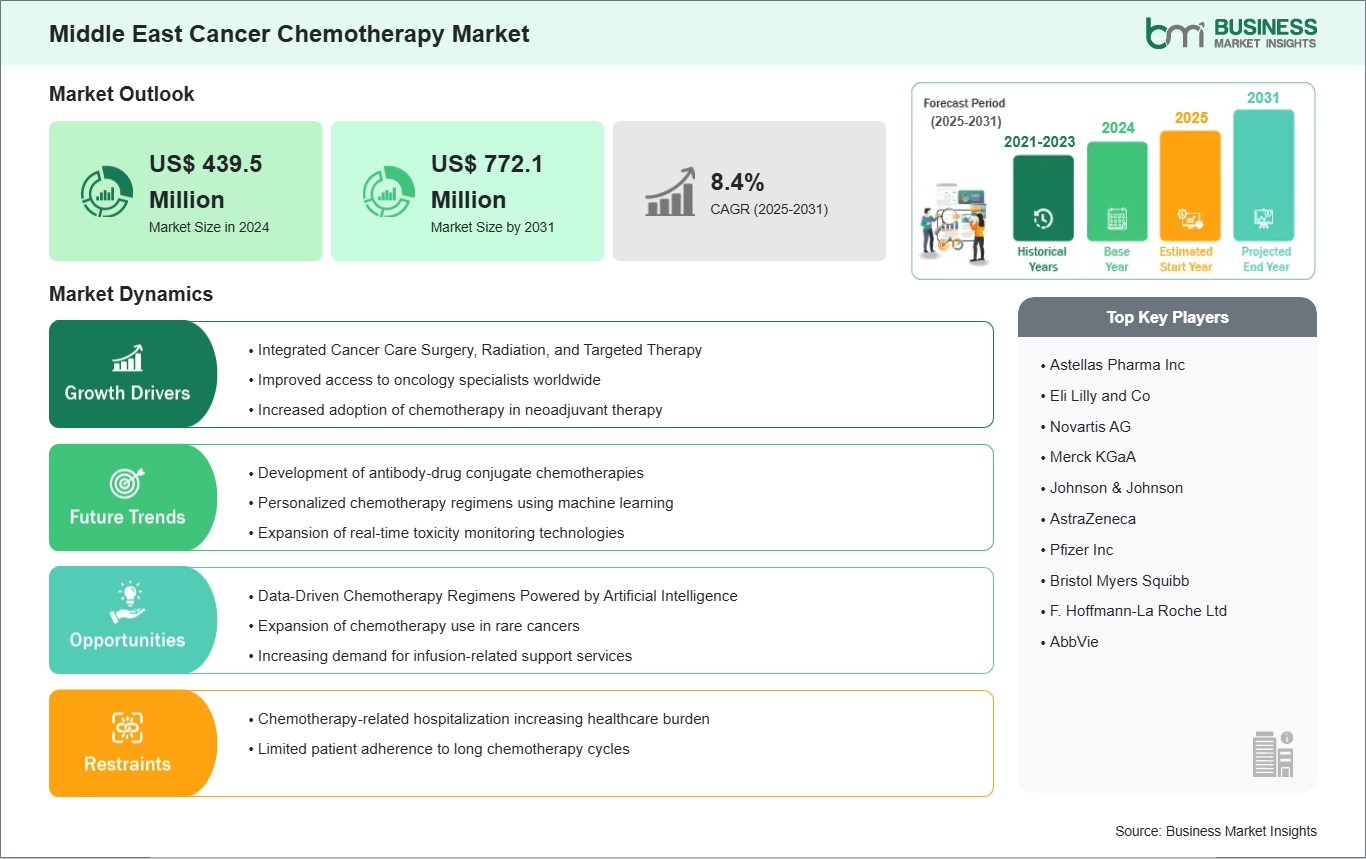

Integrated Cancer Care Surgery, Radiation, and Targeted Therapy

One of the primary drivers of chemotherapy demand in the Middle East is the increasing use of multimodal oncology treatment strategies. Chemotherapy is extensively used as neoadjuvant therapy to shrink tumors before surgery and as adjuvant therapy to eliminate residual disease afterward, particularly in breast, colorectal, and lung cancers. Chemotherapy also enhances the efficacy of radiation therapy by acting as a radiosensitizer, improving tumor cell susceptibility to radiotherapy in locoregionally advanced cancers.

In parallel, chemotherapy remains central to combination regimens with targeted therapies and immunotherapy agents. These combinations are reflected in updated clinical guidelines. They are widely adopted in oncology centers across the region, particularly for advanced and metastatic disease, where integrated treatment approaches enhance survival and quality of life.

The expansion of oncology research networks, clinical trial participation, and international collaborations further supports integration of chemotherapy with targeted and immune-based therapies. This convergence of modalities expands therapeutic options, strengthens clinical relevance, and drives broader chemotherapy utilization across Middle Eastern oncology practice.

Data-Driven Chemotherapy Regimens Powered by Artificial Intelligence

Artificial Intelligence (AI) contributes to improved chemotherapy personalization and dosing optimization in the Middle East. AI platforms can analyze complex datasets including genomics, radiologic imaging, biomarkers, and electronic health records to identify optimal drug combinations, anticipate toxicity profiles, and tailor dosing schedules to individual patient characteristics.

Major healthcare hubs in the Middle East such as those in Saudi Arabia, the UAE, and emerging oncology centers in Egypt are investing in digital health infrastructure and AI-driven decision support tools. These systems enable clinicians to refine chemotherapy regimens, forecast treatment responses, and adapt protocols based on real-time data. Importantly, AI also supports clinical trial design by identifying appropriate patient subgroups and predictive biomarkers.

Ongoing partnerships between region-focused technology firms and healthcare institutions, as well as the introduction of locally developed AI solutions for early cancer detection, lay the foundation for broader adoption of precision chemotherapy strategies. As AI becomes more integrated within oncology workflows, it is expected to improve therapeutic outcomes, reduce adverse effects, and enhance healthcare resource allocation.