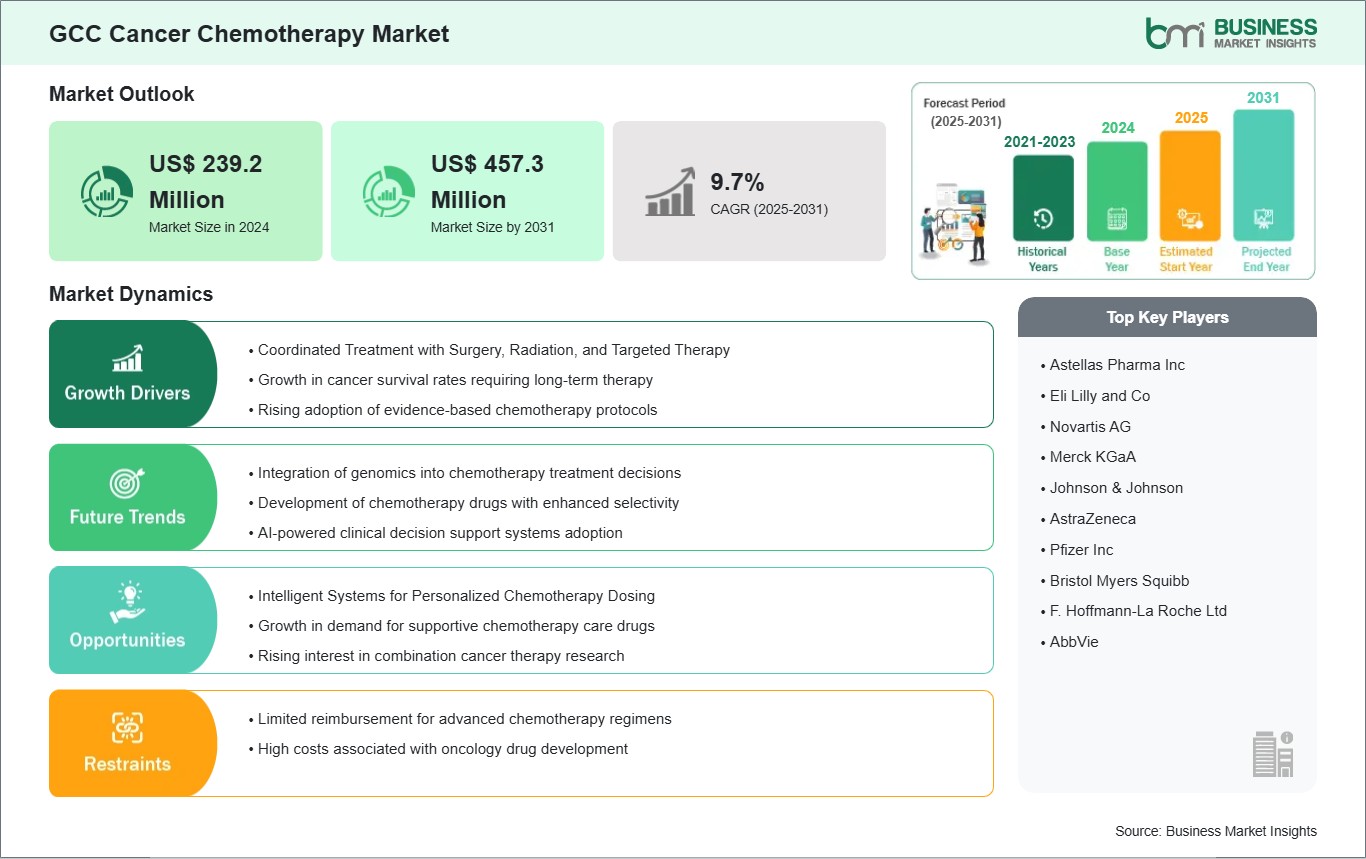

The GCC Cancer Chemotherapy Market size is expected to reach US$ 457.3 million by 2031 from US$ 239.2 million in 2024. The market is estimated to record a CAGR of 9.7% from 2025 to 2031.

Executive Summary and GCC Cancer Chemotherapy Market Analysis:

The cancer chemotherapy market in the GCC is experiencing significant growth, driven by the rising incidence of cancer globally and substantial healthcare investments by member states. Saudi Arabia represents the largest share within the GCC due to its extensive healthcare restructuring under Vision 2030, which includes significant funding for specialized cancer centers, precision diagnostics, and advanced oncology care delivery. The UAE, particularly through major tertiary care hospitals and oncology networks in Dubai and Abu Dhabi, exhibits high chemotherapy utilization supported by advanced infrastructure and international partnerships. Qatar's National Cancer Program and Kuwait's healthcare reforms have strengthened oncology services, expanding patient access to chemotherapy regimens through public and private insurance models.

Chemotherapy services in the GCC include inpatient and outpatient administrations, with hospital pharmacies dominating as the primary distribution channel for injectable and intravenous drugs. Retail pharmacy networks and emerging online platforms are increasingly important for oral cytotoxic agents and supportive care formulations, reflecting patient preference for convenience and continuity of care. The GCC also shows rising adoption of personalized treatment approaches, where chemotherapy is integrated with targeted therapies and immunotherapies in multidisciplinary care protocols.

Regional initiatives emphasize building clinical research expertise, digital health integration, and training oncology professionals to enhance treatment outcomes. Strategic collaborations with international cancer centers and pharmaceutical companies are expanding the availability of innovative chemotherapy combinations and companion diagnostics, improving treatment precision and patient quality of life. Overall, the market reflects strengthening demand, evolving clinical practices, and expanding healthcare delivery systems that are expected to sustain growth through 2031.

GCC Cancer Chemotherapy Market - Strategic Insights:

Get more information on this report

GCC Cancer Chemotherapy Market Segmentation Analysis:

Key segments that contributed to the derivation of the GCC Cancer Chemotherapy market analysis are therapy type, indication, and distribution channel.

By therapy type, the cancer chemotherapy market is segmented into alkylating agents, antimetabolites, anti-tumor antibiotics, topoisomerase inhibitors, mitotic inhibitors, and others. The alkylating agents segment dominated the market in 2024.

Based on indication, the cancer chemotherapy market is categorized into blood cancer, lung cancer, breast cancer, colorectum cancer, prostate cancer, stomach cancer, cervical cancer, liver and intrahepatic bile duct cancer, thyroid cancer, and other indications. The lung cancer segment dominated the market in 2024.

By distribution channel, the market is classified into hospital pharmacies, retail pharmacies, and online stores. The hospital pharmacies segment dominated the market in 2024.

GCC Cancer Chemotherapy Market Drivers and Opportunities:

Coordinated Treatment with Surgery, Radiation, and Targeted Therapy

A key driver for the GCC cancer chemotherapy market is the increasing adoption of multimodal treatment strategies that combine chemotherapy with surgery, radiation therapy, and targeted agents. Chemotherapy is widely used in neoadjuvant settings to reduce tumor size before surgical resection and in adjuvant contexts to eliminate residual disease and reduce recurrence risk, especially in breast, colorectal, and prostate cancers. The region is also witnessing growing integration of chemotherapy with radiation therapy, where cytotoxic agents serve as radiosensitizers to enhance tumor response in locally advanced lung, head and neck, and gastrointestinal cancers.

In parallel, chemotherapy continues to be a foundational element within combination regimens involving targeted therapies and immunotherapies. These protocols are increasingly supported by clinical guidelines and evidence from global oncology practice, enhancing treatment outcomes and broadening therapeutic options for patients with advanced and metastatic disease. Particularly in high‑income GCC states such as Saudi Arabia and the UAE, multidisciplinary cancer care models emphasize integrated treatment pathways that leverage chemotherapy alongside novel biologics and precision agents to improve survival rates and quality of life.

The expansion of oncology centers, clinical trial networks, and partnerships with international research institutions further supports the adoption of combination approaches, creating opportunities for increased chemotherapy usage across multiple cancer indications. Continued focus on integrated care strengthens the clinical relevance of chemotherapy even as the region embraces precision oncology and targeted treatments.

Intelligent Systems for Personalized Chemotherapy Dosing

Artificial Intelligence (AI) enables personalized regimens and optimized dosing strategies. AI tools can synthesize multi‑dimensional patient data including genomic profiles, clinical histories, imaging biomarkers, and real‑world treatment outcomes to support individualized treatment plans that improve effectiveness and minimize toxicity. In the GCC, investment in digital health infrastructure, electronic health records, and cloud-based clinical decision support systems is increasing, particularly in Saudi Arabia and the UAE, creating an environment conducive to AI integration.

AI‑enabled predictive models assist oncologists in selecting the most appropriate chemotherapy agents, scheduling optimal dosing, forecasting potential side effects, and adapting regimens based on early response signals. These capabilities enhance precision oncology and improve resource utilization within busy oncology services. Moreover, AI accelerates clinical research by enabling smarter patient stratification and real-time analytics in regional cancer care programs. Partnerships between AI firms and local health authorities along with rising adoption of AI-assisted diagnostics and treatment planning tools are expected to bolster personalized chemotherapy approaches across the GCC.

GCC Cancer Chemotherapy Market Size and Share Analysis:

The GCC Cancer Chemotherapy market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report further examines subsegments categorized by therapy type, indication, and distribution channel, offering insights into their contribution to overall market performance.

By therapy type, the alkylating agents subsegment dominated the market in 2024, driven by their established clinical utility across multiple cancer types.

Based on indication, the lung cancer subsegment dominated the market in 2024, driven by infection prevention initiatives and demand for biocompatible devices in GCC healthcare systems.

By distribution channel, the hospital pharmacies subsegment dominated the market in 2024, driven by centralized administration of intravenous and infusion regimens.

GCC Cancer Chemotherapy Market Report Highlights:

Report Attribute

Details

Market size in 2024

US$ 239.2 Million

Market Size by 2031

US$ 457.3 Million

CAGR (2025 - 2031)

9.7%

Historical Data

2021-2023

Forecast period

2025-2031

Segments Covered

By Therapy Type

Alkylating Agents

Antimetabolites

Anti-Tumor Antibiotics

Topoisomerase Inhibitors

Mitotic Inhibitors

Other Therapy Type

By Indication

Blood Cancer

Lung Cancer

Breast Cancer

Colorectum Cancer

Prostate Cancer

Stomach Cancer

Cervical Cancer

Liver and Intrahepatic Bile Duct Cancer

Thyroid Cancer

Other Indications

By End User

Hospital Pharmacies

Retail Pharmacies

Online Stores

Regions and Countries Covered

GCC

United Arab Emirates, Bahrain, Saudi Arabia, Oman, Qatar, and Kuwait

Market leaders and key company profiles

Astellas Pharma Inc

Eli Lilly and Co

Novartis AG

Merck KGaA

Johnson & Johnson

AstraZeneca

Pfizer Inc

Bristol Myers Squibb

F. Hoffmann-La Roche Ltd

AbbVie

Get more information on this report

GCC Cancer Chemotherapy Market Report Coverage and Deliverables:

The "GCC Cancer Chemotherapy Market Size and Forecast (202–2031)" report provides a detailed analysis of the market covering below areas:

GCC Cancer Chemotherapy market size and forecast at regional and country levels for all the key market segments covered under the scope

GCC Cancer Chemotherapy market trends, as well as market dynamics such as drivers, restraints, and key opportunities

GCC Cancer Chemotherapy market analysis covering key market trends, regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the GCC Cancer Chemotherapy market

Detailed company profiles, including SWOT analysis

GCC Cancer Chemotherapy Market Geographic Insights:

The geographical scope of the GCC Cancer Chemotherapy market report is divided into the UAE, Bahrain, Saudi Arabia, Oman, Qatar, and Kuwait. Saudi Arabia held the largest share in 2024.

Saudi Arabia is the largest market in the GCC, driven by extensive healthcare reforms under Vision 2030, which focus on modernizing oncology services, expanding cancer centers, and integrating precision medicine. Public and private sector collaborations, exemplified by initiatives such as the Oncology Center of Excellence under Johns Hopkins Aramco Healthcare, aim to elevate treatment quality, enhance early detection programs, and support clinical research networks. The UAE exhibits strong demand for chemotherapy across major metropolitan oncology centers, particularly in Dubai and Abu Dhabi, where advanced healthcare infrastructure, international medical partnerships, and investment in oncology technologies support high‑quality cancer care. Retail pharmacy expansions and outpatient infusion services further broaden chemotherapy access.

Qatar has launched comprehensive national cancer programs that prioritize access to systemic therapies, including chemotherapy, while enhancing screening and support services. Kuwait is bolstering oncology care via new cancer treatment protocols and infrastructure investments to improve patient outcomes. In Oman and Bahrain, government health systems continue to develop oncology treatment pathways with increasing chemotherapy adoption, although overall volumes remain smaller compared with Saudi Arabia and the UAE. Across the GCC, urban centers show higher uptake and access to advanced chemotherapy regimens, while strategies to expand care into peripheral regions are ongoing. Public payer systems and employer-based insurance schemes significantly influence chemotherapy uptake and affordability, shaping regional market dynamics.

Get more information on this report

GCC Cancer Chemotherapy Market Research Report Guidance:

The report includes qualitative and quantitative data in the GCC Cancer Chemotherapy market across therapy type, indication, distribution channel, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the GCC Cancer Chemotherapy market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the GCC Cancer Chemotherapy market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the GCC Cancer Chemotherapy market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 11 cover GCC Cancer Chemotherapy market segments by therapy type, indication, distribution channel, and geography across the UAE, Bahrain, Saudi Arabia, Oman, Qatar, and Kuwait. They cover the market revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the GCC Cancer Chemotherapy market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

GCC Cancer Chemotherapy Market News and Key Development:

The GCC Cancer Chemotherapy market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the GCC cancer chemotherapy market are:

In January 2026, Saudi Arabia's regulatory authority granted conditional approval for Anktiva a novel cancer therapy for advanced lung and bladder cancers marking the Kingdom as the first country to approve this treatment and signaling regional openness to innovative oncology agents that may be integrated with chemotherapy protocols.

In February 2025, Saudi Arabia announced major healthcare expansions, including an Oncology Center of Excellence, which will focus on breast, colorectal, and prostate cancers using advanced diagnostic and precision treatment technologies, strengthening regional oncology infrastructure.

Key Sources Referred:

World Health Organization (WHO)

World Heart Federation (WHF)

Organisation for Economic Cooperation and Development (OECD)

The World Bank Group

Worldometer

The Lancet

International Bar Association

International Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - GCC Cancer Chemotherapy Market

Astellas Pharma Inc

Eli Lilly and Co

Novartis AG

Merck KGaA

Johnson & Johnson

AstraZeneca

Pfizer Inc

Bristol Myers Squibb

F. Hoffmann-La Roche Ltd

AbbVie

Frequently Asked Questions

How big is the GCC Cancer Chemotherapy Market?

The GCC Cancer Chemotherapy Market is valued at US$ 239.2 Million in 2024, it is projected to reach US$ 457.3 Million by 2031.

What is the CAGR for GCC Cancer Chemotherapy Market by (2025 - 2031)?

As per our report GCC Cancer Chemotherapy Market, the market size is valued at US$ 239.2 Million in 2024, projecting it to reach US$ 457.3 Million by 2031. This translates to a CAGR of approximately 9.7% during the forecast period.

What segments are covered in this report?

The GCC Cancer Chemotherapy Market report typically cover these key segments-

Therapy Type (Alkylating Agents, Antimetabolites, Anti-Tumor Antibiotics, Topoisomerase Inhibitors, Mitotic Inhibitors, Other Therapy Type)

Indication (Blood Cancer, Lung Cancer, Breast Cancer, Colorectum Cancer, Prostate Cancer, Stomach Cancer, Cervical Cancer, Liver and Intrahepatic Bile Duct Cancer, Thyroid Cancer, Other Indications)

End User (Hospital Pharmacies, Retail Pharmacies, Online Stores)

What is the historic period, base year, and forecast period taken for GCC Cancer Chemotherapy Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the GCC Cancer Chemotherapy Market report:

Historic Period : 2021-2023

Base Year : 2024

Forecast Period : 2025-2031

Who are the major players in GCC Cancer Chemotherapy Market?

The GCC Cancer Chemotherapy Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Astellas Pharma Inc

Eli Lilly and Co

Novartis AG

Merck KGaA

Johnson & Johnson

AstraZeneca

Pfizer Inc

Bristol Myers Squibb

F. Hoffmann-La Roche Ltd

AbbVie

Who should buy this report?

The GCC Cancer Chemotherapy Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the GCC Cancer Chemotherapy Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For GCC Cancer Chemotherapy Market

Get Free Sample For GCC Cancer Chemotherapy Market