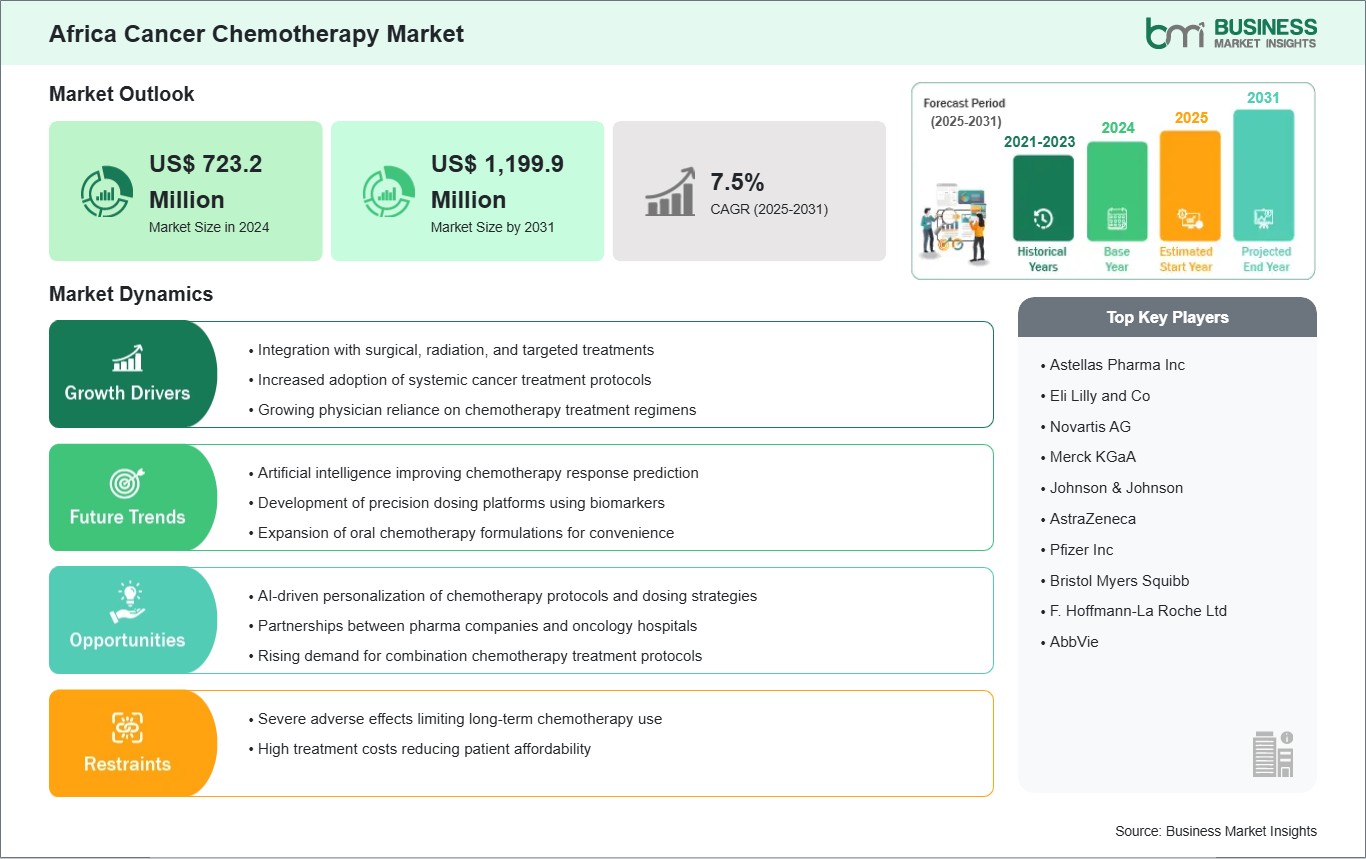

Integration with surgical, radiation, and targeted treatments

Chemotherapeutic agents are increasingly used in combination with surgery, radiation, and targeted therapies. Historically, chemotherapy was often deployed as a standalone systemic treatment. Today, multimodal treatment strategies have become the clinical standard for several solid and hematologic cancers, significantly enhancing patient outcomes and driving demand for chemotherapeutic drugs. The combination of chemotherapeutic drugs with surgery plays a crucial role in cancer treatment. Chemotherapy is frequently administered in the neoadjuvant setting (before surgery) to reduce tumor size, improve resectability, and address microscopic disease. It is also used as adjuvant therapy (after surgery) to eliminate residual cancer cells and reduce the risk of recurrence. As surgical interventions become more precise and increasingly adopted across a wide range of cancer types, the continued reliance on perioperative chemotherapy supports sustained market uptake.

Integration of chemotherapeutic drugs with radiation therapy strengthens therapeutic efficacy. Chemotherapy can act as a radiosensitizer, making tumor cells more susceptible to radiation-induced damage. This synergistic approach is especially common in head & neck, cervical, and lung cancers. The growing global adoption of combined chemoradiation protocols in standard treatment guidelines boosts chemotherapy utilization. The trend toward combining chemotherapy with targeted therapies and immunotherapies expands treatment options for resistant or advanced cancers. Chemotherapy can enhance the effectiveness of targeted agents by killing rapidly proliferating cells, disrupting tumor microenvironments, and overcoming resistance mechanisms. The rise of precision oncology has encouraged clinical trials and approvals for combination regimens, which in turn drives broader chemotherapy use across diverse patient populations. These combination strategies optimize treatment outcomes and extend the clinical relevance of chemotherapeutic drugs.

AI-driven personalization of chemotherapy protocols and dosing strategies

Artificial intelligence (AI) is leveraged to develop personalized chemotherapy regimens and optimize dosing strategies. Traditional chemotherapy has often followed standardized protocols based on cancer type and stage, but patient responses vary widely due to genetic, molecular, and physiological differences. AI offers the potential to transform this landscape by enabling precision‐tailored treatment plans, reducing toxicity, and improving therapeutic outcomes. AI algorithms can analyze large, complex datasets including genomic profiles, tumor biomarkers, imaging results, electronic health records, and real-time patient responses to identify patterns that human clinicians might miss. By integrating these multidimensional data points, AI can help determine the most effective drug combinations, optimal dosing schedules, and treatment durations for individual patients. This personalization aims to maximize efficacy while minimizing adverse effects, which is particularly valuable in chemotherapy, where toxicity can limit dose intensity and patient quality of life.

Furthermore, AI-driven predictive modeling can anticipate how patients will metabolize and respond to specific chemotherapy agents, enabling dynamic dose adjustments throughout the treatment course. Machine learning systems can continuously refine predictions as new data becomes available, supporting adaptive therapy that evolves with the patient's condition. AI-powered clinical decision support tools help oncologists navigate expanding therapeutic options and evidence, enhancing treatment precision and confidence. As healthcare systems increasingly adopt digital infrastructure and real-world data accumulates, AI's role in chemotherapy personalization promises more effective, efficient, and patient-centric cancer care.