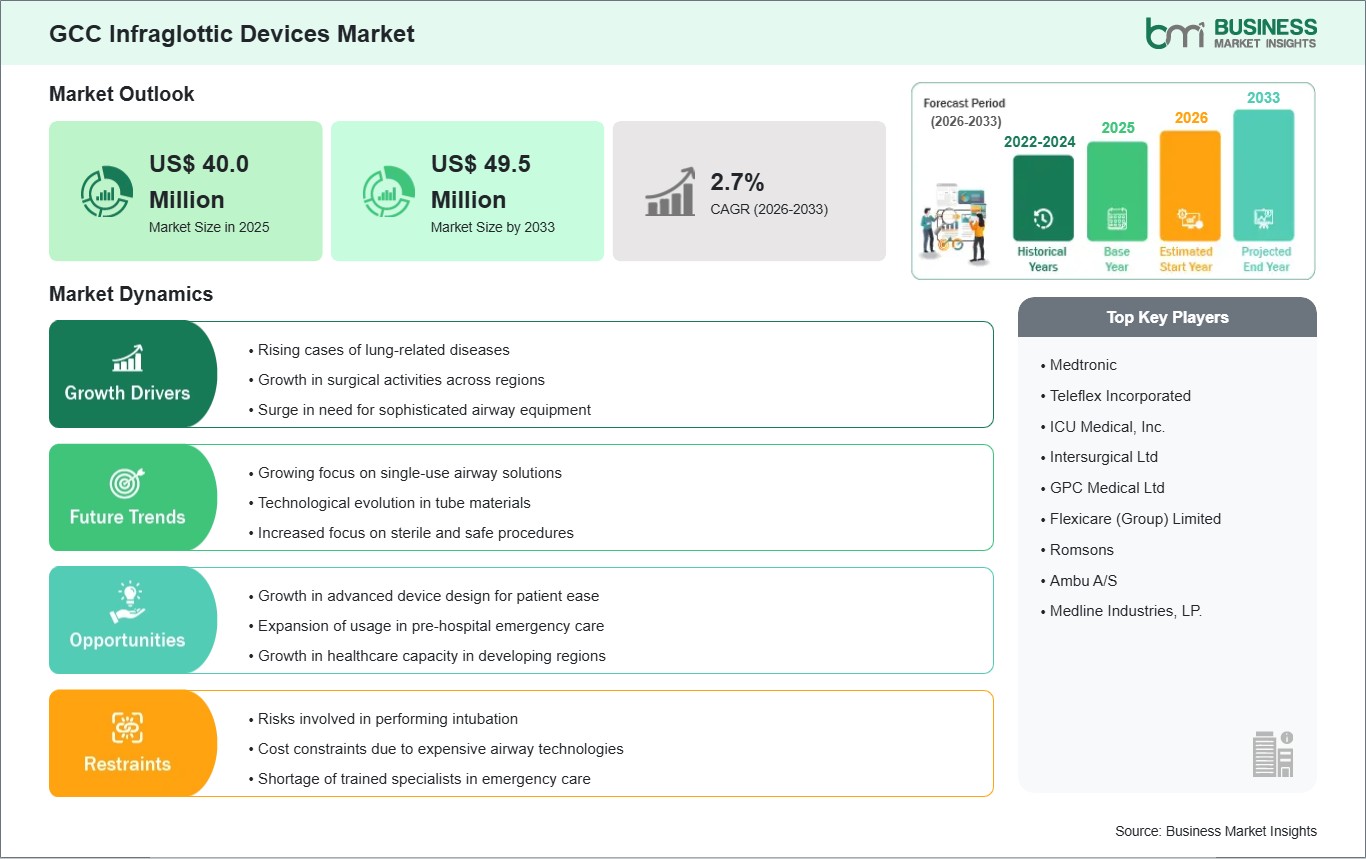

The GCC Infraglottic Devices market size is expected to reach US$ 49.5 million by 2033 from US$ 40.0 million in 2025. The market is estimated to record a CAGR of 2.7% from 2026 to 2033.

Executive Summary and GCC Infraglottic Devices Market Analysis:

The market for infraglottic devices in the GCC is experiencing significant growth owing to increased spending on healthcare infrastructure development and improved focus on providing advanced critical care. Infraglottic devices include tracheostomy tubes and endotracheal tubes and are used for airway management in surgeries and other critical procedures. There has been a marked increase in the incidence of chronic respiratory diseases like asthma and COPD in GCC countries, contributing to the rising demand for infraglottic devices. Besides, there have been several programs initiated by governments to modernize their healthcare systems, which also involve increasing ICU capacity and improving surgical facilities.

Despite the growth potential, the market faces certain challenges. High costs associated with advanced devices can limit adoption in smaller healthcare facilities, and there is a shortage of trained professionals for complex airway management procedures in some areas. However, the presence of international manufacturers, combined with increased awareness of patient safety and infection control practices, has encouraged adoption of disposable and technologically enhanced devices. The ongoing focus on establishing specialized trauma centers and enhancing emergency medical services in urban hubs is expected to maintain steady demand for infraglottic devices across the GCC in the coming years.

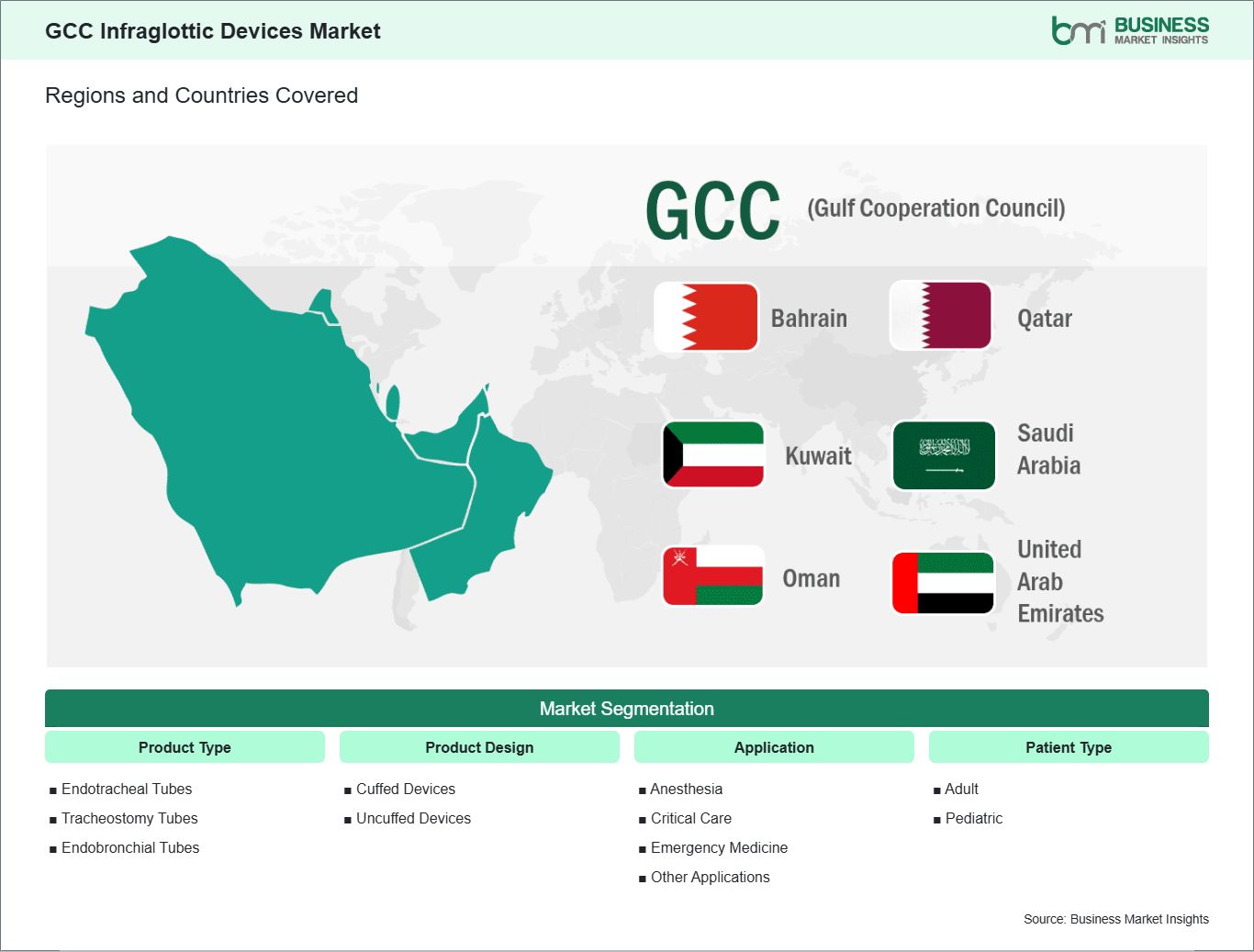

Key segments that contributed to the derivation of the North America infraglottic devices market analysis are product type, product design, application, patient type, and end user.

By product type, the infraglottic devices market is segmented into endotracheal tubes, tracheostomy tubes, and endobronchial tubes. The endotracheal tubes segment dominated the market in 2025.

Among product design, the infraglottic devices market is segmented into cuffed devices and uncuffed devices. The cuffed devices segment dominated the market in 2025.

Based on application, the infraglottic devices market is segmented into anesthesia, critical care, emergency medicine, and other applications. The anesthesia segment dominated the market in 2025.

In terms of patient type, the infraglottic devices market is segmented into adult and pediatric. The adult segment dominated the market in 2025.

By end user, the infraglottic devices market is segmented into hospitals, ambulatory surgical centers, emergency medical services, and other end users. The hospitals segment dominated the market in 2025.

GCC Infraglottic Devices Market Drivers and Opportunities:

Rising Cases of Lung-Related Diseases

The GCC countries, which include Saudi Arabia, the UAE, Qatar, Kuwait, Bahrain, and Oman, are witnessing a surge in incidences of lung disorders. The high incidence of smoking, desert pollution, and pollution caused by urban settings are some of the main reasons behind such respiratory problems as asthma and COPD among others. Besides, there has been an increase in viral respiratory infections and pneumonia, adding another challenge to the healthcare system in the form of more patients in need of ventilators. Hospitals have started relying heavily on devices like endotracheal and tracheostomy tubes for adequate airway management.

Healthcare awareness and screening programs are improving in the GCC, leading to earlier identification of respiratory disorders. This has increased hospital admissions for both planned interventions and emergency treatments, emphasizing the need for reliable airway solutions. The combination of chronic respiratory diseases, acute infections, and growing patient admissions is steadily boosting the demand for infraglottic devices across the region. Hospitals are focusing on efficient airway management to reduce complications and improve patient outcomes. As respiratory health challenges continue to rise, the GCC market for infraglottic devices is expected to grow steadily, supported by increased healthcare capacity and better access to specialized care.

Growth in Advanced Device Design for Patient Ease

The GCC region presents strong opportunities for infraglottic devices with advanced designs that improve patient comfort and procedural efficiency. Healthcare facilities in the region prioritize patient safety and convenience, driving demand for devices that are easier to use, less invasive, and more adaptable to different clinical situations. Innovative endotracheal and tracheostomy tubes with softer materials, enhanced flexibility, and improved sealing mechanisms are increasingly being adopted to reduce patient discomfort and procedural complications. These devices are particularly valuable in intensive care units, emergency departments, and surgical settings where quick and reliable airway management is critical.

Moreover, GCC countries are investing heavily in modernizing healthcare infrastructure and integrating advanced medical technologies. Manufacturers are introducing devices suitable for both high-volume hospitals and smaller clinics, including portable airway solutions that support home and emergency care. Training programs for healthcare professionals are also expanding, ensuring that advanced devices can be used effectively. As hospitals and clinics continue to focus on enhancing patient experience and reducing procedural risks, the adoption of these innovative airway devices is expected to rise steadily. This creates a significant opportunity for market players to introduce next-generation infraglottic devices across the GCC, supporting better patient outcomes and more efficient respiratory care.

GCC Infraglottic Devices Market Size and Share Analysis:

The GCC infraglottic devices market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within product type, product design, application, patient type, and end user, highlighting their respective contributions to overall market performance.

By product type, the endotracheal tubes subsegment dominated the market in 2025 due to their widespread use in airway management during surgeries, critical care, and emergency settings, offering reliable ventilation support and ease of insertion across diverse clinical scenarios.

Among product design, the cuffed devices subsegment dominated the market in 2025 due to their ability to provide effective airway sealing, prevent aspiration, and enable controlled ventilation, making them highly preferred in intensive care and surgical procedures requiring precise airway management.

Based on application, the anesthesia subsegment dominated the market in 2025 due to the high volume of surgical procedures requiring airway management, consistent use of endotracheal tubes during general anesthesia, and increasing demand for safe and controlled ventilation in operating rooms.

In terms of patient type, the adult subsegment dominated the market in 2025 due to higher incidence of chronic respiratory diseases, greater number of surgical procedures, and increased hospitalization rates requiring airway management and ventilatory support in adult populations.

By end user, the hospitals subsegment dominated the market in 2025 due to availability of advanced infrastructure, high patient inflow, presence of intensive care units, and continuous requirement for airway management devices during surgeries and emergency treatments.

GCC Infraglottic Devices Market Report Coverage and Deliverables:

The "GCC Infraglottic Devices Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

GCC Infraglottic Devices market size and forecast at regional and country levels for all market segments covered under the scope

GCC Infraglottic Devices market trends, as well as drivers, restraints, and opportunities

GCC Infraglottic Devices market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the GCC Infraglottic Devices market

Detailed company profiles, including SWOT analysis

The geographical scope of the GCC Infraglottic Devices market report is divided into: Saudi Arabia, the United Arab Emirates (UAE), Qatar, Kuwait, Bahrain, and Oman. Saudi Arabia held the largest share in 2025.

Saudi Arabia dominates the GCC infraglottic devices market due to its well-funded healthcare system, extensive hospital network, and strong focus on modern medical technologies. Hospitals and tertiary care centers across major cities are equipped with advanced ICU and surgical facilities, where infraglottic devices are routinely used for anesthesia, emergency care, and critical interventions. Rising surgical volumes, coupled with a higher prevalence of respiratory disorders, drive consistent demand for these devices throughout the country.

The nation also benefits from government-led initiatives aimed at expanding emergency medical services and establishing specialized trauma centers, which further increase the utilization of airway management devices. The presence of leading international and regional manufacturers ensures access to high-quality and innovative solutions. Challenges include the high cost of sophisticated devices and the need for specialized training for healthcare professionals. Nevertheless, Saudi Arabia’s ongoing investments in hospital modernization, focus on patient safety, and adoption of advanced airway management techniques reinforce its leading position in the GCC infraglottic devices market.

Get more information on this report

GCC Infraglottic Devices Market Research Report Guidance:

The report includes qualitative and quantitative data in the GCC Infraglottic Devices market across product type, product design, application, patient type, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the GCC Infraglottic Devices market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the GCC Infraglottic Devices market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the GCC Infraglottic Devices market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover GCC Infraglottic Devices market segments by product type, product design, application, patient type, end user, and geography across Saudi Arabia, the UAE, Qatar, Kuwait, Bahrain, and Oman. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the GCC Infraglottic Devices market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

GCC Infraglottic Devices Market News and Key Development:

The GCC Infraglottic Devices market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the GCC Infraglottic Devices market are:

In January 2025, Ambu A/S announced that it launched its new Ambu® SureSight™ Connect video laryngoscopy solution, strengthening its comprehensive airway management offering designed to support intubation and visualization workflows in operating rooms and ICUs; this product’s launch extends to global markets including EMEA where GCC clinicians can access it.

In February 2025, Teleflex Incorporated reported its full‑year 2024 financial results noting continued growth in its EMEA segment—highlighting sustained revenue and operational activity in markets that include the GCC region for its anesthesia and respiratory care products.

Key Sources Referred:

The World BankWorld Health Organization (WHO)Center for Disease Control and Prevention (CDC)American Thoracic SocietyEuropean Respiratory Society (ERS)American Society of Anesthesiologists (ASA)Society of Critical Care MedicineInternational Anesthesia Research Society (IARS)World Federation of Societies of Anaesthesiologists (WFSA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Frequently Asked Questions

How big is the GCC Infraglottic Devices Market?

The GCC Infraglottic Devices Market is valued at US$ 40.0 Million in 2025, it is projected to reach US$ 49.5 Million by 2033.

What is the CAGR for GCC Infraglottic Devices Market by (2026 - 2033)?

As per our report GCC Infraglottic Devices Market, the market size is valued at US$ 40.0 Million in 2025, projecting it to reach US$ 49.5 Million by 2033. This translates to a CAGR of approximately 2.7% during the forecast period.

What segments are covered in this report?

The GCC Infraglottic Devices Market report typically cover these key segments-

Product Type (Endotracheal Tubes, Tracheostomy Tubes, Endobronchial Tubes)

Product Design (Cuffed Devices, Uncuffed Devices)

Application (Anesthesia, Critical Care, Emergency Medicine, Other Applications)

Patient Type (Adult, Pediatric)

What is the historic period, base year, and forecast period taken for GCC Infraglottic Devices Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the GCC Infraglottic Devices Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in GCC Infraglottic Devices Market?

The GCC Infraglottic Devices Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic

Teleflex Incorporated

ICU Medical, Inc.

Intersurgical Ltd

GPC Medical Ltd

Flexicare (Group) Limited

Romsons

Ambu A/S

Medline Industries, LP.

Who should buy this report?

The GCC Infraglottic Devices Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the GCC Infraglottic Devices Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For GCC Infraglottic Devices Market

Get Free Sample For GCC Infraglottic Devices Market