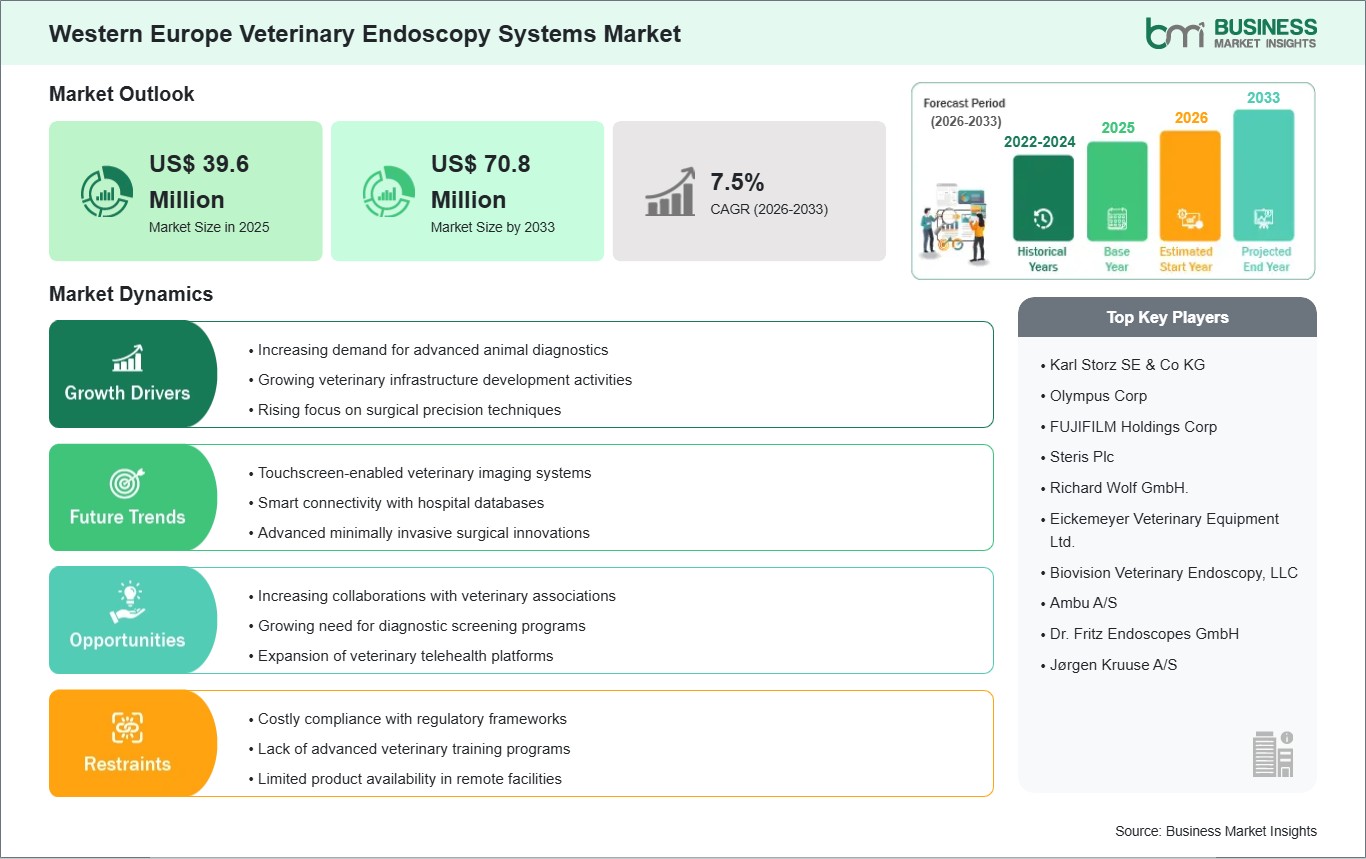

The Western Europe veterinary endoscopy systems market size is expected to reach US$ 70.8 million by 2033 from US$ 39.6 million in 2025. The market is estimated to record a CAGR of 7.5% from 2026 to 2033.

Executive Summary and Western Europe Veterinary Endoscopy Systems Market Analysis:

The Western Europe veterinary endoscopy systems market represents one of the most mature and clinically advanced veterinary technology ecosystems globally, defined by high procedural standardization, strong regulatory oversight, and deep integration of minimally invasive surgical techniques into routine veterinary practice. In terms of structure, the area features an organized approach to veterinary care, diagnostic accuracy, compliance with animal welfare regulations, and efficiency in operations, which are determining the uptake of innovations. A major source of demand is the prominence of pet animal health care, especially in densely populated urban economies, where pets are regarded as family members. As a consequence, there is a heavy investment in advanced veterinary diagnostic solutions, and endoscope technology finds application in gastroenterology, respiratory medicine, urology, and minimal invasive surgery. High penetration of pet insurance schemes contributes to the availability of advanced treatment options, allowing for veterinary practices to purchase modern equipment at reduced costs to consumers. A characteristic trait of the market is the organization of veterinary services through large corporate entities or multisite clinics. As a result, endoscopy systems are deployed as part of integrated surgical and diagnostic suites rather than standalone equipment. Technological advancement is a central pillar of market evolution. Continuous improvements in high-definition imaging, flexible endoscope design, digital integration, and workflow automation are driving frequent system upgrades. Veterinary practices are adopting connected diagnostic ecosystems, where imaging data is integrated into electronic medical records and shared across specialist networks for collaborative diagnosis. Despite its maturity, the market continues to evolve through innovation-led differentiation rather than volume expansion. Demand is influenced by system performance, service reliability, training support, and software capabilities rather than basic equipment availability. The Western Europe veterinary endoscopy systems market is a highly sophisticated, innovation-driven environment where growth is shaped by clinical specialization, digital transformation, and continuous refinement of veterinary surgical and diagnostic practices.

Western Europe Veterinary Endoscopy Systems Market - Strategic Insights:

Get more information on this report

Western Europe Veterinary Endoscopy Systems Market Segmentation Analysis:

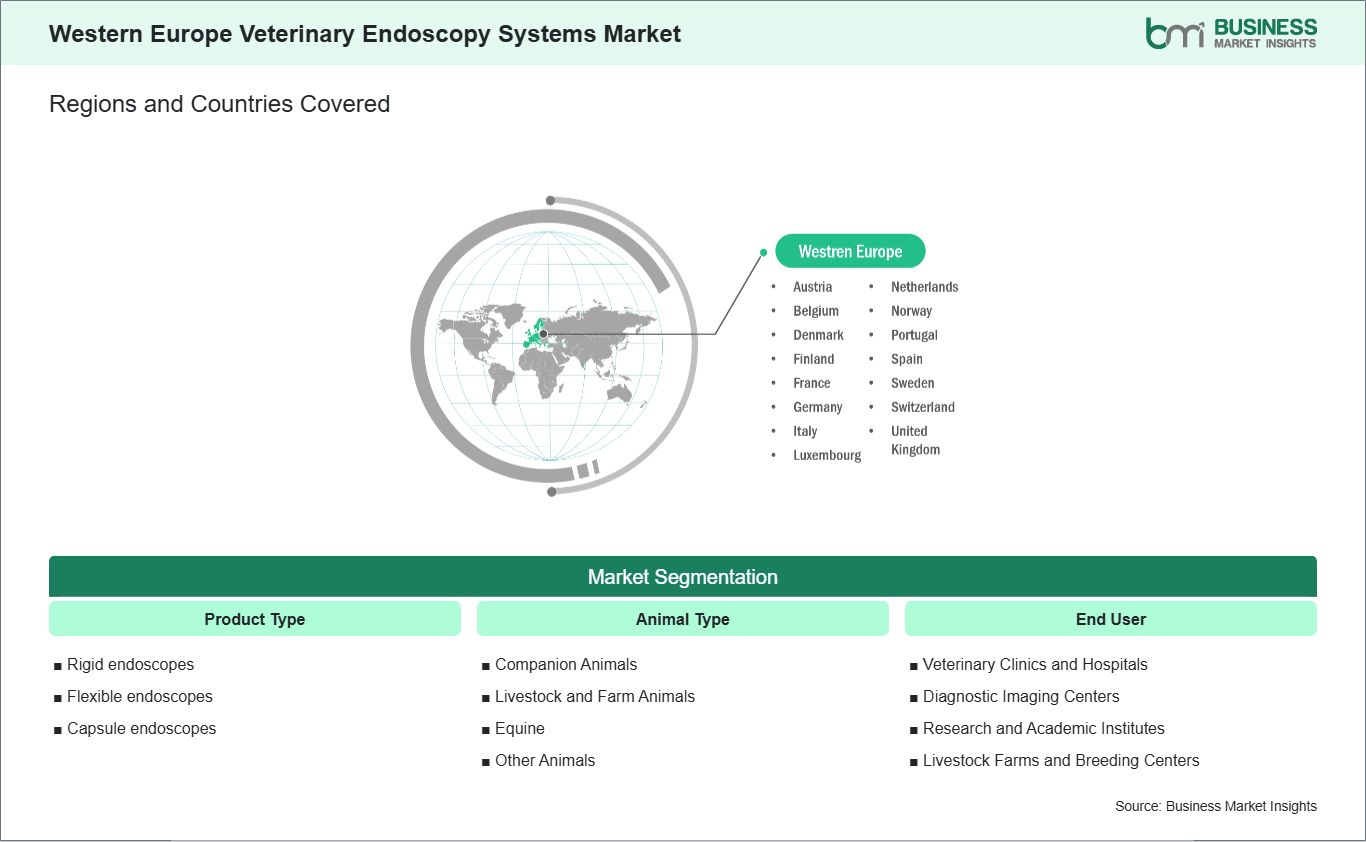

Key segments that contributed to the derivation of the Western Europe veterinary endoscopy systems market analysis are product type, animal type, and end user.

By product type, the veterinary endoscopy systems market is segmented into rigid endoscopes, flexible endoscopes, and capsule endoscopes. The rigid endoscopes segment dominated the market in 2025.

Based on animal type, the veterinary endoscopy systems market is categorized into companion animals, livestock & farm animals, equine, and others. The companion animals segment dominated the market in 2025.

In terms of end user, the veterinary endoscopy systems market is categorized into veterinary clinics & hospitals, diagnostic imaging centers, research & academic institutes, and livestock farms & breeding centers. The veterinary clinics and hospitals segment dominated the market in 2025.

Western Europe Veterinary Endoscopy Systems Market Drivers and Opportunities:

Supportive policies for animal healthcare systems

The Western Europe veterinary endoscopy systems market is supported by strong policy frameworks that prioritize animal health, welfare, and standardized clinical care across countries such as Germany, France, the UK, the Netherlands, Belgium, and Switzerland. The veterinary endoscopy procedures are enhanced in such countries since there are existing regulations in the veterinary sector focusing on preventive health measures, diagnosis, and the adoption of modern technology in clinical procedures. Such an environment facilitates veterinary endoscopy as it conforms to the policy objectives of minimizing invasive surgeries in animal treatment.

The veterinary health care systems of Germany, France, and the Netherlands are integrated with well-established veterinary service delivery frameworks that promote the application of sophisticated diagnostic tools. The regulatory pressures to ensure adequate animal welfare practices have compelled veterinary clinics to rely on minimally invasive techniques such as endoscopy. There is a high level of animal welfare regulation in the UK, which promotes early diagnosis and scientific treatment methods, resulting in increased adoption of precise veterinary tools.

In all of Western Europe, additional European Union veterinary policies add more value to this market through harmonization of the training process and competent care delivery based on a higher level of welfare treatment. Veterinarians must exhibit excellent clinical skills, which inadvertently help in implementing sophisticated diagnosis equipment within their practice. This expectation is helping in generating consistent demand for veterinary endoscopy systems in urban as well as semi-urban healthcare facilities within the region.

Increasing need for advanced surgical training

The increasing need for advanced surgical training among veterinary professionals is also driving the Western Europe veterinary endoscopy systems market. Modern surgical procedures have become quite complex, especially those involving minimal invasive surgery and internal diagnostic methods. Veterinary endoscopy equipment plays a key role in modern veterinary training, allowing veterinarians to learn and practice precise diagnostic and treatment techniques. With the increasing importance of professional training, the use of endoscopic equipment is becoming widespread.

In nations such as the UK, Germany, and France, veterinary educational facilities and hospitals are integrating training programs in surgical procedures involving the use of endoscopy and laparoscopic operations. Specialists in veterinary medicine have to undergo extensive training after their graduation, which includes the use of sophisticated diagnostic equipment. The structured training programs allow veterinarians to be adequately prepared to conduct complex surgical procedures with the aid of advanced endoscopic devices, leading to increased usage of such equipment in practice.

There is increased cooperation between various veterinary schools, specialty colleges, and clinical institutions in developing expertise in sophisticated diagnostic tools. Countries such as the Netherlands and Belgium have been especially instrumental in incorporating learning programs that promote practical training of endoscopic techniques. With increasing specialization in veterinary medicine, there will be an increasing need for surgical training.

Western Europe Veterinary Endoscopy Systems Market Size and Share Analysis:

The Western Europe veterinary endoscopy systems market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product type, animal type, and end user, offering insights into their contribution to overall market performance.

By product type, the rigid endoscopes segment dominated the market in 2025, driven by high adoption of minimally invasive veterinary surgeries and strong preference for precision-based diagnostic and therapeutic procedures in advanced clinical settings.

Based on animal type, the companion animals subsegment dominated the market in 2025, driven by high pet ownership rates, strong animal welfare standards, and significant spending on advanced veterinary healthcare for dogs and cats.

In terms of end user, the veterinary clinics and hospitals subsegment dominated the market in 2025, driven by mature veterinary healthcare infrastructure, high procedural volumes, and widespread integration of advanced endoscopy systems in routine and specialty care.

Western Europe Veterinary Endoscopy Systems Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 39.6 Million

Market Size by 2033

US$ 70.8 Million

CAGR (2026 - 2033)

7.5%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product Type

Rigid endoscopes

Flexible endoscopes

Capsule endoscopes

By Animal Type

Companion Animals

Livestock and Farm Animals

Equine

Other Animals

By End User

Veterinary Clinics and Hospitals

Diagnostic Imaging Centers

Research and Academic Institutes

Livestock Farms and Breeding Centers

Regions and Countries Covered

Western Europe

Belgium, the Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, the United Kingdom, Denmark, Portugal, Norway, Finland

Market leaders and key company profiles

Karl Storz SE & Co KG

Olympus Corp

FUJIFILM Holdings Corp

Steris Plc

Richard Wolf GmbH.

Eickemeyer Veterinary Equipment Ltd.

Biovision Veterinary Endoscopy, LLC

Ambu A/S

Dr. Fritz Endoscopes GmbH

Jørgen Kruuse A/S

Get more information on this report

Western Europe Veterinary Endoscopy Systems Market Report Coverage and Deliverables:

The "Western Europe Veterinary Endoscopy Systems Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Market concentration, heat map analysis, prominent players, and recent developments for the Market

Detailed company profiles, including SWOT analysis

Western Europe Veterinary Endoscopy Systems Market Geographic Insights:

The geographical scope of the Western Europe veterinary endoscopy systems market report is divided into Belgium, the Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, the UK, Denmark, Portugal, Norway, and Finland. Germany held the largest share in 2025.

Country-level dynamics in the Western Europe veterinary endoscopy systems market reflect an advanced and well-integrated veterinary healthcare structure, with variations driven by clinical specialization, service consolidation, and technology adoption intensity. Germany stands as a leading market, supported by a strong veterinary research ecosystem and highly specialized clinical networks. Veterinary endoscopy is used in referral hospitals and university-affiliated institutions, particularly in complex diagnostic and surgical procedures requiring high precision. The UK demonstrates a highly consolidated veterinary services landscape, where large corporate veterinary groups dominate service delivery. This structure supports standardized adoption of advanced diagnostic technologies, including endoscopy systems, across multi-location clinic networks, particularly for companion animal healthcare. France reflects a dual-structured veterinary market where urban companion animal care drives advanced technology adoption, while rural regions maintain strong livestock-focused veterinary services. Endoscopy systems are used in both segments, with growing emphasis on preventive diagnostics and reproductive health management. Italy exhibits a fragmented veterinary market dominated by independent practitioners. Adoption of endoscopy systems is selective and often influenced by clinic specialization, client demographics, and regional demand variations, particularly in urban centers. Spain shows steady growth in veterinary endoscopy adoption, driven by the modernization of veterinary clinics and increasing demand for advanced companion animal care services in metropolitan regions. The Netherlands represents a highly innovation-oriented veterinary market with strong integration of digital veterinary systems and early adoption of advanced diagnostic technologies. Clinics often participate in pilot programs for endoscopy solutions, accelerating technology diffusion. Belgium demonstrates a balanced veterinary ecosystem with strong livestock and companion animal segments, supporting consistent adoption of endoscopy systems across both clinical and agricultural applications. Western Europe is characterized by high clinical maturity and technology penetration, with Germany and the UK leading in scale and specialization, while other countries contribute through structured, innovation-driven adoption pathways.

Get more information on this report

Western Europe Veterinary Endoscopy Systems Market Research Report Guidance:

The report includes qualitative and quantitative data in the Western Europe veterinary endoscopy systems market across product type, animal type, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Western Europe Veterinary Endoscopy Systems Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Western Europe Veterinary Endoscopy Systems Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Western Europe Veterinary Endoscopy Systems Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Western Europe veterinary endoscopy systems market segments by product type, animal type, end user and geography across Belgium, the Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, the United Kingdom, Denmark, Portugal, Norway, and Finland. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Western Europe Veterinary Endoscopy Systems Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Western Europe Veterinary Endoscopy Systems Market News and Key Development:

The Western Europe veterinary endoscopy systems market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Western Europe veterinary endoscopy systems market are:

In September 2022, Olympus Corporation announced the launch of its VISERA ELITE III surgical visualization platform in Europe, a next-generation endoscopy system offering 4K, 3D, and infrared imaging capabilities used across minimally invasive surgical applications, including veterinary laparoscopic and endoscopic procedures in European clinics and universities.

In October 2024, Olympus Europa SE & Co. KG announced CE approval for three cloud-based AI endoscopy devices (CADDIE, CADU, SMARTIBD), advancing its intelligent endoscopy ecosystem in Europe and supporting enhanced imaging workflows used in diagnostic and minimally invasive endoscopy, including veterinary-adjacent applications.

Key Sources Referred:

American College of Veterinary Radiology (ACVR)World Small Animal Veterinary Association (WSAVA)British Veterinary Association (BVA)International Veterinary Radiology Association (IVRA)American Veterinary Medical Association (AVMA)ASEANan College of Veterinary Diagnostic Imaging (ECVDI)World Organisation for Animal Health (WOAH / OIE)Veterinary Imaging & Radiation Oncology Society (VIROS)

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Western Europe Veterinary Endoscopy Systems Market?

The Western Europe Veterinary Endoscopy Systems Market is valued at US$ 39.6 Million in 2025, it is projected to reach US$ 70.8 Million by 2033.

What is the CAGR for Western Europe Veterinary Endoscopy Systems Market by (2026 - 2033)?

As per our report Western Europe Veterinary Endoscopy Systems Market, the market size is valued at US$ 39.6 Million in 2025, projecting it to reach US$ 70.8 Million by 2033. This translates to a CAGR of approximately 7.5% during the forecast period.

What segments are covered in this report?

The Western Europe Veterinary Endoscopy Systems Market report typically cover these key segments-

Product Type (Rigid endoscopes, Flexible endoscopes, Capsule endoscopes)

Animal Type (Companion Animals, Livestock and Farm Animals, Equine, Other Animals)

End User (Veterinary Clinics and Hospitals, Diagnostic Imaging Centers, Research and Academic Institutes, Livestock Farms and Breeding Centers)

What is the historic period, base year, and forecast period taken for Western Europe Veterinary Endoscopy Systems Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Western Europe Veterinary Endoscopy Systems Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Western Europe Veterinary Endoscopy Systems Market?

The Western Europe Veterinary Endoscopy Systems Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Karl Storz SE & Co KG

Olympus Corp

FUJIFILM Holdings Corp

Steris Plc

Richard Wolf GmbH.

Eickemeyer Veterinary Equipment Ltd.

Biovision Veterinary Endoscopy, LLC

Ambu A/S

Dr. Fritz Endoscopes GmbH

Jørgen Kruuse A/S

Who should buy this report?

The Western Europe Veterinary Endoscopy Systems Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Western Europe Veterinary Endoscopy Systems Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Western Europe Veterinary Endoscopy Systems Market

Get Free Sample For Western Europe Veterinary Endoscopy Systems Market