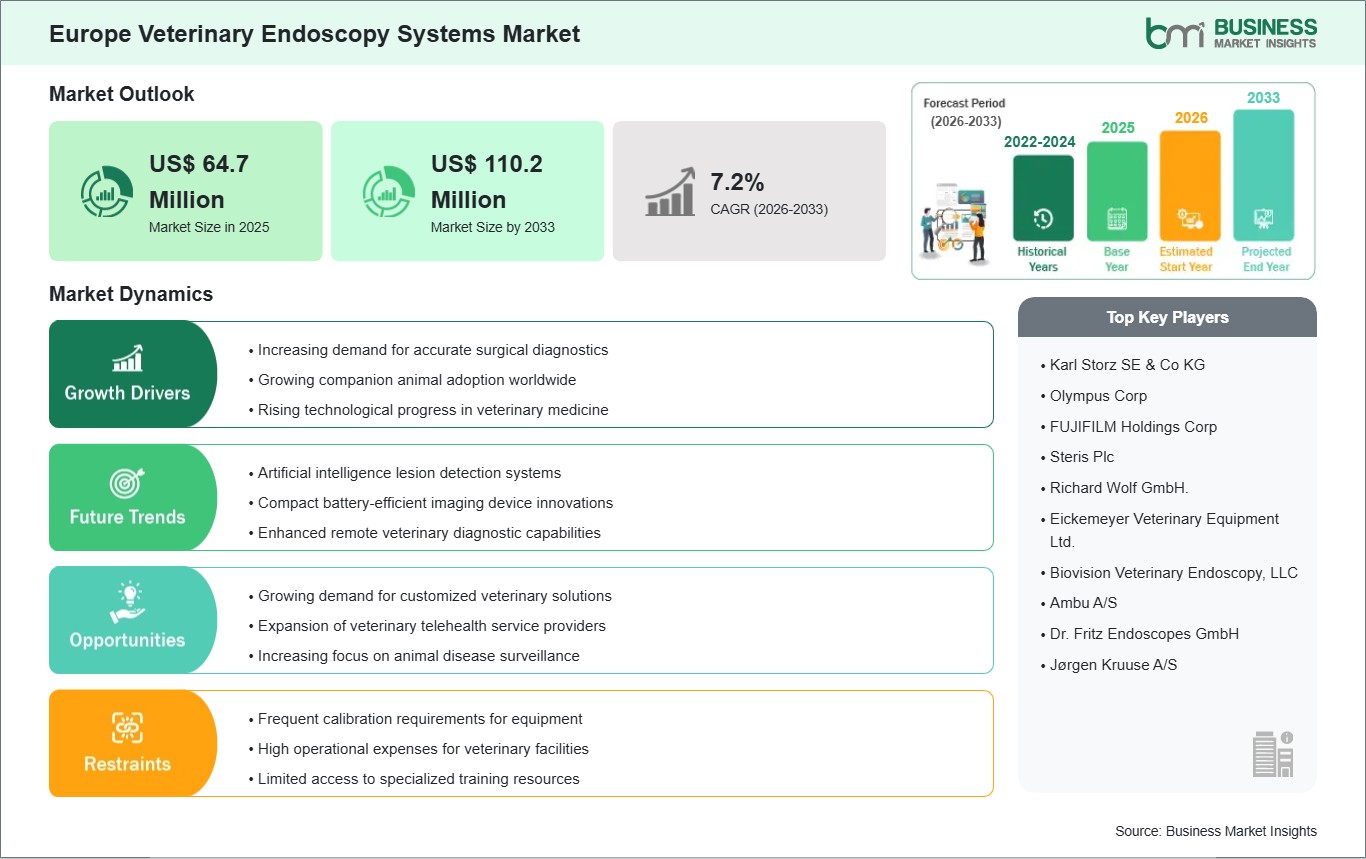

The Europe veterinary endoscopy systems market size is expected to reach US$ 110.2 million by 2033 from US$ 64.7 million in 2025. The market is estimated to record a CAGR of 7.2% from 2026 to 2033.

Executive Summary and Europe Veterinary Endoscopy Systems Market Analysis:

The Europe veterinary endoscopy systems market reflects a highly structured and efficiency-oriented environment where clinical precision and procedural standardization are central to veterinary practice. While in developing markets, the decision is made based on awareness, the European market is predominantly driven by protocols, since endoscopy systems are integrated in the existing diagnostics processes at multi-specialty veterinary hospitals. These are facilitated by robust clinical governance structures and evidence-based veterinary medicine practice. What distinguishes this market from other countries' markets is the specialization that has developed among veterinary practices. Specialty hospitals are increasingly specialized in terms of gastroenterology, pulmonology, and minimally invasive surgery where endoscopy systems are indispensable. This has created a need for specialized equipment that can be used for particular procedural purposes instead of diagnostic devices. In response to this trend, there is an increased emphasis by the manufacturers on product differentiation. The other significant trend is the increased use of evidence-based veterinary medicine. Modern endoscopic equipment can be connected to electronic medical record systems for the purpose of storing images and conducting consultations from afar. This will facilitate teamwork among clinicians and help in providing second opinions when dealing with cross-border cases in Europe. Furthermore, environmental issues are now starting to play a significant role in procurement choices, with clinics now favoring systems that are durable and cost-effective in their lifecycles as well as being less problematic from the point of view of maintenance. Another emerging trend is the rise of veterinary groups and clinic chains as a major buyer, which will impact how vendors approach these buyers. The strategy of bulk buying and the decision-making process itself will put more weight on vendors providing high-quality products as well as adequate training and after-sale services. However, even though the market is well-developed, innovations here are likely to be achieved by improving existing technology through gradual improvements in imaging, ergonomics, and work flow.

Europe Veterinary Endoscopy Systems Market - Strategic Insights:

Get more information on this report

Europe Veterinary Endoscopy Systems Market Segmentation Analysis:

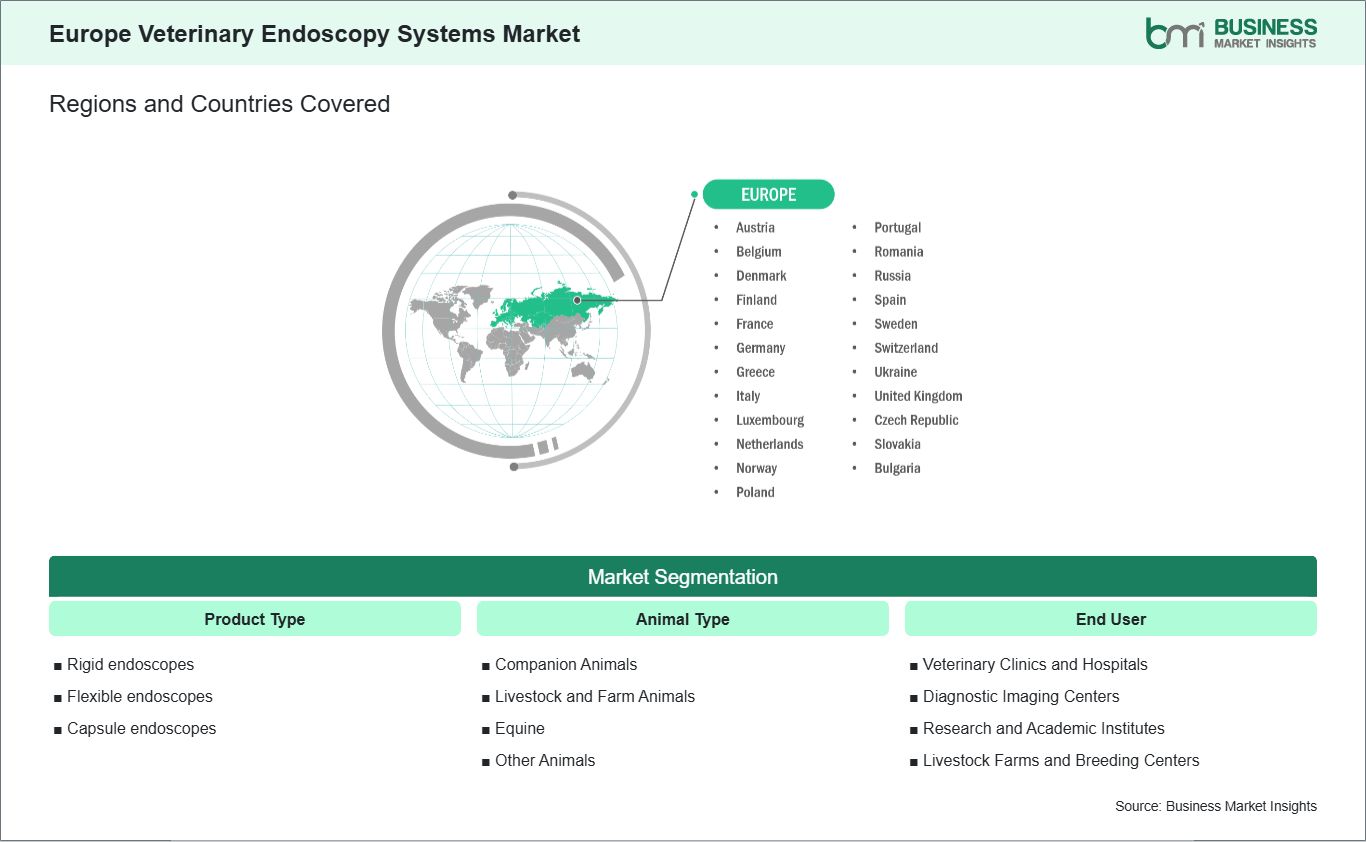

Key segments that contributed to the derivation of the Europe veterinary endoscopy systems market analysis are product type, animal type, and end user.

By product type, the veterinary endoscopy systems market is segmented into rigid endoscopes, flexible endoscopes, capsule endoscopes. The rigid endoscopes segment dominated the market in 2025.

Based on animal type, the veterinary endoscopy systems market is categorized into companion animals, livestock & farm animals, equine, others. The companion animals segment dominated the market in 2025.

In terms of end user, the veterinary endoscopy systems market is categorized veterinary clinics & hospitals, diagnostic imaging centers, research & academic institutes, livestock farms & breeding centers. The veterinary clinics and hospitals segment dominated the market in 2025.

Europe Veterinary Endoscopy Systems Market Drivers and Opportunities:

Demand for precise diagnostic procedures

The Europe veterinary endoscopy systems market is strongly driven by increasing demand for precise and reliable diagnostic procedures across companion and livestock animal care. Veterinary practitioners are now focusing more on early and precise diagnosis, especially with regard to the diagnosis of internal diseases where there is no easy way to detect the disease from outside the body. Through endoscopic systems, veterinarians are able to view inside the bodies of their animal patients and make accurate diagnoses, without having to perform exploratory surgery.

In Western European nations like Germany, France, and the United Kingdom, there is an increasing trend of employing sophisticated diagnostic systems in order to fulfill the rising demands of the pet owners and also for ensuring compliance with animal welfare policies. There is a strong tradition of excellence in the delivery of veterinary services in this area; therefore, minimally invasive and imaging-assisted techniques are highly favored. It can be said that a considerable number of veterinary organizations within Europe make use of advanced endoscopy imaging for diagnosing small animals.

There has been a trend of development that is quite evident in Southern and Northern Europe in terms of developing interest in the provision of specialized diagnostics, be it in urban and semi-urban veterinary clinics. In places like Italy and Nordic countries, there has been the adoption of technology where digital imaging systems have been integrated with the endoscopy system to allow for efficient diagnosis of patients. With the continuous increase in demand for diagnostic procedures in Europe, the demand for endoscopy systems will remain high.

Collaboration with veterinary education institutions

Collaboration with veterinary education institutions plays a crucial role in shaping the Europe veterinary endoscopy systems market by supporting skill development and technology adoption. Endoscopic training is one of the areas where European universities and teaching hospitals are contributing heavily by training veterinarians in modern diagnostic methods. Such organizations play a significant role in the transfer of knowledge, making sure that future veterinarians acquire skills in conducting minimally invasive operations as well as using imaging technologies. Academic engagement promotes use of endoscopy systems.

In nations like Germany, France, and the Netherlands, there exist robust links between schools of veterinary medicine and equipment suppliers and research organizations. Such collaboration helps in the creation and testing of novel diagnostic devices as well as introducing advanced technology in veterinary education. There are numerous veterinary education facilities in Europe that offer training in endoscopy, which promotes standardized procedures and successful procedures.

In addition, the academia is becoming an important player in upgrading veterinary care through providing more advanced techniques in diagnosis as well as increased research activities. The partnership between the universities and the private veterinary clinics can help address the issue of bridging theory and practice. With the increasing number of academic-clinical collaborations, innovations will continue and help increase the adoption of endoscopy systems. It will be one of the important factors that will contribute towards the sustained growth in the market for the foreseeable future.

Europe Veterinary Endoscopy Systems Market Size and Share Analysis:

The Europe veterinary endoscopy systems market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product type, animal type, and end user, offering insights into their contribution to overall market performance.

By product type, the rigid endoscopes segment dominated the market in 2025, driven by widespread adoption of minimally invasive veterinary procedures and strong demand for high-precision, durable instruments across advanced clinical settings.

Based on animal type, the companion animals subsegment dominated the market in 2025, driven by high pet ownership rates, significant spending on animal healthcare, and increasing preference for advanced diagnostic and surgical procedures for dogs and cats.

In terms of end user, the veterinary clinics and hospitals subsegment dominated the market in 2025, driven by well-established veterinary infrastructure, high procedural volumes, and extensive adoption of advanced endoscopic systems for routine and specialized animal care across the region.

Europe Veterinary Endoscopy Systems Market Report Highlights:

Europe Veterinary Endoscopy Systems Market Report Coverage and Deliverables:

The "Europe Veterinary Endoscopy Systems Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Market concentration, heat map analysis, prominent players, and recent developments for the Market

Detailed company profiles, including SWOT analysis

Europe Veterinary Endoscopy Systems Market Geographic Insights:

The geographical scope of the Europe veterinary endoscopy systems market report is divided into Belgium, Austria, Finland, Denmark, Greece, Poland, Romania, Russia, Ukraine, Czech Republic, Slovakia, Bulgaria, Italy, Luxembourg, Germany, Switzerland, France, Netherlands, Norway, Portugal, Spain, Sweden, United Kingdom. Germany held the largest share in 2025.

Country-level insights in the European veterinary endoscopy systems market highlight clear differentiation in adoption drivers, reflecting unique healthcare structures and veterinary practice models across nations. Germany leads the market with a strong foundation in clinical research and veterinary specialization. The country’s veterinary ecosystem is heavily influenced by academic institutions and referral networks, where endoscopy is routinely used in complex case management rather than basic diagnostics, reinforcing demand for high-performance systems. In United Kingdom, the market is shaped by the consolidation of veterinary practices under corporate groups. This has resulted in standardized equipment procurement and increased investment in advanced diagnostic infrastructure across multi-location clinics. Endoscopy systems are widely deployed to ensure consistency in clinical service delivery, particularly in urban and suburban veterinary chains. France presents a distinct dynamic where regulatory oversight and agricultural priorities intersect. While companion animal care drives innovation in urban areas, rural regions emphasize endoscopy use in herd health monitoring and reproductive diagnostics, creating a dual-market structure within the country. In Italy, adoption is influenced by a fragmented veterinary clinic landscape. Independent practitioners dominate the market, leading to selective investment in endoscopy systems based on specialization and client demographics. This creates opportunities for mid-range, adaptable systems that balance performance with cost considerations. Spain is experiencing increased demand driven by tourism-related pet care services and rising standards in veterinary hospitality. Clinics are upgrading diagnostic capabilities, including endoscopy, to cater to international clients and higher service expectations. In Northern Europe, Sweden emphasizes preventive veterinary care, where endoscopy is used as part of early-stage diagnostic protocols rather than reactive treatment. This proactive approach supports steady demand for advanced systems. Lastly, Netherlands showcases strong integration of technology and veterinary education, with clinics often participating in pilot programs for new diagnostic tools. This positions the country as an early adopter market within Europe. Collectively, these countries illustrate a nuanced landscape where adoption is shaped less by access and more by clinical structure, procurement models, and specialization depth.

Get more information on this report

Europe Veterinary Endoscopy Systems Market Research Report Guidance:

The report includes qualitative and quantitative data in the Europe veterinary endoscopy systems market across product type, animal type, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Europe Veterinary Endoscopy Systems Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Europe Veterinary Endoscopy Systems Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Europe Veterinary Endoscopy Systems Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Europe veterinary endoscopy systems market segments by product type, animal type, end user and geography across Belgium, Austria, Finland, Denmark, Greece, Poland, Romania, Russia, Ukraine, Czech Republic, Slovakia, Bulgaria, Italy, Luxembourg, Germany, Switzerland, France, Netherlands, Norway, Portugal, Spain, Sweden, United Kingdom. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Europe Veterinary Endoscopy Systems Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Europe Veterinary Endoscopy Systems Market News and Key Development:

The Europe veterinary endoscopy systems market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Europe veterinary endoscopy systems market are:

In May 2025, Fujifilm announced the launch of its new ELUXEO 800 series endoscopes in Europe, designed to improve maneuverability and access to difficult anatomical areas, supporting advanced clinical applications including veterinary use cases.

In September 2025, Zoetis announced the European rollout of its AI-powered Vetscan OptiCell diagnostic platform across multiple countries including Germany, France, Italy, and Spain, expanding its veterinary diagnostic ecosystem that complements minimally invasive procedures such as endoscopy.

Key Sources Referred:

American College of Veterinary Radiology (ACVR)World Small Animal Veterinary Association (WSAVA)British Veterinary Association (BVA)International Veterinary Radiology Association (IVRA)American Veterinary Medical Association (AVMA)ASEANan College of Veterinary Diagnostic Imaging (ECVDI)World Organisation for Animal Health (WOAH / OIE)Veterinary Imaging & Radiation Oncology Society (VIROS)

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Europe Veterinary Endoscopy Systems Market?

The Europe Veterinary Endoscopy Systems Market is valued at US$ 64.7 Million in 2025, it is projected to reach US$ 110.2 Million by 2033.

What is the CAGR for Europe Veterinary Endoscopy Systems Market by (2026 - 2033)?

As per our report Europe Veterinary Endoscopy Systems Market, the market size is valued at US$ 64.7 Million in 2025, projecting it to reach US$ 110.2 Million by 2033. This translates to a CAGR of approximately 7.2% during the forecast period.

What segments are covered in this report?

The Europe Veterinary Endoscopy Systems Market report typically cover these key segments-

Product Type (Rigid endoscopes, Flexible endoscopes, Capsule endoscopes)

Animal Type (Companion Animals, Livestock and Farm Animals, Equine, Other Animals)

End User (Veterinary Clinics and Hospitals, Diagnostic Imaging Centers, Research and Academic Institutes, Livestock Farms and Breeding Centers)

What is the historic period, base year, and forecast period taken for Europe Veterinary Endoscopy Systems Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Veterinary Endoscopy Systems Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Europe Veterinary Endoscopy Systems Market?

The Europe Veterinary Endoscopy Systems Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Karl Storz SE & Co KG

Olympus Corp

FUJIFILM Holdings Corp

Steris Plc

Richard Wolf GmbH.

Eickemeyer Veterinary Equipment Ltd.

Biovision Veterinary Endoscopy, LLC

Ambu A/S

Dr. Fritz Endoscopes GmbH

Jørgen Kruuse A/S

Who should buy this report?

The Europe Veterinary Endoscopy Systems Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Europe Veterinary Endoscopy Systems Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Europe Veterinary Endoscopy Systems Market

Get Free Sample For Europe Veterinary Endoscopy Systems Market