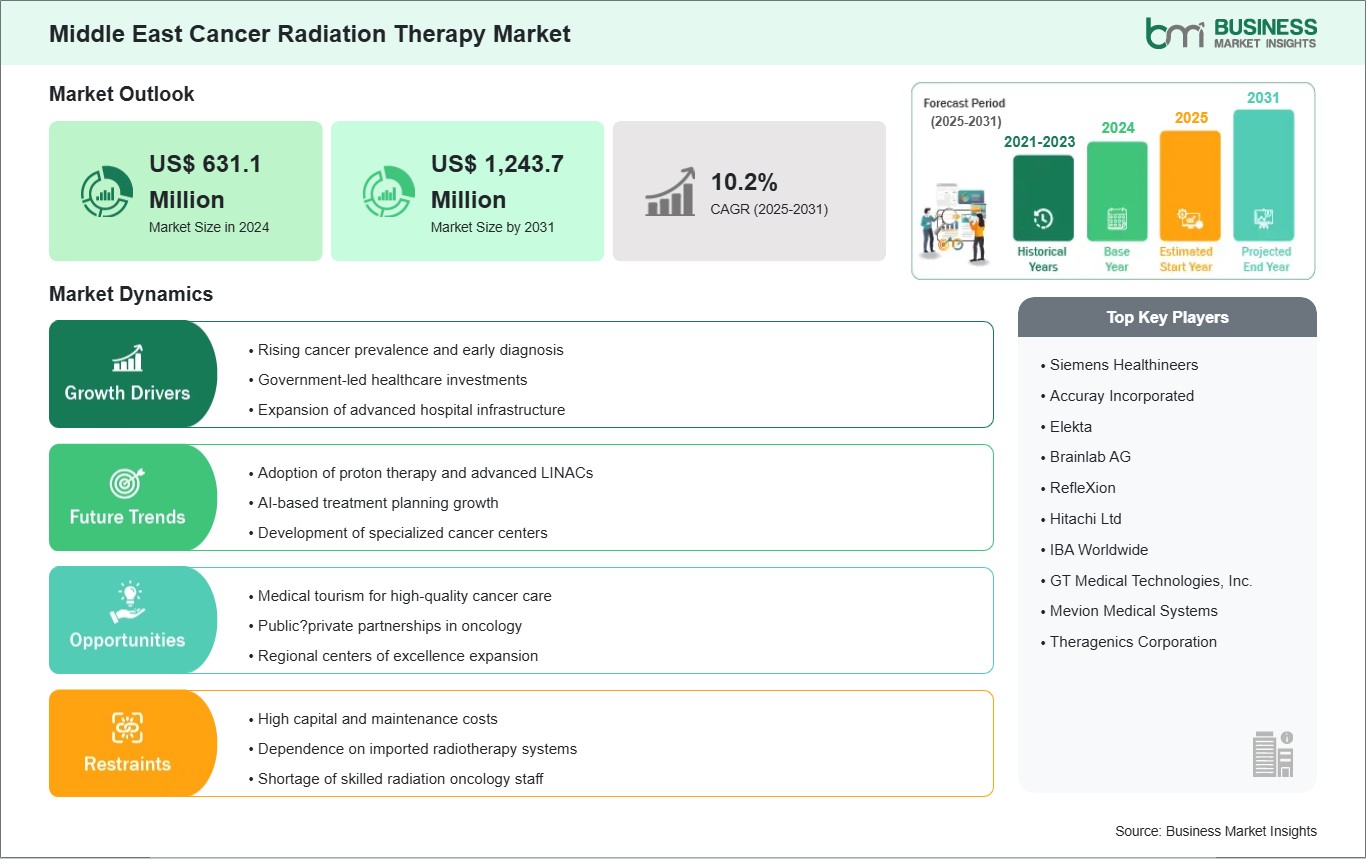

The Middle East cancer radiation therapy market size is expected to reach US$ 1,243.7 million by 2031 from US$ 631.1 million in 2024. The market is estimated to record a CAGR of 10.2% from 2025 to 2031.

Executive Summary and Middle East Cancer Radiation Therapy Market Analysis:

The Middle East cancer radiation therapy market is evolving rapidly as governments prioritize oncology care in response to increasing cancer incidence, especially breast, lung, and colorectal cancers. Urban centers across the region, including Riyadh, Dubai, and Ankara, are investing in high-precision radiotherapy technologies such as intensity-modulated radiotherapy (IMRT), image-guided radiotherapy (IGRT), and stereotactic body radiotherapy (SBRT). The expansion of specialized cancer centers and the integration of advanced imaging systems are driving improved treatment accuracy and patient outcomes. Collaborative programs with international technology providers and professional associations are enhancing workforce skills and knowledge transfer, ensuring that treatment protocols meet global standards. Public-private partnerships are also facilitating the adoption of cutting-edge equipment and digital oncology solutions, contributing to the modernization of cancer treatment across the region.

The adoption of AI-assisted treatment planning, telemedicine networks, and cloud-based radiotherapy workflow management is reinforcing opportunities for market growth in the Middle East. These initiatives allow high-precision radiotherapy capabilities to extend beyond major metropolitan hubs, improving patient access while optimizing operational efficiency. Increasing awareness of early diagnosis, targeted healthcare investments, and regional collaborations are creating a conducive environment for consistent growth. With governments actively integrating cancer care strategies into national health plans, the Middle East market is positioned for continued expansion in both advanced and emerging radiotherapy modalities.

Middle East Cancer Radiation Therapy Market - Strategic Insights:

Get more information on this report

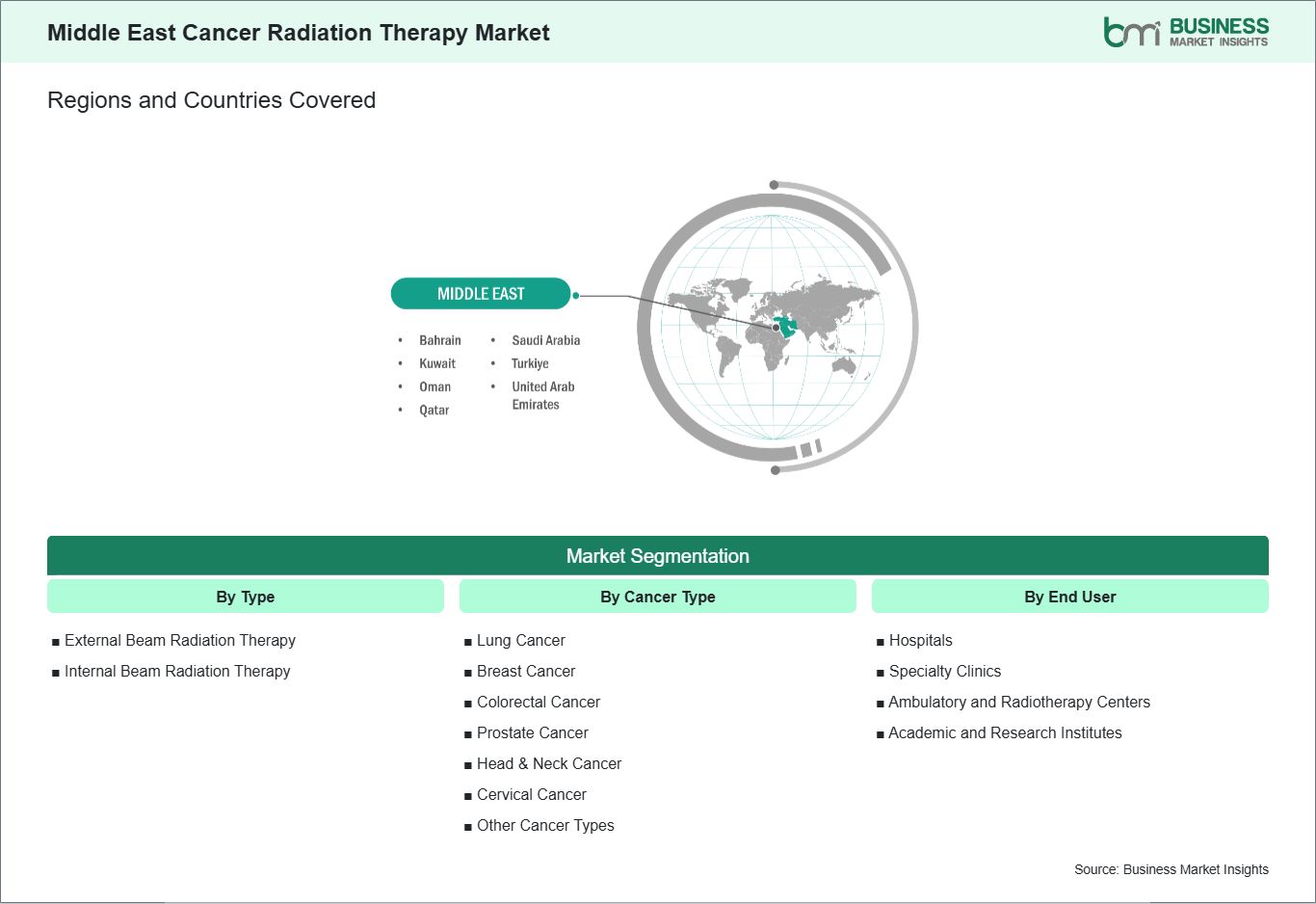

Middle East Cancer Radiation Therapy Market Segmentation Analysis:

Key segments that contributed to the derivation of the Middle East cancer radiation therapy market analysis are type, cancer type, and end user.

By type, the cancer radiation therapy market is segmented into external beam radiation therapy and internal beam radiation therapy. The external beam radiation therapy segment dominated the market in 2024.

Based on cancer type, the cancer radiation therapy market is segmented into lung cancer, breast cancer, colorectal cancer, prostate cancer, head & neck cancer, cervical cancer, and others. The lung cancer segment dominated the market in 2024.

In terms of end user, the cancer radiation therapy market is segmented into hospitals, specialty clinics, ambulatory and radiotherapy centers, and academic and research institutes. The hospitals segment dominated the market in 2024.

Middle East Cancer Radiation Therapy Market Drivers and Opportunities:

Global Trend of Increasing Cancer

Cancer incidence is rising across the Middle East as aging populations, lifestyle shifts, and environmental exposures reshape disease patterns. Gulf countries such as Saudi Arabia, the UAE, and Kuwait report increasing breast and colorectal cancers linked to sedentary lifestyles and metabolic risk, while thyroid cancer remains notably high in young adults. In Levant and North African Middle Eastern states, liver and head‑and‑neck cancers are prominent due to hepatitis prevalence and tobacco use, and late-stage presentations persist in conflict‑affected areas, elevating the role of radiation therapy in multimodal care.

Diagnostic capacity and referral pathways are strengthening in major urban centers, channeling more patients into radiotherapy. External beam radiation therapy is expanding in Riyadh, Abu Dhabi, and Doha, supported by advanced imaging and planning systems for complex cases. Brachytherapy is prioritized for gynecologic cancers in Egypt and Jordan and for prostate cancer in Saudi Arabia, reflecting local disease profiles and the need for cost‑effective, site‑specific dose delivery. These shifts are increasing throughput demands and prompting hospitals to scale linear accelerator fleets and treatment slots.

Public investment and private sector participation are accelerating oncology infrastructure, yet workforce and maintenance gaps remain. National cancer strategies in the Gulf emphasize technology upgrades, quality assurance, and accreditation, while regional collaborations support training and equipment standardization. As screening programs and awareness campaigns expand—particularly for breast and colorectal cancers—more patients are diagnosed at stages where radiation therapy is integral, making rising prevalence a durable driver of the Middle East cancer radiation therapy market.

Surge in Popularity of Custom Medical Care

Personalized oncology is advancing across the Middle East through broader use of molecular diagnostics, precision imaging, and adaptive radiotherapy planning. Leading centers integrate genomic profiling and PET/CT into treatment decisions, enabling dose modulation for radiosensitive subtypes and complex head‑and‑neck cases. Multidisciplinary tumor boards in Saudi Arabia, the UAE, and Egypt are standardizing contouring practices and leveraging MRI for brain and gynecologic tumors, improving consistency and enabling individualized dose‑painting strategies.

Technology upgrades are expanding the personalization toolkit beyond conventional EBRT. IMRT, IGRT, and SBRT are routine in tertiary hospitals, supporting hypofractionated schedules for breast and prostate cancers and stereotactic approaches for oligometastatic disease. Proton therapy access—via regional centers and cross‑border referrals—is growing for pediatric and skull‑base indications, while modern brachytherapy with 3D image guidance tailors dose for cervical cancer, reducing toxicity and enhancing local control. AI‑assisted planning pilots in the Gulf aim to refine dose distributions and reduce inter‑clinician variability.

Policy and reimbursement reforms are aligning incentives with precision care, encouraging adoption of advanced platforms and adaptive workflows. Public and private payers in the Gulf are expanding coverage for image‑guided techniques and stereotactic treatments, while regional training collaborations build expertise in QA, contouring standards, and data‑driven decision‑making. Patients seek shorter courses with fewer side effects, and providers are responding with personalized protocols and integrated care pathways, creating a strong opportunity for vendors and health systems to deliver patient‑specific radiation therapy solutions tailored to the Middle East's clinical and resource landscape.

Middle East Cancer Radiation Therapy Market Size and Share Analysis:

The Middle East cancer radiation therapy market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report further examines subsegments categorized within type, cancer type, and end user, offering insights into their contribution to overall market performance.

By type, the external beam radiation therapy subsegment dominated the market in 2024. Due to its widespread availability, precision targeting, noninvasive nature, and effectiveness in treating diverse cancers, it is the preferred choice across global oncology practices.

Based on cancer type, the lung cancer subsegment dominated the market in 2024. Due to its high incidence, strong link with smoking and pollution, late‑stage diagnoses, and reliance on advanced radiation techniques, it is the most treated cancer type globally.

In terms of end user, the hospitals subsegment dominated the market in 2024. Hospitals dominated the market since they provide comprehensive cancer care, advanced radiation infrastructure, skilled oncologists, and integrated treatment pathways, making them the primary setting for delivering radiation therapy services.

Middle East Cancer Radiation Therapy Market Report Highlights:

Report Attribute

Details

Market size in 2024

US$ 631.1 Million

Market Size by 2031

US$ 1,243.7 Million

CAGR (2025 - 2031)

10.2%

Historical Data

2021-2023

Forecast period

2025-2031

Segments Covered

By Type

External Beam Radiation Therapy

Internal Beam Radiation Therapy

By Cancer Type

Lung Cancer

Breast Cancer

Colorectal Cancer

Prostate Cancer

Head & Neck Cancer

Cervical Cancer

Other Cancer Types

By End User

Hospitals

Specialty Clinics

Ambulatory and Radiotherapy Centers

Academic and Research Institutes

Regions and Countries Covered

Middle East

UAE, Saudi Arabia, Bahrain, Oman, Kuwait, Qatar, Turkiye

Market leaders and key company profiles

Siemens Healthineers

Accuray Incorporated

Elekta

Brainlab AG

RefleXion

Hitachi Ltd

IBA Worldwide

GT Medical Technologies, Inc.

Mevion Medical Systems

Theragenics Corporation

Get more information on this report

Middle East Cancer Radiation Therapy Market Report Coverage and Deliverables:

The "Middle East Cancer Radiation Therapy Market Size and Forecast (2021 - 2031)" report provides a detailed analysis of the market covering below areas:

Middle East Cancer Radiation Therapy market size and forecast at regional and country levels for market segments covered under the scope

Middle East Cancer Radiation Therapy market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Middle East Cancer Radiation Therapy market analysis covering key market trends, regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Middle East Cancer Radiation Therapy market

Detailed company profiles, including SWOT analysis

Middle East Cancer Radiation Therapy Market Geographic Insights:

The geographical scope of the Middle East Cancer Radiation Therapy market report is divided into: the UAE, Saudi Arabia, Bahrain, Oman, Kuwait, Qatar, and Turkiye. Turkiye held the largest share in 2024.

Turkiye dominates the Middle East cancer radiation therapy market due to its well-established oncology infrastructure and robust investment in advanced radiotherapy technologies. Major cities such as Istanbul, Ankara, and Izmir host highly equipped cancer centers with linear accelerators, image-guided systems, stereotactic radiosurgery units, and brachytherapy facilities. Turkiye has developed a strong cohort of radiation oncologists, medical physicists, and technologists through comprehensive local training programs and collaborations with international oncology organizations.

The country's leadership is reinforced by its strategic focus on integrating multidisciplinary cancer care, combining surgery, systemic therapy, and precision radiotherapy for complex cases. Turkiye continuously upgrades its equipment and digital planning systems, supports research initiatives, and implements standardized treatment protocols across leading oncology centers. Its position as a regional hub attracts patients from neighboring countries seeking high-quality radiotherapy, solidifying Turkiye's role as the primary driver of the Middle East cancer radiation therapy market.

Get more information on this report

Middle East Cancer Radiation Therapy Market Research Report Guidance:

The report includes qualitative and quantitative data in the Middle East cancer radiation therapy market across type, cancer type, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Middle East Cancer Radiation Therapy market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Middle East Cancer Radiation Therapy market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Middle East Cancer Radiation Therapy market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover Middle East Cancer Radiation Therapy market segments by type, cancer type, end user, and geography across the UAE, Saudi Arabia, Bahrain, Oman, Kuwait, Qatar, and Turkiye. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Middle East Cancer Radiation Therapy market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Middle East Cancer Radiation Therapy Market News and Key Development:

The Middle East Cancer Radiation Therapy market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Middle East cancer radiation therapy market are:

In April 2025, Toshiba Energy Systems & Solutions Corporation announced that it received an order for a heavy‑ion therapy system from Cleveland Clinic Abu Dhabi, marking the first heavy‑ion cancer therapy system in the Middle East and expanding advanced radiotherapy treatment capabilities in the UAE.

In January 2023, American Hospital Dubai (UAE) announced that it signed a strategic agreement with Emitac Healthcare Solutions and Varian (a Siemens Healthineers company) to install the Halcyon linear accelerator system, making it the first of its kind in the GCC region and enhancing access to advanced image‑guided radiation therapy.

Key Sources Referred:

The World BankWorld Health Organization (WHO)Center for Disease Control and Prevention (CDC)Union for International Cancer Control (UICC)International Agency for Research on Cancer (IARC)American Society for Radiation Oncology (ASTRO)European Society for Radiotherapy & Oncology (ESTRO)Asia-Oceania Federation of Organizations for Radiological Technology (AOFRT)Company WebsitesCompany Annual ReportsCompany Investor Presentations

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Middle East Cancer Radiation Therapy Market?

The Middle East Cancer Radiation Therapy Market is valued at US$ 631.1 Million in 2024, it is projected to reach US$ 1,243.7 Million by 2031.

What is the CAGR for Middle East Cancer Radiation Therapy Market by (2025 - 2031)?

As per our report Middle East Cancer Radiation Therapy Market, the market size is valued at US$ 631.1 Million in 2024, projecting it to reach US$ 1,243.7 Million by 2031. This translates to a CAGR of approximately 10.2% during the forecast period.

What segments are covered in this report?

The Middle East Cancer Radiation Therapy Market report typically cover these key segments-

Type (External Beam Radiation Therapy, Internal Beam Radiation Therapy)

Cancer Type (Lung Cancer, Breast Cancer, Colorectal Cancer, Prostate Cancer, Head & Neck Cancer, Cervical Cancer, Other Cancer Types)

End User (Hospitals, Specialty Clinics, Ambulatory and Radiotherapy Centers, Academic and Research Institutes)

What is the historic period, base year, and forecast period taken for Middle East Cancer Radiation Therapy Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East Cancer Radiation Therapy Market report:

Historic Period : 2021-2023

Base Year : 2024

Forecast Period : 2025-2031

Who are the major players in Middle East Cancer Radiation Therapy Market?

The Middle East Cancer Radiation Therapy Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Siemens Healthineers

Accuray Incorporated

Elekta

Brainlab AG

RefleXion

Hitachi Ltd

IBA Worldwide

GT Medical Technologies, Inc.

Mevion Medical Systems

Theragenics Corporation

Who should buy this report?

The Middle East Cancer Radiation Therapy Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Middle East Cancer Radiation Therapy Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Middle East Cancer Radiation Therapy Market

Get Free Sample For Middle East Cancer Radiation Therapy Market