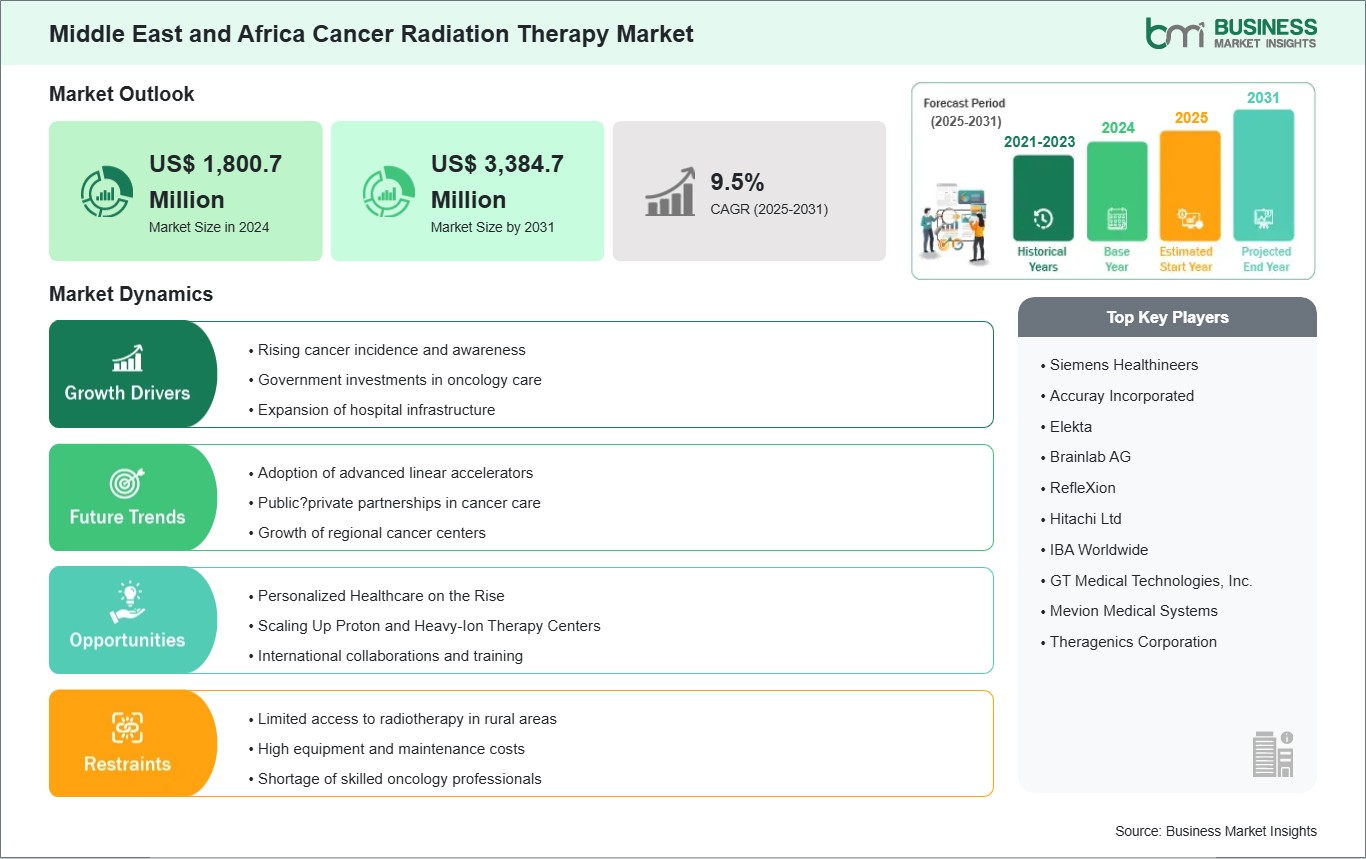

The Middle East and Africa cancer radiation therapy market size is expected to reach US$ 3,384.7 million by 2031 from US$ 1,800.7 million in 2024. The market is estimated to record a CAGR of 9.5% from 2025 to 2031.

Executive Summary and Middle East and Africa Cancer Radiation Therapy Market Analysis:

The Middle East & Africa (MEA) cancer radiation therapy market is expanding as governments and private healthcare providers respond to rising cancer incidence, particularly breast, prostate, and cervical cancers. The region shows a diverse landscape, with advanced oncology centers in South Africa, Saudi Arabia, and the UAE coexisting with areas that have limited access to radiotherapy services. Urban hospitals are adopting high-precision external beam radiotherapy, image-guided systems, and brachytherapy, while cross-border collaborations help transfer clinical expertise and technology to developing markets. Regional initiatives promoting early diagnosis and integration of radiation therapy into national cancer care programs are contributing to a steady increase in patient access in metropolitan centers.

Despite this growth, the MEA market faces several constraints that affect uniform adoption. Rural and lower-income regions struggle with limited infrastructure, workforce shortages, and high capital costs for advanced equipment. Procurement delays and inconsistent regulatory frameworks in certain countries slow technology deployment, while the lack of trained radiation oncologists and physicists restricts the reach of complex treatment modalities. Opportunities exist in leveraging digital oncology solutions, such as telemedicine-based treatment planning, cloud-enabled workflow management, and AI-assisted dose planning, which can enhance efficiency, extend care to underserved areas, and support the long-term modernization of radiation therapy services across the region.

Middle East and Africa Cancer Radiation Therapy Market - Strategic Insights:

Get more information on this report

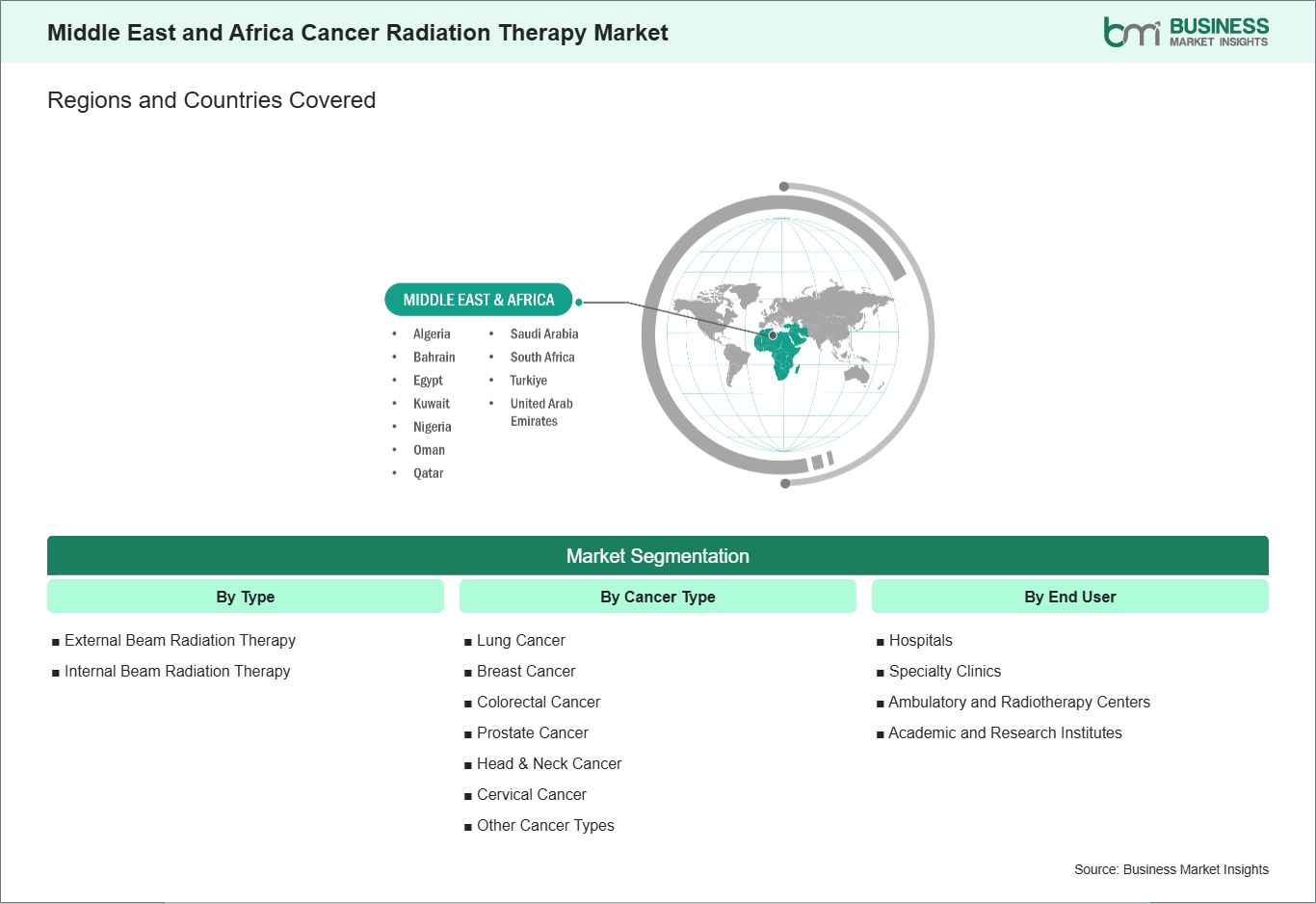

Middle East and Africa Cancer Radiation Therapy Market Segmentation Analysis:

Key segments that contributed to the derivation of the Middle East and Africa cancer radiation therapy market analysis are type, cancer type, and end user.

By type, the cancer radiation therapy market is segmented into external beam radiation therapy and internal beam radiation therapy. The external beam radiation therapy segment dominated the market in 2024.

Based on cancer type, the cancer radiation therapy market is segmented into lung cancer, breast cancer, colorectal cancer, prostate cancer, head & neck cancer, cervical cancer, and others. The lung cancer segment dominated the market in 2024.

In terms of end user, the cancer radiation therapy market is segmented into hospitals, specialty clinics, ambulatory and radiotherapy centers, and academic and research institutes. The hospitals segment dominated the market in 2024.

Middle East and Africa Cancer Radiation Therapy Market Drivers and Opportunities:

Growing Frequency of Cancer

Cancer prevalence is accelerating across the Middle East and Africa due to aging populations, rapid urbanization, and persistent exposure to risk factors such as tobacco, air pollution, and infectious agents. Gulf countries such as Saudi Arabia and the UAE are experiencing more breast and thyroid cancers alongside lifestyle-related colorectal cases, while North African nations report high burdens of liver cancer linked to hepatitis and schistosomiasis. In Sub‑Saharan Africa, head‑and‑neck and cervical cancers remain prominent, with late-stage presentations common in Nigeria, Ethiopia, and Tanzania.

Screening and diagnostic expansion are uneven, creating distinct demand profiles for radiation therapy across the region. Tertiary centers in Riyadh, Abu Dhabi, and Cairo are scaling external beam platforms for complex cases, while emerging hubs in Nairobi and Accra prioritize foundational linear accelerator capacity to address backlog and geographic access gaps. Brachytherapy is being revitalized for cervical cancer in East and Southern Africa, and for prostate cancer in South Africa and Morocco, reflecting disease patterns and cost-effectiveness in resource-limited settings.

Government strategies and philanthropic initiatives are catalyzing oncology infrastructure growth, but workforce and maintenance constraints persist. National cancer plans in the Gulf emphasize technology upgrades and quality assurance, whereas African programs focus on decentralizing services and strengthening referral networks. As awareness campaigns and vaccination efforts (HPV, hepatitis B) expand, more patients enter formal care pathways—sustaining a multi‑year surge in radiation therapy demand and positioning cancer prevalence as a durable driver of the Middle East and Africa market.

Personalized Healthcare on the Rise

Personalized oncology is gaining momentum across the Middle East and Africa as precision imaging, molecular testing, and adaptive planning become more accessible. Leading centers in the Gulf integrate genomic profiling and PET/CT into radiotherapy decision‑making, enabling dose adaptation for radiosensitive subtypes and complex head‑and‑neck cases. In South Africa and Egypt, multidisciplinary boards are standardizing contouring and leveraging MRI for gynecologic and brain tumors, while pilot radiomics projects explore image‑based biomarkers to refine treatment intensity.

Technology adoption is widening the personalization toolkit beyond conventional EBRT. IMRT, IGRT, and SBRT are routine in Gulf and North African tertiary hospitals, supporting hypofractionated schedules for breast and prostate cancers and stereotactic approaches for oligometastatic disease. Proton therapy referrals from the Middle East to regional centers are growing for pediatric and skull‑base indications, and African programs are upgrading brachytherapy with 3D image guidance to tailor dose for cervical cancer—reducing toxicity while improving local control.

Policy shifts and training collaborations are aligning incentives with individualized care. Reimbursement frameworks in the Gulf are expanding coverage for advanced techniques and adaptive workflows, while African public‑private partnerships fund planning software, QA programs, and workforce development. Patients are seeking shorter courses with fewer side effects, and cross‑border care pathways—such as referrals to high‑complexity centers—support access to precision platforms. These dynamics create a clear opportunity for vendors and providers to deliver integrated, patient‑specific radiation therapy solutions tailored to the diverse clinical and resource realities of the Middle East and Africa.

Middle East and Africa Cancer Radiation Therapy Market Size and Share Analysis:

The Middle East and Africa cancer radiation therapy market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report further examines subsegments categorized within type, cancer type, and end user, offering insights into their contribution to overall market performance.

By type, the external beam radiation therapy subsegment dominated the market in 2024. Due to its widespread availability, precision targeting, noninvasive nature, and effectiveness in treating diverse cancers, it is the preferred choice across global oncology practices.

Based on cancer type, the lung cancer subsegment dominated the market in 2024. Due to its high incidence, strong link with smoking and pollution, late‑stage diagnoses, and reliance on advanced radiation techniques, it is the most treated cancer type globally.

In terms of end user, the hospitals subsegment dominated the market in 2024. Hospitals dominated the market since they provide comprehensive cancer care, advanced radiation infrastructure, skilled oncologists, and integrated treatment pathways, making them the primary setting for delivering radiation therapy services.

Middle East and Africa Cancer Radiation Therapy Market Report Highlights:

Report Attribute

Details

Market size in 2024

US$ 1,800.7 Million

Market Size by 2031

US$ 3,384.7 Million

CAGR (2025 - 2031)

9.5%

Historical Data

2021-2023

Forecast period

2025-2031

Segments Covered

By Type

External Beam Radiation Therapy

Internal Beam Radiation Therapy

By Cancer Type

Lung Cancer

Breast Cancer

Colorectal Cancer

Prostate Cancer

Head & Neck Cancer

Cervical Cancer

Other Cancer Types

By End User

Hospitals

Specialty Clinics

Ambulatory and Radiotherapy Centers

Academic and Research Institutes

Regions and Countries Covered

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Siemens Healthineers

Accuray Incorporated

Elekta

Brainlab AG

RefleXion

Hitachi Ltd

IBA Worldwide

GT Medical Technologies, Inc.

Mevion Medical Systems

Theragenics Corporation

Get more information on this report

Middle East and Africa Cancer Radiation Therapy Market Report Coverage and Deliverables:

The "Middle East and Africa Cancer Radiation Therapy Market Size and Forecast (2021 - 2031)" report provides a detailed analysis of the market covering below areas:

Middle East and Africa Cancer Radiation Therapy market size and forecast at regional and country levels for key market segments covered under the scope

Middle East and Africa Cancer Radiation Therapy market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Middle East and Africa Cancer Radiation Therapy market analysis covering key market trends, regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Middle East and Africa Cancer Radiation Therapy market

Detailed company profiles, including SWOT analysis

Middle East and Africa Cancer Radiation Therapy Market Geographic Insights:

The geographical scope of the Middle East and Africa Cancer Radiation Therapy market report is divided into: Saudi Arabia, the UAE, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria, and the Rest of MEA. South Africa held the largest share in 2024.

South Africa leads the MEA radiation therapy market due to its well-developed oncology infrastructure, concentration of high-technology cancer centers, and a robust pool of trained professionals. Major cities such as Johannesburg, Cape Town, and Pretoria host most of the country's advanced facilities, including linear accelerators, stereotactic and image-guided systems, and brachytherapy units. South Africa's dual public-private healthcare model allows for the early adoption of advanced techniques in private hospitals while maintaining broader patient access in public centers. The country's investment in workforce training programs ensures a steady supply of radiation oncologists, medical physicists, and technologists capable of managing complex treatment protocols.

Challenges persist, particularly in extending these services to rural provinces where infrastructure and specialist availability are limited. To address these gaps, South Africa is focusing on digital oncology integration, telemedicine platforms, and coordinated public sector expansion to improve access and treatment efficiency. Additionally, as a regional referral hub, South Africa attracts patients from neighboring countries seeking high-quality radiotherapy, reinforcing its leadership position. Sustained investment in equipment modernization, clinical training, and technology adoption ensures the country continues to shape the evolution of the MEA cancer radiation therapy market.

Get more information on this report

Middle East and Africa Cancer Radiation Therapy Market Research Report Guidance:

The report includes qualitative and quantitative data in the Middle East and Africa cancer radiation therapy market across type, cancer type, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Middle East and Africa Cancer Radiation Therapy market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Middle East and Africa Cancer Radiation Therapy market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Middle East and Africa Cancer Radiation Therapy market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover Middle East and Africa Cancer Radiation Therapy market segments by type, cancer type, end user, and geography across Saudi Arabia, the UAE, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria, and the Rest of MEA. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Middle East and Africa Cancer Radiation Therapy market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Middle East and Africa Cancer Radiation Therapy Market News and Key Development:

The Middle East and Africa Cancer Radiation Therapy market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Middle East and Africa cancer radiation therapy market are:

In September 2025, Varian, a Siemens Healthineers company, announced that it donated a linear accelerator to the IAEA's Rays of Hope Initiative for installation at Black Lion Hospital in Addis Ababa, Ethiopia, aimed at strengthening radiation medicine infrastructure and cancer treatment capacity in East Africa.

In November 2021, Elekta announced that its Elekta Unity MR-Linac order in Africa included delivery of advanced radiation therapy technology (Unity plus additional linacs and brachytherapy devices) to the International Children's Cancer Research Centre in Ghana, expanding high-precision treatment access for pediatric and adult cancer patients in West Africa as part of the company's ACCESS 2025 strategy.

Key Sources Referred:

The World BankWorld Health Organization (WHO)Center for Disease Control and Prevention (CDC)Union for International Cancer Control (UICC)International Agency for Research on Cancer (IARC)American Society for Radiation Oncology (ASTRO)European Society for Radiotherapy & Oncology (ESTRO)Asia-Oceania Federation of Organizations for Radiological Technology (AOFRT)Company WebsitesCompany Annual ReportsCompany Investor Presentations

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Middle East and Africa Cancer Radiation Therapy Market?

The Middle East and Africa Cancer Radiation Therapy Market is valued at US$ 1,800.7 Million in 2024, it is projected to reach US$ 3,384.7 Million by 2031.

What is the CAGR for Middle East and Africa Cancer Radiation Therapy Market by (2025 - 2031)?

As per our report Middle East and Africa Cancer Radiation Therapy Market, the market size is valued at US$ 1,800.7 Million in 2024, projecting it to reach US$ 3,384.7 Million by 2031. This translates to a CAGR of approximately 9.5% during the forecast period.

What segments are covered in this report?

The Middle East and Africa Cancer Radiation Therapy Market report typically cover these key segments-

Type (External Beam Radiation Therapy, Internal Beam Radiation Therapy)

Cancer Type (Lung Cancer, Breast Cancer, Colorectal Cancer, Prostate Cancer, Head & Neck Cancer, Cervical Cancer, Other Cancer Types)

End User (Hospitals, Specialty Clinics, Ambulatory and Radiotherapy Centers, Academic and Research Institutes)

What is the historic period, base year, and forecast period taken for Middle East and Africa Cancer Radiation Therapy Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East and Africa Cancer Radiation Therapy Market report:

Historic Period : 2021-2023

Base Year : 2024

Forecast Period : 2025-2031

Who are the major players in Middle East and Africa Cancer Radiation Therapy Market?

The Middle East and Africa Cancer Radiation Therapy Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Siemens Healthineers

Accuray Incorporated

Elekta

Brainlab AG

RefleXion

Hitachi Ltd

IBA Worldwide

GT Medical Technologies, Inc.

Mevion Medical Systems

Theragenics Corporation

Who should buy this report?

The Middle East and Africa Cancer Radiation Therapy Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Middle East and Africa Cancer Radiation Therapy Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Middle East and Africa Cancer Radiation Therapy Market

Get Free Sample For Middle East and Africa Cancer Radiation Therapy Market