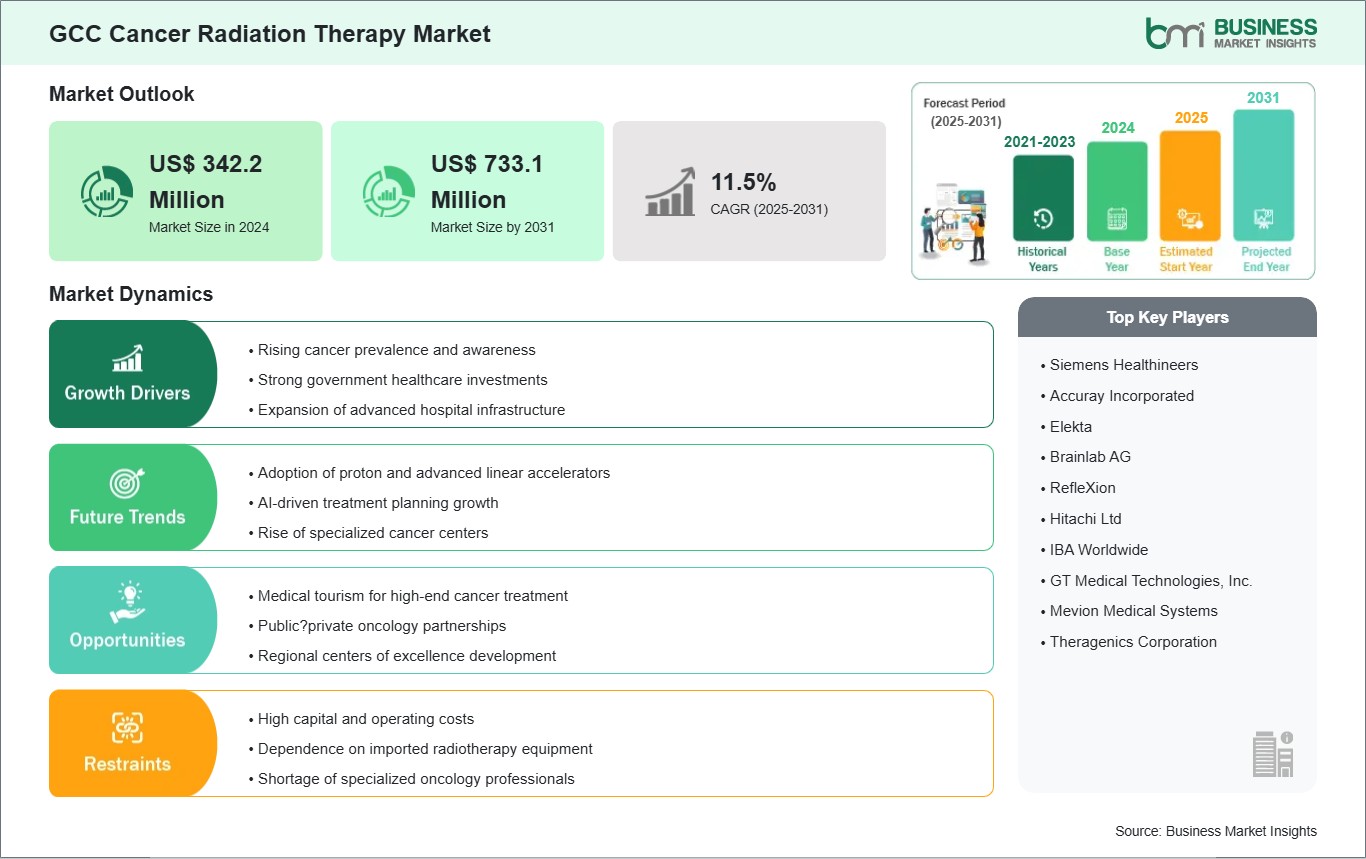

The GCC cancer radiation therapy market size is expected to reach US$ 733.1 million by 2031 from US$ 342.2 million in 2024. The market is estimated to record a CAGR of 11.5% from 2025 to 2031.

Executive Summary and GCC Cancer Radiation Therapy Market Analysis:

The cancer radiation therapy market in the GCC is evolving rapidly, supported by large‑scale healthcare transformation programs and strong government initiatives aimed at expanding specialized oncology services. Countries such as Saudi Arabia, the UAE, and Qatar are investing heavily in modern radiotherapy infrastructure, integrating advanced treatment technologies, and strengthening multidisciplinary cancer care pathways. These investments are aligned with national health visions that emphasize early diagnosis, improved patient navigation, and the establishment of comprehensive cancer centers capable of handling complex cases. The region's growing focus on medical tourism, especially for high‑technology oncology procedures, reinforces the demand for precision‑based radiotherapy.

Despite this momentum, several structural restraints remain. Dependence on expatriate clinical talent, limited regional training pipelines, and fragmented access outside major metropolitan hubs create disparities in care availability. Procurement cycles can be lengthy due to regulatory and budgeting complexities, slowing the adoption of next‑generation systems. Nonetheless, the GCC presents substantial opportunities for long‑term growth. Artificial intelligence tools, adaptive therapy platforms, cloud‑enabled planning ecosystems, and fully digitalized oncology workflows can help optimize throughput, standardize protocols, and reduce reliance on external expertise. As GCC countries continue reshaping their healthcare systems toward advanced, technology‑driven oncology models, radiotherapy is set to become a central pillar of modern cancer treatment strategies across the region.

GCC Cancer Radiation Therapy Market - Strategic Insights:

Get more information on this report

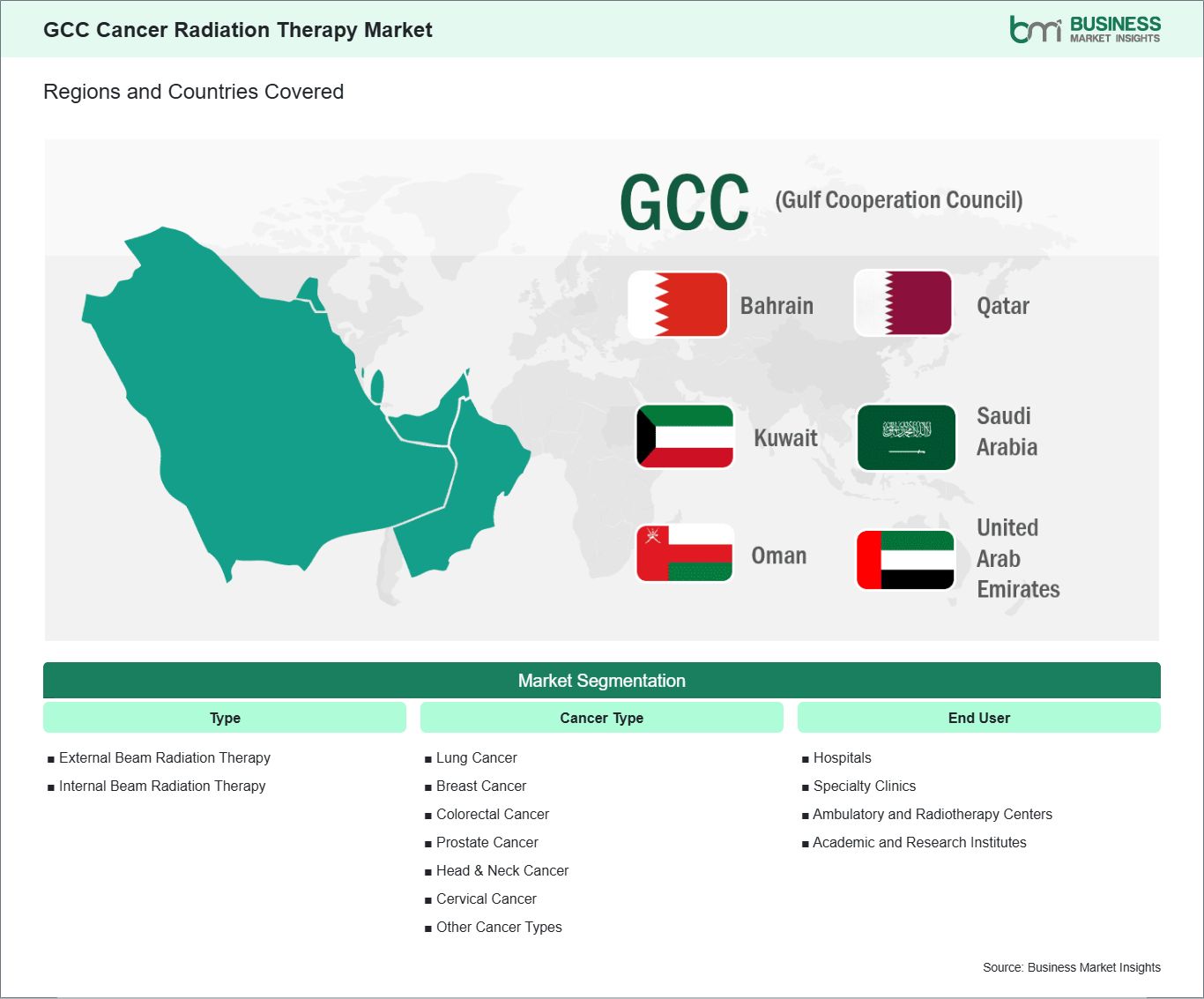

GCC Cancer Radiation Therapy Market Segmentation Analysis:

Key segments that contributed to the derivation of the GCC cancer radiation therapy market analysis are type, cancer type, and end user.

By type, the cancer radiation therapy market is segmented into external beam radiation therapy and internal beam radiation therapy. The external beam radiation therapy segment dominated the market in 2024.

Based on cancer type, the cancer radiation therapy market is segmented into lung cancer, breast cancer, colorectal cancer, prostate cancer, head & neck cancer, cervical cancer, and others. The lung cancer segment dominated the market in 2024.

In terms of end user, the cancer radiation therapy market is segmented into hospitals, specialty clinics, ambulatory and radiotherapy centers, and academic and research institutes. The hospitals segment dominated the market in 2024.

GCC Cancer Radiation Therapy Market Drivers and Opportunities:

Widening Spread of Cancer

Cancer incidence in the GCC (Gulf Cooperation Council) countries including Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, and Oman is rising due to aging populations, urbanization, and lifestyle-related risk factors such as obesity, diabetes, and smoking. Breast, colorectal, and thyroid cancers are among the most commonly diagnosed, with prostate and lung cancers also showing increasing trends. Early detection programs are improving, leading to higher numbers of patients eligible for radiation therapy.

Healthcare systems in the GCC are heavily investing in oncology infrastructure, with advanced cancer centers established in major cities such as Riyadh, Dubai, and Doha. External beam radiation therapy is widely available and is used to treat solid tumors such as breast and colorectal cancers, while internal beam therapy is adopted for prostate and gynecological cancers. These expansions are aimed at addressing the growing cancer burden and ensuring comprehensive care.

Government initiatives and private-sector investments are boosting diagnostic capabilities and treatment capacity across the region. Referral networks are strengthening, enabling timely access to radiation therapy for both early- and late-stage cancer patients. The increasing prevalence of cancer remains a key driver for the GCC cancer radiation therapy market, fueling demand for both infrastructure and advanced treatment technologies.

Demand Soars for Individualized Healthcare

Personalized medicine is emerging as a significant focus in the GCC, driven by patient demand for tailored treatment and government support for advanced healthcare technologies. Radiation therapy is delivered based on individual tumor characteristics, location, and patient-specific factors, improving treatment outcomes while minimizing side effects. Hospitals in the region are adopting image-guided and intensity-modulated radiation therapy to enhance precision.

External beam radiation therapy is customized using advanced planning tools, while internal beam therapy, particularly for prostate and gynecological cancers, is delivered with patient-specific dosing. The integration of AI-driven software and modern imaging is allowing clinicians to optimize treatment schedules and achieve better outcomes. These technologies are being implemented in leading cancer centers in the UAE, Saudi Arabia, and Qatar.

Collaboration with international research institutes and technology providers is helping the GCC region build expertise in personalized oncology care. Patients are becoming more aware of treatment options and are actively seeking therapies with reduced side effects and higher efficacy. This rising demand for personalized medicine presents substantial opportunities for equipment manufacturers, software providers, and healthcare service companies in the GCC cancer radiation therapy market.

GCC Cancer Radiation Therapy Market Size and Share Analysis:

The GCC cancer radiation therapy market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report further examines subsegments categorized within type, cancer type, and end user, offering insights into their contribution to overall market performance.

By type, the external beam radiation therapy subsegment dominated the market in 2024. Due to its widespread availability, precision targeting, noninvasive nature, and effectiveness in treating diverse cancers, it is the preferred choice across global oncology practices.

Based on cancer type, the lung cancer subsegment dominated the market in 2024. Due to its high incidence, strong link with smoking and pollution, late‑stage diagnoses, and reliance on advanced radiation techniques, it is the most treated cancer type globally.

In terms of end user, the hospitals subsegment dominated the market in 2024. Hospitals dominated the market since they provide comprehensive cancer care, advanced radiation infrastructure, skilled oncologists, and integrated treatment pathways, making them the primary setting for delivering radiation therapy services.

GCC Cancer Radiation Therapy Market Report Highlights:

Report Attribute

Details

Market size in 2024

US$ 342.2 Million

Market Size by 2031

US$ 733.1 Million

CAGR (2025 - 2031)

11.5%

Historical Data

2021-2023

Forecast period

2025-2031

Segments Covered

By Type

External Beam Radiation Therapy

Internal Beam Radiation Therapy

By Cancer Type

Lung Cancer

Breast Cancer

Colorectal Cancer

Prostate Cancer

Head & Neck Cancer

Cervical Cancer

Other Cancer Types

By End User

Hospitals

Specialty Clinics

Ambulatory and Radiotherapy Centers

Academic and Research Institutes

Regions and Countries Covered

GCC

UAE, Bahrain, Saudi Arabia, Oman, Qatar, Kuwait

Market leaders and key company profiles

Siemens Healthineers

Accuray Incorporated

Elekta

Brainlab AG

RefleXion

Hitachi Ltd

IBA Worldwide

GT Medical Technologies, Inc.

Mevion Medical Systems

Theragenics Corporation

Get more information on this report

GCC Cancer Radiation Therapy Market Report Coverage and Deliverables:

The "GCC Cancer Radiation Therapy Market Size and Forecast (2021 - 2031)" report provides a detailed analysis of the market covering below areas:

GCC Cancer Radiation Therapy market size and forecast at regional and country levels for key market segments covered under the scope

GCC Cancer Radiation Therapy market trends, as well as market dynamics such as drivers, restraints, and key opportunities

GCC Cancer Radiation Therapy market analysis covering key market trends, regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the GCC Cancer Radiation Therapy market

Detailed company profiles, including SWOT analysis

GCC Cancer Radiation Therapy Market Geographic Insights:

The geographical scope of the GCC Cancer Radiation Therapy market report is divided into: Saudi Arabia, the United Arab Emirates (UAE), Qatar, Kuwait, Bahrain, and Oman. Saudi Arabia held the largest share in 2024.

Saudi Arabia dominates the GCC cancer radiation therapy market due to its extensive healthcare transformation agenda, significant infrastructure investments, and rapidly expanding network of specialized cancer centers. The Kingdom has prioritized oncology within its national health vision, enabling the deployment of advanced radiotherapy technologies across major hospitals and dedicated cancer institutes. These facilities incorporate sophisticated treatment‑planning platforms, high‑precision imaging workflows, and modern linear accelerator technologies that support complex, protocol‑driven radiotherapy techniques. A defining strength of Saudi Arabia's leadership is its systematic approach to building a resilient oncology ecosystem. Large-scale government initiatives focus on enhancing clinical pathways, strengthening physics oversight, and integrating multidisciplinary tumor boards to ensure consistent, evidence‑based care. The Kingdom is also expanding its training capacity through partnerships with global academic institutions and medical technology companies, enabling local clinicians, physicists, and radiotherapy technologists to gain expertise in advanced workflows. Additionally, the country's strategic investment in digital health—ranging from integrated oncology records to AI-assisted planning and automated quality systems—positions it at the forefront of tech‑driven radiotherapy modernization in the region. As Saudi Arabia continues advancing its oncology capabilities, it stands as the key anchor shaping radiotherapy standards and innovation within the GCC.

Get more information on this report

GCC Cancer Radiation Therapy Market Research Report Guidance:

The report includes qualitative and quantitative data in the GCC cancer radiation therapy market across type, cancer type, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the GCC Cancer Radiation Therapy market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the GCC Cancer Radiation Therapy market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the GCC Cancer Radiation Therapy market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover GCC Cancer Radiation Therapy market segments by type, cancer type, end user, and geography across Saudi Arabia, the United Arab Emirates (UAE), Qatar, Kuwait, Bahrain, and Oman. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the GCC Cancer Radiation Therapy market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

GCC Cancer Radiation Therapy Market News and Key Development:

The GCC Cancer Radiation Therapy market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the GCC cancer radiation therapy market are:

In February2025, Burjeel Holdings announced that it had acquired an 80% stake in the Dubai‑based Advanced Care Oncology Center (ACOC) and planned to establish a leading radiation oncology network across the GCC, integrating advanced LINAC systems, AI‑driven radiation planning, and precision imaging tools to expand access to cancer radiotherapy services across the UAE and neighboring markets.

In June2023, American Hospital Dubai announced that it had signed a strategic agreement with Emitac Healthcare Solutions and Varian (a Siemens Healthineers company) to install a Varian Halcyon linear accelerator—the first of its kind in the GCC—enhancing precise, image‑guided radiation therapy offerings for cancer patients in the region.

Key Sources Referred:

The World BankWorld Health Organization (WHO)Center for Disease Control and Prevention (CDC)Union for International Cancer Control (UICC)International Agency for Research on Cancer (IARC)American Society for Radiation Oncology (ASTRO)European Society for Radiotherapy & Oncology (ESTRO)Asia-Oceania Federation of Organizations for Radiological Technology (AOFRT)Company WebsitesCompany Annual ReportsCompany Investor Presentations

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the GCC Cancer Radiation Therapy Market?

The GCC Cancer Radiation Therapy Market is valued at US$ 342.2 Million in 2024, it is projected to reach US$ 733.1 Million by 2031.

What is the CAGR for GCC Cancer Radiation Therapy Market by (2025 - 2031)?

As per our report GCC Cancer Radiation Therapy Market, the market size is valued at US$ 342.2 Million in 2024, projecting it to reach US$ 733.1 Million by 2031. This translates to a CAGR of approximately 11.5% during the forecast period.

What segments are covered in this report?

The GCC Cancer Radiation Therapy Market report typically cover these key segments-

Type (External Beam Radiation Therapy, Internal Beam Radiation Therapy)

Cancer Type (Lung Cancer, Breast Cancer, Colorectal Cancer, Prostate Cancer, Head & Neck Cancer, Cervical Cancer, Other Cancer Types)

End User (Hospitals, Specialty Clinics, Ambulatory and Radiotherapy Centers, Academic and Research Institutes)

What is the historic period, base year, and forecast period taken for GCC Cancer Radiation Therapy Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the GCC Cancer Radiation Therapy Market report:

Historic Period : 2021-2023

Base Year : 2024

Forecast Period : 2025-2031

Who are the major players in GCC Cancer Radiation Therapy Market?

The GCC Cancer Radiation Therapy Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Siemens Healthineers

Accuray Incorporated

Elekta

Brainlab AG

RefleXion

Hitachi Ltd

IBA Worldwide

GT Medical Technologies, Inc.

Mevion Medical Systems

Theragenics Corporation

Who should buy this report?

The GCC Cancer Radiation Therapy Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the GCC Cancer Radiation Therapy Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For GCC Cancer Radiation Therapy Market

Get Free Sample For GCC Cancer Radiation Therapy Market