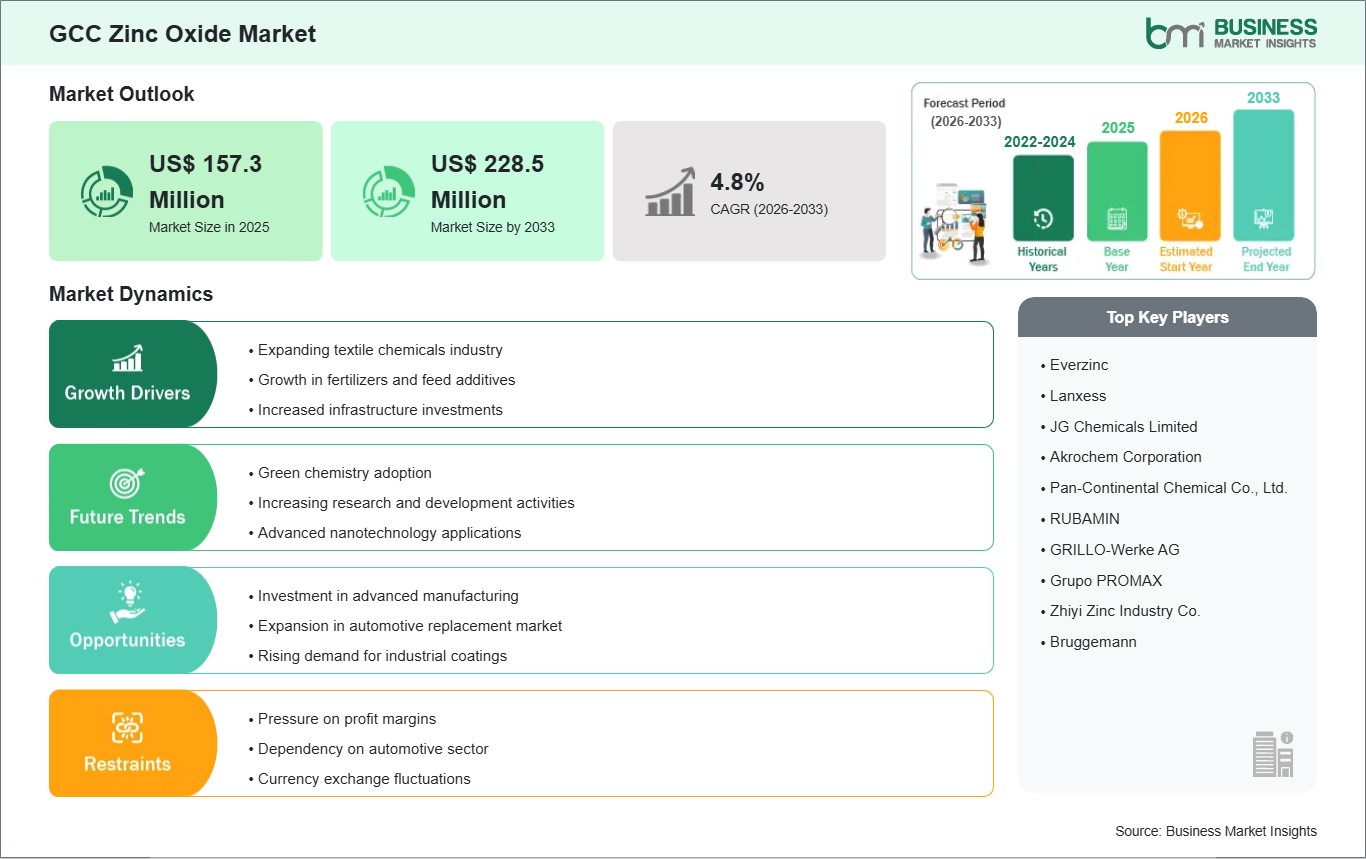

The GCC zinc oxide market size is expected to reach US$ 228.5 million by 2033 from US$ 157.3 million in 2025. The market is estimated to record a CAGR of 4.8% from 2026 to 2033.

Executive Summary and GCC Zinc Oxide Market Analysis:

GCC zinc oxide industry is characterized by fast-paced diversification of industries, high integration of petrochemicals, and increased downstream manufacturing operations in construction, rubber compounding, coatings, and specialty chemicals. The consumption of zinc oxide in the GCC countries is mainly propelled by its uses in rubber vulcanization, protective coatings, ceramics, pharmaceuticals, and personal care products. The GCC zinc oxide market is highly dependent on large-scale infrastructure projects, industrial diversification policies beyond oil, and localization of chemical manufacturing processes in GCC nations. In the GCC, countries like UAE, Qatar, and Oman continue to add to the demand side in terms of construction-driven economies, upgrading infrastructure, and establishing manufacturing areas. The UAE, in particular, emerges as an important country for the trade and re-trade of specialty chemicals, which ensures that zinc oxide is supplied to other countries in the region. Moreover, the growing trend of cosmetics and personal care products in the GCC is leading to demand for high-purity zinc oxide to be used in skin care and sunscreens suitable for extreme climates. The market is, however, constrained by the shortage of domestic resources, dependence on imported zinc as raw materials, and increased costs of manufacturing due to energy-intensive operations. In addition to that, environmental laws concerning industrial emissions and chemical handling are becoming stricter, especially for urban-based industrial areas. Also, changes in the supply chain of global zinc may affect pricing stability in the region. Overall, the market in the GCC is growing steadily owing to diversification in industries, construction activities, and the growing demand for specialty chemicals.

GCC Zinc Oxide Market - Strategic Insights:

Get more information on this report

GCC Zinc Oxide Market Segmentation Analysis:

Key segments that contributed to the derivation of the GCC zinc oxide market analysis are process, grade, and application.

By process, the zinc oxide market is segmented into Indirect process, direct process, and wet chemical process. The indirect process segment dominated the market in 2025.

Based on grade, the zinc oxide market is segmented into standard, treated, USP, FCC, and other grades. The standard segment dominated the market in 2025.

On the basis of application, the zinc oxide market is classified into rubber, ceramics, chemicals, agriculture, cosmetics and personal care, pharmaceuticals, and other applications. The rubber segment dominated the market in 2025.

GCC Zinc Oxide Market Drivers and Opportunities:

Expanding Textile Chemicals Industry

The GCC market for zinc oxide continues to grow steadily, thanks to the growth in the production of textile chemicals in nations like Saudi Arabia, the UAE, and Oman. Although the GCC nations are not major centers of textile production, they have become adept at producing technical textiles, clothing finish, and industrial fabrics. Zinc oxide has come to be used more and more in textile chemicals because of its anti-bacterial, UV protective, and deodorizing capabilities. This becomes particularly useful in the GCC, which enjoys a hot climate where the need for UV-protecting and breathable fabrics is increasing.

Textile finishing and functional textile manufacturing are growing in Saudi Arabia as part of the country's efforts at industrial diversification. The industrial cities of Jubail and Yanbu are developing textile finishes based on petrochemicals and therefore promoting the inclusion of zinc oxide in coating solutions and treatment of synthetic fibers. Dubai and Abu Dhabi in the United Arab Emirates have become centers of high-performance textiles in the hospitality, military, and sportswear industries. Zinc oxide-treated textiles are increasingly being utilized in uniforms, protective garments, and outdoor clothing because of their ability to withstand degradation from ultraviolet radiation and microorganisms in high temperatures.

Oman and Bahrain are also slowly establishing their textile and garment manufacturing capacity, especially industrial textiles. The use of antimicrobial textiles in the health care and hospitality sectors is driving demand for zinc oxide. Hospitals and hotels in the Gulf Cooperation Council countries are incorporating treated textiles in beddings, curtains, and upholstery to enhance hygiene levels. As consumers become more aware of the importance of functional and sustainable textiles, zinc oxide will continue to be incorporated in textile chemical formulations.

Investment in Advanced Manufacturing

The GCC zinc oxide market is being significantly impacted by increasing investments in advanced manufacturing technologies amid the diversification efforts away from oil-based economies. The Vision 2030 of Saudi Arabia and the industrial plans of the UAE have been instrumental in the rapid emergence of advanced manufacturing clusters, especially in the chemicals, electronics, and materials processing sectors. Zinc oxide finds extensive application in these industries owing to its use in the manufacturing of ceramics, coatings, electronics, and rubber processing.

The kingdom of Saudi Arabia is making significant investments in industrial mega projects such as NEOM and the development of its petrochemical downstream sector which includes the manufacturing of advanced materials and coatings. Zinc oxide is utilized in the manufacturing of corrosion protection coatings, catalysis, and rubber products for automotive and industrial purposes. In the UAE, free zones such as Jebel Ali and KIZAD are attracting many international players in the manufacture of electronics, automotive parts, and specialty chemicals, further boosting the need for zinc oxide in industrial applications.

Similarly, Qatar, Oman, and Bahrain are playing their part in driving advanced manufacturing through the processing of aluminum, construction materials, and petrochemical derivatives. Zinc oxide finds extensive use in heat resistant ceramic materials, industrial adhesives, and protective coatings for infrastructure facing extreme heat exposure and corrosive conditions due to proximity to the coast. With the increasing trend towards localization of manufacturing activities in the GCC region, the market for zinc oxide is set to see steady growth in the coming years.

GCC Zinc Oxide Market Size and Share Analysis:

The GCC zinc oxide market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within process, grade, and application, highlighting their respective contributions to overall market performance.

By process, the indirect subsegment dominated the market in 2025, because it produces high-purity zinc oxide, which is essential for rubber, pharmaceuticals, and cosmetics. It ensures uniform particle size and better performance consistency, which industries require for quality-critical applications. Even though it is costlier than direct process, its product reliability and compliance with strict standards make it the preferred choice.

Based on grade, the standard subsegment dominated the market in 2025 due to its massive use in bulk manufacturing industries, especially rubber, ceramics, and paints. It offers a cost-effective balance between purity and performance, making it suitable for high-volume consumption. Industries prefer it because it is easily available and economically viable compared to high-purity grades.

On the basis of application, the rubber subsegment dominated the market in 2025, because zinc oxide is a key activator in vulcanization, which is essential for tire production. The global expansion of automotive and tire manufacturing directly drives demand. It improves strength, durability, and heat resistance of rubber products, making it irreplaceable. Continuous growth in mobility, logistics, and EV tires further strengthens its dominance.

GCC Zinc Oxide Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 157.3 Million

Market Size by 2033

US$ 228.5 Million

CAGR (2026 - 2033)

4.8%

Historical Data

2022-2024

Forecast period

2026-2033

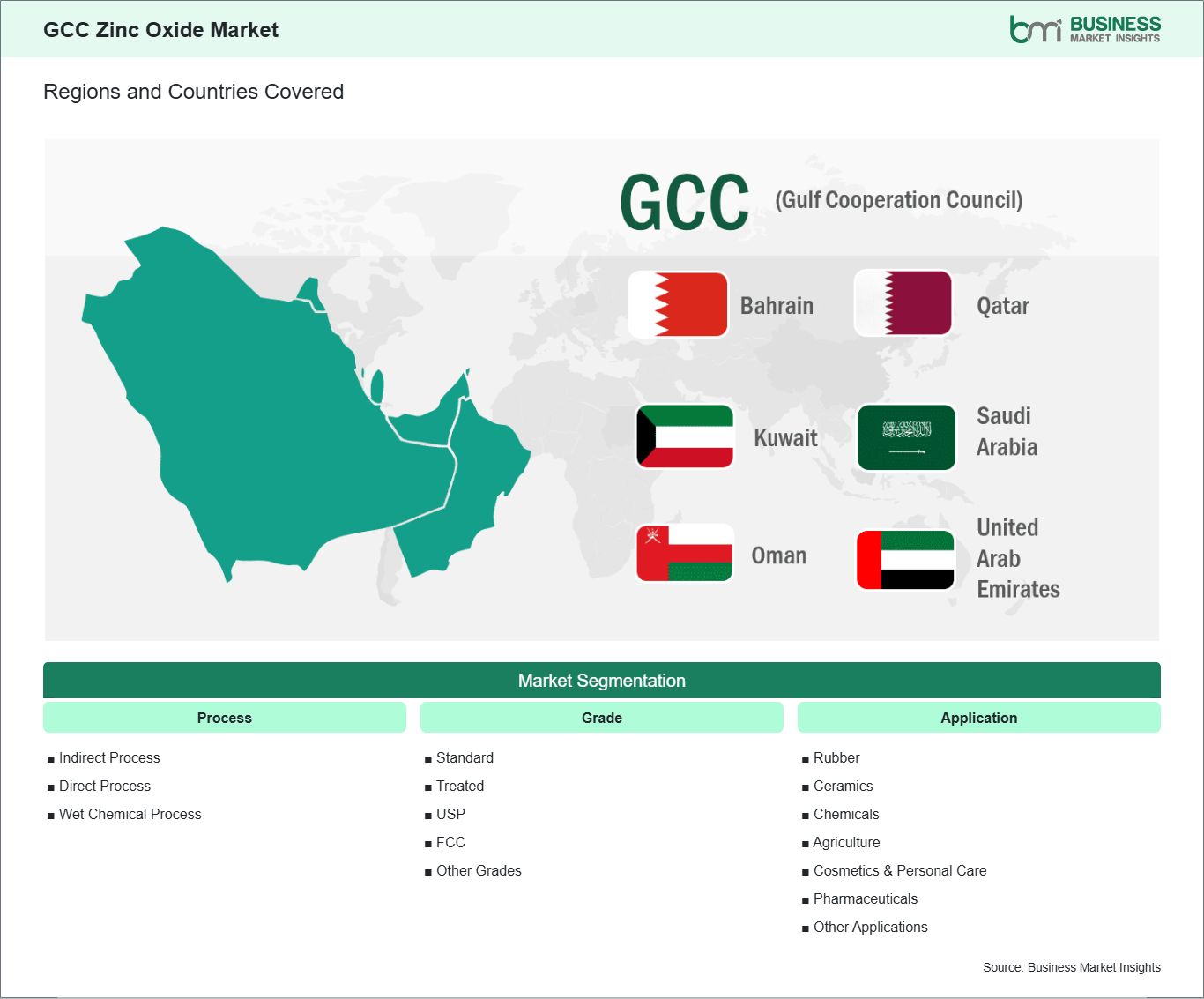

Segments Covered

By Process

Indirect Process

Direct Process

Wet Chemical Process

By Grade

Standard

Treated

USP

FCC

Other Grades

By Application

Rubber

Ceramics

Chemicals

Agriculture

Cosmetics & Personal Care

Pharmaceuticals

Other Applications

Regions and Countries Covered

GCC

UAE, Bahrain, Saudi Arabia, Oman, Qatar, Kuwait

Market leaders and key company profiles

Everzinc

Lanxess

JG Chemicals Limited

Akrochem Corporation

Pan-Continental Chemical Co., Ltd.

RUBAMIN

GRILLO-Werke AG

Grupo PROMAX

Zhiyi Zinc Industry Co.

Bruggemann

Get more information on this report

GCC Zinc Oxide Market Report Coverage and Deliverables:

The "GCC Zinc Oxide Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at regional and country levels for all market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Market concentration, heat map analysis, prominent players, and recent developments for the Market

Detailed company profiles, including SWOT analysis

GCC Zinc Oxide Market Geographic Insights:

The geographical scope of the GCC Zinc oxide market report is divided into: Saudi Arabia, the UAE, Qatar, Kuwait, Bahrain, and Oman. Saudi Arabia held the largest share in 2025.

Saudi Arabia is the dominant market for zinc oxide in the GCC region, thanks to its well-developed industrial base, integration with petrochemicals, and efforts towards non-oil economic diversification. The industrialization strategy adopted by Saudi Arabia has resulted in an increase in downstream industries like rubber, building material production, paints, ceramics, and specialty chemicals that are end users of zinc oxide. One of the key reasons for the use of zinc oxide in Saudi Arabia is the construction industry. Big urban development programs, smart cities, and industrial zones need high-quality coatings and sealants that utilize zinc oxide because of its ability to prevent corrosion and enhance durability. The construction of buildings and other facilities also drives the use of ceramic tiles and glass products containing zinc oxide. The automobile industry and the industrial manufacturing sector are also becoming significant players. Though the country does not have much involvement in the manufacture of automobiles, there has been an increasing trend in automobile assembly, components manufacturing, and maintenance facilities. Zinc oxide is extensively utilized in rubber-based products like tires, belts, hoses, and industrial gaskets to support logistics, transport, and heavy equipment use in the growing industrial areas of the Kingdom. There is ample potential in the petrochemicals and specialty chemicals sector of Saudi Arabia as a base for downstream processing of zinc oxide. There are industrial cities like Jubail and Yanbu that allow clustering of chemical industries for both local consumption and export-oriented production. Increasing demands are being witnessed in the healthcare sector in the form of pharmaceuticals, cosmetics, and personal care products using zinc oxide in sunscreen lotions.

Get more information on this report

GCC Zinc Oxide Market Research Report Guidance:

The report includes qualitative and quantitative data in the GCC zinc oxide market across across process, grade, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the GCC zinc oxide market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the GCC zinc oxide market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the GCC zinc oxide market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover GCC zinc oxide market segments by across process, grade, application, geography across Saudi Arabia, the UAE, Qatar, Kuwait, Bahrain, and Oman. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the GCC zinc oxide market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

GCC Zinc Oxide Market News and Key Development:

The GCC zinc oxide market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the GCC zinc oxide market are:

In March 2024, Gulf Fluor (UAE) announced that it expanded its specialty inorganic chemicals portfolio, including zinc-based compounds used in rubber, ceramics, and coatings applications, to strengthen supply capabilities for industrial customers across the GCC region.

In July 2023, Ma'aden (Saudi Arabian Mining Company) announced that it was progressing downstream diversification initiatives focused on zinc value-added products, including zinc oxide feedstock integration as part of its broader zinc supply chain development strategy in Saudi Arabia.

Key Sources Referred:

Environmental Protection Agency (EPA)Food and Drug Administration (FDA)European Chemicals Agency (ECHA)International Zinc Association (IZA)United Nations Environment Programme (UNEP)Occupational Safety and Health Administration (OSHA)Central Pollution Control Board (CPCB)S. Energy Information Administration (EIA)European Chemical Industry Council (Cefic)Medicines and Healthcare products Regulatory Agency (MHRA)Company WebsitesCompany Annual ReportsCompany Investor Presentation

Identical Market Reports with other Region/Countries

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the GCC Zinc Oxide Market?

The GCC Zinc Oxide Market is valued at US$ 157.3 Million in 2025, it is projected to reach US$ 228.5 Million by 2033.

What is the CAGR for GCC Zinc Oxide Market by (2026 - 2033)?

As per our report GCC Zinc Oxide Market, the market size is valued at US$ 157.3 Million in 2025, projecting it to reach US$ 228.5 Million by 2033. This translates to a CAGR of approximately 4.8% during the forecast period.

What segments are covered in this report?

The GCC Zinc Oxide Market report typically cover these key segments-

Process (Indirect Process, Direct Process, Wet Chemical Process)

Grade (Standard, Treated, USP, FCC, Other Grades)

Application (Rubber, Ceramics, Chemicals, Agriculture, Cosmetics & Personal Care, Pharmaceuticals, Other Applications)

What is the historic period, base year, and forecast period taken for GCC Zinc Oxide Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the GCC Zinc Oxide Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in GCC Zinc Oxide Market?

The GCC Zinc Oxide Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Everzinc

Lanxess

JG Chemicals Limited

Akrochem Corporation

Pan-Continental Chemical Co., Ltd.

RUBAMIN

GRILLO-Werke AG

Grupo PROMAX

Zhiyi Zinc Industry Co.,

Bruggemann

Who should buy this report?

The GCC Zinc Oxide Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the GCC Zinc Oxide Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For GCC Zinc Oxide Market

Get Free Sample For GCC Zinc Oxide Market