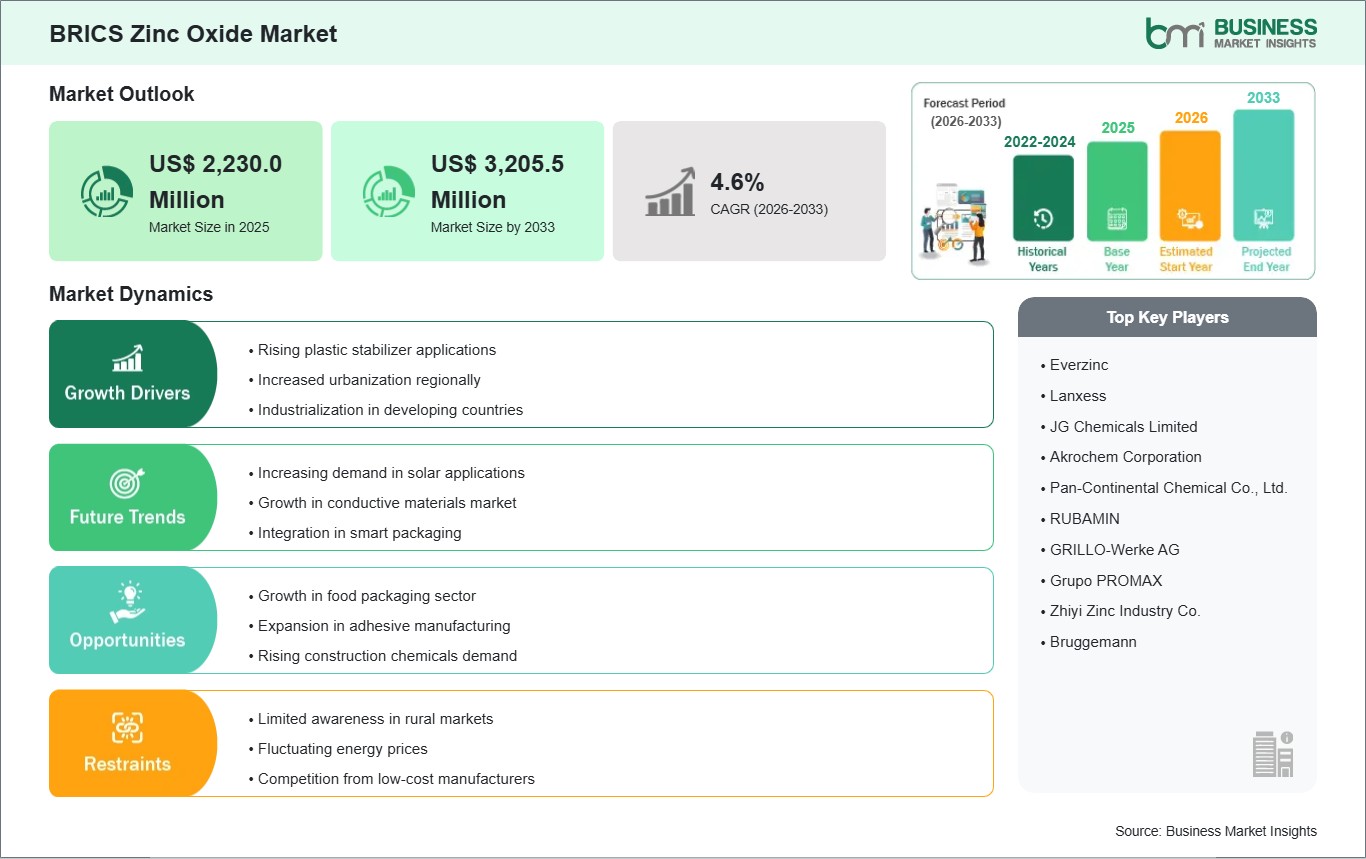

The BRICS zinc oxide market size is expected to reach US$ 3,205.5 million by 2033 from US$ 2,230.0 million in 2025. The market is estimated to record a CAGR of 4.6% from 2026 to 2033.

Executive Summary and BRICS Zinc Oxide Market Analysis:

BRICS zinc oxide market dynamics include extensive industrialization, increased production of automobiles, high investments in infrastructure development, and the availability of downstream manufacturing industries. The use of zinc oxide in BRICS countries is mainly driven by rubber industry, tires, ceramic manufacturing, chemicals, paints and coatings, pharmaceuticals, electronics, and animal feed industry. Overall, the region acts as one of the largest consumers of zinc oxide owing to its diversified manufacturing industries. There is a trend toward the use of high purity and specialized grade zinc oxide in the BRICS market, especially in the pharmaceutical, electronic, cosmetic, and advanced rubber industries. Process modernization and energy efficient production processes are being pursued to enhance product quality and address emerging environmental issues. Moreover, increased domestic manufacturing trends within BRICS countries are promoting the procurement of industrial intermediates locally, hence favoring the production of zinc oxide within BRICS. Some of the factors limiting the growth of the BRICS zinc oxide market include the volatility of zinc raw materials, environmental compliance, and energy intensive production processes. Increased regulation of industrial emissions and hazardous waste management adds cost pressures, especially for small and medium size producers. Infrastructure inadequacies and fluctuations in industrial demand cycles in some BRICS economies contribute to supply-demand imbalances at times. Nevertheless, favorable industrial conditions, growing manufacturing capacity, and increasing demand for zinc oxide in specialty chemical applications continue to support the BRICS zinc oxide market.

BRICS Zinc Oxide Market - Strategic Insights:

Get more information on this report

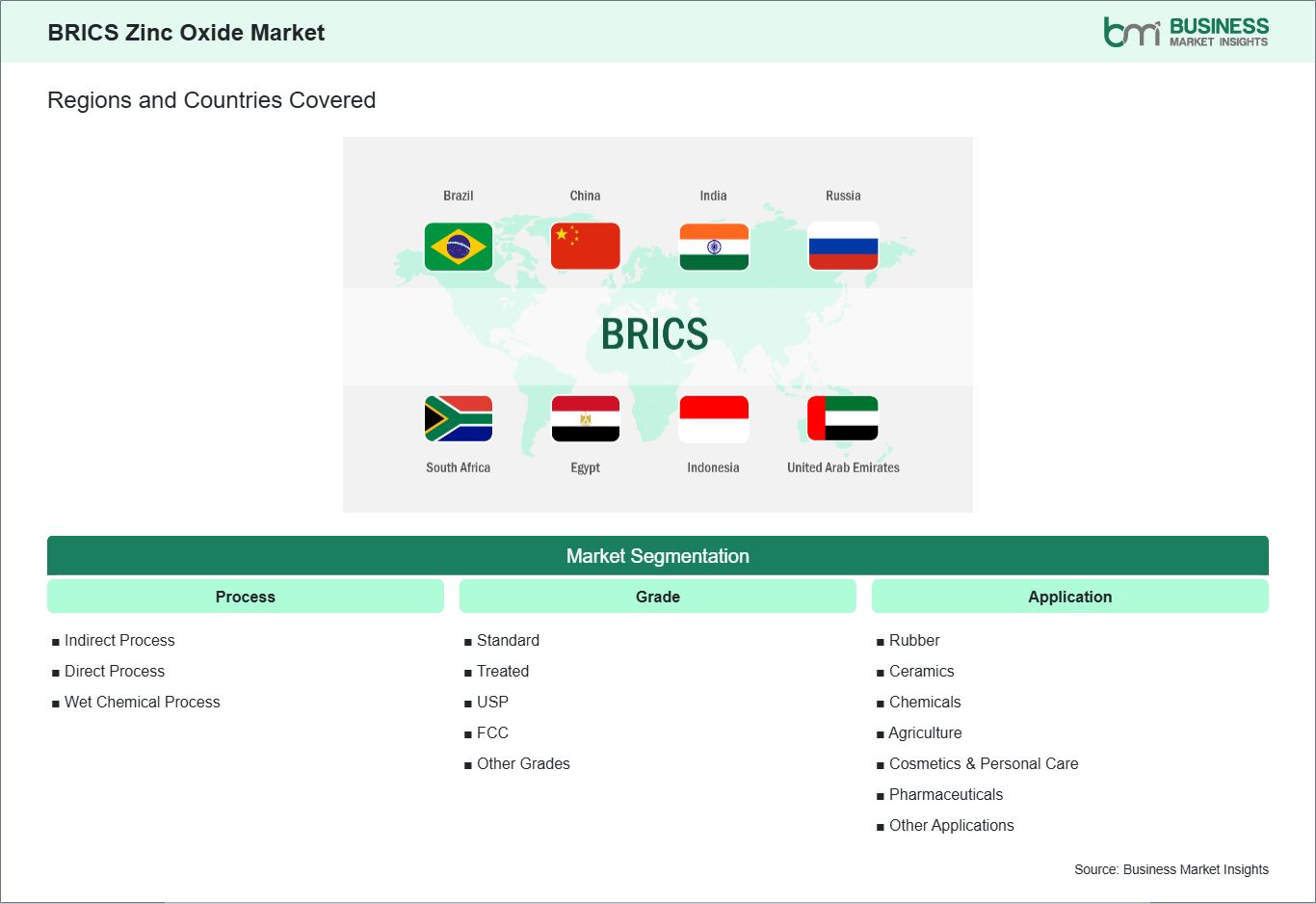

BRICS Zinc Oxide Market Segmentation Analysis:

Key segments that contributed to the derivation of the BRICS Zinc oxide market analysis are process, grade, and application.

By process, the zinc oxide market is segmented into Indirect process, direct process, and wet chemical process. The indirect process segment dominated the market in 2025.

Based on grade, the zinc oxide market is segmented into standard, treated, USP, FCC, and other grades. The standard segment dominated the market in 2025.

On the basis of application, the zinc oxide market is classified into rubber, ceramics, chemicals, agriculture, cosmetics & personal care, pharmaceuticals, and other applications. The rubber segment dominated the market in 2025.

BRICS Zinc Oxide Market Drivers and Opportunities:

Rising Plastic Stabilizer Applications

The market for zinc oxide in BRICS nations is growing fast due to increased usage in plastic stabilization, especially in countries like China, India, Brazil, Russia, and South Africa, where plastic production and the subsequent plastic processing industries are growing at a quick pace. Zinc oxide is being used in plastics such as PVC, polyethylene, and engineering plastics as a heat stabilizer, UV absorber, and process aid. Over 60 million tonnes of plastic are produced in China per year, and zinc oxide is being used increasingly in flexible packaging, interior auto parts, and construction plastics that need to withstand heat and sun exposure.

In Brazil and Russia, the rise in packaging and agriculture plastics has further boosted demand. In Brazil, agricultural films that are used in the production of soybeans and grains require more of the zinc oxide-based stabilizers to increase durability due to intense exposure to ultraviolet light. The same case applies to the use of zinc compounds in cables and plastic parts for increased fire resistance and mechanical stability in the Russian polymer processing industry.

The trend towards higher performance and longer-lasting plastics has led to an increase in the usage of zinc oxide among BRICS nations. This is because manufacturers are increasingly replacing the use of lead-based stabilizers, which are environmentally hazardous, with zinc oxide. The adoption of this substance has been fueled by the implementation of stringent polymer safety standards in countries such as China and India. With the anticipated rise in plastics manufacturing among BRICS nations, there will be continued demand for zinc oxide in stabilization.

Growth in Food Packaging Sector

Zinc oxide consumption within the BRICS countries is also growing owing to its use in the packaging sector due to the urbanization trend, increase in online shopping, and consumption of packaged food products. The reason behind the adoption of zinc oxide in the production of food-grade packaging is because of its properties such as being an antimicrobial agent, ultraviolet blocker, and barrier enhancer that increase the shelf-life of food products and ensure their safety. India and China are two countries where most of the packaged food products are consumed, with India's packaged food market worth more than hundreds of billions annually.

Market expansion is further facilitated by food export companies operating in Brazil and Russia. Brazil has a major export industry in meats, dairy products, and agriculture, which utilizes high-performance packaging films and containers to maintain food quality when shipped over long distances. The use of packaging material containing zinc oxide makes food safer by decreasing microbial contamination as well as protecting the product from moisture and oxygen penetration. In Russia, the rise in the demand for processed and frozen foods has led to the use of multilayer films and coatings, which include zinc oxide.

The same trends are prevalent in South Africa as well, especially in packaged drinks, dairy products, and ready-to-eat meals. The increasing modernization of retailing and the proliferation of supermarkets are pushing the adoption of extended shelf life packaging options. In BRICS, increased food safety legislation and rising consumer awareness regarding hygiene have been fueling the trend towards adopting functional packaging materials. Zinc oxide is gaining popularity in the manufacture of polymer films, paper coating, and food packages owing to its antimicrobial nature and regulatory compliance in appropriate doses. With the increasing consumption of packaged foods in developing countries, zinc oxide in food packaging will experience robust demand.

BRICS Zinc Oxide Market Size and Share Analysis:

The BRICS zinc oxide market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within process, grade, and application, highlighting their respective contributions to overall market performance.

By process, the indirect subsegment dominated the market in 2025, because it produces high-purity zinc oxide, which is essential for rubber, pharmaceuticals, and cosmetics. It ensures uniform particle size and better performance consistency, which industries require for quality-critical applications. Even though it is costlier than direct process, its product reliability and compliance with strict standards make it the preferred choice.

Based on grade, the standard subsegment dominated the market in 2025 due to its massive use in bulk manufacturing industries, especially rubber, ceramics, and paints. It offers a cost-effective balance between purity and performance, making it suitable for high-volume consumption. Industries prefer it because it is easily available and economically viable compared to high-purity grades.

On the basis of application, the rubber subsegment dominated the market in 2025, because zinc oxide is a key activator in vulcanization, which is essential for tire production. The global expansion of automotive and tire manufacturing directly drives demand. It improves strength, durability, and heat resistance of rubber products, making it irreplaceable. Continuous growth in mobility, logistics, and EV tires further strengthens its dominance.

BRICS Zinc Oxide Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 2,230.0 Million

Market Size by 2033

US$ 3,205.5 Million

CAGR (2026 - 2033)

4.6%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Process

Indirect Process

Direct Process

Wet Chemical Process

By Grade

Standard

Treated

USP

FCC

Other Grades

By Application

Rubber

Ceramics

Chemicals

Agriculture

Cosmetics & Personal Care

Pharmaceuticals

Other Applications

Regions and Countries Covered

BRICS

Russia, Brazil, South Africa, India, China, Egypt, Indonesia, Saudi Arabia, United Arab Emirates

Market leaders and key company profiles

Everzinc

Lanxess

JG Chemicals Limited

Akrochem Corporation

Pan-Continental Chemical Co., Ltd.

RUBAMIN

GRILLO-Werke AG

Grupo PROMAX

Zhiyi Zinc Industry Co.

Bruggemann

Get more information on this report

BRICS Zinc Oxide Market Report Coverage and Deliverables:

The "BRICS Zinc Oxide Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at the regional and country levels for market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Market concentration, heat map analysis, prominent players, and recent developments for the Market

Detailed company profiles, including SWOT analysis

BRICS Zinc Oxide Market Geographic Insights:

The geographical scope of the BRICS zinc oxide market report is divided into: Russia, Brazil, South Africa, India, China, Egypt, Indonesia, Saudi Arabia, and the UAE. China held the largest share in 2025.

China is the main player in the BRICS zinc oxide industry owing to its well-developed manufacturing environment and efficient supply chain networks. China boasts of one of the largest zinc oxide production centers in the world, offering its output to various industries such as automotive tires, industrial rubber, ceramics, electronics, pharmaceuticals, paints, chemicals, and personal care products. The developed industrial structure and chemical processing facilities of China facilitate efficient manufacturing processes for commodity zinc oxide as well as high purity zinc oxide. The tire and rubber industries continue to dominate the market for zinc oxide in China. Provinces such as Shandong, Jiangsu, Zhejiang, and Guangdong have large numbers of tire makers, automobile parts companies, and rubber industries that depend on zinc oxide due to its properties such as vulcanization efficiency, heat resistance, and product longevity. China's export focus on automotive parts and rubber products is expected to continue influencing the demand trends for zinc oxide over time. There has also been increased demand for specialty zinc oxides in China, especially for the electronics, semiconductors, cosmetics, pharmaceuticals, and coatings industries. With the increase in electric vehicle production and electronics parts manufacturing, there has been growing interest in utilizing high purity and nanoscale zinc oxide in conductive material applications and UV protection technology. Moreover, skincare and pharmaceutical industries in China have been increasingly procuring high-grade zinc oxide for medicinal creams and sunscreens. Environmental regulation will be emerging as one of the key structural factors affecting the Chinese zinc oxide industry. The government is tightening its grip on the emissions from industries, as well as their energy usage and waste management. Manufacturers will have to modernize their technologies, and plants using outdated technology will be under threat of being consolidated by bigger players.

Get more information on this report

BRICS Zinc Oxide Market Research Report Guidance:

The report includes qualitative and quantitative data in the BRICS zinc oxide market across process, grade, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the BRICS zinc oxide market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the BRICS zinc oxide market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the BRICS zinc oxide market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the BRICS zinc oxide market segments by process, grade, application and geography across Russia, Brazil, South Africa, India, China, Egypt, Indonesia, Saudi Arabia, and the UAE. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the BRICS zinc oxide market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

BRICS Zinc Oxide Market News and Key Development:

The BRICS zinc oxide market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the BRICS zinc oxide market are:

In February 2024, Nexa Resources announced strong 2023 operational results, including continued zinc and zinc oxide sales across Brazil and Latin America, driven by higher ore processing and ramp-up activities at the Aripuana mine.

In December 2023, Nexa Resources announced that it had signed an agreement with Aperam BioEnergia to acquire 10,000 tons of bio-oil for use in zinc oxide production at its Tres Marias facility in Brazil, supporting decarbonization and sustainable manufacturing initiatives in the BRICS region.

Key Sources Referred:

Environmental Protection Agency (EPA)Food and Drug Administration (FDA)European Chemicals Agency (ECHA)International Zinc Association (IZA)United Nations Environment Programme (UNEP)Occupational Safety and Health Administration (OSHA)Central Pollution Control Board (CPCB)S. Energy Information Administration (EIA)European Chemical Industry Council (Cefic)Medicines and Healthcare products Regulatory Agency (MHRA)Company WebsitesCompany Annual ReportsCompany Investor Presentation

Identical Market Reports with other Region/Countries

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the BRICS Zinc Oxide Market?

The BRICS Zinc Oxide Market is valued at US$ 2,230.0 Million in 2025, it is projected to reach US$ 3,205.5 Million by 2033.

What is the CAGR for BRICS Zinc Oxide Market by (2026 - 2033)?

As per our report BRICS Zinc Oxide Market, the market size is valued at US$ 2,230.0 Million in 2025, projecting it to reach US$ 3,205.5 Million by 2033. This translates to a CAGR of approximately 4.6% during the forecast period.

What segments are covered in this report?

The BRICS Zinc Oxide Market report typically cover these key segments-

Process (Indirect Process, Direct Process, Wet Chemical Process)

Grade (Standard, Treated, USP, FCC, Other Grades)

Application (Rubber, Ceramics, Chemicals, Agriculture, Cosmetics & Personal Care, Pharmaceuticals, Other Applications)

What is the historic period, base year, and forecast period taken for BRICS Zinc Oxide Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the BRICS Zinc Oxide Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in BRICS Zinc Oxide Market?

The BRICS Zinc Oxide Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Everzinc

Lanxess

JG Chemicals Limited

Akrochem Corporation

Pan-Continental Chemical Co., Ltd.

RUBAMIN

GRILLO-Werke AG

Grupo PROMAX

Zhiyi Zinc Industry Co.,

Bruggemann

Who should buy this report?

The BRICS Zinc Oxide Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the BRICS Zinc Oxide Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For BRICS Zinc Oxide Market

Get Free Sample For BRICS Zinc Oxide Market