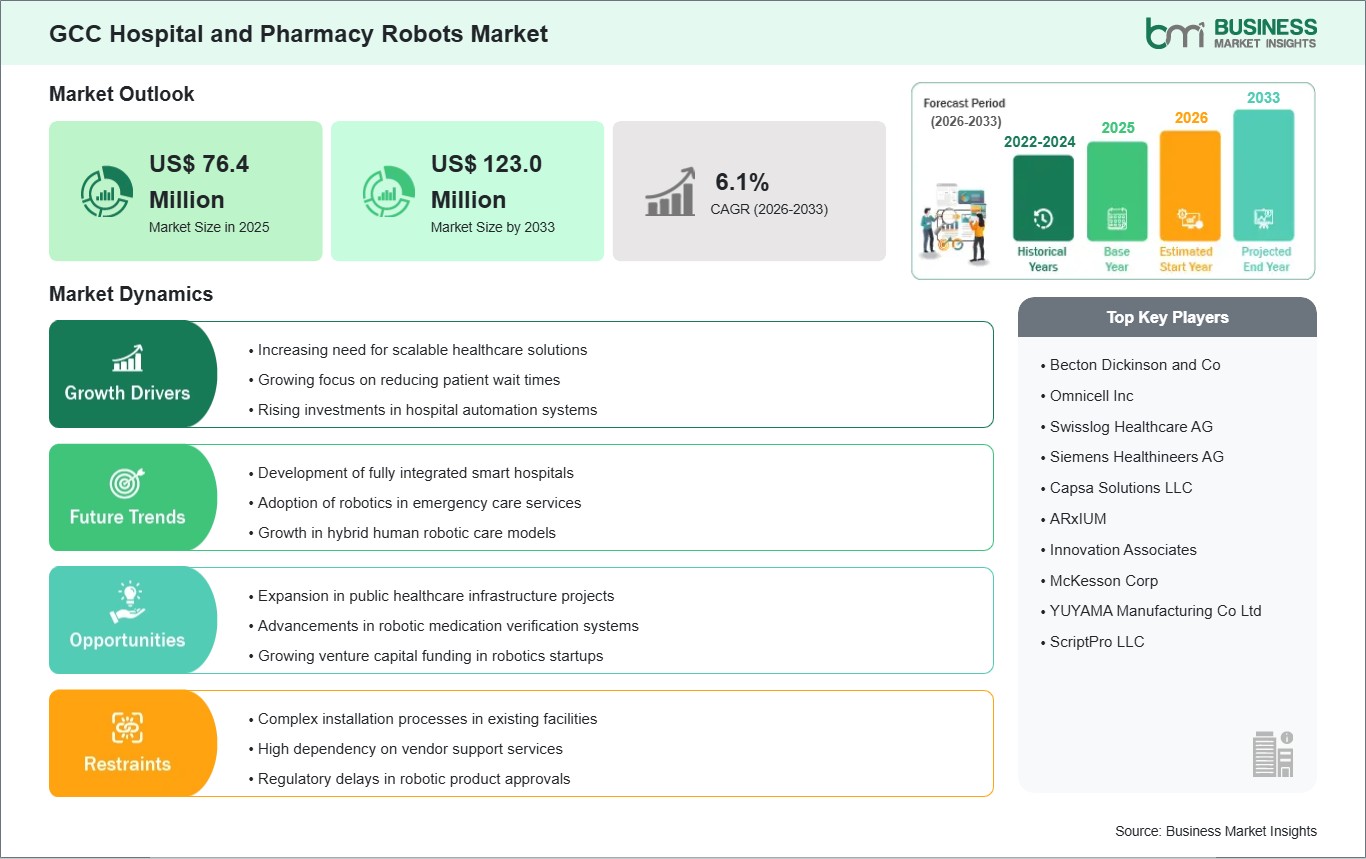

The GCC hospital and pharmacy robots market size is expected to reach US$123.0 million by 2033 from US$76.4 million in 2025. The market is estimated to record a CAGR of 6.1% from 2026 to 2033.

Executive Summary and GCC Hospital and Pharmacy Robots Market Analysis:

The GCC hospital and pharmacy robots market is emerging as a strategic component of healthcare modernization, driven by the region’s focus on operational excellence, patient safety, and digital transformation. Healthcare institutions across the United Arab Emirates, Saudi Arabia, Qatar, Kuwait, Oman, and Bahrain are increasingly adopting robotic systems to automate high-volume and repetitive pharmacy operations, such as medication sorting, compounding, labeling, and automated dispensing. The integration of robotics addresses challenges associated with manual errors, workforce shortages, and complex drug regimens, particularly in large urban hospitals and multi-hospital networks. Operational productivity remains a central driver in the GCC. Automated pharmacy systems enable hospitals to standardize processes, improve medication accuracy, and reduce turnaround times for inpatient and outpatient prescriptions. Robotics also facilitates high-density inventory management, allowing pharmacy teams to optimize stock rotation, track expiry dates, and maintain regulatory compliance. These improvements are particularly critical in tertiary care hospitals that handle high-risk medications, oncology therapies, and controlled substances. Healthcare digitalization in the GCC further enhances robotics adoption. Hospitals are connecting pharmacy robots to electronic prescription systems, hospital management platforms, and clinical decision-support software, creating a seamless ecosystem that improves prescription validation, inventory monitoring, and reporting. Automation also supports audit readiness, enabling real-time logging of medication dispensing activities and reducing compliance risks. The market is additionally shaped by demographic pressures and rising healthcare demand. Increasing patient volumes and multi-specialty treatments necessitate faster medication processing, while robotics reduces the physical burden on pharmacy staff. Autonomous mobile robots are increasingly deployed to transport medications and laboratory samples within hospital campuses, accelerating internal logistics and minimizing delays. The GCC hospital and pharmacy robots market is defined by high capital investment in healthcare technology, a strategic focus on workflow optimization, and a growing emphasis on patient-centric care. Robotics is rapidly becoming an essential tool for hospitals seeking to enhance operational efficiency, maintain medication accuracy, and support workforce productivity in a region experiencing both rapid healthcare expansion and technological modernization.

GCC Hospital and Pharmacy Robots Market - Strategic Insights:

Get more information on this report

GCC Hospital and Pharmacy Robots Market Segmentation Analysis:

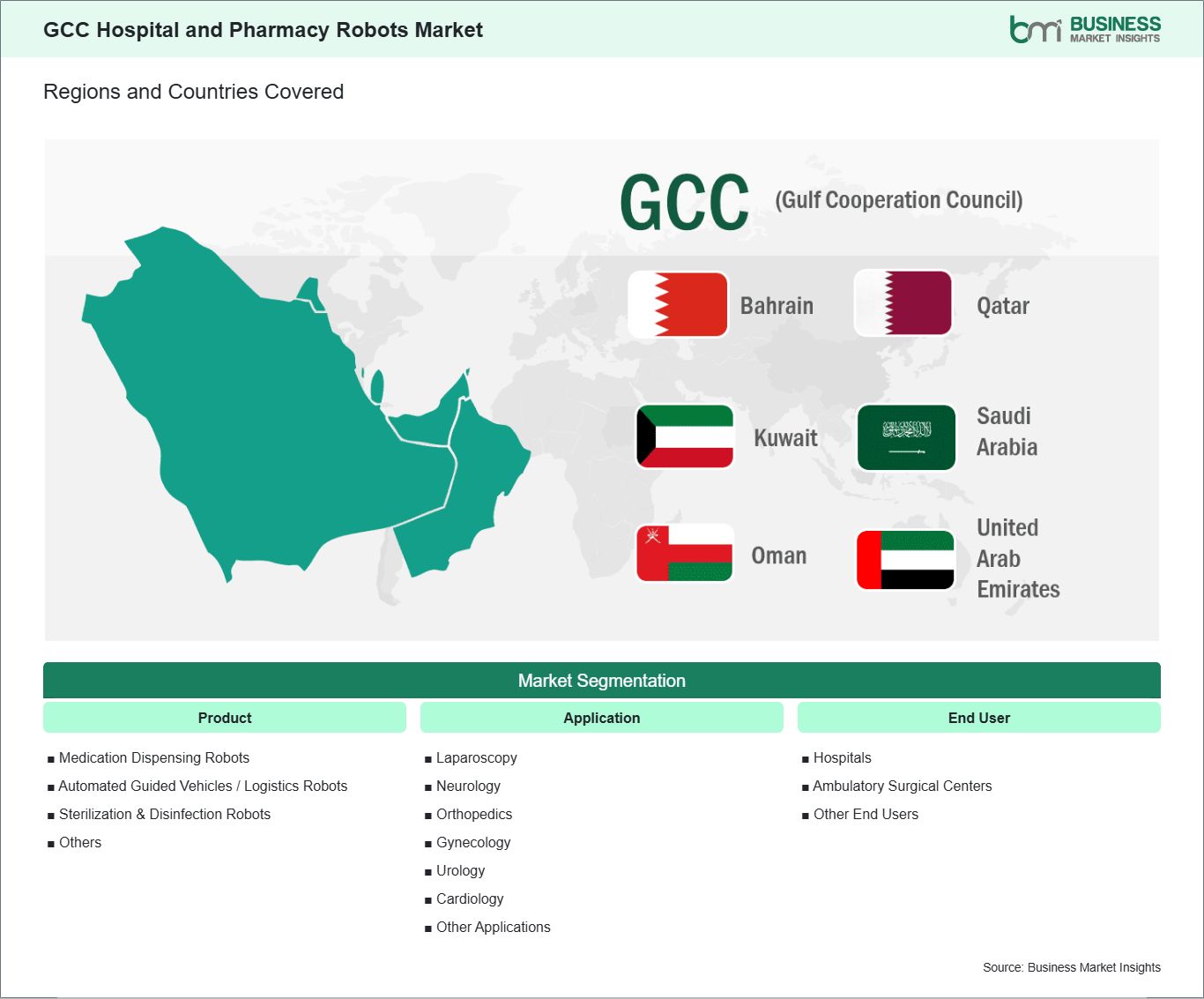

Key segments that contributed to the derivation of the GCC hospital and pharmacy robots market analysis are product, application, and end user.

By product, the hospital and pharmacy robots market is segmented into medication dispensing robots, automated guided vehicles (AGVs) / logistics robots, sterilization & disinfection robots and other products. The medication dispensing robots segment dominated the market in 2025.

In terms of application, the hospital and pharmacy robots market is categorized into laparoscopy, neurology, orthopedics, gynecology, urology, cardiology and other applications. The laparoscopy segment dominated the market in 2025.

Based on end user, the market is classified into hospitals, ambulatory surgical centers and other end users. The hospitals segment dominated the market in 2025.

GCC Hospital and Pharmacy Robots Market Drivers and Opportunities:

Expansion of smart hospital technologies

Across the GCC region, hospitals are actively embracing smart technologies as part of broader efforts to modernize healthcare delivery and improve service quality. Countries such as Saudi Arabia, the United Arab Emirates, and Qatar have launched national health transformation programs that emphasize digital infrastructure, patient‑centric care, and efficient clinical workflows. Within this context, smart hospital initiatives are driving interest in advanced automation solutions that can support hospital operations, elevate clinical services, and enhance patient experiences. Robotics—both in clinical settings and pharmacy operations—is increasingly viewed as a key enabler of these smart hospital strategies. In large tertiary care institutions throughout the GCC, administrators are exploring the integration of robotics into areas such as internal logistics, medication handling, and patient support services. Smart hospital environments are designed to leverage data, connectivity, and automation to reduce manual workload and improve operational responsiveness. For example, robotics can be deployed to transport medications, laboratory samples, and supplies across hospital corridors, which helps staff focus more on direct patient care. Investment in smart infrastructure such as wireless networks, IoT sensors, and centralized management systems creates a foundation that makes robotic deployment more practical and effective in complex hospital environments. Beyond operational advantages, the expansion of smart hospital technologies in the GCC also reflects broader healthcare goals tied to quality, safety, and reputation. Hospitals in the region are increasingly competing for regional and international patients, and demonstrating advanced capabilities—such as robotics‑enabled pharmacy automation—can enhance institutional standing. Smart hospitals that incorporate robotics into routine workflows are perceived as more forward‑looking and responsive to modern healthcare expectations. As healthcare systems across the GCC continue to invest in digital and smart technology frameworks, the role of hospital and pharmacy robots is expected to grow, supporting smarter, safer, and more efficient care delivery.

Integration of robotics with hospital IT

Integration of robotics with hospital information technology (IT) systems is emerging as a critical trend in the GCC hospital and pharmacy robots market. Hospitals in the region are investing heavily in comprehensive IT infrastructure—including electronic health records (EHR), pharmacy management systems, and enterprise resource planning (ERP) platforms—to centralize clinical data and streamline workflows. As these digital backbones mature, they create an environment where robotic systems can be seamlessly connected to existing hospital software, enabling data‑driven automation that enhances accuracy and operational coherence. In pharmacy departments across the GCC, robotic solutions are being integrated with digital prescribing and inventory management systems to support more reliable medication dispensing processes. Robotics that can communicate with pharmacy IT platforms help ensure that prescriptions are accurately interpreted, medication selections align with digital orders, and inventory levels are updated in real time. This level of connectivity replaces many traditional manual checks with automated verification, reducing the likelihood of discrepancies and supporting consistent medication delivery. For hospital administrators, integration between robotics and IT systems also provides better visibility into pharmacy performance metrics and operational trends, which can be used to optimize staffing and resource allocation. Beyond pharmacy operations, hospitals throughout the GCC are linking robotic systems with broader clinical and administrative IT tools. For example, robotics involved in logistics or patient support can be coordinated with bed management systems, clinical scheduling platforms, and communication networks to support more efficient hospital workflows. When robotics operate within an integrated IT ecosystem, hospitals can achieve synchronized task execution across departments, reduce delays caused by manual handoffs, and improve the overall responsiveness of care teams. As GCC healthcare providers continue to enhance their digital architectures, the integration of robotics with hospital IT is expected to accelerate, bringing more cohesive, data‑rich, and efficient automation to clinical and pharmacy environments alike.

GCC Hospital and Pharmacy Robots Market Size and Share Analysis:

The GCC hospital and pharmacy robots market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

By product, the medication dispensing robots subsegment dominated the market in 2025, driven by the push to enhance pharmacy efficiency and ensure precise medication management in high-demand healthcare settings.

In terms of application, the laparoscopy subsegment dominated the market in 2025, driven by the rising adoption of minimally invasive robotic surgeries that improve accuracy and reduce recovery time.

Based on end user, the hospitals subsegment dominated the market in 2025, driven by the high patient throughput and the need for advanced automation to optimize clinical operations and patient care.

GCC Hospital and Pharmacy Robots Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 76.4 Million

Market Size by 2033

US$ 123.0 Million

CAGR (2026 - 2033)

6.1%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Medication Dispensing Robots

Automated Guided Vehicles / Logistics Robots

Sterilization & Disinfection Robots

Others

By Application

Laparoscopy

Neurology

Orthopedics

Gynecology

Urology

Cardiology

Other Applications

By End User

Hospitals

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

GCC

UAE, Bahrain, Saudi Arabia, Oman, Qatar, Kuwait

Market leaders and key company profiles

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Get more information on this report

GCC Hospital and Pharmacy Robots Market Report Coverage and Deliverables:

The "GCC Hospital and Pharmacy Robots Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

GCC Hospital and Pharmacy Robots Market size and forecast at regional and country levels for all segments covered under the scope

GCC Hospital and Pharmacy Robots Market trends, as well as drivers, restraints, and opportunities

GCC Hospital and Pharmacy Robots Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the GCC Hospital and Pharmacy Robots Market

Detailed company profiles, including SWOT analysis

GCC Hospital and Pharmacy Robots Market Geographic Insights:

The geographical scope of the GCC Hospital and Pharmacy Robots Market report is divided into UAE, Bahrain, Saudi Arabia, Oman, Qatar, and Kuwait. UAE held the largest share in 2025.

Country-level insights in the GCC hospital and pharmacy robots market reveal a diverse adoption landscape shaped by healthcare infrastructure, government investment, and technological readiness. The United Arab Emirates emerges as the dominant market, driven by its advanced healthcare infrastructure, high adoption of digital health systems, and strategic investments in hospital automation. Hospitals in the UAE widely implement robotic pharmacy systems for automated dispensing, sterile compounding, and inventory management. In addition, autonomous mobile robots are deployed for internal logistics, transporting medications, laboratory samples, and medical supplies across hospital departments. Integration with electronic health records and hospital management platforms enables real-time inventory monitoring, prescription verification, and compliance with regulatory standards, making UAE hospitals leaders in operational efficiency and patient safety. Saudi Arabia represents a strong and rapidly growing market, with robotics adoption driven by Vision 2030 initiatives and extensive investment in modern healthcare infrastructure. Hospitals in urban centers are deploying automated pharmacy solutions to improve prescription accuracy, streamline workflows, and reduce staff workload. Multi-hospital networks are increasingly investing in scalable and modular robotic platforms to meet growing patient demand and enhance operational efficiency. Qatar and Kuwait are emerging markets where adoption is primarily concentrated in tertiary and academic hospitals. These countries are piloting robotic dispensing and inventory management systems to reduce human error, optimize pharmacy workflows, and enhance patient safety. Autonomous mobile robots are also being tested for internal logistics to accelerate medication delivery within hospital facilities. Oman and Bahrain are in the early stages of robotics adoption, focusing on select private hospitals and academic medical centers. Investment is centered on automated dispensing units, compounding systems, and inventory optimization tools to improve pharmacy efficiency and reduce medication errors. These countries are gradually integrating robotics with hospital management systems to support operational transparency and compliance. Across the GCC, hospitals are increasingly viewing robotics as a strategic solution for workforce optimization, operational efficiency, and patient safety. Adoption trends reflect a mix of large-scale deployment in the UAE, rapid modernization in Saudi Arabia, emerging pilot programs in Qatar and Kuwait, and early-stage adoption in Oman and Bahrain. The GCC hospital and pharmacy robots market is dominated by the UAE, while Saudi Arabia and Qatar represent high-growth potential, and Kuwait, Oman, and Bahrain are emerging markets. The region’s strong focus on technological innovation, operational optimization, and modern healthcare infrastructure ensures continued expansion of robotic solutions in hospital pharmacy operations.

Get more information on this report

GCC Hospital and Pharmacy Robots Market Research Report Guidance:

The report includes qualitative and quantitative data in the GCC Hospital and Pharmacy Robots Market across product, application, end user and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the GCC Hospital and Pharmacy Robots Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the GCC Hospital and Pharmacy Robots Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the GCC Hospital and Pharmacy Robots Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover GCC Hospital and Pharmacy Robots Market segments by product, application, end user, and geography across UAE, Bahrain, Saudi Arabia, Oman, Qatar, and Kuwait. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the GCC Hospital and Pharmacy Robots Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

GCC Hospital and Pharmacy Robots Market News and Key Development:

The GCC Hospital and Pharmacy Robots Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the GCC hospital and pharmacy robots market are:

In August 2025, Aster Al Raffah Hospitals & Clinics in Oman launched the Aster Al Raffah Walk Again Advanced Robotic Rehabilitation Centre in Muscat, featuring state‑of‑the‑art robotic technologies such as Cyberdyne HAL (robotic exoskeleton), Recoverix Pro (brain‑computer interface rehabilitation), Vibramoov, Luna EMG, and Meissa OT to support neuro‑rehabilitation for stroke, spinal injuries, cerebral palsy and other mobility impairments. This centre is one of the first of its kind in the GCC, bringing advanced robotic‑assisted rehabilitation care close to patients. It aims to reduce the need for patients to travel abroad for high‑tech recovery solutions and strengthens Oman’s healthcare technology profile. The facility also supports research and multidisciplinary clinical practice for complex neurological conditions.

In January 2024, American Hospital Dubai launched the Center for Surgical Simulation, Robotics and Artificial Intelligence a specialised training and deployment hub for advanced robotic systems, including the Da Vinci Xi surgical robot, ROSA Knee System, CMR Surgical’s Versius robot, and Mazor X Stealth Edition for spinal procedures. These global robotic systems are increasingly used in complex surgical cases such as orthopaedics, spinal surgery, and general surgery, supporting skill development for GCC surgeons.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the GCC Hospital and Pharmacy Robots Market?

The GCC Hospital and Pharmacy Robots Market is valued at US$ 76.4 Million in 2025, it is projected to reach US$ 123.0 Million by 2033.

What is the CAGR for GCC Hospital and Pharmacy Robots Market by (2026 - 2033)?

As per our report GCC Hospital and Pharmacy Robots Market, the market size is valued at US$ 76.4 Million in 2025, projecting it to reach US$ 123.0 Million by 2033. This translates to a CAGR of approximately 6.1% during the forecast period.

What segments are covered in this report?

The GCC Hospital and Pharmacy Robots Market report typically cover these key segments-

Application (Laparoscopy, Neurology, Orthopedics, Gynecology, Urology, Cardiology, Other Applications)

End User (Hospitals, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for GCC Hospital and Pharmacy Robots Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the GCC Hospital and Pharmacy Robots Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in GCC Hospital and Pharmacy Robots Market?

The GCC Hospital and Pharmacy Robots Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Who should buy this report?

The GCC Hospital and Pharmacy Robots Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the GCC Hospital and Pharmacy Robots Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For GCC Hospital and Pharmacy Robots Market

Get Free Sample For GCC Hospital and Pharmacy Robots Market