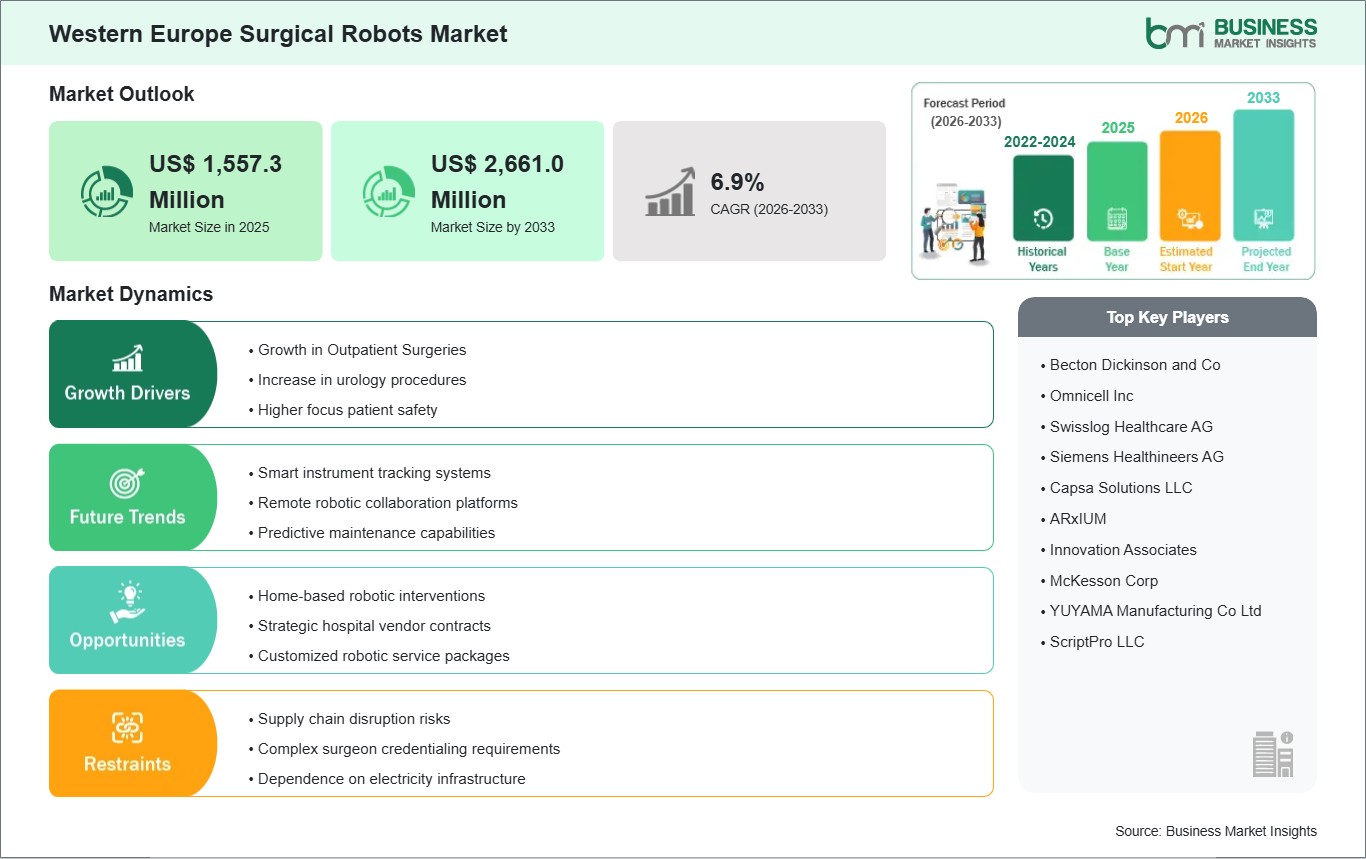

The Western Europe Surgical Robots Market size is expected to reach US$ 2,661.0 million by 2033 from US$ 1,557.3 million in 2025. The market is estimated to record a CAGR of 6.9% from 2026 to 2033.

Executive Summary and Western Europe Surgical Robots Market Analysis:

The Western Europe surgical robots market is witnessing strategic growth driven by an emphasis on precision medicine, minimally invasive procedures, and hospital modernization initiatives. Adoption is largely concentrated in tertiary care hospitals, university medical centers, and specialty private clinics that perform high volumes of complex surgical procedures. The market is propelled by rising patient expectations for minimally invasive interventions, increasing procedural complexity in urology, gynecology, cardiothoracic, and oncological surgeries, and the need to enhance clinical outcomes while optimizing operational efficiency. Key drivers include technological advancements in robotic-assisted systems, integration with high-resolution imaging, and alignment with digital health infrastructure, which collectively improve surgical accuracy and support data-driven decision-making.

Hospitals are increasingly evaluating robotic systems based on multispecialty applicability, workflow efficiency, and postoperative outcome improvement, rather than purely on cost. Regulatory oversight in Western Europe ensures clinical efficacy and safety, which strengthens institutional confidence in robotics. Public and private hospitals adopt differentiated strategies: public institutions prioritize systems with long-term cost-effectiveness and broad clinical applications, whereas private hospitals focus on patient experience, service differentiation, and attracting international medical tourists. Barriers to adoption include the high upfront capital requirement, the need for specialized surgical training, and variability in reimbursement policies. Additionally, hospitals consider compatibility with existing hospital information systems, integration with surgical planning software, and the ability to collect outcome-based data for quality assessment. Overall, Western Europe represents a technologically mature and strategically evolving market where robotics adoption is shaped by clinical excellence, operational optimization, and competitive positioning in a highly regulated healthcare environment.

Western Europe Surgical Robots Market - Strategic Insights:

Get more information on this report

Western Europe Surgical Robots Market Segmentation Analysis:

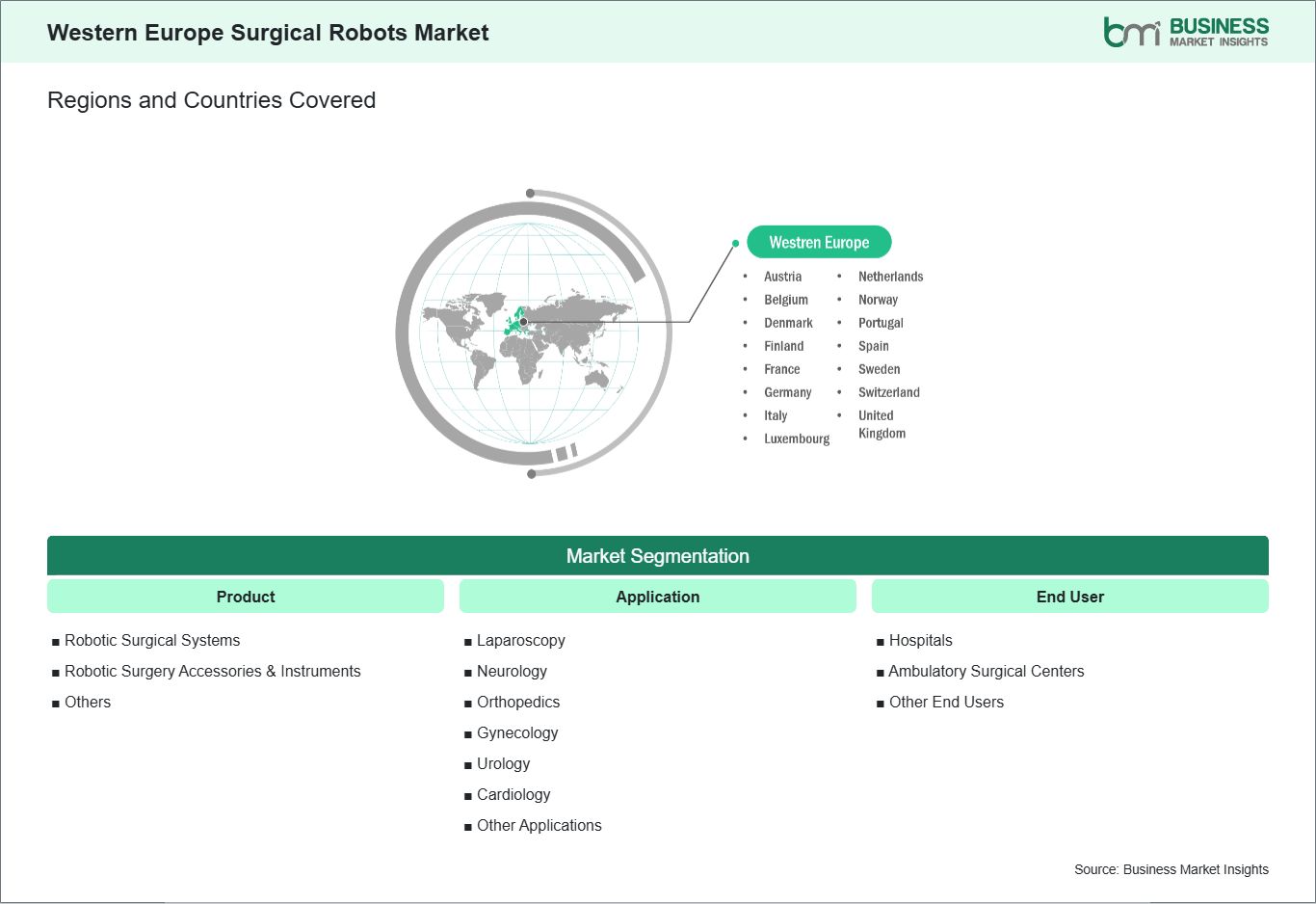

Key segments that contributed to the derivation of the Western Europe Surgical Robots Market analysis are product, application, and end user.

By product, the surgical robots market is segmented into robotic surgical systems, robotic surgery accessories & instruments, and others. The robotic surgery accessories & instruments segment dominated the market in 2025.

In terms of application, the surgical robots market is categorized into laparoscopy, neurology, orthopedics, gynecology, urology, cardiology, and other applications. The laparoscopy segment dominated the market in 2025.

Based on end user, the surgical robots market is classified into hospitals, ambulatory surgical centers, and other end users. The hospitals segment dominated the market in 2025.

Western Europe Surgical Robots Market Drivers and Opportunities:

Growth in Outpatient Surgeries

Healthcare systems in countries such as Germany, France, the Netherlands, Spain, and Belgium are increasingly shifting surgical procedures out of traditional inpatient settings and into dedicated outpatient or day‑surgery units. This transition reflects payer and provider priorities to optimize bed utilization, reduce hospital costs, and improve patient experience. Robotic systems are being evaluated and adopted specifically for procedures that can be safely performed without overnight stays, such as select hernia repairs, hysterectomies, and prostatectomies. Hospitals and specialized surgical centers in metropolitan regions—such as Berlin, Paris, Amsterdam, and Barcelona—are leading pilots of robotics‑enabled outpatient programs. These facilities are configuring operating theatres to accommodate compact robotic platforms that facilitate minimally invasive access, precise instrument control, and quicker recovery, all of which support discharge on the same day.

Surgeons and perioperative teams report that robotics helps reduce operative trauma and postoperative pain, making it easier to meet clinical criteria for outpatient release. Patient demand is also accelerating uptake, as individuals in Western European countries become more informed about the benefits of outpatient surgical options. Public health insurance schemes in nations such as France and the Netherlands are incentivizing value‑based care, supporting broader adoption of robotics for outpatient procedures. As protocols mature and clinical evidence grows, robotics is increasingly becoming a strategic enabler of outpatient surgical expansion in Western Europe, supporting efficiency and high standards of surgical quality.

Home-based robotic interventions

Pilot programs in countries such as Sweden, Denmark, the UK, and Switzerland are exploring how robotics can support remote procedural assistance, rehabilitation, and follow‑up care delivered at or near the patient's home. These initiatives reflect broader regional priorities to reduce hospital congestion and extend care continuity beyond traditional clinical settings. In the UK, some research institutions are evaluating how robotic systems can assist clinicians in guiding minor interventions or procedural support remotely. This includes technologies that combine teleoperation with real‑time imaging and communication tools, enabling specialists to advise or collaborate on procedures without requiring patients to travel to large urban hospitals. Such approaches are seen as especially valuable for rural populations in Scotland and Wales, where access to specialist surgical care can be constrained by distance.

Meanwhile, rehabilitation and follow‑up care supported by robotic devices are emerging in Sweden and Denmark as complementary components of home‑based intervention strategies. Robotic systems designed for physical therapy and motor function support help patients recover postoperatively in their own environments, reducing readmissions and supporting long‑term functional improvement. These technologies are being integrated with regional telehealth services and physiotherapy programs to improve accessibility and continuity of care. Thus, evolving regulatory frameworks and reimbursement models support home‑centered robotics in Western Europe.

Western Europe Surgical Robots Market Size and Share Analysis:

The Western Europe Surgical Robots Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

By product, the robotic surgery accessories & instruments segment dominated the market in 2025, driven by the recurring and high replacement demand for consumable, procedure‑specific tools required in every robotic surgery, which must be regularly procured as surgical volumes increase.

In terms of application, the laparoscopy segment dominated the market in 2025, driven by the strong adoption of minimally invasive laparoscopic robotic procedures in Western Europe, due to enhanced precision, reduced recovery times, and growing surgeon preference for MIS techniques.

Based on end user, the hospitals segment dominated the market in 2025, driven by their advanced healthcare infrastructure, high surgical volumes, financial capacity to invest in cutting‑edge robotic systems, and access to skilled surgical teams that maximize technology utilization.

Western Europe Surgical Robots Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 1,557.3 Million

Market Size by 2033

US$ 2,661.0 Million

CAGR (2026 - 2033)

6.9%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Robotic Surgical Systems

Robotic Surgery Accessories & Instruments

Others

By Application

Laparoscopy

Neurology

Orthopedics

Gynecology

Urology

Cardiology

Other Applications

By End User

Hospitals

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

Western Europe

Belgium, the Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, the United Kingdom, Denmark, Portugal, Norway, Finland

Market leaders and key company profiles

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Get more information on this report

Western Europe Surgical Robots Market Report Coverage and Deliverables:

The "Western Europe Surgical Robots Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Western Europe Surgical Robots Market size and forecast at regional and country levels for all market segments covered under the scope

Western Europe Surgical Robots Market trends, as well as drivers, restraints, and opportunities

Western Europe Surgical Robots Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Western Europe Surgical Robots Market

Detailed company profiles, including SWOT analysis

Western Europe Surgical Robots Market Geographic Insights:

The geographical scope of the Western Europe Surgical Robots Market report is divided into Belgium, the Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, the UK, Denmark, Portugal, Norway, and Finland. Germany held the largest share in 2025.

Country-level adoption patterns in Western Europe reveal significant heterogeneity influenced by healthcare system structure, reimbursement frameworks, and hospital modernization strategies. Germany leads regional deployment, with high-volume tertiary hospitals and university medical centers integrating robotic systems across urology, oncology, and cardiothoracic surgery to improve outcomes and procedural efficiency. France demonstrates growing adoption in public and private hospitals, emphasizing multispecialty robotic platforms that facilitate minimally invasive procedures while supporting research and surgical education initiatives. The UK prioritizes deployment in teaching hospitals and specialist referral centers, integrating robotics with digital surgical planning tools and workflow management systems to optimize operational efficiency.

In Italy, adoption is concentrated in metropolitan hospitals performing high-complexity procedures, with an emphasis on postoperative outcomes and reduced hospital stays. Spain is gradually expanding its robotic surgical programs, leveraging government-supported training initiatives and pilot programs in leading tertiary care institutions. Across Western Europe, adoption is influenced by hospital capital allocation, surgeon expertise, regulatory compliance, and patient demand for minimally invasive surgery. Germany's leadership sets a benchmark for technological integration, while other countries follow phased and strategic deployment models that balance clinical excellence with operational efficiency. Overall, Western Europe presents a structured and mature market for surgical robotics, combining regulatory rigor, technological sophistication, and evidence-based clinical strategies to support widespread adoption.

Get more information on this report

Western Europe Surgical Robots Market Research Report Guidance:

The report includes qualitative and quantitative data in the Western Europe Surgical Robots Market across product, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Western Europe Surgical Robots Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Western Europe Surgical Robots Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Western Europe Surgical Robots Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Western Europe Surgical Robots Market segments by product, application, end user, and geography across Belgium, the Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, the UK, Denmark, Portugal, Norway, and Finland. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Western Europe Surgical Robots Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Western Europe Surgical Robots Market News and Key Development:

The Western Europe Surgical Robots Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Western Europe Surgical Robots Market are:

In July 2025, the Intuitive da Vinci 5 surgical robot system was granted CE mark approval for use across Europe, covering both adult and pediatric minimally invasive procedures such as urology, gynecology, and general laparoscopic surgery. This latest‑generation multiport robot includes over 150 enhancements, including improved vision and force‑feedback capabilities over earlier models. The European clearance enables hospitals throughout Western Europe to begin deploying this cutting‑edge platform clinically. The approval strengthens access to advanced robotic care across major surgical specialties.

In September 2025, Surgerii Robotics' Shurui single‑port surgical robot earned CE mark certification in Europe, making it one of the few single‑port robotic platforms cleared for clinical use alongside earlier systems. This approval unlocks its use for minimally invasive procedures in hospitals across Western Europe. Shurui's design enables flexible, high‑precision procedures through a single incision, potentially reducing trauma and recovery time. The CE mark supports broader adoption and training in hospitals.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - Western Europe Surgical Robots Market

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Frequently Asked Questions

How big is the Western Europe Surgical Robots Market?

The Western Europe Surgical Robots Market is valued at US$ 1,557.3 Million in 2025, it is projected to reach US$ 2,661.0 Million by 2033.

What is the CAGR for Western Europe Surgical Robots Market by (2026 - 2033)?

As per our report Western Europe Surgical Robots Market, the market size is valued at US$ 1,557.3 Million in 2025, projecting it to reach US$ 2,661.0 Million by 2033. This translates to a CAGR of approximately 6.9% during the forecast period.

What segments are covered in this report?

The Western Europe Surgical Robots Market report typically cover these key segments-

Product (Robotic Surgical Systems, Robotic Surgery Accessories & Instruments, Others)

Application (Laparoscopy, Neurology, Orthopedics, Gynecology, Urology, Cardiology, Other Applications)

End User (Hospitals, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for Western Europe Surgical Robots Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Western Europe Surgical Robots Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Western Europe Surgical Robots Market?

The Western Europe Surgical Robots Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Who should buy this report?

The Western Europe Surgical Robots Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Western Europe Surgical Robots Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Western Europe Surgical Robots Market

Get Free Sample For Western Europe Surgical Robots Market