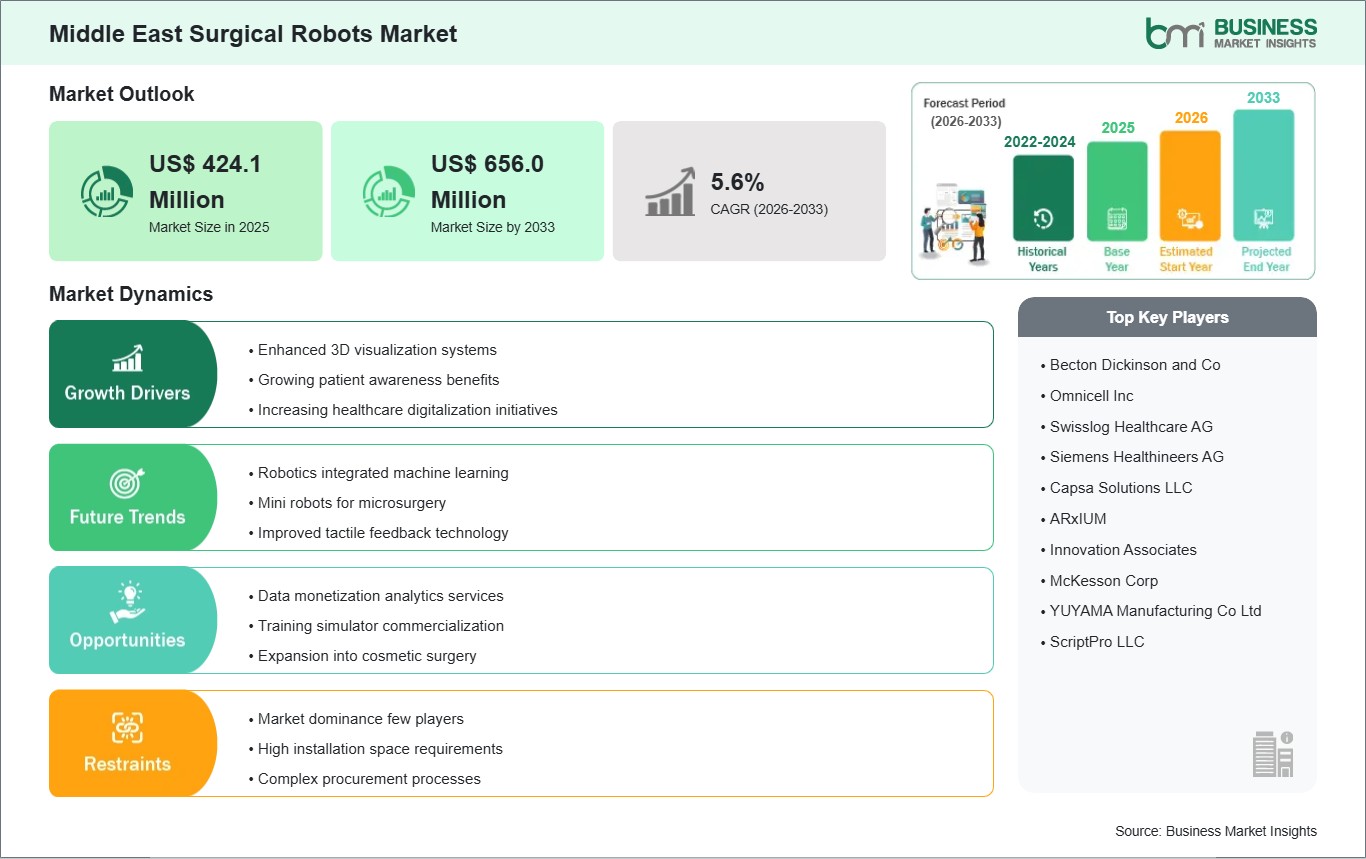

The Middle East Surgical Robots Market size is expected to reach US$ 656.0 million by 2033 from US$ 424.1 million in 2025. The market is estimated to record a CAGR of 5.6% from 2026 to 2033.

Executive Summary and Middle East Surgical Robots Market Analysis:

The Middle East surgical robots market has emerged as a strategic segment within the region’s healthcare modernization initiatives, fueled by strong government investments, rising healthcare expenditure, and the growing emphasis on minimally invasive procedures. The market is concentrated in urban centers and tertiary hospitals with sufficient procedural volumes to justify the capital-intensive nature of robotic-assisted platforms. Leading private hospital networks and academic medical centers are deploying surgical robots across specialties such as urology, cardiothoracic surgery, oncology, and gynecology to enhance precision, reduce intraoperative complications, and improve postoperative recovery times. Global manufacturers, including Intuitive Surgical, Medtronic, and CMR Surgical, have established strong distribution and service networks across the region, providing technical maintenance, surgeon training, and integration support. Hospitals are increasingly evaluating robotic systems not only for their clinical capabilities but also for their ability to support multi-specialty use, enhance operational efficiency, and align with international accreditation standards. The competitive landscape is driven by strategic investments in advanced surgical technologies to differentiate institutions in high-income patient segments and medical tourism markets. Adoption is influenced by regulatory approvals, infrastructure readiness, and availability of trained surgeons, with private hospitals typically leading implementation due to more flexible capital allocation. Public-sector adoption, while slower, is gradually increasing in countries pursuing national healthcare modernization and high-complexity care strategies. Overall, the Middle East surgical robots market is positioned for strategic growth, emphasizing technological excellence, improved clinical outcomes, and operational optimization as hospitals aim to strengthen competitive positioning and patient-centric care.

Middle East Surgical Robots Market - Strategic Insights:

Get more information on this report

Middle East Surgical Robots Market Segmentation Analysis:

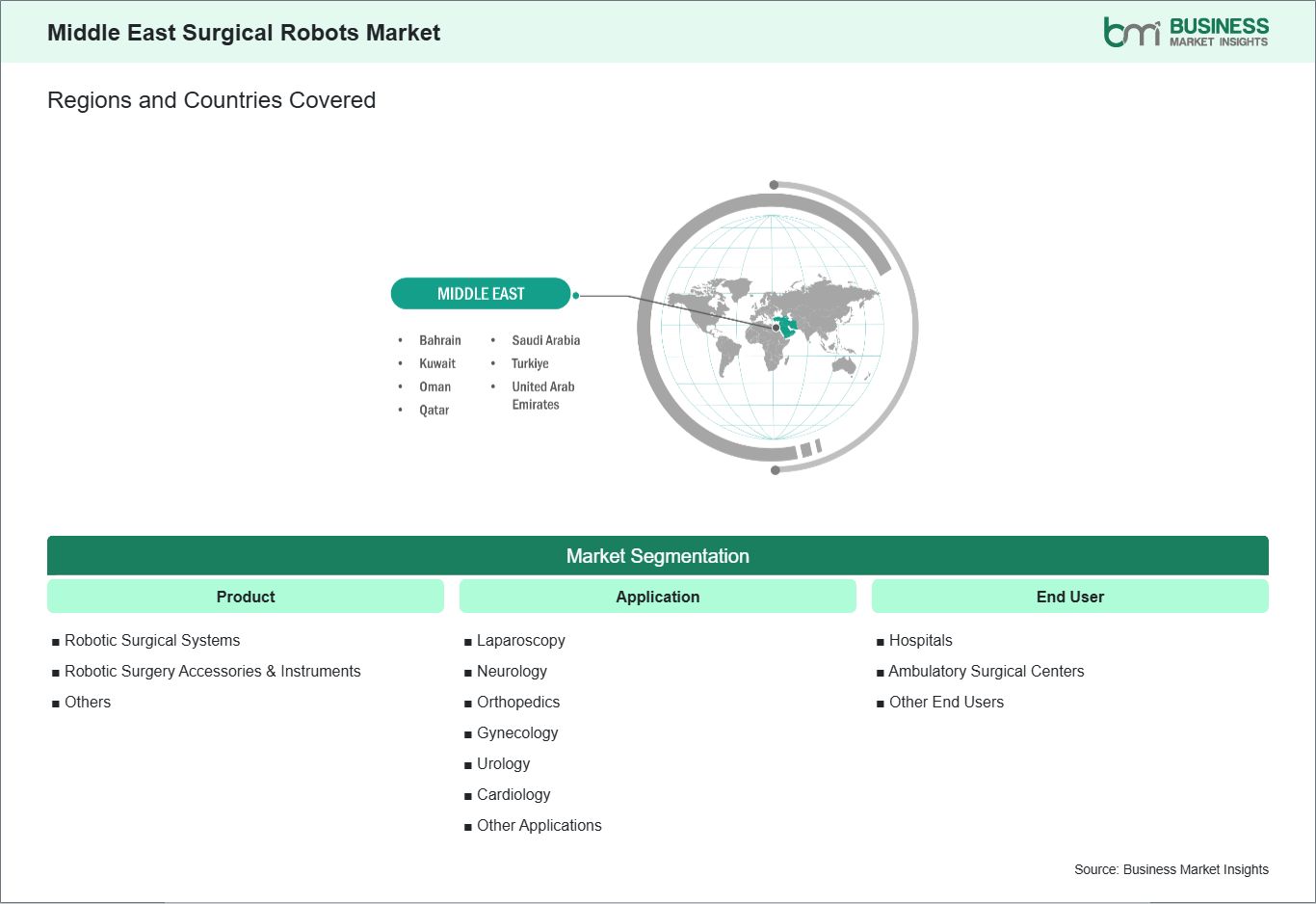

Key segments that contributed to the derivation of the Middle East Surgical Robots Market analysis are product, application, and end user.

By product, the surgical robots market is segmented into robotic surgical systems, robotic surgery accessories & instruments and others. The robotic surgery accessories & instruments segment dominated the market in 2025.

In terms of application, the surgical robots market is categorized into laparoscopy, neurology, orthopedics, gynecology, urology, cardiology and other applications. The laparoscopy segment dominated the market in 2025.

Based on end user, the surgical robots market is classified into hospitals, ambulatory surgical centers and other end users. The hospitals segment dominated the market in 2025.

Middle East Surgical Robots Market Drivers and Opportunities:

Enhanced 3D visualization systems

In the Middle East surgical robots market, enhanced 3D visualization systems are becoming a cornerstone of clinical investment decisions, particularly within advanced tertiary care centers across Saudi Arabia, the United Arab Emirates, and Qatar. Hospitals in these markets are prioritizing next‑generation visualization technologies that provide high‑definition, stereoscopic views of the surgical field, enabling surgeons to perceive depth and anatomical detail with greater clarity. This capability is especially valuable in procedures such as urology, gynecology, and complex soft tissue surgeries where visual precision directly influences clinical outcomes. Healthcare executives are emphasizing 3D visualization as a competitive differentiator in regional centers of excellence. For example, major medical facilities in Dubai and Riyadh are incorporating robotic systems with integrated 3D imaging platforms into surgical suites to support minimally invasive procedures and reduce reliance on traditional open surgery. For patient populations with higher prevalence of conditions such as prostate and gynecologic cancers, enhanced visualization is seen as critical to improving surgical accuracy and reducing complication rates. These systems also support surgeons in navigating complex anatomy, which can be particularly variable in diverse Middle Eastern populations. Adoption of enhanced 3D visualization is further supported by surgeon training initiatives and academic collaborations. Regional medical universities and surgical societies in the Middle East are hosting hands‑on workshops and simulation labs that leverage these advanced imaging systems, helping clinicians build proficiency before deploying technology in live surgery. This focus on skill development not only accelerates surgeon confidence but also strengthens institutional justification for investing in premium visualization capabilities. As a result, enhanced 3D systems are playing an increasingly strategic role in how hospitals in the Middle East plan and scale their surgical robotics programs.

Data monetization analytics services

Data monetization analytics services are beginning to emerge as a distinct market opportunity within the Middle East surgical robots ecosystem. As hospitals in Saudi Arabia, the UAE, and Kuwait adopt robotic platforms, they are generating significant volumes of procedural, performance, and outcomes data. Healthcare organizations and technology vendors are recognizing the potential value of this data when aggregated and analyzed at scale, particularly for insights that can inform clinical best practices, supply chain optimization, and predictive maintenance of surgical assets. Advanced analytics services are being designed to package de‑identified surgical data into performance dashboards, benchmarking tools, and outcome prediction models that can be shared across hospital networks. For example, large multi‑hospital systems in Dubai and Abu Dhabi are partnering with analytics firms to transform raw robotics usage metrics into actionable insights that inform staffing, instrument utilization, and patient risk stratification. These analytics services help hospitals reduce costs and improve workflow efficiency, while also creating opportunities for data‑driven consulting arrangements that extend beyond the initial technology sale. Beyond operational improvements, data monetization analytics services are enabling new revenue streams for both healthcare providers and technology partners. With appropriate governance and patient privacy safeguards, anonymized datasets are being used to support research collaborations, medical device refinement, and third‑party software development. In Qatar and Bahrain, public‑private initiatives are exploring frameworks that allow surgical outcome data to contribute to regional health research consortia and quality registries. As analytics capabilities continue to mature, data monetization services are positioned to enhance the economic value of surgical robotics investment, supporting evidence‑based decision‑making and long‑term sustainability for healthcare organizations across the Middle East.

Middle East Surgical Robots Market Size and Share Analysis:

The Middle East Surgical Robots Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

By product, the robotic surgery accessories & instruments segment dominated the market in 2025, driven by the recurring and high replacement demand for consumable tools required in robotic procedures, ensuring continuous revenue as surgical volumes grow.

In terms of application, the laparoscopy segment dominated the market in 2025, driven by the increasing adoption of minimally invasive laparoscopic robotic surgeries in the Middle East due to their enhanced precision, reduced trauma, and improved patient outcomes.

Based on end user, the hospitals segment dominated the market in 2025, driven by their advanced infrastructure, high surgical volumes, and increased investment in cutting‑edge robotic technologies to meet rising demand for precision and minimally invasive procedures.

Middle East Surgical Robots Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 424.1 Million

Market Size by 2033

US$ 656.0 Million

CAGR (2026 - 2033)

5.6%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Robotic Surgical Systems

Robotic Surgery Accessories & Instruments

Others

By Application

Laparoscopy

Neurology

Orthopedics

Gynecology

Urology

Cardiology

Other Applications

By End User

Hospitals

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

Middle East

UAE, Saudi Arabia, Bahrain, Oman, Kuwait, Qatar, and Turkiye

Market leaders and key company profiles

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Get more information on this report

Middle East Surgical Robots Market Report Coverage and Deliverables:

The "Middle East Surgical Robots Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Middle East Surgical Robots Market size and forecast at regional and country levels for all market segments covered under the scope

Middle East Surgical Robots Market trends, as well as drivers, restraints, and opportunities

Middle East Surgical Robots Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Middle East Surgical Robots Market

Detailed company profiles, including SWOT analysis

Middle East Surgical Robots Market Geographic Insights:

The geographical scope of the Middle East Surgical Robots Market report is divided into UAE, Saudi Arabia, Bahrain, Oman, Kuwait, Qatar, and Turkiye. Turkiye held the largest share in 2025.

Country-level adoption within the Middle East shows a heterogeneous landscape, shaped by national healthcare strategies, infrastructure maturity, and capital availability. Turkey is the dominant market, with robotic systems deployed extensively across tertiary hospitals and specialized centers in metropolitan hubs such as Istanbul and Ankara. The focus is on high-volume procedures in urology, oncology, cardiothoracic, and gynecology, supported by public healthcare modernization initiatives and strong private hospital investments. United Arab Emirates demonstrates high adoption in Dubai and Abu Dhabi, driven by medical tourism ambitions, international hospital accreditation, and investment in smart hospital technologies. Qatar integrates robotics in state-funded specialty hospitals, emphasizing complex surgical care aligned with national health priorities. Kuwait shows selective deployment in urban referral hospitals, focusing on high-precision interventions to optimize patient outcomes. Oman and Bahrain are gradually introducing robotics in leading private hospitals and tertiary care centers, leveraging partnerships with global vendors for surgeon training and system maintenance. Adoption across the region is influenced by capital availability, surgeon expertise, patient demand for advanced surgical outcomes, and regulatory frameworks. Turkey’s leadership sets a benchmark for the region, while other countries follow phased, strategic integration, creating a heterogeneous but steadily advancing Middle East surgical robotics landscape.

Get more information on this report

Middle East Surgical Robots Market Research Report Guidance:

The report includes qualitative and quantitative data in the Middle East Surgical Robots Market across product, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Middle East Surgical Robots Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Middle East Surgical Robots Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Middle East Surgical Robots Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Middle East Surgical Robots Market segments by product, application, end user, and geography across UAE, Saudi Arabia, Bahrain, Oman, Kuwait, Qatar, and Turkiye. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Middle East Surgical Robots Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Middle East Surgical Robots Market News and Key Development:

The Middle East Surgical Robots Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Middle East Surgical Robots Market are:

In September 2025, American Hospital Dubai introduced the Intuitive da Vinci SP (Single Port) robotic surgical system to the Middle East, offering ultra‑precise surgery through a single incision and minimal scarring. This launch marked a major innovation for region‑wide access to advanced minimally invasive robotic care across multiple specialties. The system builds on earlier da Vinci generations already in use locally, strengthening Dubai’s role as a hub for surgical tech. It also supports faster patient recovery and improved outcomes with cutting‑edge robotics.

In October 2025, Dubai Hospital under Dubai Health celebrated over 145 successful robotic‑assisted surgeries since launching its robotic surgery programme in late 2022. The multi‑specialty procedures, using robotic platforms like the da Vinci Xi, highlight the integration of robotics into routine clinical care. This milestone underscores the growing adoption and scale‑up of surgical robotics across general, urological and gynaecological operations in the UAE. It reflects robust regional infrastructure and surgeon training to support advanced robotic procedures.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - Middle East Surgical Robots Market

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Frequently Asked Questions

How big is the Middle East Surgical Robots Market?

The Middle East Surgical Robots Market is valued at US$ 424.1 Million in 2025, it is projected to reach US$ 656.0 Million by 2033.

What is the CAGR for Middle East Surgical Robots Market by (2026 - 2033)?

As per our report Middle East Surgical Robots Market, the market size is valued at US$ 424.1 Million in 2025, projecting it to reach US$ 656.0 Million by 2033. This translates to a CAGR of approximately 5.6% during the forecast period.

What segments are covered in this report?

The Middle East Surgical Robots Market report typically cover these key segments-

Product (Robotic Surgical Systems, Robotic Surgery Accessories & Instruments, Others)

Application (Laparoscopy, Neurology, Orthopedics, Gynecology, Urology, Cardiology, Other Applications)

End User (Hospitals, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for Middle East Surgical Robots Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East Surgical Robots Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Middle East Surgical Robots Market?

The Middle East Surgical Robots Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Who should buy this report?

The Middle East Surgical Robots Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Middle East Surgical Robots Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Middle East Surgical Robots Market

Get Free Sample For Middle East Surgical Robots Market