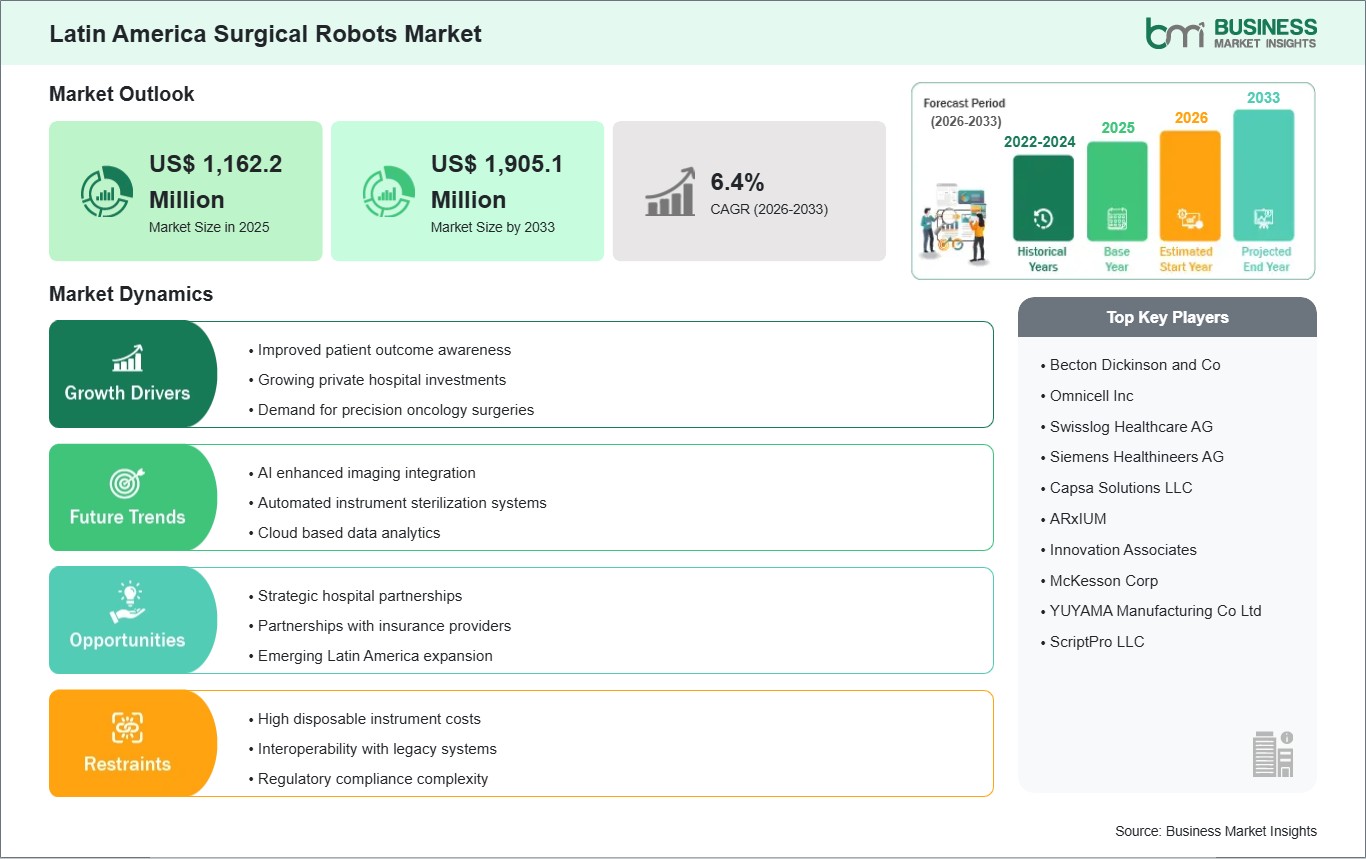

The Latin America Surgical Robots Market size is expected to reach US$ 1,905.1 million by 2033 from US$ 1,162.2 million in 2025. The market is estimated to record a CAGR of 6.4% from 2026 to 2033.

Executive Summary and Latin America Surgical Robots Market Analysis:

The Latin America surgical robots market is progressively expanding, driven by private healthcare sector growth, increasing demand for minimally invasive procedures, and modernization of high-complexity hospitals. Adoption is primarily concentrated in leading metropolitan areas where tertiary care institutions possess the financial and technical capacity to deploy robotic-assisted surgical platforms. The market is shaped by growing incidence of oncological, urological, and bariatric conditions requiring precision-based interventions. Hospitals are leveraging robotic systems to enhance surgical dexterity, reduce recovery times, and strengthen institutional positioning in competitive urban healthcare markets. Global manufacturers such as Intuitive Surgical, Medtronic, and Stryker Corporation maintain strong regional distribution networks, providing clinical training and long-term maintenance support to ensure system utilization efficiency. Market penetration remains uneven, with higher concentration in private hospital chains compared to public healthcare facilities, where capital allocation constraints limit rapid adoption. Procurement decisions are increasingly influenced by return-on-investment metrics, system versatility across specialties, and compatibility with advanced imaging technologies. Furthermore, medical tourism in select countries is reinforcing demand for high-precision surgical capabilities. Despite regulatory and economic variability across the region, the market demonstrates steady structural advancement, supported by institutional focus on improving surgical outcomes and operational performance through robotic integration.

Latin America Surgical Robots Market - Strategic Insights:

Get more information on this report

Latin America Surgical Robots Market Segmentation Analysis:

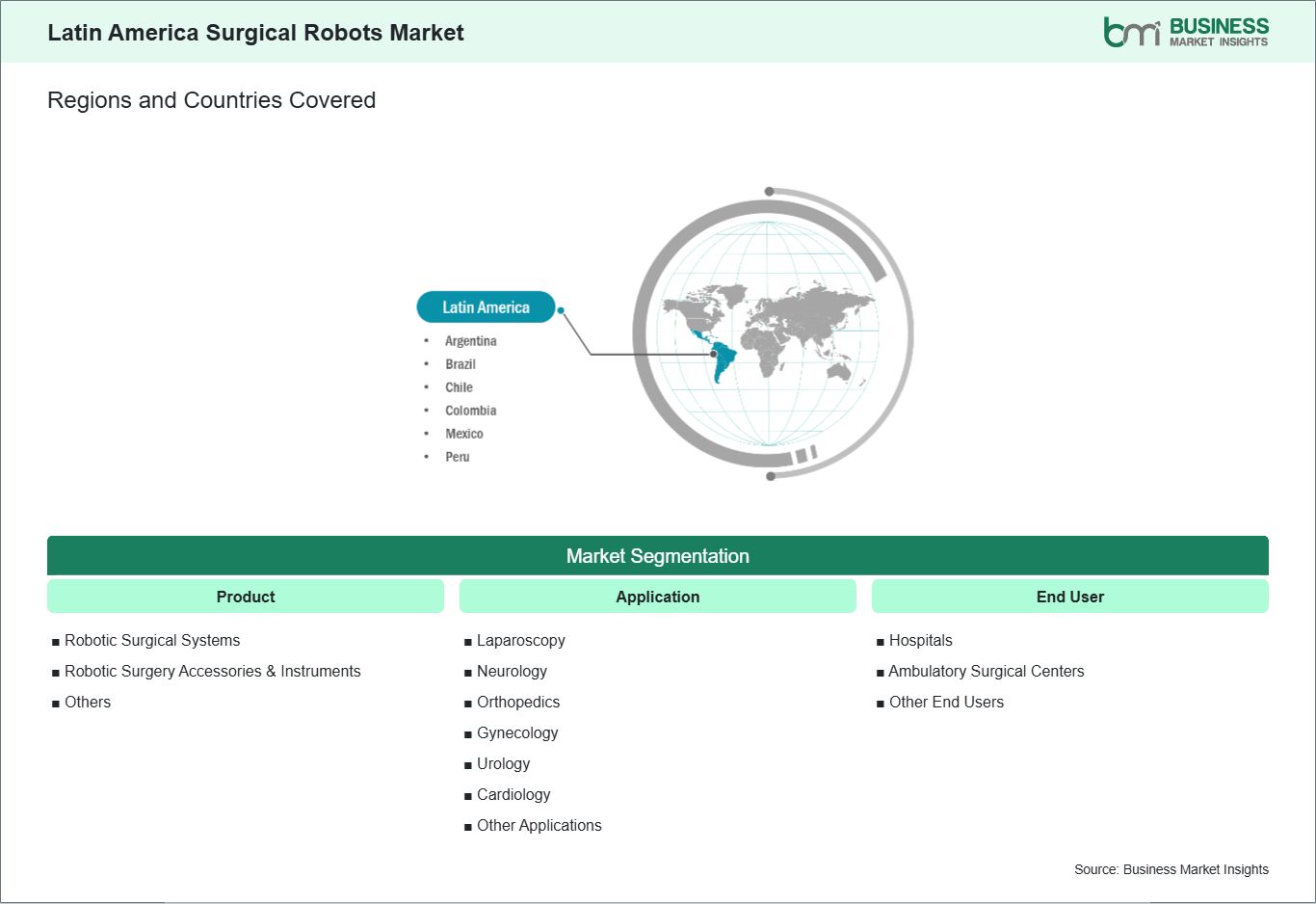

Key segments that contributed to the derivation of the Latin America Surgical Robots Market analysis are product, usability, and application.

By product, the surgical robots market is segmented into robotic surgical systems, robotic surgery accessories & instruments and others. The robotic surgery accessories & instruments segment dominated the market in 2025.

In terms of application, the surgical robots market is categorized into laparoscopy, neurology, orthopedics, gynecology, urology, cardiology and other applications. The laparoscopy segment dominated the market in 2025.

Based on end user, the surgical robots market is classified into hospitals, ambulatory surgical centers and other end users. The hospitals segment dominated the market in 2025.

Latin America Surgical Robots Market Drivers and Opportunities:

Improved patient outcome awareness

In the Latin America surgical robots market, growing awareness of improved patient outcomes is a key force shaping technology adoption. Patients and healthcare professionals in countries such as Brazil, Mexico, Argentina, and Chile are increasingly informed about the benefits of robotic‑assisted surgery, including reduced trauma, smaller incisions, and faster recovery. As educational campaigns and clinical success stories circulate through professional networks and media, patient expectations are rising, and demand is shifting toward high‑quality surgical options that prioritize recovery experience and long‑term results. Healthcare providers are responding to this shift by positioning robotic surgery as a value‑enhancing proposition. In major urban centers such as São Paulo, Buenos Aires, and Mexico City, hospitals highlight robotics in their service portfolios to distinguish themselves in competitive markets. For many patients, especially those seeking treatment for complex conditions in urology, gynecology, or oncology, robotic procedures are perceived not just as a technological upgrade but as a pathway to better clinical outcomes and improved quality of life. This perception is influencing decision‑making and becoming an important factor in where patients choose to seek care. Physician communities across Latin America are also playing a role in expanding outcome awareness by sharing clinical evidence and best practices through regional conferences, specialist societies, and collaborative networks. Surgeons trained in robotic techniques are increasingly vocal about the advantages they observe, such as decreased complication rates and shorter hospital stays, which reinforces trust among peers and patients alike. This growing emphasis on outcome transparency is contributing to a broader cultural shift in surgical care expectations, encouraging more healthcare organizations to allocate capital toward robotic systems as part of long‑term clinical strategy.

Strategic hospital partnerships

Strategic hospital partnerships are emerging as a central growth driver in the Latin America surgical robots market. Leading hospitals in Brazil, Colombia, Peru, and Chile are entering formal alliances with robotic technology suppliers to enhance access, training, and support infrastructure. These partnerships often include structured clinical programs, ongoing technical assistance, and coordinated educational initiatives that help institutions build sustainable robotic surgery practices. By sharing responsibilities and aligning strategic interests, hospitals and vendors are jointly driving market expansion at a faster pace than isolated procurement efforts. Partnership models in the region are evolving beyond traditional sales arrangements to include value‑based collaborations. For example, some health systems and technology developers agree to outcome‑aligned performance benchmarks that influence long‑term engagement terms. These arrangements help hospitals mitigate risk by tying parts of the investment to actual clinical performance improvements. In competitive healthcare environments like Mexico and Argentina, where resource allocation decisions are scrutinized carefully, such strategic alignment offers both financial and operational confidence to hospital administrators considering robotics adoption. Additionally, public and private hospital networks are leveraging partnership frameworks to expand surgical robotics beyond flagship facilities into broader care ecosystems. By pooling resources, sharing training platforms, and facilitating surgeon exchanges across member institutions, networks in Central America and the Southern Cone are reducing barriers to entry for smaller hospitals. These collaborative models are enabling a more distributed rollout of robotic technology, increasing the number of facilities capable of offering advanced surgical care and strengthening regional surgical capabilities overall. As partnerships mature, they are expected to play an increasingly pivotal role in shaping how surgical robotics diffuse across Latin American healthcare markets.

Latin America Surgical Robots Market Size and Share Analysis:

The Latin America Surgical Robots Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

By product, the robotic surgery accessories & instruments segment dominated the market in 2025, driven by the recurring and high usage demand for consumables and procedure‑specific tools required across increasing numbers of robotic surgeries, creating steady revenue.

In terms of application, the laparoscopy segment dominated the market in 2025, driven by the rising adoption of minimally invasive robotic laparoscopic procedures in Latin American healthcare settings due to benefits like reduced recovery time and improved surgical outcomes.

Based on end user, the hospitals segment dominated the market in 2025, driven by their expanding infrastructure, high surgical volumes, and growing investments in advanced surgical technologies to improve care quality and attract patients.

Latin America Surgical Robots Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 1,162.2 Million

Market Size by 2033

US$ 1,905.1 Million

CAGR (2026 - 2033)

6.4%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Robotic Surgical Systems

Robotic Surgery Accessories & Instruments

Others

By Application

Laparoscopy

Neurology

Orthopedics

Gynecology

Urology

Cardiology

Other Applications

By End User

Hospitals

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

Latin America

Mexico, Brazil, Argentina, Peru, Chile, Colombia

Market leaders and key company profiles

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Get more information on this report

Latin America Surgical Robots Market Report Coverage and Deliverables:

The "Latin America Surgical Robots Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Latin America Surgical Robots Market size and forecast at regional and country levels for all market segments covered under the scope

Latin America Surgical Robots Market trends, as well as drivers, restraints, and opportunities

Latin America Surgical Robots Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Latin America Surgical Robots Market

Detailed company profiles, including SWOT analysis

Latin America Surgical Robots Market Geographic Insights:

The geographical scope of the Latin America Surgical Robots Market report is divided into Mexico, Brazil, Argentina, Peru, Chile, and Colombia. Brazil held the largest share in 2025.

Country-level dynamics in Latin America reveal highly varied adoption trends shaped by healthcare infrastructure, financial capacity, and strategic institutional priorities. Brazil dominates regional adoption, with robotic systems concentrated in private hospital networks in São Paulo, Rio de Janeiro, and other metropolitan centers. Focused primarily on oncology, urology, and bariatric procedures, these hospitals leverage robotics to improve clinical outcomes, reduce patient recovery time, and attract medical tourists. Mexico demonstrates strong adoption in metropolitan private hospitals and international medical tourism corridors, particularly for minimally invasive general surgery and bariatric interventions. In Argentina, adoption is concentrated in leading urban academic hospitals, supported by partnerships with international manufacturers for surgeon training and technical support. Chile shows selective integration in tertiary hospitals, prioritizing high-precision procedures and efficient surgical workflows. Meanwhile, Colombia is gradually expanding robotic surgery programs in metropolitan centers, leveraging international collaborations to strengthen surgeon capabilities. Across the region, adoption is influenced by hospital capital availability, case volumes, reimbursement mechanisms, and surgeon expertise. Leading economies demonstrate high sophistication in procedural integration, whereas smaller markets rely on phased deployment strategies. Collectively, these country-specific trends underscore a diverse Latin American market characterized by concentrated adoption in high-capacity urban hospitals, growing medical tourism influence, and progressive expansion into secondary facilities as infrastructure and expertise develop.

Get more information on this report

Latin America Surgical Robots Market Research Report Guidance:

The report includes qualitative and quantitative data in the Latin America Surgical Robots Market across product, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Latin America Surgical Robots Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Latin America Surgical Robots Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Latin America Surgical Robots Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Latin America Surgical Robots Market segments by product, application, end user, and geography across Mexico, Brazil, Argentina, Peru, Chile, and Colombia. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Latin America Surgical Robots Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Latin America Surgical Robots Market News and Key Development:

The Latin America Surgical Robots Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Latin America Surgical Robots Market are:

In January 2025, MicroPort MedBots Toumai Laparoscopic Surgical Robot received market approval from Brazil’s National Health Surveillance Agency (ANVISA), allowing its commercial use in minimally invasive surgery across the country. The approval positions Toumai as a cutting‑edge robotic platform in Latin America’s largest healthcare market. The launch event in São Paulo also showcased remote surgery capabilities using the Toumai system. This marks a key regulatory breakthrough expanding robotic surgery accessibility in Latin America.

In January 2025, the MicroPort MedBot SkyWalker orthopedic surgical robot completed its first total knee arthroplasty at Vera Cruz Hospital in Sao Paulo, representing its entry into the South American clinical landscape. The platform enhances precision and alignment planning in joint replacement procedures, advancing robotic orthopedics locally. This first commercial clinical application demonstrates the increasing adoption of purpose‑built robotic systems beyond general laparoscopic robots. The deployment supports a broader robotics ecosystem in Latin American hospitals.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - Latin America Surgical Robots Market

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Frequently Asked Questions

How big is the Latin America Surgical Robots Market?

The Latin America Surgical Robots Market is valued at US$ 1,162.2 Million in 2025, it is projected to reach US$ 1,905.1 Million by 2033.

What is the CAGR for Latin America Surgical Robots Market by (2026 - 2033)?

As per our report Latin America Surgical Robots Market, the market size is valued at US$ 1,162.2 Million in 2025, projecting it to reach US$ 1,905.1 Million by 2033. This translates to a CAGR of approximately 6.4% during the forecast period.

What segments are covered in this report?

The Latin America Surgical Robots Market report typically cover these key segments-

Product (Robotic Surgical Systems, Robotic Surgery Accessories & Instruments, Others)

Application (Laparoscopy, Neurology, Orthopedics, Gynecology, Urology, Cardiology, Other Applications)

End User (Hospitals, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for Latin America Surgical Robots Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Latin America Surgical Robots Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Latin America Surgical Robots Market?

The Latin America Surgical Robots Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Who should buy this report?

The Latin America Surgical Robots Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Latin America Surgical Robots Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Latin America Surgical Robots Market

Get Free Sample For Latin America Surgical Robots Market