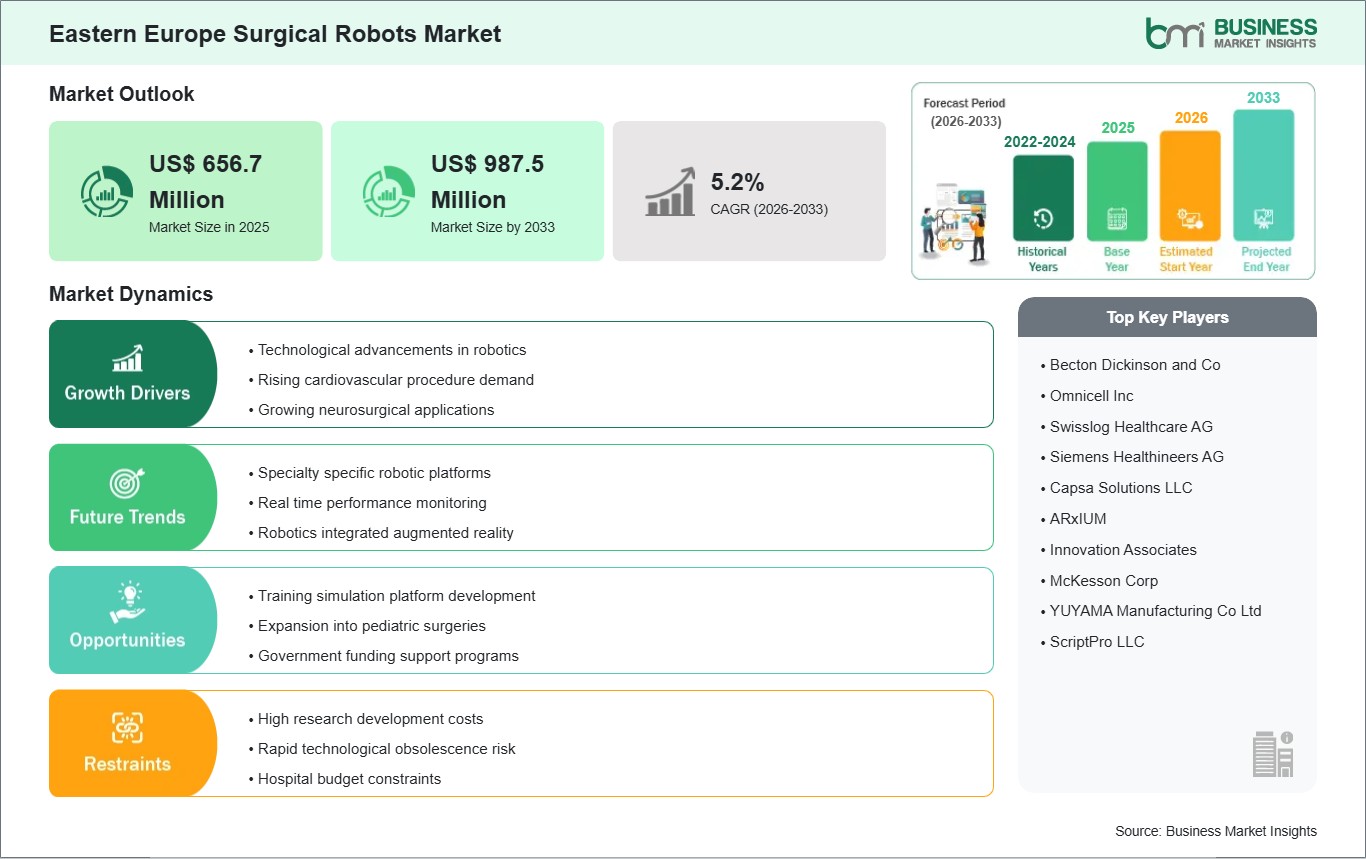

The Eastern Europe Surgical Robots Market size is expected to reach US$ 987.5 million by 2033 from US$ 656.7 million in 2025. The market is estimated to record a CAGR of 5.2% from 2026 to 2033.

Executive Summary and Eastern Europe Surgical Robots Market Analysis:

The Eastern Europe surgical robots market is gradually maturing, driven by increasing hospital modernization initiatives, rising prevalence of chronic and lifestyle-related diseases, and the growing demand for precision-based surgical care. Adoption is concentrated in urban tertiary care hospitals and private specialty centers that can support the significant capital investment required for robotic-assisted surgical systems. The market is characterized by a focus on urology, gynecology, cardiothoracic, and colorectal procedures, where robotic platforms provide high dexterity and reduce intraoperative variability, improving patient outcomes and shortening hospital stays. Leading global manufacturers such as Intuitive Surgical, Medtronic, and Stryker Corporation have strengthened their presence through regional distributors, training programs, and service agreements, ensuring operational continuity and skill development. Market growth is also influenced by healthcare institutions seeking to attract international patients and position themselves as centers of surgical excellence. However, barriers remain in the form of limited reimbursement frameworks, budgetary constraints in public hospitals, and inconsistent surgeon training availability across Eastern Europe. Competitive strategies increasingly rely on bundled solutions that integrate imaging systems, AI-enabled surgical planning, and tele-mentoring capabilities. Additionally, hospitals are emphasizing long-term return on investment by selecting platforms capable of supporting multiple surgical specialties. Overall, the Eastern Europe surgical robots market is in a phase of strategic adoption, with growth focused on combining clinical precision, operational efficiency, and the capacity to meet evolving patient expectations.

Eastern Europe Surgical Robots Market - Strategic Insights:

Get more information on this report

Eastern Europe Surgical Robots Market Segmentation Analysis:

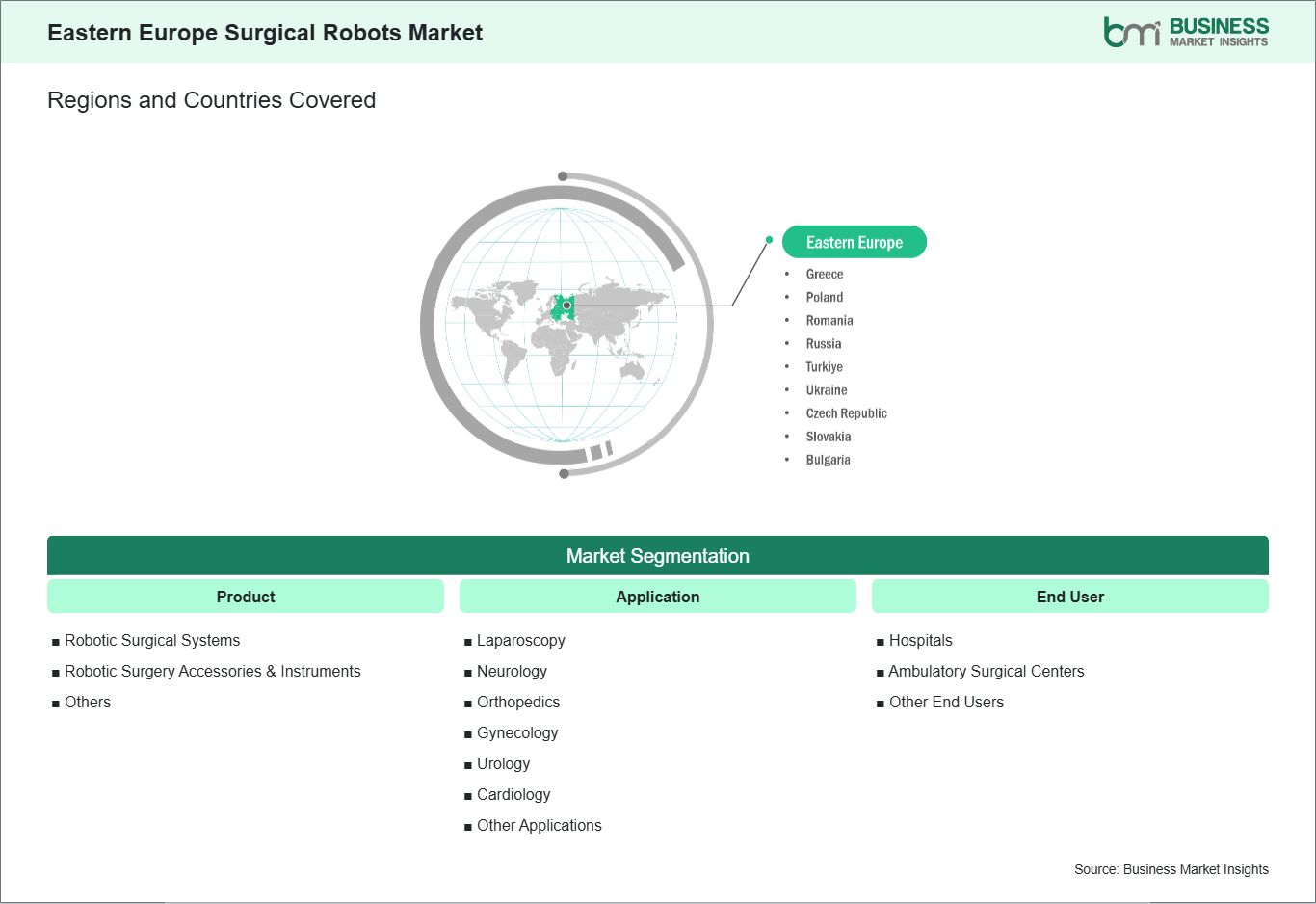

Key segments that contributed to the derivation of the Eastern Europe Surgical Robots Market analysis are product, application, and end user.

By product, the surgical robots market is segmented into robotic surgical systems, robotic surgery accessories & instruments and others. The robotic surgery accessories & instruments segment dominated the market in 2025.

In terms of application, the surgical robots market is categorized into laparoscopy, neurology, orthopedics, gynecology, urology, cardiology and other applications. The laparoscopy segment dominated the market in 2025.

Based on end user, the surgical robots market is classified into hospitals, ambulatory surgical centers and other end users. The hospitals segment dominated the market in 2025.

Eastern Europe Surgical Robots Market Drivers and Opportunities:

Technological advancements in robotics

In the Eastern Europe surgical robots market, technological advancements are rapidly reshaping clinical capabilities and healthcare delivery. Countries such as Poland, Czech Republic, Hungary, Romania, and Ukraine are witnessing increased interest in next‑generation robotic systems that offer superior precision, multi‑instrument flexibility, and enhanced imaging integration. Healthcare leaders in these markets recognize that innovation in robotics can address longstanding challenges in surgical accuracy and operative efficiency, especially for complex procedures in urology, gynecology, and oncology where precision directly influences patient outcomes. Hospitals in Eastern Europe are progressively adopting robotic platforms that incorporate artificial intelligence, improved haptic feedback, and automated motion scaling to support surgeons in demanding clinical environments. These enhancements help reduce surgeon fatigue during prolonged operations and enable more consistent procedural performance across diverse case types. For example, tertiary care centers in Warsaw and Budapest are deploying systems equipped with advanced end‑effectors and superior visualization to support minimally invasive surgery. The growing focus on improved ergonomics and data‑driven surgical support is strengthening confidence among clinicians who have historically relied more heavily on traditional surgical techniques. Moreover, partnerships between Eastern European medical institutions and international robotics developers are accelerating the pace of technological integration. Collaborative research projects, pilot programs, and localized customization of robotic platforms are enabling hospitals to tailor solutions to regional caseloads and clinical preferences. This emphasis on innovation is also encouraging local supply chain development for robotics accessories and software tools, supporting broader ecosystem maturity. As Eastern Europe continues to invest in cutting‑edge surgical technology, the market is positioned for steady growth, with advanced robotics becoming central to modern surgical strategy across both public and private sectors.

Training simulation platform development

Training simulation platforms are increasingly recognized as essential enablers of successful surgical robotics adoption in Eastern Europe. As hospitals introduce advanced robots into clinical practice, the need for structured training pathways that build surgeon competence and confidence is becoming paramount. Simulation technologies, including virtual reality (VR) and augmented reality (AR) modules, are being used more frequently in surgical education programs at major medical universities in Krakow, Prague, and Bucharest, helping to close the skills gap between traditional surgical techniques and robot‑assisted procedures. Simulation platforms allow surgeons to rehearse complex interventions in risk‑free environments, accelerating their learning curve and improving proficiency before working with patients. In Poland and Hungary, healthcare institutions are collaborating with robotics vendors to develop tailored simulation curricula that reflect regional procedural priorities and case mixes. These programs often include standardized performance benchmarks and objective assessment tools, enabling participants to monitor improvement and certification readiness. By embedding simulation into core training pathways, Eastern European providers are strengthening workforce capabilities that support safe, effective robotic surgery adoption. In addition, training simulation development is fostering broader educational ecosystems within the region. Simulation centers are emerging as hubs of surgical excellence, attracting trainees from neighboring countries and facilitating cross‑institutional knowledge exchange. These centers often partner with surgical societies and academic bodies to host workshops, hands‑on labs, and multidisciplinary training events focused on robotics, further building regional expertise. As simulation platforms continue to expand, Eastern Europe is establishing a sustainable foundation for high‑quality robotic surgical practice that supports long‑term clinical growth and improved patient care.

Eastern Europe Surgical Robots Market Size and Share Analysis:

The Eastern Europe Surgical Robots Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

By product, the robotic surgery accessories & instruments segment dominated the market in 2025, driven by the recurring, procedure‑specific demand for consumables and precision tools required in nearly all robotic surgical procedures, ensuring continuous revenue growth.

In terms of application, the laparoscopy segment dominated the market in 2025, driven by the increasing adoption of minimally invasive laparoscopic robotic procedures, which offer enhanced precision, smaller incisions, reduced complications, and faster patient recovery.

Based on end user, the hospitals segment dominated the market in 2025, driven by their advanced infrastructure, high surgical volumes, financial capacity to invest in robotic systems, and the presence of skilled multidisciplinary surgical teams.

Eastern Europe Surgical Robots Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 656.7 Million

Market Size by 2033

US$ 987.5 Million

CAGR (2026 - 2033)

5.2%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Robotic Surgical Systems

Robotic Surgery Accessories & Instruments

Others

By Application

Laparoscopy

Neurology

Orthopedics

Gynecology

Urology

Cardiology

Other Applications

By End User

Hospitals

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

Eastern Europe

Russia, Poland, Ukraine, Romania, the Czech Republic, Slovakia, Bulgaria, Greece

Market leaders and key company profiles

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Get more information on this report

Eastern Europe Surgical Robots Market Report Coverage and Deliverables:

The "Eastern Europe Surgical Robots Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Eastern Europe Surgical Robots Market size and forecast at regional and country levels for all market segments covered under the scope

Eastern Europe Surgical Robots Market trends, as well as drivers, restraints, and opportunities

Eastern Europe Surgical Robots Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Eastern Europe Surgical Robots Market

Detailed company profiles, including SWOT analysis

Eastern Europe Surgical Robots Market Geographic Insights:

The geographical scope of the Eastern Europe Surgical Robots Market report is divided into Russia, Poland, Ukraine, Romania, the Czech Republic, Slovakia, Bulgaria, and Greece. Russia held the largest share in 2025.

Country-level dynamics in Eastern Europe reveal a highly varied adoption of surgical robots, driven by differences in healthcare infrastructure, funding models, and institutional priorities. Russia is the dominant market in the region, with high-volume urban hospitals and academic medical centers leading deployment. Robotic-assisted systems are primarily used for urology, oncology, cardiothoracic, and gynecological procedures, supported by government-led hospital modernization programs, robust capital investments, and a strong network of trained surgeons. Poland demonstrates strong adoption within private hospitals and tertiary care centers, focusing on high-complexity procedures such as minimally invasive oncological and urological surgeries, often backed by partnerships with global manufacturers for training and maintenance. Ukraine shows selective integration in urban hospitals, leveraging pilot programs and international collaborations to develop local surgeon expertise while managing capital constraints. In Romania, adoption is concentrated in leading university hospitals and private specialty centers, with robotics used to enhance surgical precision in cardiology, oncology, and gynecology. Czech Republic and Slovakia are gradually expanding robotics in public teaching hospitals and private urban centers, focusing on high-demand procedures and leveraging government incentives for infrastructure modernization. Bulgaria is an emerging market with limited adoption, mostly in private hospitals in Sofia and Plovdiv, where advanced surgical services are prioritized for high-income patients. Finally, Greece shows selective deployment in tertiary hospitals, driven by urban private institutions and specialized surgical centers. Across these markets, adoption is influenced by regulatory clarity, hospital funding models, surgeon expertise, and strategic prioritization of advanced surgical care. Russia’s leadership in adoption establishes it as the benchmark for regional deployment, while other countries follow phased, strategic integration reflecting local healthcare capacity and investment priorities.

Get more information on this report

Eastern Europe Surgical Robots Market Research Report Guidance:

The report includes qualitative and quantitative data in the Eastern Europe Surgical Robots Market across product, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Eastern Europe Surgical Robots Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Eastern Europe Surgical Robots Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Eastern Europe Surgical Robots Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Eastern Europe Surgical Robots Market segments by product, application, end user, and geography across Russia, Poland, Ukraine, Romania, the Czech Republic, Slovakia, Bulgaria, and Greece. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Eastern Europe Surgical Robots Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Eastern Europe Surgical Robots Market News and Key Development:

The Eastern Europe Surgical Robots Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Eastern Europe Surgical Robots Market are:

In August 2025, Polish surgeons used the EDGE MP1000 surgical robot to perform a remote coronary bypass and prostatectomy, operating on patients in Warsaw while controlling the robot from Gdańsk. The procedures spanning over 350 km were reported as Europe’s first remote robotic heart and urology surgeries with ultra‑low latency control. This milestone demonstrated next‑generation robotic telesurgery capabilities in Eastern Europe. It also showcased how emerging platforms like EDGE MP1000 can expand advanced care beyond traditional operating rooms.

In December 2025, the Wielkopolskie Oncology Centre in Poznań began using the latest Intuitive da Vinci 5 surgical robot for routine operations. The introduction of this fifth‑generation platform marks a significant upgrade in robotic surgery technology available within Poland, particularly for complex cancer and soft‑tissue procedures. Hospital teams reported improved precision and surgical ergonomics compared with older systems. This launch signals broader adoption of cutting‑edge robotic platforms in Eastern European surgical care.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - Eastern Europe Surgical Robots Market

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Frequently Asked Questions

How big is the Eastern Europe Surgical Robots Market?

The Eastern Europe Surgical Robots Market is valued at US$ 656.7 Million in 2025, it is projected to reach US$ 987.5 Million by 2033.

What is the CAGR for Eastern Europe Surgical Robots Market by (2026 - 2033)?

As per our report Eastern Europe Surgical Robots Market, the market size is valued at US$ 656.7 Million in 2025, projecting it to reach US$ 987.5 Million by 2033. This translates to a CAGR of approximately 5.2% during the forecast period.

What segments are covered in this report?

The Eastern Europe Surgical Robots Market report typically cover these key segments-

Product (Robotic Surgical Systems, Robotic Surgery Accessories & Instruments, Others)

Application (Laparoscopy, Neurology, Orthopedics, Gynecology, Urology, Cardiology, Other Applications)

End User (Hospitals, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for Eastern Europe Surgical Robots Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Eastern Europe Surgical Robots Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Eastern Europe Surgical Robots Market?

The Eastern Europe Surgical Robots Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Becton Dickinson and Co

Omnicell Inc

Swisslog Healthcare AG

Siemens Healthineers AG

Capsa Solutions LLC

ARxIUM

Innovation Associates

McKesson Corp

YUYAMA Manufacturing Co Ltd

ScriptPro LLC

Who should buy this report?

The Eastern Europe Surgical Robots Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Eastern Europe Surgical Robots Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Eastern Europe Surgical Robots Market

Get Free Sample For Eastern Europe Surgical Robots Market