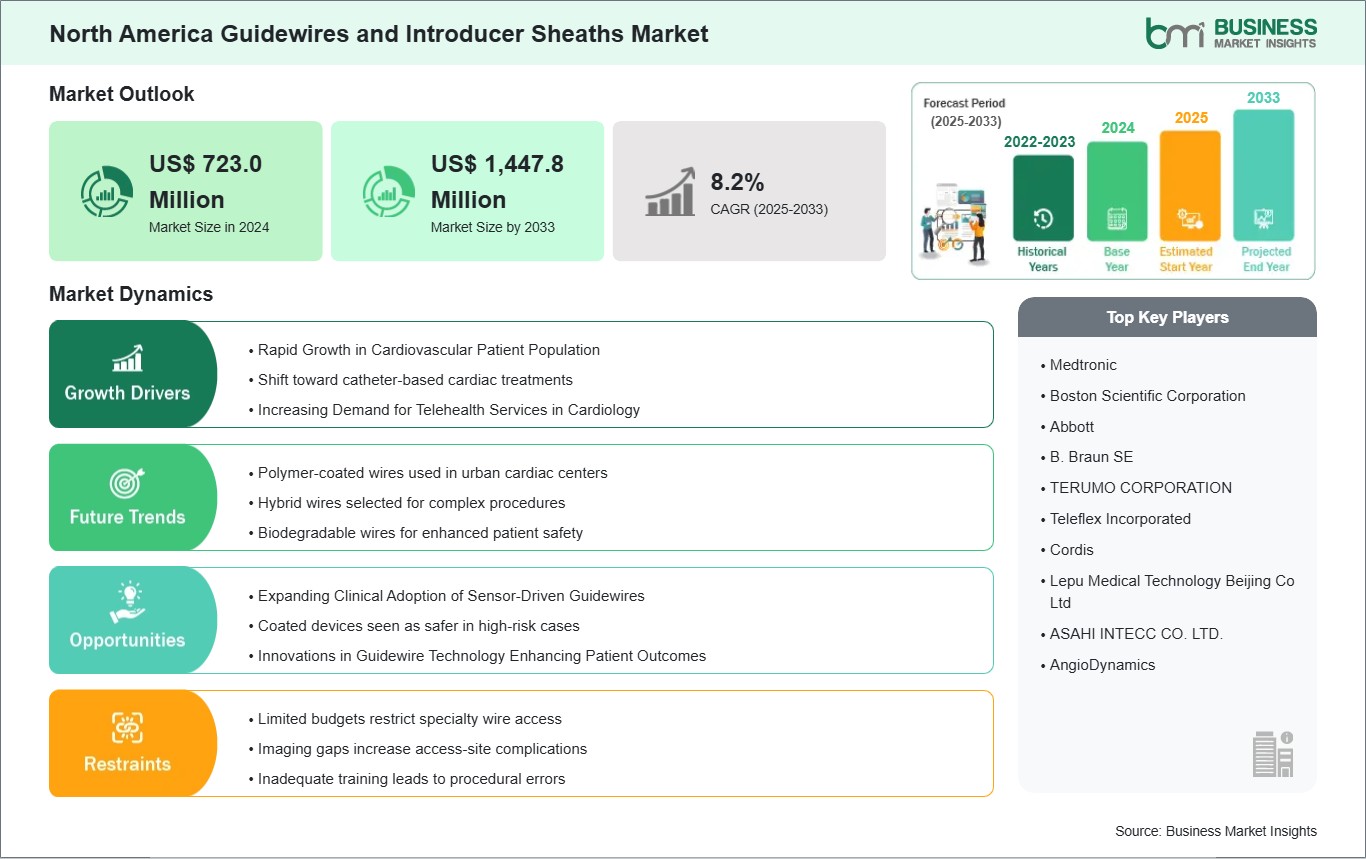

The North America guidewires and introducer sheaths market size is expected to reach US$ 1,447.8 million by 2033 from US$ 723.0 million in 2024. The market is estimated to record a CAGR of 8.2% from 2025 to 2033.

Executive Summary and North America Guidewires and Introducer Sheaths Market Analysis:

The North America guidewires and introducer sheaths market is defined by advanced hospital infrastructure, strong reimbursement frameworks, and a culture of evidence‑based adoption. Hospitals across the US and Canada are early adopters of minimally invasive cardiovascular and peripheral procedures, supported by robust imaging systems and hybrid operating rooms. A key driver is the region's emphasis on patient safety and efficiency. Clinicians prioritize guidewires with predictable tactile feedback and introducer sheaths engineered for smooth insertion, reliable hemostasis, and rapid catheter exchanges. Procurement is shaped by group purchasing organizations (GPOs), integrated delivery networks (IDNs), and hospital consortia, which negotiate long‑term contracts and favor vendors that demonstrate consistent lot quality, transparent post‑market surveillance, and sustainability in packaging. Another distinctive factor is the integration of digital health and electronic medical records, where consumables are tracked against patient outcomes and replenishment cycles.

Market restraints include strict cost‑effectiveness evaluations, competitive price pressures from bulk tenders, and regulatory requirements under the FDA and Health Canada that extend product launch timelines. Despite these challenges, North America benefits from strong government funding, private sector investment, and academic hospitals that pilot new technologies and generate clinical data for broader adoption. Hospitals remain the dominant end users, while specialized cardiovascular centers and diagnostic networks contribute by standardizing imaging‑led triage into interventional pathways. Vendors that align with GPO procurement models, sustainability initiatives, and evidence‑driven positioning are best placed to sustain growth in this sophisticated market.

North America Guidewires and Introducer Sheaths Market - Strategic Insights:

Get more information on this report

North America Guidewires and Introducer Sheaths Market Segmentation Analysis:

Key segments that contributed to the derivation of the North America guidewires and introducer sheaths market analysis are product type, coating, application, and end user.

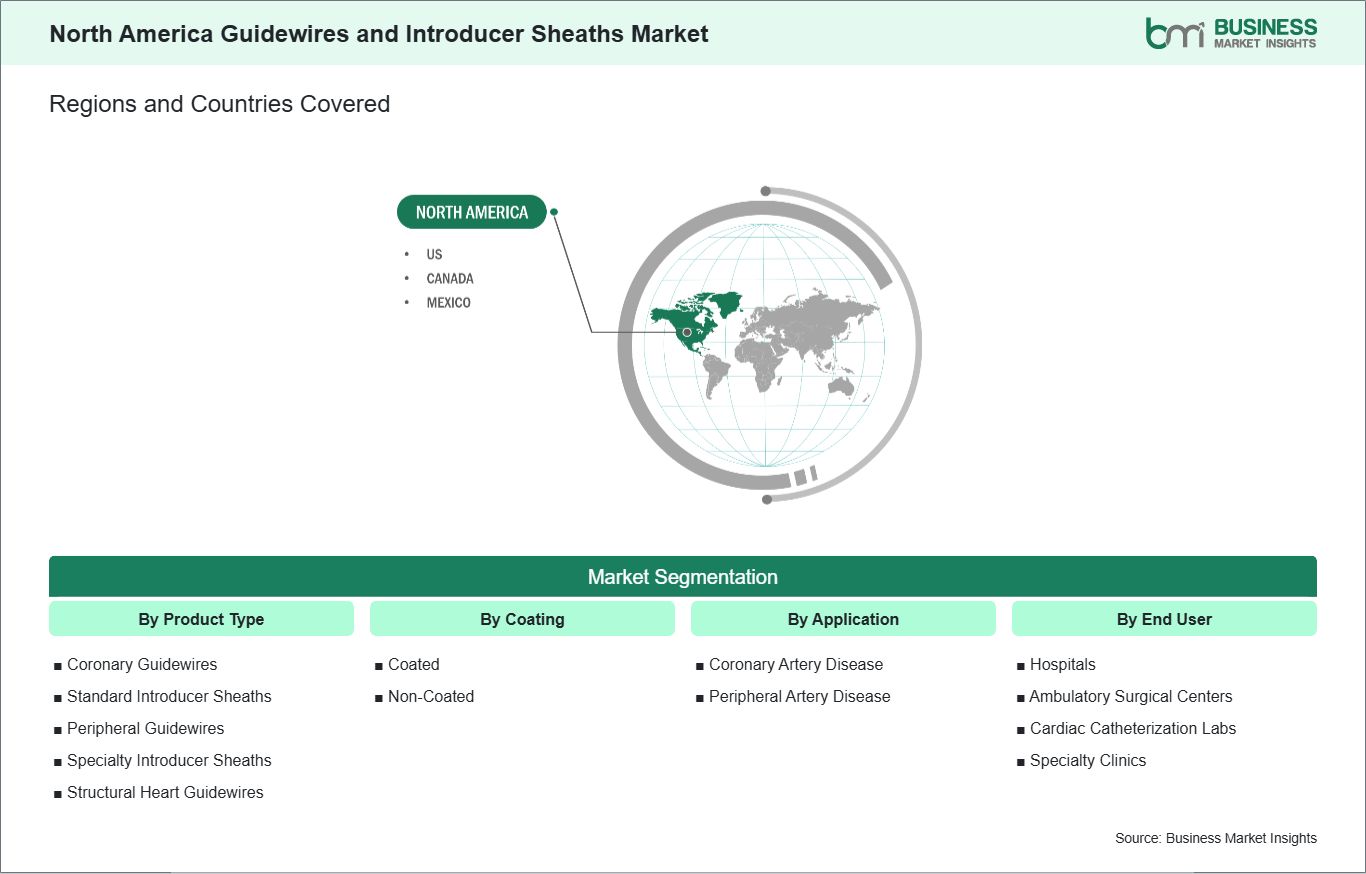

By product type, the guidewires and introducer sheaths market is segmented into coronary guidewires, standard introducer sheaths, peripheral guidewires, specialty introducer sheaths, and structural heart guidewires. The coronary guidewires segment dominated the market in 2024.

By coating, the guidewires and introducer sheaths market is bifurcated into coated and non-coated. The coated segment dominated the market in 2024.

By application, the guidewires and introducer sheaths market is segmented into coronary artery disease, peripheral artery disease, and structural heart disease. The coronary artery disease segment dominated the market in 2024.

By end user, the guidewires and introducer sheaths market is segmented into hospitals, ambulatory surgical centers, cardiac catheterization labs, and specialty clinics. The hospitals segment dominated the market in 2024.

North America Guidewires and Introducer Sheaths Market Drivers and Opportunities:

Rising Prevalence of Cardiovascular Diseases

North America continues to face one of the world's highest burdens of cardiovascular disease, driven by aging populations, obesity, diabetes, and sedentary lifestyles. In the US, heart disease remains the leading cause of death, while Canada is seeing a rising incidence of coronary artery disease and heart failure among people over 60. These trends translate into millions of diagnostic angiographies, percutaneous coronary interventions, and peripheral vascular procedures each year, creating sustained and large-scale demand for guidewires and introducer sheaths across hospitals and outpatient cardiac centers.

The region's highly developed healthcare infrastructure supports a very high volume of interventional cardiology procedures. Large hospital networks and specialized cardiac institutes in cities such as Houston, Boston, Toronto, and Los Angeles operate multiple catheterization laboratories that perform complex coronary, neurovascular, and structural heart interventions daily. These advanced procedures rely on a wide range of specialized guidewires and introducer sheaths designed for different vessel sizes, lesion types, and access routes, making these devices essential consumables within North American cath labs.

The shift toward minimally invasive treatment pathways is accelerating across North America as payers and providers aim to reduce hospital stays and overall healthcare costs. Procedures such as transcatheter aortic valve replacement (TAVR), endovascular aneurysm repair, and percutaneous coronary intervention are preferred over open surgery. Each of these therapies requires precise vascular access and navigation, increasing the utilization of high-quality guidewires and introducer sheaths. As cardiovascular disease remains a dominant healthcare challenge, these trends ensure strong, long-term market growth.

Growing Adoption of Sensor-Enabled Guidewires

North America is the global leader in the adoption of sensor-enabled guidewires, driven by its strong innovation ecosystem and widespread acceptance of advanced interventional technologies. Pressure and flow-sensing guidewires are now commonly used in US and Canadian cath labs to perform fractional flow reserve (FFR) and other physiologic assessments during coronary angiography. These measurements help cardiologists determine whether a blockage truly requires stenting, improving patient outcomes and reducing unnecessary interventions.

Major academic medical centers and large hospital systems, such as those in New York, Cleveland, and Vancouver, have incorporated sensor-enabled guidewires into standard clinical protocols for complex coronary and peripheral artery disease. Their ability to provide real-time, objective data supports more precise decision-making, especially in patients with multi-vessel disease or ambiguous lesions. This technology also aligns with the region's growing focus on value-based care, where better outcomes and efficient use of resources are rewarded.

The market is strengthened by the presence of leading medical device manufacturers and a robust clinical research environment in North America. Continuous innovation, rapid regulatory approvals, and extensive physician training programs accelerate the uptake of next-generation sensor-enabled guidewires. As healthcare providers rely on data-driven insights to guide interventional strategies, these advanced devices are becoming a standard of care, reinforcing North America's dominant position in the global guidewires and introducer sheaths market.

North America Guidewires and Introducer Sheaths Market Size and Share Analysis:

The North America Guidewires and Introducer Sheaths market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report further examines subsegments categorized within product type, coating, application, and end user, offering insights into their contribution to overall market performance.

By product type, the coronary guidewires subsegment dominated the market in 2024. Coronary guidewires dominate due to their critical role in minimally invasive procedures, the rising prevalence of coronary artery disease, and technological advancements ensuring precision, safety, and improved patient outcomes in cardiovascular interventions.

Based on coating, the coated subsegment dominated the market in 2024. Coated guidewires led the market as surface coatings enhance durability, reduce friction, improve navigation through complex vessels, and minimize complications, making them the preferred choice among physicians for efficiency and patient safety.

In terms of application, the coronary artery disease subsegment dominated the market in 2024. The coronary artery disease segment dominated as increasing global incidence, lifestyle risk factors, and demand for advanced interventional cardiology solutions drove adoption of guidewires and sheaths tailored for coronary procedures.

By end user, the hospitals subsegment dominated the market in 2024. Hospitals dominated the market since they handle the majority of complex cardiovascular interventions, offer advanced infrastructure, skilled specialists, and comprehensive patient care, making them the primary setting for guidewire and sheath usage.

North America Guidewires and Introducer Sheaths Market Report Highlights:

Report Attribute

Details

Market size in 2024

US$ 723.0 Million

Market Size by 2033

US$ 1,447.8 Million

CAGR (2025 - 2033)

8.2%

Historical Data

2022-2023

Forecast period

2025-2033

Segments Covered

By By Product Type

Coronary Guidewires

Standard Introducer Sheaths

Peripheral Guidewires

Specialty Introducer Sheaths

Structural Heart Guidewires

By By Coating

Coated

Non-Coated

By By Application

Coronary Artery Disease

Peripheral Artery Disease

By By End User

Hospitals

Ambulatory Surgical Centers

Cardiac Catheterization Labs

Specialty Clinics

Regions and Countries Covered

North America

US, Canada, Mexico

Market leaders and key company profiles

Medtronic

Boston Scientific Corporation

Abbott

B. Braun SE

TERUMO CORPORATION

Teleflex Incorporated

Cordis

Lepu Medical Technology Beijing Co Ltd

ASAHI INTECC CO. LTD.

AngioDynamics

Get more information on this report

North America Guidewires and Introducer Sheaths Market Report Coverage and Deliverables:

The "North America Guidewires and Introducer Sheaths Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

North America Guidewires and Introducer Sheaths market size and forecast at the regional and country levels for key market segments covered under the scope

North America Guidewires and Introducer Sheaths market trends, as well as market dynamics such as drivers, restraints, and key opportunities

North America Guidewires and Introducer Sheaths market analysis covering key market trends, regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the North America Guidewires and Introducer Sheaths market

Detailed company profiles, including SWOT analysis

North America Guidewires and Introducer Sheaths Market Geographic Insights:

The geographical scope of the North America Guidewires and Introducer Sheaths market report is divided into: The US, Canada, and Mexico. The US held the largest share in 2024.

The US dominates the North American market due to its scale, advanced hospital networks, and leadership in cardiovascular innovation. Hospitals across major metropolitan hubs are equipped with state‑of‑the‑art catheterization labs, driving demand for guidewires and introducer sheaths optimized for efficiency and reproducibility. Procurement is structured, with GPOs and IDNs negotiating contracts that emphasize cost efficiency, clinical evidence, and vendor service commitments. Clinicians in the US emphasize reproducibility and precision, selecting devices that integrate seamlessly into standardized care pathways and support rapid patient recovery. A distinctive feature of the US market is its integration of digital health and quality registries. Devices are tracked against patient outcomes, complication rates, and procedural efficiency, influencing procurement strategies. Growth is reinforced by partnerships with international vendors, academic hospitals piloting new consumables, and simulation‑based training programs that elevate clinician proficiency. Constraints include strict cost‑effectiveness evaluations, competitive pricing pressures, and the need for vendors to comply with rigorous regulatory standards. Nonetheless, the US benefits from a culture of innovation, collaborative procurement, and patient‑centric care models. Vendors that invest in localized training, sustainability initiatives, and evidence‑driven product positioning are best placed to deepen adoption and sustain share in this dominant North American market.

Get more information on this report

North America Guidewires and Introducer Sheaths Market Research Report Guidance:

The report includes qualitative and quantitative data in the North America Guidewires and Introducer Sheaths market across product type, coating, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the North America Guidewires and Introducer Sheaths market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the North America Guidewires and Introducer Sheaths market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the North America Guidewires and Introducer Sheaths market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover the North America Guidewires and Introducer Sheaths market segments by product type, coating, application, end user, and geography across the United States, Canada, and Mexico. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the North America Guidewires and Introducer Sheaths market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

North America Guidewires and Introducer Sheaths Market News and Key Development:

The North America Guidewires and Introducer Sheaths market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the North America guidewires and introducer sheaths market are:

In August 2025, Merit Medical Systems, Inc. announced the official launch of the Prelude Wave Hydrophilic Sheath Introducer featuring SnapFix Technology. Designed to enhance the physician's experience during vascular access, this sheath incorporates a specialized hydrophilic coating for smoother insertion and a unique hub design that provides a more secure connection. This launch targets the growing demand in the US and Canada for "slender" access tools that reduce the risk of arterial spasm and improve patient comfort during long procedures.

In April 2024, Teleflex Incorporated announced the North American launch of the Wattson Temporary Pacing Guidewire. This dual-function device is the first 0.035-inch bipolar temporary pacing guidewire designed specifically for use during Balloon Aortic Valvuloplasty (BAV) and Transcatheter Aortic Valve Replacement (TAVR).

Key Sources Referred:

The World BankWorld Health Organization (WHO)Center for Disease Control and Prevention (CDC)European Society of CardiologyAmerican College of CardiologyAmerican Heart AssociationAsian Pacific Society of Interventional CardiologyCompany WebsitesCompany Annual ReportsCompany Investor Presentations

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the North America Guidewires and Introducer Sheaths Market?

The North America Guidewires and Introducer Sheaths Market is valued at US$ 723.0 Million in 2024, it is projected to reach US$ 1,447.8 Million by 2033.

What is the CAGR for North America Guidewires and Introducer Sheaths Market by (2025 - 2033)?

As per our report North America Guidewires and Introducer Sheaths Market, the market size is valued at US$ 723.0 Million in 2024, projecting it to reach US$ 1,447.8 Million by 2033. This translates to a CAGR of approximately 8.2% during the forecast period.

What segments are covered in this report?

The North America Guidewires and Introducer Sheaths Market report typically cover these key segments-

By Product Type (Coronary Guidewires, Standard Introducer Sheaths, Peripheral Guidewires, Specialty Introducer Sheaths, Structural Heart Guidewires)

By Coating (Coated, Non-Coated)

By Application (Coronary Artery Disease, Peripheral Artery Disease)

By End User (Hospitals, Ambulatory Surgical Centers, Cardiac Catheterization Labs, Specialty Clinics)

What is the historic period, base year, and forecast period taken for North America Guidewires and Introducer Sheaths Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Guidewires and Introducer Sheaths Market report:

Historic Period : 2022-2023

Base Year : 2024

Forecast Period : 2025-2033

Who are the major players in North America Guidewires and Introducer Sheaths Market?

The North America Guidewires and Introducer Sheaths Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic

Boston Scientific Corporation

Abbott

B. Braun SE

TERUMO CORPORATION

Teleflex Incorporated

Cordis

Lepu Medical Technology Beijing Co Ltd

ASAHI INTECC CO. LTD.

AngioDynamics

Who should buy this report?

The North America Guidewires and Introducer Sheaths Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the North America Guidewires and Introducer Sheaths Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For North America Guidewires and Introducer Sheaths Market

Get Free Sample For North America Guidewires and Introducer Sheaths Market