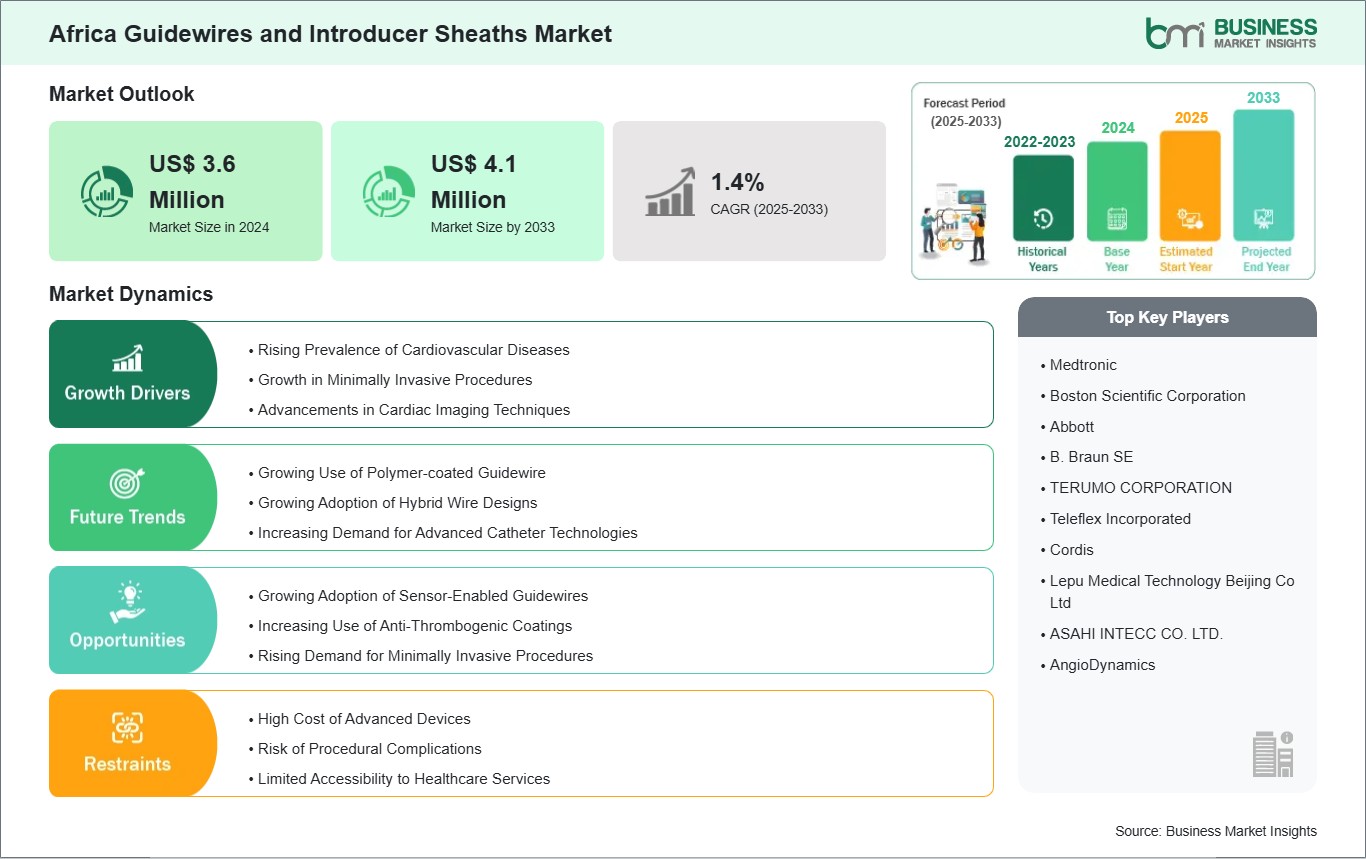

The Africa guidewires and introducer sheaths market size is expected to reach US$ 4.1 million by 2033 from US$ 3.6 million in 2024. The market is estimated to record a CAGR of 1.4% from 2025 to 2033.

Executive Summary and Africa Guidewires and Introducer Sheaths Market Analysis:

Africa's guidewires and introducer sheaths market is propelled by the expansion of interventional cardiology and peripheral vascular services in urban hubs, alongside the gradual modernization of public hospitals and steady growth in private networks. Demand is concentrated in high‑volume centers that prioritize minimally invasive procedures, favoring torque‑responsive stainless-steel guidewires for control and polymer‑coated options for trackability through tortuous anatomy. Introducer sheaths with low profiles and radial‑friendly designs are preferred to reduce access‑site complications and support faster patient turnover. Distributors play a pivotal role in training and last‑mile logistics, ensuring device availability beyond capital cities and harmonizing product use across diverse clinical settings. Key growth drivers include rising noncommunicable disease burdens, investments in catheterization labs, and structured clinician education that improves procedural consistency. Restraints stem from uneven reimbursement, import dependence, and variability in technical proficiency, which can slow adoption of advanced coatings and specialty wires in lower‑resource facilities.

Hospitals remain the primary end users, with diagnostic centers supporting imaging‑led triage into interventional pathways. Vendors that pair robust clinical support with adaptable product portfolios—spanning stainless steel and polymer‑coated guidewires, and introducer sheaths optimized for radial and femoral access—are best positioned to capture demand. Success hinges on aligning inventory, training, and procurement strategies to country‑specific workflows and regulatory timelines across the continent.

Africa Guidewires and Introducer Sheaths Market - Strategic Insights:

Get more information on this report

Africa Guidewires and Introducer Sheaths Market Segmentation Analysis:

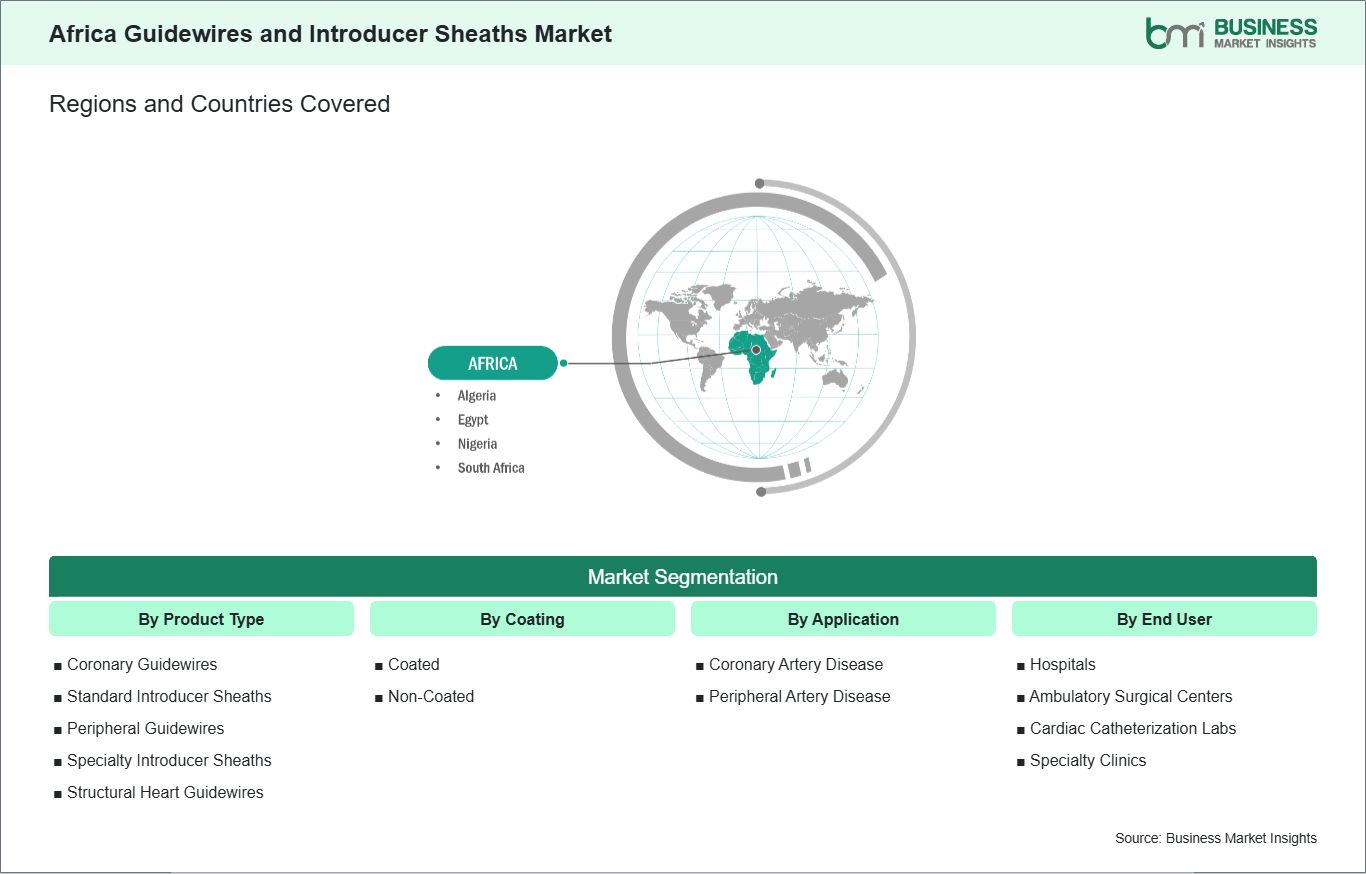

Key segments that contributed to the derivation of the Africa guidewires and introducer sheaths market analysis are product type, coating, application, and end user.

By product type, the guidewires and introducer sheaths market is segmented into coronary guidewires, standard introducer sheaths, peripheral guidewires, specialty introducer sheaths, and structural heart guidewires. The coronary guidewires segment dominated the market in 2024.

By coating, the guidewires and introducer sheaths market is bifurcated into coated and non-coated. The coated segment dominated the market in 2024.

By application, the guidewires and introducer sheaths market is segmented into coronary artery disease, peripheral artery disease, and structural heart disease. The coronary artery disease segment dominated the market in 2024.

By end user, the guidewires and introducer sheaths market is segmented into hospitals, ambulatory surgical centers, cardiac catheterization labs, and specialty clinics. The hospitals segment dominated the market in 2024.

Africa Guidewires and Introducer Sheaths Market Drivers and Opportunities:

Rising Prevalence of Cardiovascular Diseases

Africa is experiencing a rapid epidemiological transition, with cardiovascular diseases (CVDs) rising sharply due to urbanization, changing diets, tobacco use, and increasing life expectancy. Countries such as South Africa, Egypt, Nigeria, and Morocco are reporting a higher incidence of hypertension, ischemic heart disease, and stroke, placing a growing strain on stretched healthcare systems. This expanding disease burden is driving demand for interventional cardiology procedures, where guidewires and introducer sheaths are critical in accessing coronary and peripheral vessels safely and efficiently.

As CVD cases rise, major tertiary hospitals and cardiac centers across Africa are expanding their catheterization laboratory capabilities. Private hospital chains in South Africa, Egypt, and Kenya are investing in angiography suites and minimally invasive treatment programs to meet the needs of a cardiac-risk population. These investments translate into higher consumption of guidewires and introducer sheaths, which are indispensable for angioplasty, stent placement, and diagnostic catheterization procedures.

Governments and international health organizations are prioritizing noncommunicable disease management through funding, training, and infrastructure upgrades. Initiatives to improve access to cardiac care in countries such as Rwanda, Ghana, and Ethiopia are increasing procedural volumes in public hospitals. As awareness of minimally invasive cardiac treatments grows among both physicians and patients, the demand for high-quality, reliable guidewires and introducer sheaths is expected to strengthen, supporting long-term market expansion across Africa.

Growing Adoption of Sensor-Enabled Guidewires

Africa's leading cardiac centers are beginning to adopt sensor-enabled guidewires as part of a broader push toward advanced, data-driven interventional cardiology. These guidewires provide real-time measurements of pressure and flow within blood vessels, enabling clinicians to assess lesion severity more accurately and tailor interventions accordingly. Hospitals in South Africa, Egypt, and Tunisia, which host some of the continent's most advanced Cath labs, are at the forefront of introducing these technologies into routine practice.

The clinical value of sensor-enabled guidewires is significant in Africa, where late presentation of coronary artery disease is common. By offering precise physiological insights during procedures, these devices help physicians decide whether a lesion requires stenting or can be managed medically, reducing unnecessary implants and improving patient outcomes. This capability is attractive to private hospitals and cardiac institutes that are focused on improving procedural efficiency, lowering complication rates, and delivering outcomes that meet international benchmarks.

Global medical device manufacturers are strengthening their partnerships with African distributors and training centers to support the rollout of sensor-enabled technologies. Educational programs, on-site demonstrations, and bundled equipment offerings are making these advanced guidewires more accessible to cardiologists across key urban markets. As Africa continues to modernize its cardiovascular care infrastructure, the growing use of sensor-enabled guidewires is expected to create a high-value growth avenue within the guidewires and introducer sheaths market.

Africa Guidewires and Introducer Sheaths Market Size and Share Analysis:

The Africa Guidewires and Introducer Sheaths market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report further examines subsegments categorized within product type, coating, application, and end user, offering insights into their contribution to overall market performance.

By product type, the coronary guidewires subsegment dominated the market in 2024. Coronary guidewires dominate due to their critical role in minimally invasive procedures, the rising prevalence of coronary artery disease, and technological advancements ensuring precision, safety, and improved patient outcomes in cardiovascular interventions.

Based on coating, the coated subsegment dominated the market in 2024. Coated guidewires led the market as surface coatings enhance durability, reduce friction, improve navigation through complex vessels, and minimize complications, making them the preferred choice among physicians for efficiency and patient safety.

In terms of application, the coronary artery disease subsegment dominated the market in 2024. The coronary artery disease segment dominated as increasing global incidence, lifestyle risk factors, and demand for advanced interventional cardiology solutions drove adoption of guidewires and sheaths tailored for coronary procedures.

By end user, the hospitals subsegment dominated the market in 2024. Hospitals dominated the market since they handle the majority of complex cardiovascular interventions, offer advanced infrastructure, skilled specialists, and comprehensive patient care, making them the primary setting for guidewire and sheath usage.

Africa Guidewires and Introducer Sheaths Market Report Highlights:

Report Attribute

Details

Market size in 2024

US$ 3.6 Million

Market Size by 2033

US$ 4.1 Million

CAGR (2025 - 2033)

1.4%

Historical Data

2022-2023

Forecast period

2025-2033

Segments Covered

By By Product Type

Coronary Guidewires

Standard Introducer Sheaths

Peripheral Guidewires

Specialty Introducer Sheaths

Structural Heart Guidewires

By By Coating

Coated

Non-Coated

By By Application

Coronary Artery Disease

Peripheral Artery Disease

By By End User

Hospitals

Ambulatory Surgical Centers

Cardiac Catheterization Labs

Specialty Clinics

Regions and Countries Covered

Africa

Egypt, South Africa, Nigeria, Algeria

Market leaders and key company profiles

Medtronic

Boston Scientific Corporation

Abbott

B. Braun SE

TERUMO CORPORATION

Teleflex Incorporated

Cordis

Lepu Medical Technology Beijing Co Ltd

ASAHI INTECC CO. LTD.

AngioDynamics

Get more information on this report

Africa Guidewires and Introducer Sheaths Market Report Coverage and Deliverables:

The "Africa Guidewires and Introducer Sheaths Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Africa Guidewires and Introducer Sheaths market size and forecast at the regional and country levels for key market segments covered under the scope

Africa Guidewires and Introducer Sheaths market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Africa Guidewires and Introducer Sheaths market analysis covering key market trends, regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Africa Guidewires and Introducer Sheaths market

Detailed company profiles, including SWOT analysis

Africa Guidewires and Introducer Sheaths Market Geographic Insights:

The geographical scope of the Africa Guidewires and Introducer Sheaths market report is divided into Nigeria, Egypt, South Africa, and Algeria. South Africa held the largest share in 2024.

South Africa leads the regional market due to its mature private hospital systems, advanced tertiary centers, and ongoing upgrades in public facilities that sustain high procedural volumes. Clinicians adopt hydrophilic‑coated guidewires for complex anatomies and prefer introducer sheaths designed for radial access to minimize complications and enable shorter stays, reflecting a strong tilt toward minimally invasive care. Procurement is split between direct purchasing by large hospital groups and established distributors that provide technical support, in‑service training, and a reliable supply of specialty SKUs, ensuring consistency across provinces. Growth is reinforced by investments in catheterization labs, structured training pathways, and multidisciplinary teams that standardize device selection for cardiovascular and peripheral interventions. Constraints include budget variability in public institutions, reimbursement differences for advanced consumables, and occasional supply chain friction that encourages dual sourcing and inventory buffers. South Africa's market also benefits from data‑driven planning and clinical governance that refine product mix, balancing torque‑responsive stainless steel wires with polymer‑coated variants for trackability, and selecting sheath profiles that match access strategies. Hospitals remain the dominant end users, while diagnostic centers support imaging‑led triage into interventional care. Vendors that align education, inventory management, and product breadth with South Africa's procurement models and clinical workflows are best placed to deepen adoption and sustain share.

Get more information on this report

Africa Guidewires and Introducer Sheaths Market Research Report Guidance:

The report includes qualitative and quantitative data in the Africa Guidewires and Introducer Sheaths market across product type, coating, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Africa Guidewires and Introducer Sheaths market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Africa Guidewires and Introducer Sheaths market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Africa Guidewires and Introducer Sheaths market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover the Africa Guidewires and Introducer Sheaths market segments by product type, coating, application, end user, and geography across Nigeria, Egypt, South Africa, and Algeria. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Africa Guidewires and Introducer Sheaths market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Africa Guidewires and Introducer Sheaths Market News and Key Development:

The Africa Guidewires and Introducer Sheaths market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Africa guidewires and introducer sheaths market are:

In April 2025, Boston Scientific announced that it had launched its new Kinetix Guidewire, designed to provide enhanced torque control for use in percutaneous coronary intervention (PCI) procedures, which is a key advancement in guidewire technology that companies serving the Africa/Middle East & Africa markets can distribute regionally.

In October 2024, Boston Scientific announced that it had launched its Journey Guidewire (0.014″), developed for challenging small-vessel peripheral angioplasty procedures, which is an expansion of its guidewire portfolio with implications for interventional cardiology offerings worldwide, including MEA distribution networks

Key Sources Referred:

The World Bank

World Health Organization (WHO)

Center for Disease Control and Prevention (CDC)

European Society of Cardiology

American College of Cardiology

American Heart Association

Asian Pacific Society of Interventional Cardiology

Company Websites

Company Annual Reports

Company Investor Presentations

Identical Market Reports with other Region/Countries

The List of Companies - Africa Guidewires and Introducer Sheaths Market

Medtronic

Boston Scientific Corporation

Abbott

B. Braun SE

TERUMO CORPORATION

Teleflex Incorporated

Cordis

Lepu Medical Technology Beijing Co Ltd

ASAHI INTECC CO. LTD.

AngioDynamics

Frequently Asked Questions

How big is the Africa Guidewires and Introducer Sheaths Market?

The Africa Guidewires and Introducer Sheaths Market is valued at US$ 3.6 Million in 2024, it is projected to reach US$ 4.1 Million by 2033.

What is the CAGR for Africa Guidewires and Introducer Sheaths Market by (2025 - 2033)?

As per our report Africa Guidewires and Introducer Sheaths Market, the market size is valued at US$ 3.6 Million in 2024, projecting it to reach US$ 4.1 Million by 2033. This translates to a CAGR of approximately 1.4% during the forecast period.

What segments are covered in this report?

The Africa Guidewires and Introducer Sheaths Market report typically cover these key segments-

By Product Type (Coronary Guidewires, Standard Introducer Sheaths, Peripheral Guidewires, Specialty Introducer Sheaths, Structural Heart Guidewires)

By Coating (Coated, Non-Coated)

By Application (Coronary Artery Disease, Peripheral Artery Disease)

By End User (Hospitals, Ambulatory Surgical Centers, Cardiac Catheterization Labs, Specialty Clinics)

What is the historic period, base year, and forecast period taken for Africa Guidewires and Introducer Sheaths Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Africa Guidewires and Introducer Sheaths Market report:

Historic Period : 2022-2023

Base Year : 2024

Forecast Period : 2025-2033

Who are the major players in Africa Guidewires and Introducer Sheaths Market?

The Africa Guidewires and Introducer Sheaths Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic

Boston Scientific Corporation

Abbott

B. Braun SE

TERUMO CORPORATION

Teleflex Incorporated

Cordis

Lepu Medical Technology Beijing Co Ltd

ASAHI INTECC CO. LTD.

AngioDynamics

Who should buy this report?

The Africa Guidewires and Introducer Sheaths Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Africa Guidewires and Introducer Sheaths Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Africa Guidewires and Introducer Sheaths Market

Get Free Sample For Africa Guidewires and Introducer Sheaths Market