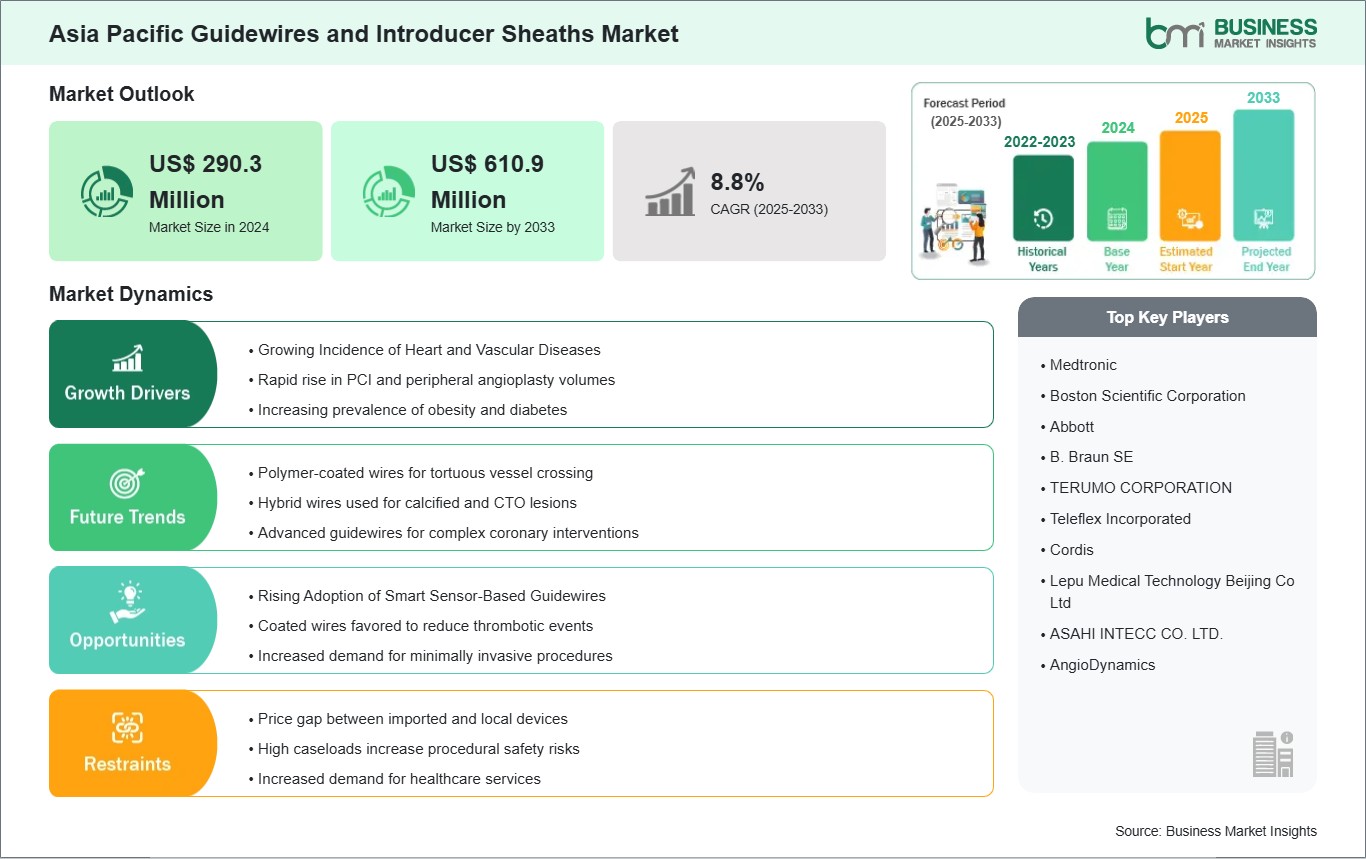

The Asia Pacific guidewires and introducer sheaths market size is expected to reach US$ 610.9 million by 2033 from US$ 290.3 million in 2024. The market is estimated to record a CAGR of 8.8% from 2025 to 2033.

Executive Summary and Asia Pacific Guidewires and Introducer Sheaths Market Analysis:

Asia Pacific guidewires and introducer sheaths market is defined by high procedural diversity—from complex coronary interventions in advanced centers to expanding peripheral programs in emerging health systems—underpinned by rapid imaging adoption, cross‑border training ecosystems, and hospital consolidation. Demand is shaped by the region's push for day‑care interventional models, where device choices emphasize smooth vessel navigation, consistent tactile feedback, and sheath designs that minimize tissue trauma while supporting swift turnover. Procurement strategies vary widely: integrated hospital groups in developed markets favor standardized formularies and vendor scorecards, while fast‑growing systems in Southeast and South Asia rely on agile distributors to bridge inventory gaps and provide on‑site proctoring. A distinct driver is the surge in hybrid ORs and cath labs that blend cardiovascular and endovascular workflows, prompting hospitals to prefer multi‑indication guidewire families and sheath platforms compatible with varied access strategies.

Restraints include fragmented reimbursement for consumables, uneven sterilization and reprocessing protocols, and regulatory heterogeneity that complicates synchronized product launches. The competitive edge hinges on clinical education embedded within service contracts, device traceability for quality governance, and packaging that supports sterile field efficiency. Hospitals remain the core end users, with specialized centers accelerating adoption through protocolized pathways and outcome benchmarking. Vendors that align portfolio breadth with country‑specific clinical pathways, while optimizing training and logistics for high‑throughput environments, are best positioned to sustain momentum across Asia Pacific.

Asia Pacific Guidewires and Introducer Sheaths Market - Strategic Insights:

Get more information on this report

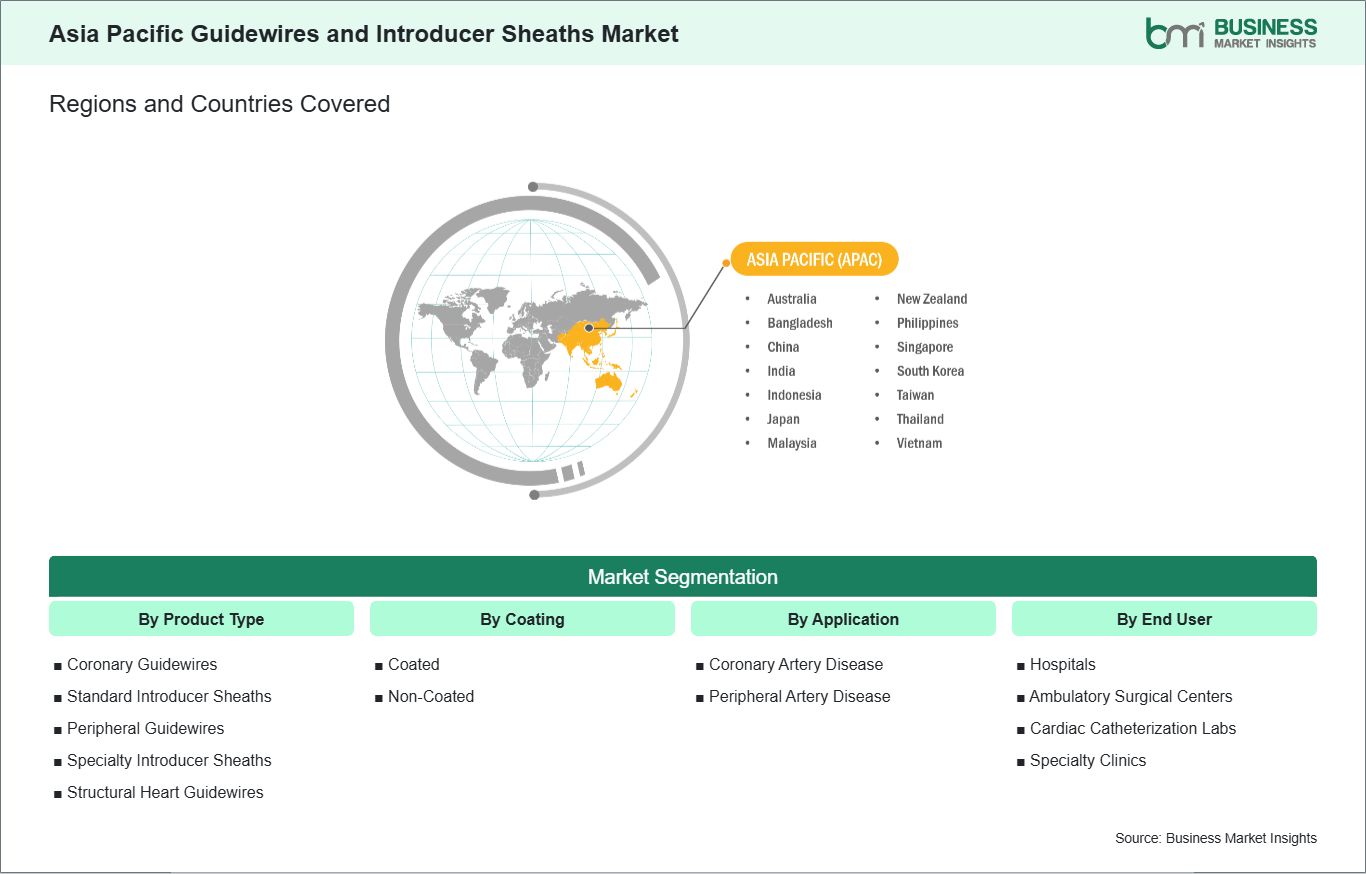

Asia Pacific Guidewires and Introducer Sheaths Market Segmentation Analysis:

Key segments that contributed to the derivation of the Asia Pacific guidewires and introducer sheaths market analysis are product type, coating, application, and end user.

By product type, the guidewires and introducer sheaths market is segmented into coronary guidewires, standard introducer sheaths, peripheral guidewires, specialty introducer sheaths, and structural heart guidewires. The coronary guidewires segment dominated the market in 2024.

By coating, the guidewires and introducer sheaths market is bifurcated into coated and non-coated. The coated segment dominated the market in 2024.

By application, the guidewires and introducer sheaths market is segmented into coronary artery disease, peripheral artery disease, and structural heart disease. The coronary artery disease segment dominated the market in 2024.

By end user, the guidewires and introducer sheaths market is segmented into hospitals, ambulatory surgical centers, cardiac catheterization labs, and specialty clinics. The hospitals segment dominated the market in 2024.

Asia Pacific Guidewires and Introducer Sheaths Market Drivers and Opportunities:

Rising Prevalence of Cardiovascular Diseases

Asia Pacific has emerged as the global epicenter of cardiovascular disease (CVD) burden. According to a forecast analysis published in The Lancet Regional Health, Southeast Asia in August 2024, the crude prevalence of CVDs in Asia is projected to reach 729.5 million cases by 2050, representing a 109% increase from 2025 levels. This staggering rise is driven by aging populations in East Asia and rapid urbanization in South Asia. Consequently, healthcare systems are prioritizing the procurement of essential interventional tools, with guidewires and introducer sheaths seeing high-volume adoption to manage ischemic heart disease and peripheral artery conditions.

To combat this rising mortality, regional healthcare providers are aggressively expanding their interventional capabilities. In October 2025, Terumo India announced the launch of the FineCross M3 Coronary Micro-Guide Catheter, a device specifically engineered to enhance navigability and guidewire support during complex percutaneous coronary interventions (PCI). Such developments reflect a broader regional trend where medical device manufacturers are tailoring high-performance access tools to the complex vascular anatomies found in the region's aging and diabetic patient cohorts.

The shift toward minimally invasive surgery (MIS) continues to gain momentum across the region. In October 2025, Boston Scientific announced the global launch of the Journey Guidewire, a specialized 0.014-inch tool designed for challenging small-vessel peripheral angioplasty. This launch, which targeted major Asian medical hubs, underscores the critical role of advanced guidewire technology in meeting the demand for limb-salvage and complex vascular procedures. As governments in China and India continue to expand insurance coverage for these minimally invasive techniques, the demand for reliable, high-quality introducer sheaths and guidewires is expected to remain a cornerstone of the regional market.

Growing Adoption of Sensor-Enabled Guidewires

Asia Pacific is witnessing a rapid transition toward "smart" cardiology, characterized by the growing adoption of sensor-enabled guidewires that provide real-time physiological data. In March 2025, Abbott introduced an upgraded FFR (Fractional Flow Reserve) guidewire system specifically designed to enhance diagnostic precision in complex coronary lesions. By integrating miniaturized sensors directly into the guidewire, this technology allows physicians in high-volume Asian cath labs to make data-driven decisions on stenting, thereby reducing procedural complications and optimizing hospital resources.

The demand for these advanced diagnostic tools is strong in Japan and South Korea, where evidence-based medicine is central to clinical practice. A market report from Data Bridge Market Research in November 2025 highlighted that flexible-tipped pressure guidewires held a dominant market share of 52.8% within the pressure wire segment, owing to their superior performance in navigating the tortuous coronary arteries common in elderly patients. This trend is being bolstered by clinical validation; for instance, a multi-center study involving Japanese researchers validated new diastolic pressure ratio (dPR) workflows, which simplify the use of sensor-enabled wires in daily practice.

Strategic partnerships are also playing a vital role in localizing these advanced technologies. In February 2024, BIOTRONIK collaborated with IMDS to launch the micro Rx catheter, designed to work in tandem with high-performance guidewires for interventional cardiac applications. Additionally, in September 2024, Viz.ai partnered with Cleerly to develop an AI-based platform for heart disease diagnosis, which integrates with data from interventional devices. As Asia Pacific continues to modernize its healthcare infrastructure, the integration of sensor-enabled guidewires with digital diagnostic platforms is positioning the region as a leader in the global shift toward precision interventional cardiology.

Asia Pacific Guidewires and Introducer Sheaths Market Size and Share Analysis:

The Asia Pacific Guidewires and Introducer Sheaths market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report further examines subsegments categorized within product type, coating, application, and end user, offering insights into their contribution to overall market performance.

By product type, the coronary guidewires subsegment dominated the market in 2024. Coronary guidewires dominate due to their critical role in minimally invasive procedures, the rising prevalence of coronary artery disease, and technological advancements ensuring precision, safety, and improved patient outcomes in cardiovascular interventions.

Based on coating, the coated subsegment dominated the market in 2024. Coated guidewires led the market as surface coatings enhance durability, reduce friction, improve navigation through complex vessels, and minimize complications, making them the preferred choice among physicians for efficiency and patient safety.

In terms of application, the coronary artery disease subsegment dominated the market in 2024. The coronary artery disease segment dominated as increasing global incidence, lifestyle risk factors, and demand for advanced interventional cardiology solutions drove adoption of guidewires and sheaths tailored for coronary procedures.

By end user, the hospitals subsegment dominated the market in 2024. Hospitals dominated the market since they handle the majority of complex cardiovascular interventions, offer advanced infrastructure, skilled specialists, and comprehensive patient care, making them the primary setting for guidewire and sheath usage.

Asia Pacific Guidewires and Introducer Sheaths Market Report Highlights:

Report Attribute

Details

Market size in 2024

US$ 290.3 Million

Market Size by 2033

US$ 610.9 Million

CAGR (2025 - 2033)

8.8%

Historical Data

2022-2023

Forecast period

2025-2033

Segments Covered

By By Product Type

Coronary Guidewires

Standard Introducer Sheaths

Peripheral Guidewires

Specialty Introducer Sheaths

Structural Heart Guidewires

By By Coating

Coated

Non-Coated

By By Application

Coronary Artery Disease

Peripheral Artery Disease

By By End User

Hospitals

Ambulatory Surgical Centers

Cardiac Catheterization Labs

Specialty Clinics

Regions and Countries Covered

Asia Pacific

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

Market leaders and key company profiles

Medtronic

Boston Scientific Corporation

Abbott

B. Braun SE

TERUMO CORPORATION

Teleflex Incorporated

Cordis

Lepu Medical Technology Beijing Co Ltd

ASAHI INTECC CO. LTD.

AngioDynamics

Get more information on this report

Asia Pacific Guidewires and Introducer Sheaths Market Report Coverage and Deliverables:

The "Asia Pacific Guidewires and Introducer Sheaths Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Asia Pacific Guidewires and Introducer Sheaths market size and forecast at the regional and country levels for key market segments covered under the scope

Asia Pacific Guidewires and Introducer Sheaths market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Asia Pacific Guidewires and Introducer Sheaths market analysis covering key market trends, regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Asia Pacific Guidewires and Introducer Sheaths market

Detailed company profiles, including SWOT analysis

Asia Pacific Guidewires and Introducer Sheaths Market Geographic Insights:

The geographical scope of the Asia Pacific Guidewires and Introducer Sheaths market report is divided into: China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. China held the largest share in 2024.

China dominates the regional market through scale, speed of cath lab deployment, and a strong emphasis on domestically engineered consumables that meet national procurement priorities. Hospitals adopt standardized device kits—guidewires, introducer sheaths, and ancillary accessories pre‑configured for coronary, neurovascular, or peripheral pathways—to reduce variability and accelerate turnover in busy centers. Clinical teams favor sheath platforms that integrate reliable hemostasis valves, smooth dilator transitions, and packaging designed for rapid sterile field setup, reflecting a system‑wide focus on efficiency and predictable workflows. Centralized tenders shape procurement and volume‑based purchasing alliances, which reward manufacturers that demonstrate consistent batch performance, robust post‑market surveillance, and responsive technical service. A notable feature is the integration of digital traceability—QR‑coded consumables linked to hospital quality systems—enabling real‑time monitoring of device usage, adverse events, and replenishment cycles. Growth is reinforced by national training networks, fellowship exchanges, and simulation labs that codify escalation strategies and access planning across diverse anatomies. Constraints include periodic price compression from bulk tenders, documentation demands for localized clinical evidence, and regional disparities in operator experience that necessitate on‑site proctoring. Diagnostic centers contribute by standardizing imaging protocols that inform access site selection and device kit composition, improving downstream cath lab efficiency. Vendors that localize product design, invest in field education, and align with China's data‑driven procurement and quality governance are best placed to deepen adoption and sustain share.

Get more information on this report

Asia Pacific Guidewires and Introducer Sheaths Market Research Report Guidance:

The report includes qualitative and quantitative data in the Asia Pacific Guidewires and Introducer Sheaths market across product type, coating, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Asia Pacific Guidewires and Introducer Sheaths market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Asia Pacific Guidewires and Introducer Sheaths market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Asia Pacific Guidewires and Introducer Sheaths market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover the Asia Pacific Guidewires and Introducer Sheaths market segments by product type, coating, application, end user, and geography across China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia Pacific. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Asia Pacific Guidewires and Introducer Sheaths market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Asia Pacific Guidewires and Introducer Sheaths Market News and Key Development:

The Asia Pacific Guidewires and Introducer Sheaths market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Asia Pacific guidewires and introducer sheaths market are:

In December 2024, Teleflex Incorporated announced the launch of its new Pressure Injectable Arrowg+ard Blue Plus MSB Procedure Kit in Europe, the Middle East, and Africa (EMEA). This kit is a major addition to their vascular access portfolio, featuring a kink-resistant Nitinol guidewire and a specialized dilator that reduces vessel penetration force by up to 72% compared to standard models, facilitating safer and more efficient sheath introduction for critically ill patients.

In November 2024, APT Medical announced that its Braidin Pro adjustable valve large sheath and Distail microcatheter successfully received CE certification under the European Union Medical Device Regulation (MDR). The Braidin Pro is designed for complex peripheral and structural heart interventions, offering an adjustable hemostasis valve that allows for the delivery of various device sizes while maintaining effective sealing and minimizing vascular trauma.

Key Sources Referred:

The World BankWorld Health Organization (WHO)Center for Disease Control and Prevention (CDC)European Society of CardiologyAmerican College of CardiologyAmerican Heart AssociationAsian Pacific Society of Interventional CardiologyCompany WebsitesCompany Annual ReportsCompany Investor Presentations

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Asia Pacific Guidewires and Introducer Sheaths Market?

The Asia Pacific Guidewires and Introducer Sheaths Market is valued at US$ 290.3 Million in 2024, it is projected to reach US$ 610.9 Million by 2033.

What is the CAGR for Asia Pacific Guidewires and Introducer Sheaths Market by (2025 - 2033)?

As per our report Asia Pacific Guidewires and Introducer Sheaths Market, the market size is valued at US$ 290.3 Million in 2024, projecting it to reach US$ 610.9 Million by 2033. This translates to a CAGR of approximately 8.8% during the forecast period.

What segments are covered in this report?

The Asia Pacific Guidewires and Introducer Sheaths Market report typically cover these key segments-

By Product Type (Coronary Guidewires, Standard Introducer Sheaths, Peripheral Guidewires, Specialty Introducer Sheaths, Structural Heart Guidewires)

By Coating (Coated, Non-Coated)

By Application (Coronary Artery Disease, Peripheral Artery Disease)

By End User (Hospitals, Ambulatory Surgical Centers, Cardiac Catheterization Labs, Specialty Clinics)

What is the historic period, base year, and forecast period taken for Asia Pacific Guidewires and Introducer Sheaths Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Guidewires and Introducer Sheaths Market report:

Historic Period : 2022-2023

Base Year : 2024

Forecast Period : 2025-2033

Who are the major players in Asia Pacific Guidewires and Introducer Sheaths Market?

The Asia Pacific Guidewires and Introducer Sheaths Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic

Boston Scientific Corporation

Abbott

B. Braun SE

TERUMO CORPORATION

Teleflex Incorporated

Cordis

Lepu Medical Technology Beijing Co Ltd

ASAHI INTECC CO. LTD.

AngioDynamics

Who should buy this report?

The Asia Pacific Guidewires and Introducer Sheaths Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Asia Pacific Guidewires and Introducer Sheaths Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Asia Pacific Guidewires and Introducer Sheaths Market

Get Free Sample For Asia Pacific Guidewires and Introducer Sheaths Market