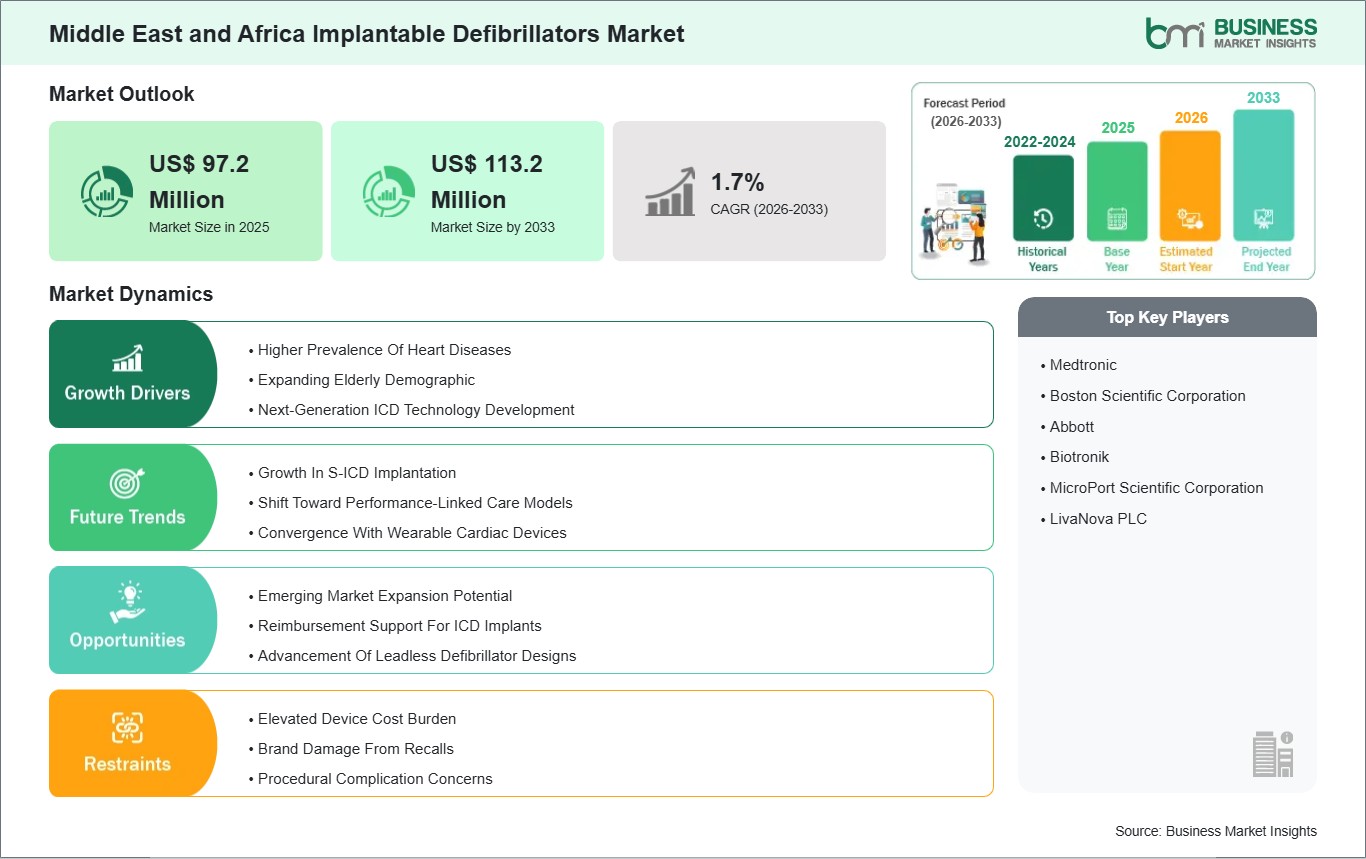

The Middle East and Africa implantable defibrillators market size is expected to reach US$ 113.2 million by 2033 from US$ 97.2 million in 2025. The market is estimated to record a CAGR of 1.7% from 2026 to 2033.

Executive Summary and Middle East and Africa Implantable Defibrillators Market Analysis:

The Middle East and Africa implantable defibrillators market reflects a heterogeneous but progressively evolving landscape characterized by widening access to advanced cardiac care technologies amidst persistent structural challenges. Across the region, demand for implantable defibrillators is buoyed by rising incidence of cardiovascular diseases, increasing awareness of sudden cardiac death prevention, and expanding healthcare services, particularly in urban centers and high-income economies. Regional healthcare infrastructure improvements and investments in electrophysiology and cardiac intervention capabilities have supported device adoption in specialist hospitals and cardiac centers throughout the Middle East and select African markets. Collaboration between global device manufacturers and regional healthcare providers has played an important role in introducing technologically advanced ICD variants to clinicians and patients across the region.

The market contends with constraints related to affordability, uneven reimbursement frameworks, and a shortage of highly trained cardiac electrophysiologists in several countries. Fragmented regulatory processes across the combined Middle Eastern and African landscape also contribute to delayed product introductions and inconsistent access to next-generation defibrillation devices. Moreover, disparities in healthcare spending between wealthier Gulf Cooperation Council (GCC) nations and lower-income African markets shape distinct adoption curves, making uniform market development strategies challenging for manufacturers.

Middle East and Africa Implantable Defibrillators Market - Strategic Insights:

Get more information on this report

Middle East and Africa Implantable Defibrillators Market Segmentation Analysis:

Key segments that contributed to the derivation of the Middle East and Africa Implantable Defibrillators market analysis are product type, patient type, and end user.

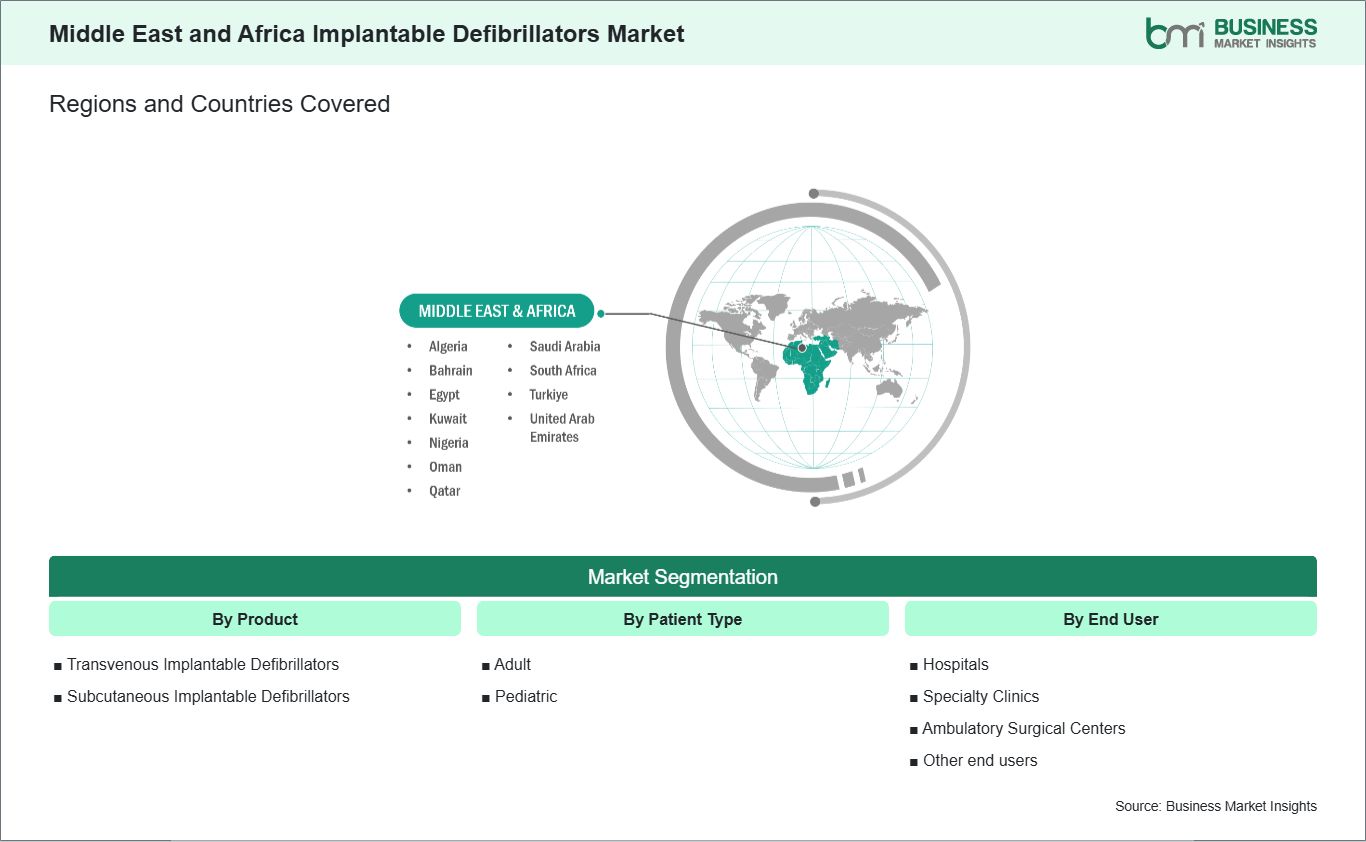

By product type, the implantable defibrillators market is segmented into transvenous implantable defibrillators and subcutaneous implantable defibrillators. The transvenous implantable defibrillators segment dominated the market in 2025.

Based on patient type, the implantable defibrillators market is classified into adult and pediatric. The adult segment dominated the market in 2025.

In terms of end user, the implantable defibrillators market is categorized into hospitals, specialty clinics, ambulatory surgical centers, and others. The hospitals segment dominated the market in 2025.

Middle East and Africa Implantable Defibrillators Market Drivers and Opportunities:

Higher Prevalence of Heart Diseases

The Middle East and Africa is experiencing a growing prevalence of heart diseases, particularly coronary artery disease and serious heart rhythm disorders. Rapid urbanization, sedentary lifestyles, unhealthy diets, smoking, and rising cases of diabetes are contributing to the increasing burden of cardiovascular conditions. In several Middle Eastern countries, lifestyle-related risk factors are highly common, leading to a greater number of patients at risk of sudden cardiac arrest. This rising disease burden is increasing the need for effective cardiac rhythm management solutions such as implantable cardioverter defibrillators (ICDs).

Healthcare infrastructure in parts of the Middle East, especially in countries such as Saudi Arabia, the UAE, and Qatar, is well developed and equipped with advanced cardiac centers. These facilities are capable of performing ICD implantation procedures and managing complex heart conditions. In Africa, although access varies widely between countries, leading urban hospitals are gradually improving their cardiac care capabilities. Growing awareness among physicians about sudden cardiac death prevention is also supporting ICD adoption.

As the number of high-risk cardiac patients continues to rise, healthcare providers are focusing more on long-term disease management and prevention strategies. ICD therapy is recognized as an important treatment option for eligible patients. The higher prevalence of heart diseases acts as a strong driver for the ICD market in the Middle East and Africa.

Reimbursement Support for ICD Implants

Reimbursement support for ICD implants in the Middle East and Africa varies across countries, but positive developments are creating new opportunities. In wealthier Middle Eastern nations, public healthcare systems and government-funded insurance programs often cover advanced cardiac procedures, including ICD implantation for eligible patients. This financial support reduces out-of-pocket costs and encourages wider adoption of the therapy.

Private healthcare also plays an important role in the region. Many patients in the Gulf countries rely on private insurance plans that provide coverage for specialized cardiac treatments. As insurance penetration increases, more patients gain access to ICD implants. Hospitals and cardiac centers are therefore more willing to invest in advanced device technologies, supported by clearer reimbursement pathways.

In several African countries, reimbursement systems are still developing, and access to ICD therapy remains limited in some areas. However, healthcare reforms and international partnerships are gradually strengthening funding mechanisms for critical treatments. As governments focus on improving outcomes for non-communicable diseases, support for life-saving cardiac devices is expected to improve. Expanding reimbursement support presents a meaningful opportunity for ICD manufacturers to grow their presence in the Middle East and Africa market.

Middle East and Africa Implantable Defibrillators Market Size and Share Analysis:

The Middle East and Africa implantable defibrillators market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within product type, patient type, and end user, highlighting their respective contributions to overall market performance.

By product type, the transvenous implantable defibrillators subsegment dominated the market in 2025, due to established clinical efficacy, broader physician familiarity, proven long-term outcomes, wider availability, and strong adoption in treating high-risk cardiac patients compared to newer subcutaneous options.

In terms of patient type, the adult subsegment dominated the market in 2025. This leadership is attributed to the higher prevalence of cardiac disorders in the adult population, increased awareness of sudden cardiac death prevention, and greater accessibility of advanced defibrillator therapies for adult patients.

Based on end user, the hospitals subsegment dominated the market in 2025. Hospitals remain the primary distribution channel due to their comprehensive cardiac care facilities, access to trained cardiologists and specialized technicians, advanced monitoring infrastructure, and ability to provide immediate, life-saving interventions.

Middle East and Africa Implantable Defibrillators Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 97.2 Million

Market Size by 2033

US$ 113.2 Million

CAGR (2026 - 2033)

1.7%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Transvenous Implantable Defibrillators

Subcutaneous Implantable Defibrillators

By Patient Type

Adult

Pediatric

By End User

Hospitals

Specialty Clinics

Ambulatory Surgical Centers

Other end users

Regions and Countries Covered

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Medtronic

Boston Scientific Corporation

Abbott

Biotronik

MicroPort Scientific Corporation

LivaNova PLC

Get more information on this report

Middle East and Africa Implantable Defibrillators Market Report Coverage and Deliverables:

The "Middle East and Africa Implantable Defibrillators Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Middle East and Africa Implantable Defibrillators market size and forecast at regional and country levels for all market segments covered under the scope

Middle East and Africa Implantable Defibrillators market trends, as well as drivers, restraints, and opportunities

Middle East and Africa Implantable Defibrillators market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Middle East and Africa Implantable Defibrillators market

Detailed company profiles, including SWOT analysis

Middle East and Africa Implantable Defibrillators Market Geographic Insights:

The geographical scope of the Middle East and Africa Implantable Defibrillators market report is divided into: Saudi Arabia, the United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria, and the Rest of MEA. Turkiye held the largest share in 2025.

In the Middle East & Africa context, Turkiye stands out as a pivotal market for implantable defibrillators, supported by a relatively mature medical device ecosystem and a robust network of cardiac care facilities. Within the country's active implantable medical devices segment, ICDs maintain a leading position, reflecting strong clinical engagement and integration into cardiovascular therapeutic protocols. Local healthcare providers, particularly in major metropolitan areas such as Istanbul and Ankara, have adopted advanced ICD technologies, including transvenous and subcutaneous systems, driven by growing clinical recognition of arrhythmia management and preventive cardiology.

Turkiye's role as a regional medical technology hub is reinforced by its strategic geographical position and growing manufacturing capabilities, which support domestic distribution and regional export potential for cardiac devices. Public-private collaborations and training initiatives for cardiac specialists have enhanced procedural competencies and helped bridge gaps in clinical expertise. Nevertheless, cost sensitivity and variability in insurance reimbursement remain notable factors influencing ICD uptake, particularly outside major urban centers. Additionally, broader economic dynamics and regulatory alignment with European and international standards continue to shape the competitive landscape for global and local ICD suppliers within the country.

Get more information on this report

Middle East and Africa Implantable Defibrillators Market Research Report Guidance:

The report includes qualitative and quantitative data in the Middle East and Africa Implantable Defibrillators market across product type, patient type, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Middle East and Africa Implantable Defibrillators market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Middle East and Africa Implantable Defibrillators market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Middle East and Africa Implantable Defibrillators market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Middle East and Africa Implantable Defibrillators market segments by product type, patient type, end user, and geography across Saudi Arabia, the United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria, and the Rest of MEA. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Middle East and Africa Implantable Defibrillators market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Middle East and Africa Implantable Defibrillators Market News and Key Development:

The Middle East and Africa implantable defibrillators market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Middle East and Africa implantable defibrillators market are:

In May 2024, Boston Scientific announced that it received regional regulatory approvals for its MRI-compatible EMBLEM MRI Subcutaneous Implantable Cardioverter Defibrillator (S-ICD) System, enabling expanded availability of the device in the Middle East & Africa to support advanced sudden cardiac arrest therapy without transvenous leads. While global product details from Boston Scientific's S-ICD portfolio indicate worldwide regulatory adoption, including in major markets, the company has been actively promoting these systems to electrophysiology centers in the Middle East & Africa, given rising cardiac care demand.

In January 2025, BIOTRONIK announced strategic expansion of its cardiac rhythm management product offerings—including subcutaneous and transvenous implantable cardioverter defibrillator systems—through its presence in the Middle East via BIOTRONIK Middle East FZE, strengthening product access and support for ICD therapies across Gulf Cooperation Council countries and broader MEA healthcare markets.

Key Sources Referred:

The World BankWorld Health Organization (WHO)Center for Disease Control and Prevention (CDC)European Database on Medical Devices (EUDAMED)European Society of CardiologyAmerican College of CardiologyAmerican Heart AssociationCompany WebsitesCompany Annual ReportsCompany Investor Presentations

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Middle East and Africa Implantable Defibrillators Market?

The Middle East and Africa Implantable Defibrillators Market is valued at US$ 97.2 Million in 2025, it is projected to reach US$ 113.2 Million by 2033.

What is the CAGR for Middle East and Africa Implantable Defibrillators Market by (2026 - 2033)?

As per our report Middle East and Africa Implantable Defibrillators Market, the market size is valued at US$ 97.2 Million in 2025, projecting it to reach US$ 113.2 Million by 2033. This translates to a CAGR of approximately 1.7% during the forecast period.

What segments are covered in this report?

The Middle East and Africa Implantable Defibrillators Market report typically cover these key segments-

End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Other end users)

What is the historic period, base year, and forecast period taken for Middle East and Africa Implantable Defibrillators Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East and Africa Implantable Defibrillators Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Middle East and Africa Implantable Defibrillators Market?

The Middle East and Africa Implantable Defibrillators Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic

Boston Scientific Corporation

Abbott

Biotronik

MicroPort Scientific Corporation

LivaNova PLC

Who should buy this report?

The Middle East and Africa Implantable Defibrillators Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Middle East and Africa Implantable Defibrillators Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Middle East and Africa Implantable Defibrillators Market

Get Free Sample For Middle East and Africa Implantable Defibrillators Market