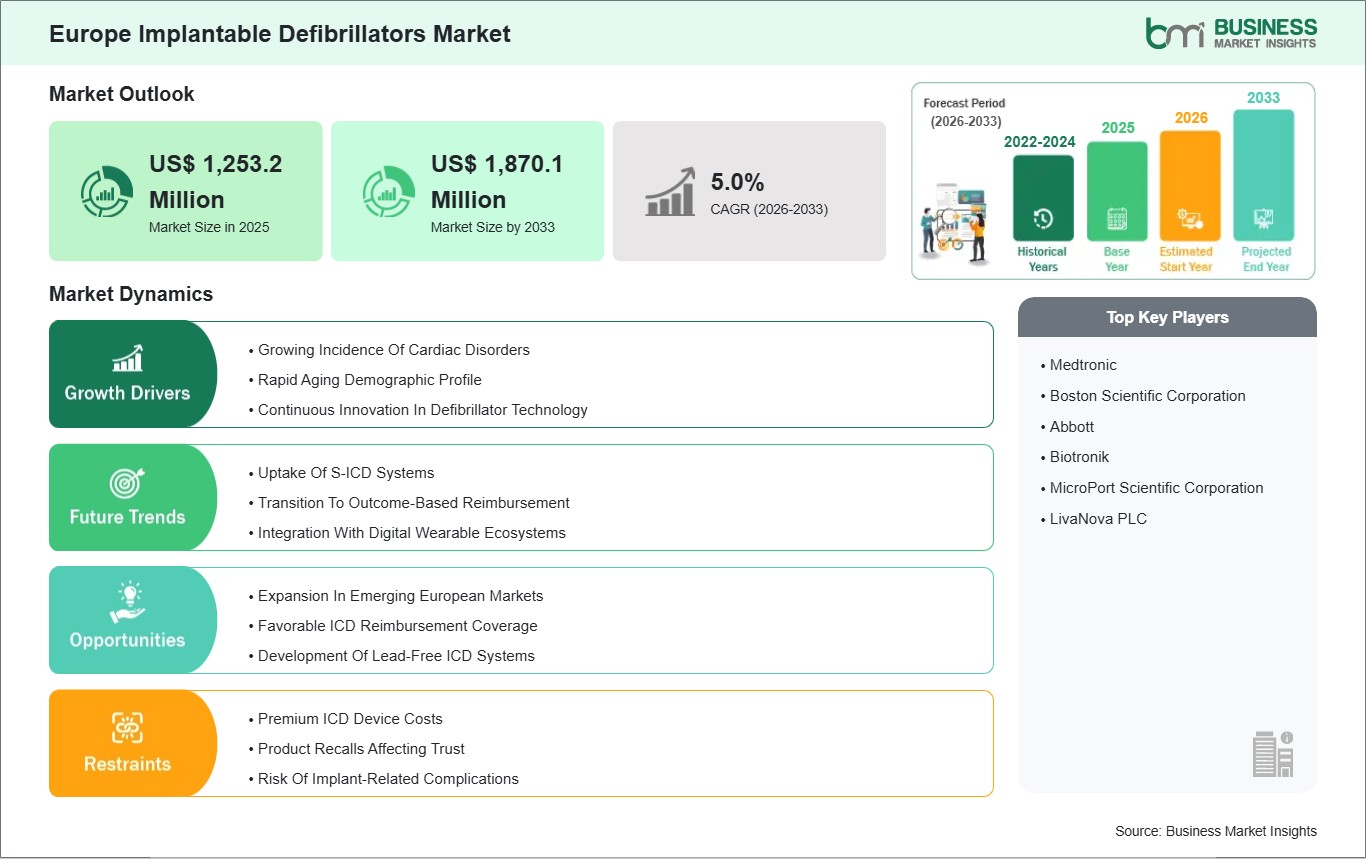

The Europe Implantable Defibrillators market size is expected to reach US$ 1,870.1 million by 2033 from US$ 1,253.2 million in 2025. The market is estimated to record a CAGR of 5.0% from 2026 to 2033.

Executive Summary and Europe Implantable Defibrillators Market Analysis:

The implantable defibrillators market in Europe is a key regional hub for advanced cardiac device adoption, underpinned by strong healthcare systems, high clinician awareness, and guideline-driven preventive care practices. Across Western and Central Europe, a high prevalence of cardiovascular diseases combined with well-established electrophysiology centers has accelerated the uptake of implantable cardioverter defibrillators (ICDs) for both primary and secondary prevention of sudden cardiac death. Reimbursement frameworks in major European markets generally support broad access to ICD therapy, reinforcing sustained clinical utilization in both inpatient and outpatient settings. National guidelines from bodies such as the European Society of Cardiology emphasize evidence-based use of ICDs, solidifying their role in contemporary cardiac care pathways.

The European market faces nuances that temper growth dynamics. Variability in healthcare funding and procedural adoption between Western and Eastern European countries can create disparities in device penetration. Additionally, evolving cost-containment policies in some health systems introduce pressure on pricing and reimbursement negotiations, particularly for advanced and next-generation defibrillator technologies. Despite these challenges, Europe's strategic emphasis on preventive cardiology and integrated care models continues to support robust demand for ICDs, positioning the region as a critical contributor to global device innovation and adoption.

Europe Implantable Defibrillators Market - Strategic Insights:

Get more information on this report

Europe Implantable Defibrillators Market Segmentation Analysis:

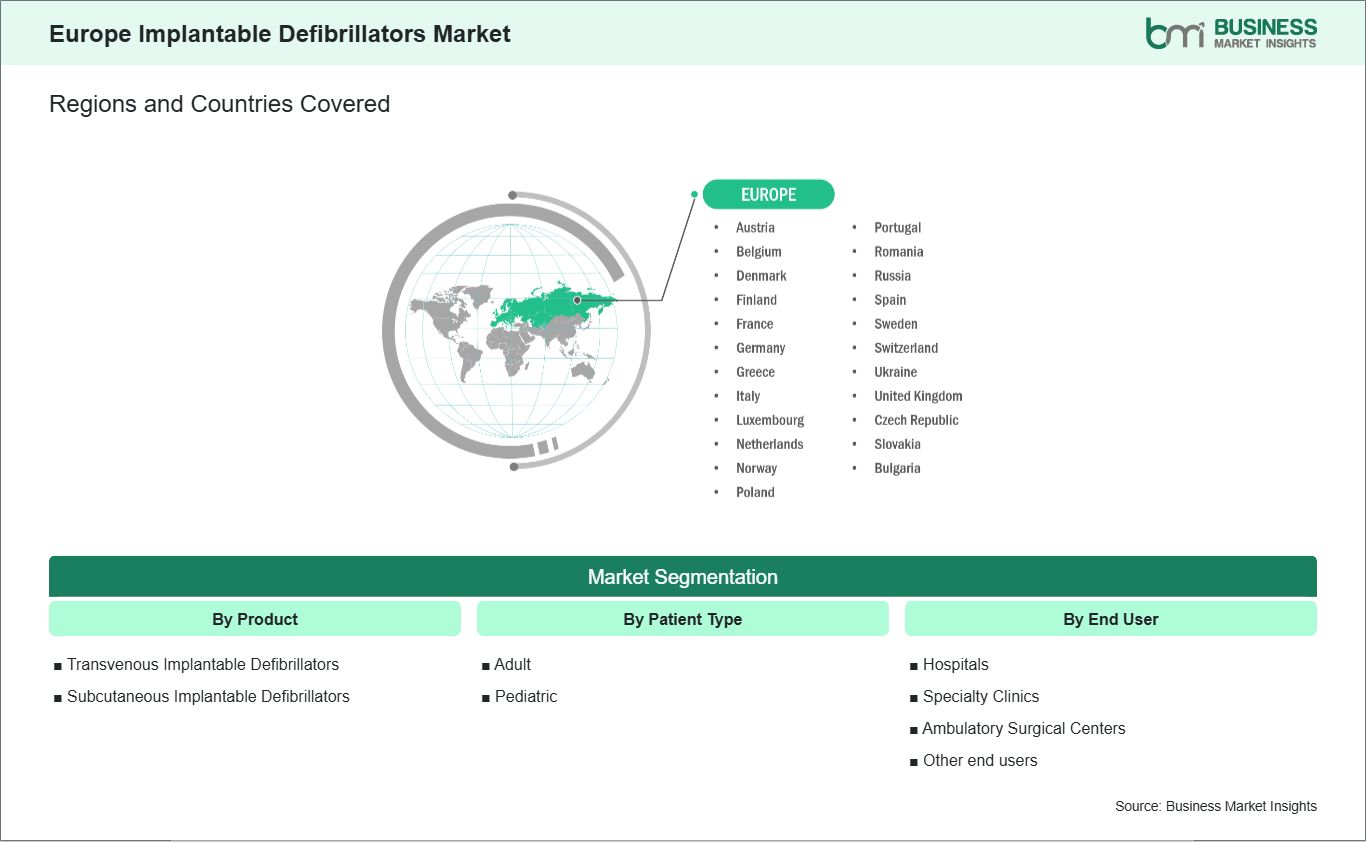

Key segments that contributed to the derivation of the Europe Implantable Defibrillators market analysis are product type, patient type, and end user.

By product type, the implantable defibrillators market is segmented into transvenous implantable defibrillators and subcutaneous implantable defibrillators. The transvenous implantable defibrillators segment dominated the market in 2025.

Based on patient type, the implantable defibrillators market is classified into adult and pediatric. The adult segment dominated the market in 2025.

In terms of end user, the implantable defibrillators market is categorized into hospitals, specialty clinics, ambulatory surgical centers, and others. The hospitals segment dominated the market in 2025.

Europe Implantable Defibrillators Market Drivers and Opportunities:

Growing Incidence of Cardiac Disorders

Europe is experiencing a growing incidence of cardiac disorders, particularly heart failure and life-threatening arrhythmias. An aging population across Western and Eastern Europe is one of the key reasons behind the rising number of patients with serious heart conditions. In addition, lifestyle factors such as smoking, unhealthy diets, stress, and low physical activity levels continue to contribute to heart rhythm abnormalities. As more people are diagnosed with high-risk cardiac conditions, the need for implantable cardioverter defibrillators (ICDs) is increasing across the region.

European healthcare systems place strong emphasis on early diagnosis and structured cardiac care pathways. Several countries have established specialized cardiac centers and electrophysiology units that focus on managing complex rhythm disorders. Physicians follow clear clinical guidelines that recommend ICD therapy for patients at risk of sudden cardiac death. This strong clinical framework supports consistent adoption of ICDs in both public and private hospitals.

Although access levels may vary between Western Europe and parts of Eastern Europe, advanced cardiac care is widely available in major markets such as Germany, France, Italy, the UK, and Spain. As the burden of serious heart disorders continues to rise, ICD therapy remains an essential part of long-term disease management. The growing incidence of cardiac disorders acts as a major driver for the ICD market in Europe.

Favorable ICD Reimbursement Coverage

Europe benefits from well-established healthcare reimbursement systems that support access to advanced cardiac therapies, including ICD implantation. Most Western European countries operate under public healthcare models where ICD procedures are covered for eligible patients. Clear treatment guidelines and structured approval processes make reimbursement predictable for hospitals and healthcare providers. This reduces financial uncertainty and encourages broader adoption of ICD therapy.

In countries such as Germany, France, Italy, and the UK, reimbursement policies recognize ICDs as a standard treatment for patients at high risk of sudden cardiac arrest. Hospitals are able to perform ICD implantations with confidence, knowing that the procedure and device costs are supported by national health systems. This stable reimbursement environment strengthens physician confidence and promotes timely treatment decisions.

While reimbursement frameworks may differ in parts of Eastern Europe, overall coverage across the region continues to improve. Governments are focused on improving survival outcomes for cardiac patients and reducing long-term healthcare burden. Supportive ICD reimbursement policies create strong opportunities for device manufacturers to expand their presence in Europe. A stable and structured payment environment remains a key opportunity factor for the regional ICD market.

Europe Implantable Defibrillators Market Size and Share Analysis:

The Europe implantable defibrillators market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within product type, patient type, and end user, highlighting their respective contributions to overall market performance.

By product type, the transvenous implantable defibrillators subsegment dominated the market in 2025, due to established clinical efficacy, broader physician familiarity, proven long-term outcomes, wider availability, and strong adoption in treating high-risk cardiac patients compared to newer subcutaneous options.

In terms of patient type, the adult subsegment dominated the market in 2025. This leadership is attributed to the higher prevalence of cardiac disorders in the adult population, increased awareness of sudden cardiac death prevention, and greater accessibility of advanced defibrillator therapies for adult patients.

Based on end user, the hospitals subsegment dominated the market in 2025. Hospitals remain the primary distribution channel due to their comprehensive cardiac care facilities, access to trained cardiologists and specialized technicians, advanced monitoring infrastructure, and ability to provide immediate, life-saving interventions.

Europe Implantable Defibrillators Market Report Highlights:

Europe Implantable Defibrillators Market Report Coverage and Deliverables:

The "Europe Implantable Defibrillators Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Europe Implantable Defibrillators market size and forecast at regional and country levels for all market segments covered under the scope

Europe Implantable Defibrillators market trends, as well as drivers, restraints, and opportunities

Europe Implantable Defibrillators market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Europe Implantable Defibrillators market

Detailed company profiles, including SWOT analysis

Europe Implantable Defibrillators Market Geographic Insights:

The geographical scope of the Europe Implantable Defibrillators market report is divided into: Germany, Italy, France, the UK, Spain, Belgium, the Netherlands, Luxembourg, Norway, Finland, Denmark, Sweden, Austria, Switzerland, Russia, Romania, Greece, the Czech Republic, Portugal, Ukraine, Poland, Slovakia, and Bulgaria. Germany held the largest share in 2025.

Germany stands as the dominant force in the European implantable defibrillators market, widely recognized for its advanced cardiac care infrastructure, comprehensive reimbursement environment, and deep clinical expertise. As the largest national market in Europe, Germany leads in both the volume of ICD procedures and the breadth of technology utilization, with a vast network of tertiary cardiac centers and electrophysiologists driving adoption. The country's statutory health insurance system broadly supports ICD implantation, minimizing patient cost barriers and solidifying routine integration of defibrillator therapy into cardiac care algorithms.

Germany's market leadership is also strengthened by its role as both a consumer and innovation hub. Major global medical device manufacturers maintain strong operational and research and development footprints within the country, facilitating early clinical trials, technology refinement, and adoption of next-generation systems such as MRI-conditional and subcutaneous ICD platforms. High public awareness of cardiovascular risks and structured post-implantation monitoring protocols further enhance Germany's market vibrancy, enabling clinicians to optimize long-term patient outcomes. While broader European markets grapple with varied healthcare funding models, Germany's systemic focus on preventive cardiology and device-enabled care ensures its position remains preeminent in the regional ICD landscape.

Get more information on this report

Europe Implantable Defibrillators Market Research Report Guidance:

The report includes qualitative and quantitative data in the Europe Implantable Defibrillators market across product type, patient type, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Europe Implantable Defibrillators market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Europe Implantable Defibrillators market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Europe Implantable Defibrillators market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Europe Implantable Defibrillators market segments product type, patient type, end user, and geography across Germany, Italy, France, the UK, Spain, Belgium, the Netherlands, Luxembourg, Norway, Finland, Denmark, Sweden, Austria, Switzerland, Russia, Romania, Greece, the Czech Republic, Portugal, Ukraine, Poland, Slovakia and Bulgaria. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Europe Implantable Defibrillators market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Europe Implantable Defibrillators Market News and Key Development:

The Europe Implantable Defibrillators market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Europe Implantable Defibrillators market are:

In July 2025, FineHeart was named the lead partner of the IPCEI Tech4Cure initiative to spearhead the structuring of the European implantable medical device sector, including active implantable devices such as ICDs, under a multi-country EU innovation programme. This designation highlights strategic industry efforts within Europe to advance implantable cardiac device technologies and strengthen the region's innovation ecosystem.

In February 2024, Royal Papworth Hospital NHS Foundation Trust in the UK announced that patients at its centre became among the first in Europe, outside of clinical trials, to be implanted with the new Medtronic Aurora EV-ICD to protect against sudden cardiac arrest. This represented one of the earliest real-world uses of the CE-marked extravascular ICD system in European clinical practice.

Key Sources Referred:

The World BankWorld Health Organization (WHO)Center for Disease Control and Prevention (CDC)European Database on Medical Devices (EUDAMED)European Society of CardiologyAmerican College of CardiologyAmerican Heart AssociationCompany WebsitesCompany Annual ReportsCompany Investor Presentations

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Europe Implantable Defibrillators Market?

The Europe Implantable Defibrillators Market is valued at US$ 1,253.2 Million in 2025, it is projected to reach US$ 1,870.1 Million by 2033.

What is the CAGR for Europe Implantable Defibrillators Market by (2026 - 2033)?

As per our report Europe Implantable Defibrillators Market, the market size is valued at US$ 1,253.2 Million in 2025, projecting it to reach US$ 1,870.1 Million by 2033. This translates to a CAGR of approximately 5.0% during the forecast period.

What segments are covered in this report?

The Europe Implantable Defibrillators Market report typically cover these key segments-

End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Other end users)

What is the historic period, base year, and forecast period taken for Europe Implantable Defibrillators Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Implantable Defibrillators Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Europe Implantable Defibrillators Market?

The Europe Implantable Defibrillators Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic

Boston Scientific Corporation

Abbott

Biotronik

MicroPort Scientific Corporation

LivaNova PLC

Who should buy this report?

The Europe Implantable Defibrillators Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Europe Implantable Defibrillators Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Europe Implantable Defibrillators Market

Get Free Sample For Europe Implantable Defibrillators Market