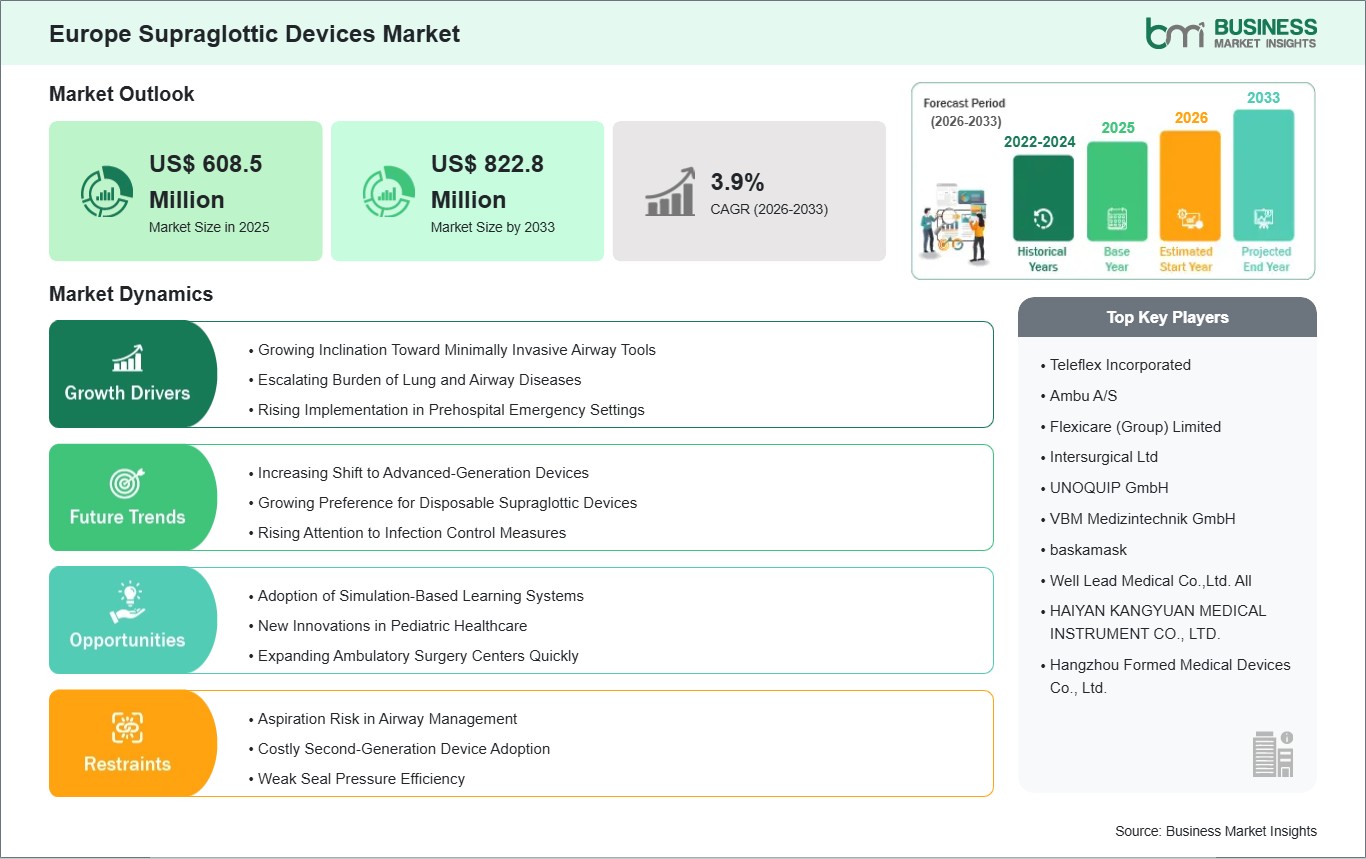

The Europe Supraglottic Devices market size is expected to reach US$ 822.8 million by 2033 from US$ 608.5 million in 2025. The market is estimated to record a CAGR of 3.9% from 2026 to 2033.

Executive Summary and Europe Supraglottic Devices Market Analysis:

The Europe supraglottic devices market represents one of the most developed markets, given the clinical expertise, patient safety considerations, and operational efficiencies that characterize this region. Both western and central European hospitals, surgery centers, and other institutions place great importance on implementing innovative airway management technologies to optimize their processes and ensure patient safety during surgery. Supraglottic airway devices have been shown to be more convenient, quicker to deploy, and less likely to result in complications than traditional endotracheal intubation techniques. The market growth can be attributed to increasing awareness of airway management techniques and a focus on minimizing anesthesia complications.

One of the factors that makes the continent a leader in the uptake of these devices is the existence of robust hospital infrastructure and well-trained clinicians in the medical field. Specialists such as anesthetists, emergency physicians, and intensive care staff receive training in modern airway tools, promoting their efficient application and adoption. Furthermore, private hospitals and ambulatory surgery centers are increasingly adopting these tools for better patient flow management. Though these devices have gained significant clinical acceptance, the availability of funds in some public healthcare systems may impede the adoption of more advanced or disposable equipment. In addition, dependence on conventional intubation practices in complicated surgeries may hinder full integration. The other factor that may influence the pace at which new devices come into practice includes regulatory considerations and procurement procedures. The European continent offers a favorable environment for the development of the supraglottic airway device market.

Europe Supraglottic Devices Market - Strategic Insights:

Get more information on this report

Europe Supraglottic Devices Market Segmentation Analysis:

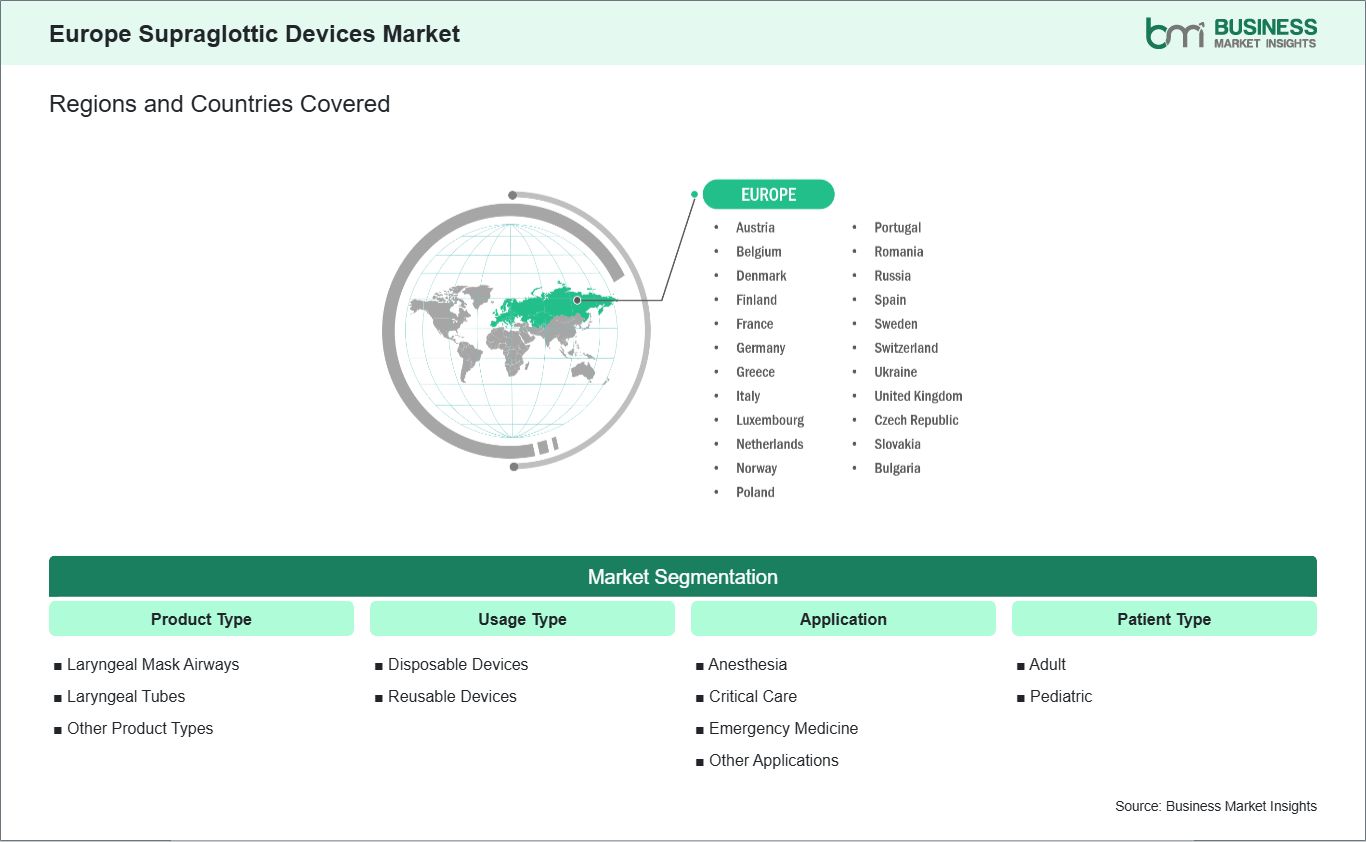

Key segments that contributed to the derivation of the Europe Supraglottic Devices market analysis are product type, usage type, application, patient type, and end user.

By product type, the supraglottic devices market is segmented into laryngeal mask airways, laryngeal tubes, and other product types. The laryngeal mask airways segment dominated the market in 2025.

Based on usage type, the supraglottic devices market is classified into disposable devices and reusable devices. The disposable devices segment dominated the market in 2025.

In terms of application, the supraglottic devices market is categorized into anesthesia, critical care, emergency medicine, and other applications. The anesthesia segment dominated the market in 2025.

By patient type, the supraglottic devices market is bifurcated into adult and pediatric. The adult segment dominated the market in 2025.

Based on end user, the supraglottic devices market is segmented into hospitals, ambulatory surgical centers, emergency medical services, and other end users. The hospitals segment dominated the market in 2025.

Europe Supraglottic Devices Market Drivers and Opportunities:

The European supraglottic devices market is witnessing a growing inclination toward minimally invasive airway tools as healthcare providers aim to improve patient safety and operational efficiency. Supraglottic airway devices (SGAs) are increasingly preferred for their simplicity, ease of insertion, and reduced need for specialized intubation skills. In high-volume hospitals and surgical centers, these devices allow clinicians to secure airways quickly, improving workflow and reducing the risk of complications during both elective surgeries and emergency procedures.

Rising demand for outpatient procedures and short-stay surgeries is further accelerating adoption. Minimally invasive airway tools enable faster airway control and shorter anesthesia times, allowing hospitals to optimize patient turnover without compromising care quality. Their versatility across various clinical applications, from routine operations to critical care, makes SGAs a practical choice for facilities aiming to balance efficiency with high standards of patient care.

Economic and safety considerations also support the shift toward these devices. Single-use SGAs reduce cross-contamination risks and minimize the burden of sterilization, while improved device designs enhance patient comfort and ventilation efficiency. Combined with growing awareness of minimally invasive approaches in perioperative care, these factors are positioning SGAs as essential tools in Europe’s modern airway management landscape.

Adoption of Simulation-Based Learning Systems

Simulation-based learning systems are increasingly driving the adoption of supraglottic airway devices across Europe. Healthcare institutions are investing in training programs that allow clinicians to practice SGA placement and management in controlled, risk-free environments. This hands-on approach enables practitioners to build confidence, troubleshoot potential complications, and refine their techniques before applying them in real-world clinical settings, particularly in emergency and high-acuity care scenarios.

Structured workshops and interactive modules are widely used to complement theoretical instruction. These programs expose practitioners to different device types and patient scenarios, promoting standardized airway management protocols and ensuring consistent clinical outcomes. Simulation-based learning also facilitates multidisciplinary team training, allowing doctors, nurses, and emergency responders to coordinate effectively during airway management procedures.

The introduction of simulation into continuing education for medical professionals has increased the importance of its effects even more. Even centers lacking financial power could adopt simulations that do not require huge amounts of money for their conduct. Continuous engagement with real-life simulations makes individuals better in making decisions and using SGA devices safely and effectively. The growing emphasis on the use of simulation is contributing greatly to the consistent adoption of supraglottic airway devices in Europe.

Europe Supraglottic Devices Market Size and Share Analysis:

The Europe Supraglottic Devices market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report evaluates important subsegments categorized within product type, usage type, application, patient type, and end user, highlighting their respective contributions to overall market performance.

By product type, the laryngeal mask airways subsegment dominated the supraglottic devices market in 2025. The dominance of laryngeal mask airways is driven by their ease of insertion, high success rate in securing the airway, reduced risk of complications compared to traditional intubation, and broad adoption in surgical and emergency settings, making them a key revenue contributor for manufacturers.

Based on usage type, the disposable devices subsegment led the market in 2025. Disposable supraglottic devices are preferred due to their reduced risk of cross-contamination, lower sterilization requirements, and convenience for high-volume clinical environments, which supports their widespread adoption across hospitals and emergency care facilities.

In terms of application, the anesthesia subsegment dominated the market in 2025. This leadership is attributed to the frequent use of supraglottic devices in elective and emergency surgical procedures, the increasing number of surgeries worldwide, and the clinical benefits of providing a safe and effective airway without the need for invasive intubation.

By patient type, the adult subsegment dominated the market in 2025. The preference for adult patients is driven by higher procedural volumes in adult surgeries, the established clinical efficacy of supraglottic devices in adult airway management, and increasing adoption in critical care and emergency settings.

Based on end user, the hospitals subsegment dominated the market in 2025. Hospitals lead due to their well-established anesthesia and critical care departments, access to advanced airway management devices, trained staff, and the capability to perform a high volume of surgical and emergency procedures requiring reliable airway management.

Europe Supraglottic Devices Market Report Highlights:

Europe Supraglottic Devices Market Report Coverage and Deliverables:

The "Europe Supraglottic Devices Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Europe Supraglottic Devices market size and forecast at regional and country levels for all market segments covered under the scope

Europe Supraglottic Devices market trends, as well as drivers, restraints, and opportunities

Europe Supraglottic Devices market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Europe Supraglottic Devices market

Detailed company profiles, including SWOT analysis

Europe Supraglottic Devices Market Geographic Insights:

The geographical scope of the Europe Supraglottic Devices market report is divided into: Germany, Italy, France, the UK, Spain, Belgium, the Netherlands, Luxembourg, Norway, Finland, Denmark, Sweden, Austria, Switzerland, Russia, Romania, Greece, the Czech Republic, Portugal, Ukraine, Poland, Slovakia, and Bulgaria. Germany held the largest share in 2025.

Germany dominates the Europe supraglottic devices market, owing to its highly developed healthcare system, strong hospital infrastructure, and commitment to clinical innovation. Hospitals in Germany, especially tertiary hospitals and teaching hospitals, focus on patient safety and efficiency, which has contributed to the use of supraglottic airway devices during elective operations and emergency situations. Supraglottic devices are employed in order to minimize problems that might occur during anesthesia and for the efficient management of the airway in emergencies or trauma cases.

One of the reasons why Germany is at the forefront of using such airway devices is because of the German focus on education and ongoing training. Physicians, especially anesthesiologists, intensive care physicians, and emergency physicians, constantly undergo advanced training in the management of patients' airways. Moreover, there is an efficient supply chain for medical equipment and great cooperation between hospitals and suppliers, which ensures access to different types of products. In particular, although the main innovations are being made in urban hospitals, regional institutions are increasing their use of devices in the process of infrastructure modernization. Considering cost aspects associated with the use of newer and disposable devices, Germany’s priority to achieve maximum clinical efficacy and high-quality treatment makes it the leader of the European market.

Get more information on this report

Europe Supraglottic Devices Market Research Report Guidance:

The report includes qualitative and quantitative data in the Europe Supraglottic Devices market across product type, usage type, application, patient type, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Europe Supraglottic Devices market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Europe Supraglottic Devices market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Europe Supraglottic Devices market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 12 cover Europe Supraglottic Devices market segments product type, usage type, application, patient type, end user, and geography across Germany, Italy, France, the UK, Spain, Belgium, the Netherlands, Luxembourg, Norway, Finland, Denmark, Sweden, Austria, Switzerland, Russia, Romania, Greece, the Czech Republic, Portugal, Ukraine, Poland, Slovakia and Bulgaria. They cover the market revenue, forecast, and factors driving the market.

Chapter 13 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 14 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 15 provides detailed profiles of the major companies operating in the Europe Supraglottic Devices market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 16, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Europe Supraglottic Devices Market News and Key Development:

The Europe Supraglottic Devices market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Europe Supraglottic Devices market are:

In December 2025, Teleflex Incorporated also confirmed that it had entered into agreements to sell its Acute Care and Interventional Urology businesses (which include parts of its airway device lines) to Intersurgical Ltd., with regulatory approvals targeted for completion by late 2026.

In December 2025, Intersurgical announced that it reached an agreement to acquire the Acute Care and Interventional Urology businesses of Teleflex, a strategic move that broadens Intersurgical’s product portfolio (including airway management devices) and enhances its operational footprint globally.

Key Sources Referred:

The World BankWorld Health Organization (WHO)Center for Disease Control and Prevention (CDC)Food and Drug Administration (FDA)European Database on Medical Devices (EUDAMED)European Society of Cardiology (ESC)American College of Cardiology (ACC)American Heart Association (AHA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

Identical Market Reports with other Region/Countries

The List of Companies - Europe Supraglottic Devices Market

Teleflex Incorporated

Ambu A/S

Flexicare (Group) Limited

Intersurgical Ltd

UNOQUIP GmbH

VBM Medizintechnik GmbH

baskamask

Well Lead Medical Co.,Ltd. All

HAIYAN KANGYUAN MEDICAL INSTRUMENT CO., LTD.

Hangzhou Formed Medical Devices Co., Ltd.

Frequently Asked Questions

How big is the Europe Supraglottic Devices Market?

The Europe Supraglottic Devices Market is valued at US$ 608.5 Million in 2025, it is projected to reach US$ 822.8 Million by 2033.

What is the CAGR for Europe Supraglottic Devices Market by (2026 - 2033)?

As per our report Europe Supraglottic Devices Market, the market size is valued at US$ 608.5 Million in 2025, projecting it to reach US$ 822.8 Million by 2033. This translates to a CAGR of approximately 3.9% during the forecast period.

What segments are covered in this report?

The Europe Supraglottic Devices Market report typically cover these key segments-

Product Type (Laryngeal Mask Airways, Laryngeal Tubes, Other Product Types)

Usage Type (Disposable Devices, Reusable Devices)

Application (Anesthesia, Critical Care, Emergency Medicine, Other Applications)

Patient Type (Adult, Pediatric)

What is the historic period, base year, and forecast period taken for Europe Supraglottic Devices Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Supraglottic Devices Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Europe Supraglottic Devices Market?

The Europe Supraglottic Devices Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Teleflex Incorporated

Ambu A/S

Flexicare (Group) Limited

Intersurgical Ltd

UNOQUIP GmbH

VBM Medizintechnik GmbH

baskamask

Well Lead Medical Co.,Ltd. All

HAIYAN KANGYUAN MEDICAL INSTRUMENT CO., LTD.

Hangzhou Formed Medical Devices Co., Ltd.

Who should buy this report?

The Europe Supraglottic Devices Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Europe Supraglottic Devices Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Europe Supraglottic Devices Market

Get Free Sample For Europe Supraglottic Devices Market