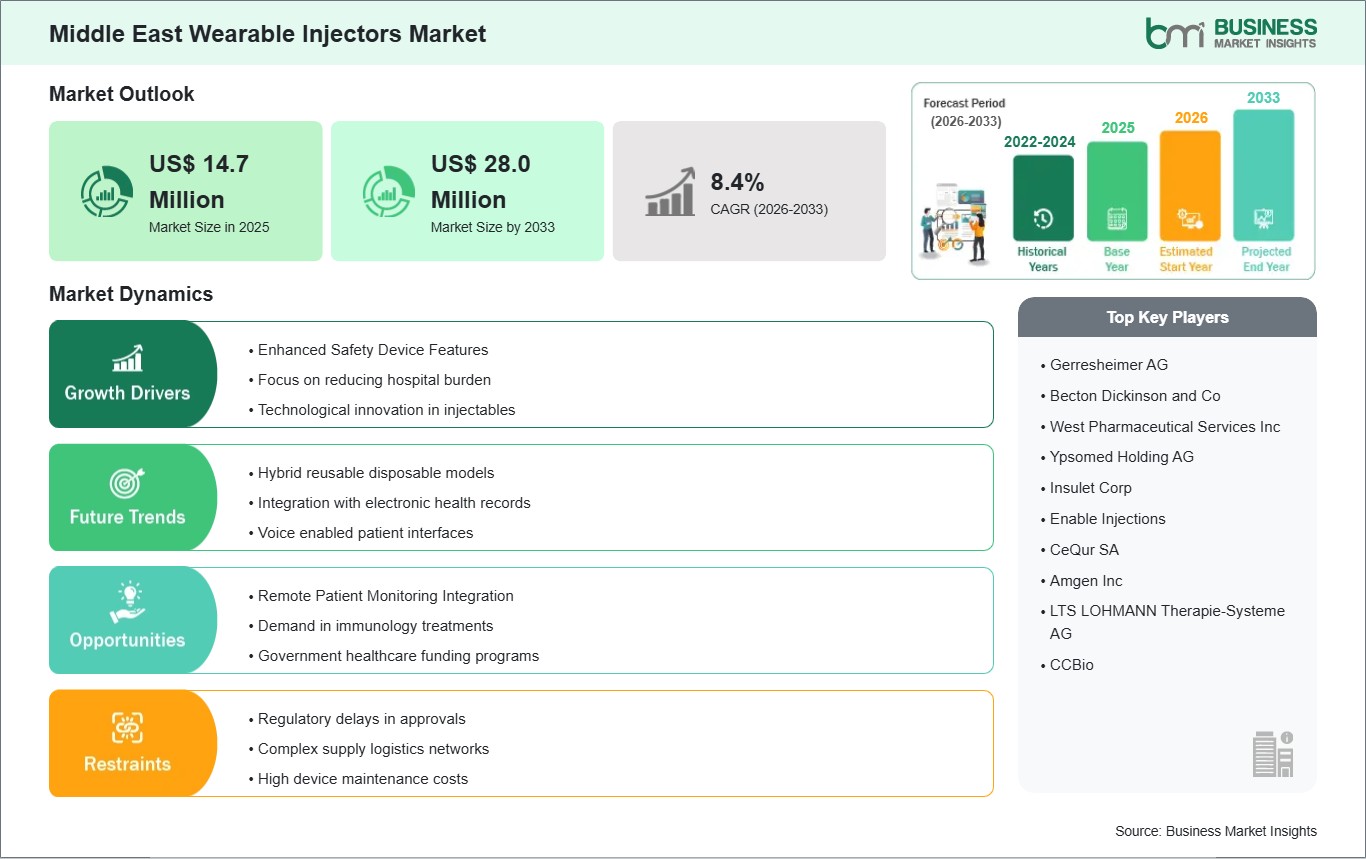

The Middle East Wearable Injectors Market size is expected to reach US$ 28.0 million by 2033 from US$ 14.7 million in 2025. The market is estimated to record a CAGR of 8.4% from 2026 to 2033.

Executive Summary and Middle East Wearable Injectors Market Analysis:

The Middle East wearable injectors market is gaining traction as healthcare systems across the region modernize and shift toward outpatient-centric care delivery models. The increasing prevalence of chronic diseases such as diabetes, oncology disorders, and autoimmune conditions is creating sustained demand for advanced drug delivery solutions that enhance dosing precision and patient convenience. Wearable injectors, designed to administer high-volume biologic therapies subcutaneously over extended periods, are increasingly recognized as a viable alternative to repeated hospital-based injections. Market activity is primarily concentrated in economically advanced countries with structured healthcare systems and significant public healthcare spending. Adoption is strongest in urban tertiary hospitals and specialty clinics that manage long-term biologic therapies. Competitive dynamics are shaped by multinational device manufacturers partnering with regional distributors to navigate regulatory approvals and hospital procurement processes. Product differentiation focuses on reliability, ease of application, safety mechanisms, and compatibility with specialty pharmaceuticals. Regulatory environments across the Middle East are relatively structured, particularly in Gulf countries where centralized authorities oversee medical device approvals. However, procurement is often influenced by government tenders, hospital group purchasing committees, and national healthcare strategies. Private healthcare networks are playing an increasingly important role in early adoption, particularly where insurance penetration is high. Despite favorable infrastructure in leading markets, broader regional adoption remains influenced by cost considerations, physician familiarity with wearable technologies, and alignment with national reimbursement frameworks. Overall, the market is positioned as a specialized but expanding segment within the Middle East’s broader chronic care and biologics ecosystem.

Middle East Wearable Injectors Market - Strategic Insights:

Get more information on this report

Middle East Wearable Injectors Market Segmentation Analysis:

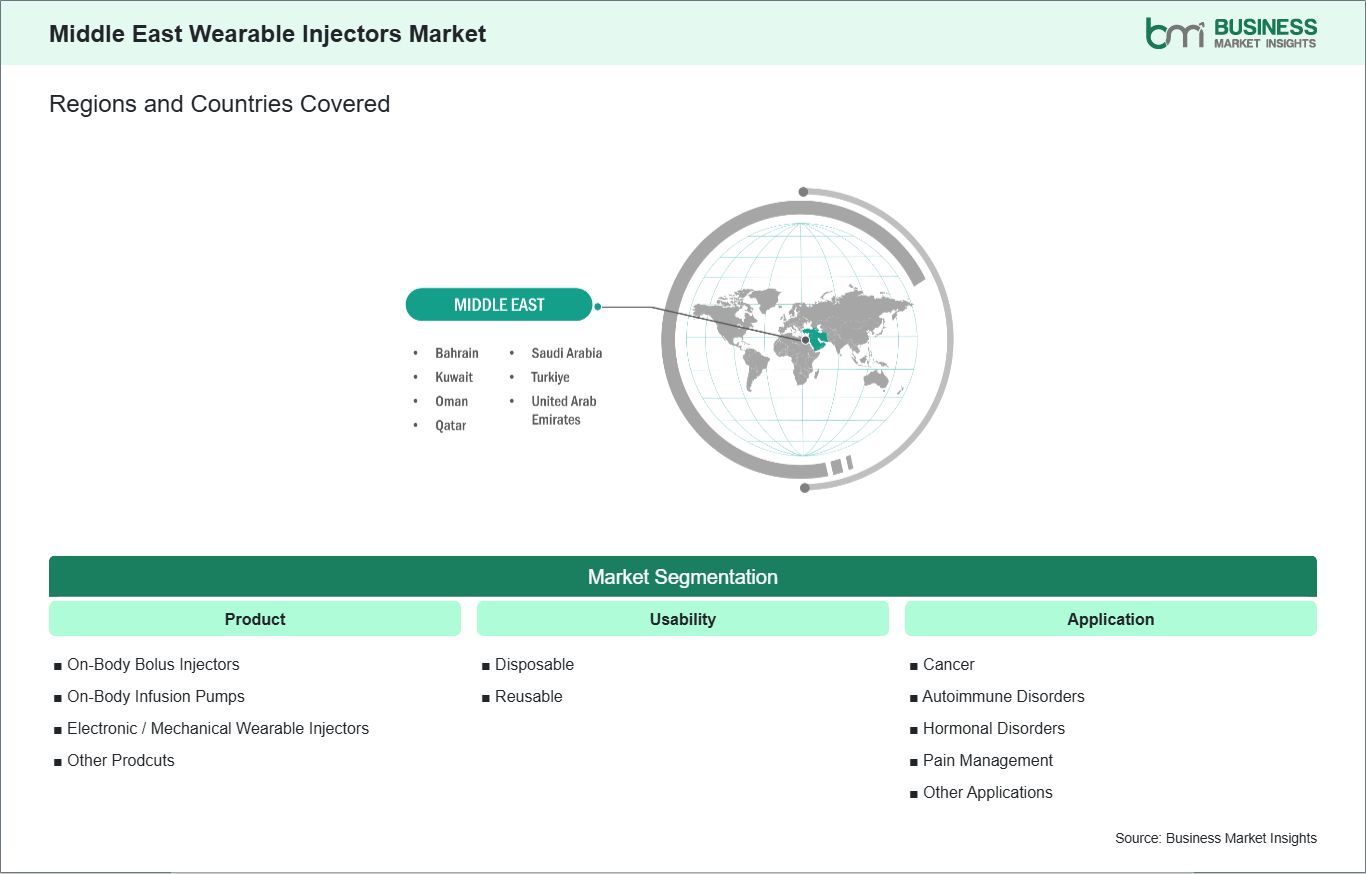

Key segments that contributed to the derivation of the Middle East wearable injectors market analysis are product, usability, and application.

By product, the wearable injectors market is segmented into on-body bolus injectors, on-body infusion pumps, electronic / mechanical wearable injectors, and others. The on-body bolus injectors segment dominated the market in 2025.

Based on usability, the wearable injectors market is categorized into disposable and reusable. The disposable segment dominated the market in 2025.

In terms of application, the market is classified into cancer, autoimmune disorders, hormonal disorders, pain management, and other applications. The autoimmune disorders segment dominated the market in 2025.

Middle East Wearable Injectors Market Drivers and Opportunities:

Enhanced Safety Device Features

Hospitals and specialty clinics in countries such as Saudi Arabia, the United Arab Emirates, and Qatar are increasingly evaluating drug delivery technologies based not only on convenience but also on built-in safeguards that reduce dosing errors, prevent needle exposure, and ensure controlled administration of high-value biologics. Enhanced safety features such as automated needle insertion and retraction, audible and visual dose confirmation, and lockout mechanisms are becoming important differentiators for wearable injector manufacturers targeting the region. The growing prevalence of chronic diseases, including diabetes and autoimmune disorders, in the Middle East has amplified the need for reliable long-term injectable therapies. In response, healthcare providers are seeking devices that minimize user error and support proper adherence outside hospital environments. Wearable injectors equipped with fail-safe activation systems and tamper-resistant designs are particularly attractive in markets where patient self-administration is expanding, but clinical oversight remains a priority. This balance between innovation and safety aligns with regional health transformation strategies that aim to combine advanced care delivery with strict quality assurance standards. Regulatory authorities and procurement bodies in the Gulf Cooperation Council are also strengthening device evaluation frameworks to ensure imported technologies meet international benchmarks. As a result, manufacturers entering the Middle East wearable injectors market must demonstrate compliance with rigorous safety and performance criteria. Devices that integrate advanced sensor feedback, temperature monitoring for biologic stability, and error notification systems are more likely to gain acceptance in both public and private healthcare settings. This focus on enhanced safety is shaping product development strategies and reinforcing confidence among clinicians and patients considering wearable injectors as part of routine therapeutic protocols.

Remote Patient Monitoring Integration

Countries such as the United Arab Emirates and Saudi Arabia are advancing telehealth frameworks and national digital health platforms that connect patients, providers, and medical devices through secure data networks. Wearable injectors that can integrate with remote monitoring systems are well-positioned within this landscape, as they enable clinicians to track therapy adherence, review dosing histories, and receive alerts without requiring in-person visits. This capability is especially valuable for managing chronic conditions that require continuous oversight. In geographically dispersed areas or regions with uneven specialist distribution, remote monitoring integration enhances care accessibility. Patients in secondary cities or rural communities can maintain consistent treatment regimens while remaining connected to healthcare providers through digital platforms. Wearable injectors equipped with Bluetooth or cloud-based connectivity can transmit administration data to centralized systems, supporting follow-up consultations and early intervention if irregularities are detected. This model aligns with Middle Eastern healthcare objectives focused on improving service reach while reducing pressure on major tertiary hospitals in metropolitan centers like Riyadh, Dubai, and Doha. Private healthcare groups and specialty clinics are increasingly incorporating connected devices into premium care offerings, viewing remote monitoring as a value-added service that improves patient engagement. Integration of wearable injectors with mobile health applications and hospital information systems allows for comprehensive disease management programs, particularly in endocrinology and immunology segments. As digital infrastructure continues to expand and regulatory frameworks evolve to support secure data exchange, the integration of remote patient monitoring with wearable injectors is expected to become a central growth driver in the Middle East market, reinforcing a shift toward more connected and patient-centered healthcare delivery models.

Middle East Wearable Injectors Market Size and Share Analysis:

The Middle East Wearable Injectors Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, usability, and application, offering insights into their contribution to overall market performance.

By product, the on-body bolus injectors subsegment dominated the market in 2025, driven by expanding demand for technologically advanced drug delivery systems that enable controlled, high-dose administration in outpatient settings.

Based on usability, the disposable subsegment dominated the market in 2025, driven by increasing preference for safe, ready-to-use injectors that minimize sterilization requirements and operational complexity.

In terms of application, the autoimmune disorders subsegment dominated the market in 2025, driven by growing diagnosis rates and improving access to biologic therapies for chronic inflammatory diseases across the region.

Middle East Wearable Injectors Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 14.7 Million

Market Size by 2033

US$ 28.0 Million

CAGR (2026 - 2033)

8.4%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

On-Body Bolus Injectors

On-Body Infusion Pumps

Electronic / Mechanical Wearable Injectors

Other Prodcuts

By Usability

Disposable

Reusable

By Application

Cancer

Autoimmune Disorders

Hormonal Disorders

Pain Management

Other Applications

Regions and Countries Covered

Middle East

UAE, Saudi Arabia, Bahrain, Oman, Kuwait, Qatar, and Turkiye

Market leaders and key company profiles

Gerresheimer AG

Becton Dickinson and Co

West Pharmaceutical Services Inc

Ypsomed Holding AG

Insulet Corp

Enable Injections

CeQur SA

Amgen Inc

LTS LOHMANN Therapie-Systeme AG

CCBio

Get more information on this report

Middle East Wearable Injectors Market Report Coverage and Deliverables:

The "Middle East Wearable Injectors Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Middle East Wearable Injectors Market size and forecast at regional and country levels for all segments covered under the scope

Middle East Wearable Injectors Market trends, as well as drivers, restraints, and opportunities

Middle East Wearable Injectors Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Middle East Wearable Injectors Market

Detailed company profiles, including SWOT analysis

Middle East Wearable Injectors Market Geographic Insights:

The geographical scope of the Middle East Wearable Injectors Market report is divided into the UAE, Saudi Arabia, Bahrain, Oman, Kuwait, Qatar, and Turkiye. Turkiye held the largest share in 2025.

Country-level dynamics across the Middle East demonstrate varied adoption patterns influenced by healthcare investment, regulatory structure, insurance penetration, and specialty care capacity. Turkiye emerges as the dominant market in the region, driven by its large population base, well-developed hospital infrastructure, and strategic positioning as a medical hub bridging Europe and the Middle East. Major metropolitan centers such as Istanbul, Ankara, and Izmir are witnessing increasing integration of wearable injectors within tertiary hospitals and specialty clinics managing oncology, endocrinology, and autoimmune therapies. Turkiye benefits from a structured regulatory framework, expanding domestic medical device capabilities, and a strong private healthcare sector that supports early adoption of advanced drug delivery technologies. Additionally, growing patient awareness of self-administration benefits and an expanding outpatient treatment ecosystem reinforce its leadership position. Saudi Arabia represents a significant secondary market, supported by substantial public healthcare spending and national transformation programs aimed at enhancing chronic disease management. Adoption is concentrated in major cities, including Riyadh and Jeddah, where specialty care centers are incorporating wearable injectors into biologic therapy pathways. The United Arab Emirates demonstrates strong uptake within private hospital networks in Dubai and Abu Dhabi. High insurance coverage, advanced healthcare infrastructure, and a focus on medical innovation support the integration of connected drug delivery systems. Qatar and Kuwait show steady demand, primarily within specialized urban healthcare facilities serving high-income populations. Meanwhile, Oman and Bahrain represent smaller but developing markets where adoption is concentrated in select specialty clinics. Overall, Turkiye leads the Middle East wearable injectors market, while Saudi Arabia and the UAE provide substantial complementary opportunities. Market participants must implement country-specific regulatory strategies, clinician engagement programs, and localized distribution partnerships to effectively capture growth across this diverse regional landscape.

Get more information on this report

Middle East Wearable Injectors Market Research Report Guidance:

The report includes qualitative and quantitative data in the Middle East Wearable Injectors Market across product, usability, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Middle East Wearable Injectors Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Middle East Wearable Injectors Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Middle East Wearable Injectors Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Middle East Wearable Injectors Market segments by product, usability, application, and geography across the UAE, Saudi Arabia, Bahrain, Oman, Kuwait, Qatar, and Turkiye. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Middle East Wearable Injectors Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Middle East Wearable Injectors Market News and Key Development:

The Middle East Wearable Injectors Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Middle East wearable injectors market are:

In January 2026, Ypsomed Holding AG announced a partnership with Novo Nordisk to develop and supply large‑volume wearable patch injectors, broadening choices for subcutaneous self‑administration of biologics and aligning with demand for patient‑friendly delivery systems.

In December 2025, Enable Injections received regulatory approval from the Saudi Food and Drug Authority (SFDA) for the EMPAVELI Injector based on its enFuse On‑Body Delivery System, enabling legal marketing and distribution of this large‑volume subcutaneous delivery device in Saudi Arabia. This clearance allows wearable injector technology to support patient self‑administration of therapies in the Kingdom.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - Middle East Wearable Injectors Market

Gerresheimer AG

Becton Dickinson and Co

West Pharmaceutical Services Inc

Ypsomed Holding AG

Insulet Corp

Enable Injections

CeQur SA

Amgen Inc

LTS LOHMANN Therapie-Systeme AG

CCBio

Frequently Asked Questions

How big is the Middle East Wearable Injectors Market?

The Middle East Wearable Injectors Market is valued at US$ 14.7 Million in 2025, it is projected to reach US$ 28.0 Million by 2033.

What is the CAGR for Middle East Wearable Injectors Market by (2026 - 2033)?

As per our report Middle East Wearable Injectors Market, the market size is valued at US$ 14.7 Million in 2025, projecting it to reach US$ 28.0 Million by 2033. This translates to a CAGR of approximately 8.4% during the forecast period.

What segments are covered in this report?

The Middle East Wearable Injectors Market report typically cover these key segments-

Application (Cancer, Autoimmune Disorders, Hormonal Disorders, Pain Management, Other Applications)

What is the historic period, base year, and forecast period taken for Middle East Wearable Injectors Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East Wearable Injectors Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Middle East Wearable Injectors Market?

The Middle East Wearable Injectors Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Gerresheimer AG

Becton Dickinson and Co

West Pharmaceutical Services Inc

Ypsomed Holding AG

Insulet Corp

Enable Injections

CeQur SA

Amgen Inc

LTS LOHMANN Therapie-Systeme AG

CCBio

Who should buy this report?

The Middle East Wearable Injectors Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Middle East Wearable Injectors Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Middle East Wearable Injectors Market

Get Free Sample For Middle East Wearable Injectors Market