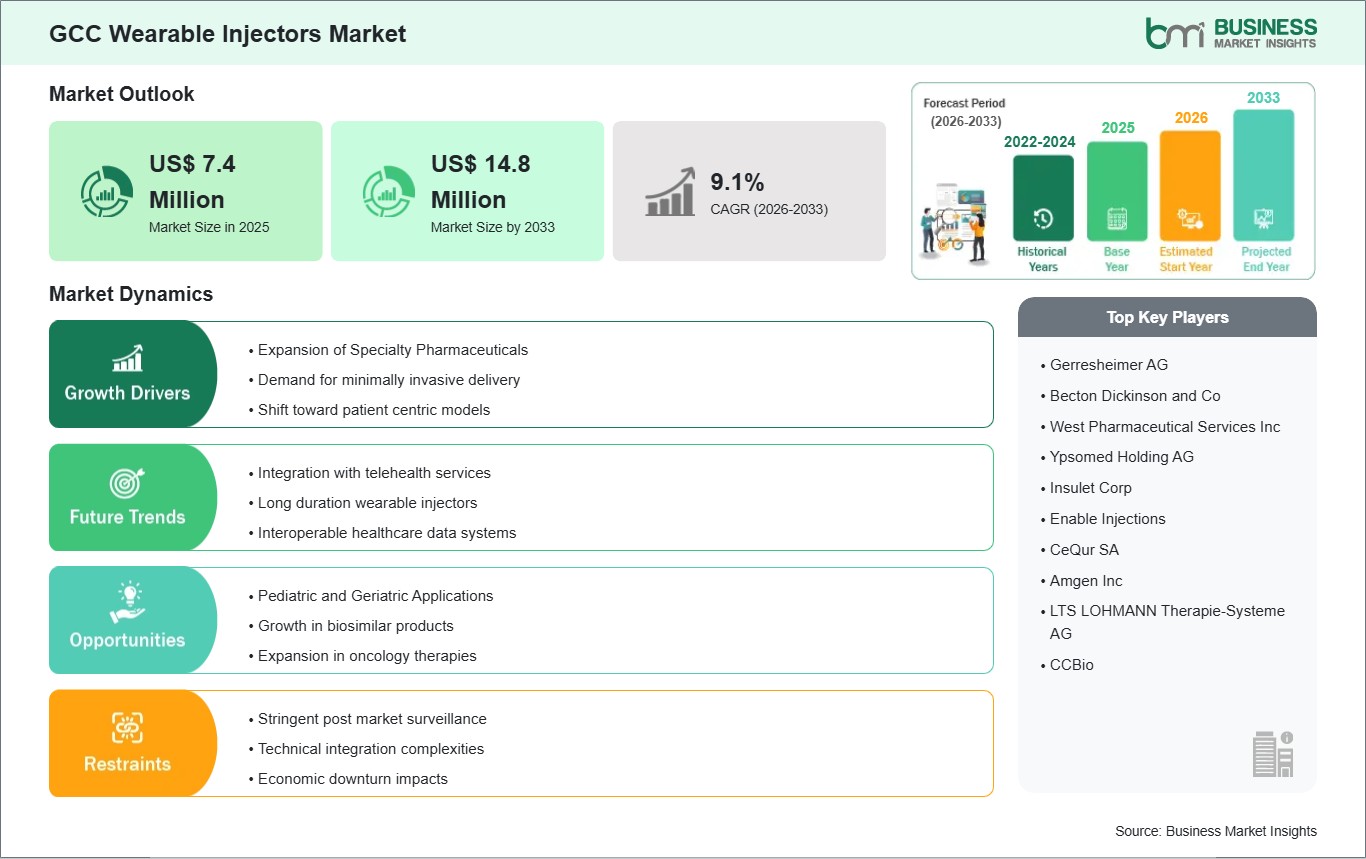

The GCC Wearable Injectors Market size is expected to reach US$ 14.8 million by 2033 from US$ 7.4 million in 2025. The market is estimated to record a CAGR of 9.1% from 2026 to 2033.

Executive Summary and GCC Wearable Injectors Market Analysis:

The GCC wearable injectors market is experiencing accelerated growth driven by rising chronic disease prevalence, increased adoption of biologic therapies, and a strategic shift toward patient-centric care. Countries such as Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, Bahrain, and Oman are witnessing increasing incidences of diabetes, autoimmune disorders, and oncology conditions, which are driving demand for self-administration devices capable of delivering high-volume therapies with accuracy and convenience. Wearable injectors offer a viable alternative to hospital-based injections, reducing patient dependency on clinical visits and supporting home-based care initiatives. Market dynamics are characterized by competition between established multinational device manufacturers and emerging regional players focused on localized solutions. Device innovation is a key differentiator, with emphasis on ergonomics, user-friendliness, extended wear times, and smart connectivity features such as remote monitoring, dose tracking, and integration with mobile health platforms. These connected devices enable healthcare providers to monitor adherence, intervene proactively in case of dosing irregularities, and personalize therapy regimens, enhancing both clinical outcomes and patient satisfaction. Regulatory frameworks in the GCC are generally favorable, with countries such as Saudi Arabia and the UAE streamlining approval processes to encourage the adoption of advanced medical devices. Distribution channels leverage hospitals, specialty clinics, and pharmacy-led networks, while telemedicine-supported home delivery services are emerging as critical facilitators of accessibility. Physician engagement and patient education programs remain central to driving adoption, particularly in markets where self-injection is still gaining acceptance. Cost considerations, insurance coverage variability, and alignment with national healthcare strategies continue to influence adoption patterns. Nevertheless, increasing digital health penetration, government initiatives supporting chronic care management, and rising patient awareness of self-administration benefits indicate significant growth potential. Overall, the GCC wearable injectors market is positioned to expand steadily as the region embraces innovative, patient-centered, and digitally integrated therapeutic solutions.

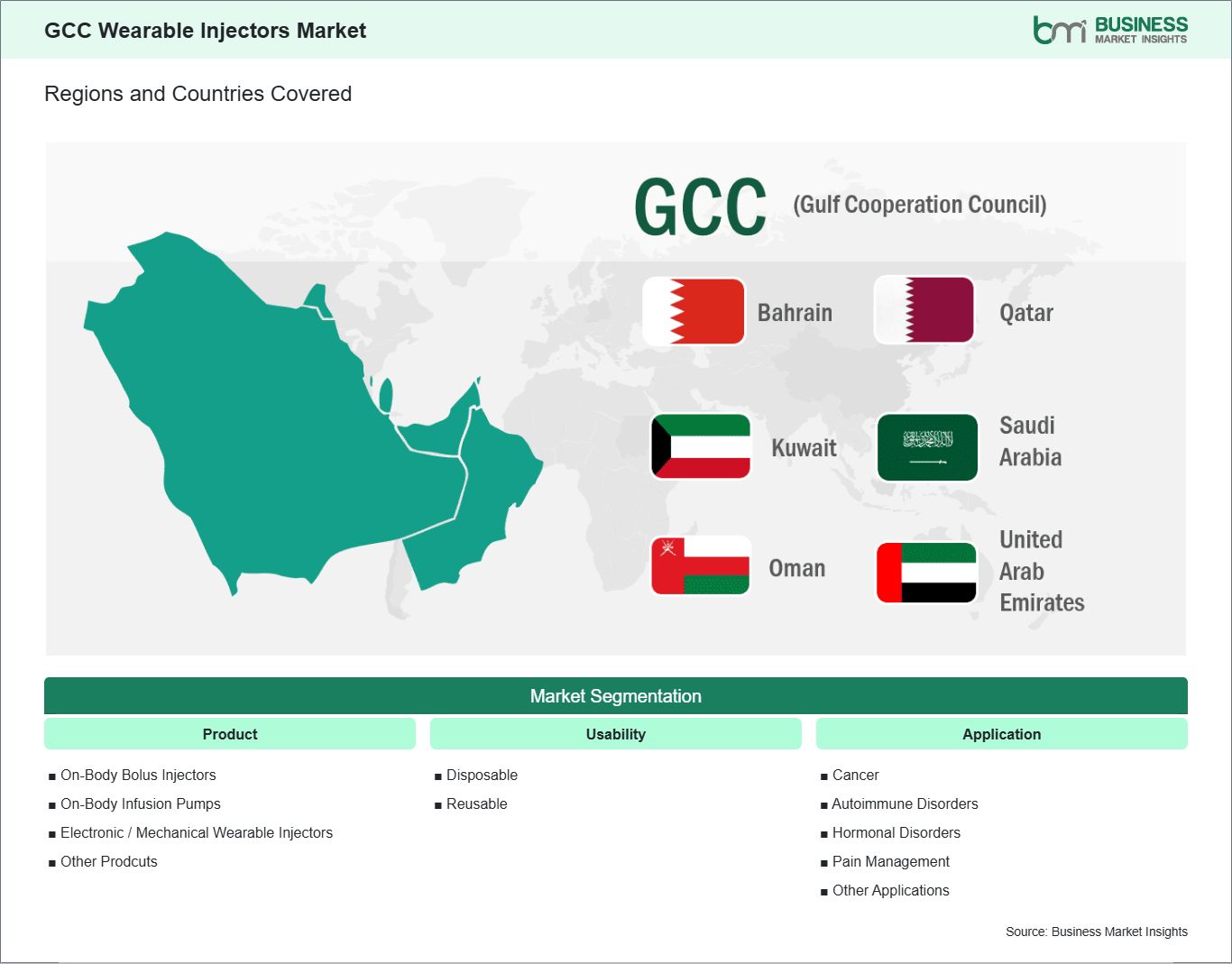

Key segments that contributed to the derivation of the GCC wearable injectors market analysis are product, usability, and application.

By product, the wearable injectors market is segmented into on-body bolus injectors, on-body infusion pumps, electronic / mechanical wearable injectors, and others. The on-body bolus injectors segment dominated the market in 2025.

Based on usability, the wearable injectors market is categorized into disposable and reusable. The disposable segment dominated the market in 2025.

In terms of application, the market is classified into cancer, autoimmune disorders, hormonal disorders, pain management, and other applications. The autoimmune disorders segment dominated the market in 2025.

GCC Wearable Injectors Market Drivers and Opportunities:

Expansion of Specialty Pharmaceuticals

The GCC region is witnessing a rapid shift toward high-value specialty pharmaceuticals, driven by government initiatives to improve treatment outcomes for complex and chronic diseases. Countries like Saudi Arabia and the UAE are actively supporting the introduction of advanced biologics, targeted therapies, and gene-based medications, reflecting a broader ambition to elevate the quality of care in line with global standards. This expansion is creating demand for drug delivery solutions that can manage the unique requirements of specialty medicines, including high viscosity, precise dosing, and stability concerns. Wearable injectors are increasingly positioned as the ideal delivery platform to complement these advanced therapies, enabling patients to safely self-administer medications outside hospital settings while maintaining treatment consistency. In addition, the growing private healthcare sector in the GCC is fostering the adoption of technologies that enhance patient convenience and improve operational efficiency. Specialty pharmaceuticals often require complex dosing schedules that can strain hospital resources if delivered exclusively through clinical visits. Wearable injectors address this challenge by decentralizing therapy administration, allowing patients to follow treatment plans at home or in community care settings. This aligns with regional health strategies that aim to reduce inpatient loads and optimize healthcare delivery efficiency, particularly in rapidly growing urban centers like Riyadh, Dubai, and Doha. Pharmaceutical companies operating in the GCC are also leveraging wearable injectors to differentiate their specialty drug offerings. By bundling therapy with advanced delivery devices, manufacturers can enhance perceived value and support adherence, while also gathering real-world usage data that informs ongoing therapy optimization. Collaborative efforts between local distributors, healthcare providers, and device manufacturers are creating integrated programs that ensure both patients and clinicians are confident in the safety and efficacy of self-administered specialty treatments. This ecosystem approach is fueling the market for wearable injectors as part of a broader strategy to expand specialty pharmaceutical adoption in the region.

Pediatric and Geriatric Applications

The GCC market is uniquely influenced by a dual demographic focus: a growing elderly population alongside a dynamic pediatric segment with evolving healthcare needs. In the geriatric population, chronic conditions such as diabetes, arthritis, and cardiovascular diseases require frequent or long-term injectable therapies. Wearable injectors offer an accessible solution by simplifying administration and reducing the physical strain associated with traditional injections, enabling older patients to manage their treatment independently while maintaining a higher quality of life. For pediatric patients, wearable injectors address both clinical and emotional challenges associated with repeated injections. Children with growth disorders, autoimmune conditions, or chronic illnesses often experience anxiety and discomfort with conventional therapy methods. Wearable injectors designed with child-friendly ergonomics and minimal pain delivery can enhance adherence and improve overall treatment experience. Caregivers in the GCC are increasingly receptive to these devices as they offer reassurance, reduce the burden of frequent hospital visits, and fit seamlessly into family routines, supporting continuity of care for young patients. Healthcare systems in the GCC are also adapting clinical protocols and support services to optimize the use of wearable injectors across age groups. Training programs for caregivers, guidance for clinicians, and integration with digital health monitoring are becoming standard practices in larger hospitals and private clinics. Device manufacturers are responding by developing injectors with adjustable dosing, user-friendly interfaces, and features that accommodate varying mobility and dexterity levels. This emphasis on patient-centered design for both children and older adults strengthens the adoption potential of wearable injectors, highlighting the GCC market as one that values devices tailored to the full spectrum of patient needs.

GCC Wearable Injectors Market Size and Share Analysis:

The GCC Wearable Injectors Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, usability, and application, offering insights into their contribution to overall market performance.

By product, the on-body bolus injectors subsegment dominated the market in 2025, driven by a growing focus on advanced drug delivery solutions that support enhanced mobility and adherence for chronic conditions.

Based on usability, the disposable subsegment dominated the market in 2025, driven by a strong preference for cost‑effective, low‑risk single‑use devices that simplify self‑administration.

In terms of application, the autoimmune disorders subsegment dominated the market in 2025, driven by rising prevalence of immune‑mediated diseases and increased access to biologic therapies requiring frequent injections.

GCC Wearable Injectors Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 7.4 Million

Market Size by 2033

US$ 14.8 Million

CAGR (2026 - 2033)

9.1%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

On-Body Bolus Injectors

On-Body Infusion Pumps

Electronic / Mechanical Wearable Injectors

Other Prodcuts

By Usability

Disposable

Reusable

By Application

Cancer

Autoimmune Disorders

Hormonal Disorders

Pain Management

Other Applications

Regions and Countries Covered

GCC

UAE, Bahrain, Saudi Arabia, Oman, Qatar, Kuwait

Market leaders and key company profiles

Gerresheimer AG

Becton Dickinson and Co

West Pharmaceutical Services Inc

Ypsomed Holding AG

Insulet Corp

Enable Injections

CeQur SA

Amgen Inc

LTS LOHMANN Therapie-Systeme AG

CCBio

Get more information on this report

GCC Wearable Injectors Market Report Coverage and Deliverables:

The "GCC Wearable Injectors Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

GCC Wearable Injectors Market size and forecast at regional and country levels for all segments covered under the scope

GCC Wearable Injectors Market trends, as well as drivers, restraints, and opportunities

GCC Wearable Injectors Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the GCC Wearable Injectors Market

Detailed company profiles, including SWOT analysis

The geographical scope of the GCC Wearable Injectors Market report is divided into the UAE, Bahrain, Saudi Arabia, Oman, Qatar, and Kuwait. The UAE held the largest share in 2025.

Country-level dynamics in the GCC wearable injectors market demonstrate diverse adoption patterns driven by healthcare infrastructure, regulatory support, and patient behavior. Saudi Arabia emerges as the dominant market, fueled by a large patient population, increasing chronic disease burden, and robust private and public healthcare infrastructure. Urban centers such as Riyadh, Jeddah, and Dammam are leading adoption, with hospitals and specialty clinics integrating wearable injectors into chronic disease management programs. Government initiatives supporting home-based care and telemedicine further strengthen Saudi Arabia’s leadership position. The United Arab Emirates represents a highly advanced market, characterized by early adoption of wearable injectors in Dubai and Abu Dhabi specialty clinics. Integration with telehealth platforms and strong insurance coverage enable patients to access connected devices, while urbanized healthcare networks provide training and monitoring support. Qatar and Kuwait demonstrate growing adoption in urban centers, driven by high-income patient populations and expanding private hospitals. Adoption is primarily concentrated in diabetes and oncology care programs, with digital health integration facilitating patient engagement and therapy adherence. Bahrain and Oman represent smaller but emerging markets, where adoption is concentrated in specialty clinics in Manama and Muscat. Awareness campaigns, digital health initiatives, and partnerships with multinational manufacturers are critical for expanding penetration. Across the GCC, Saudi Arabia dominates the market, while the UAE, Qatar, Kuwait, Bahrain, and Oman provide complementary growth opportunities. Companies entering the region must adopt country-specific strategies focusing on regulatory compliance, clinician training, patient education, and integration with telemedicine and digital health platforms to maximize adoption and establish a sustainable presence.

Get more information on this report

GCC Wearable Injectors Market Research Report Guidance:

The report includes qualitative and quantitative data in the GCC Wearable Injectors Market across product, usability, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the GCC Wearable Injectors Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the GCC Wearable Injectors Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the GCC Wearable Injectors Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover GCC Wearable Injectors Market segments by product, usability, application, and geography across the UAE, Bahrain, Saudi Arabia, Oman, Qatar, and Kuwait. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the GCC Wearable Injectors Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

GCC Wearable Injectors Market News and Key Development:

The GCC Wearable Injectors Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the GCC wearable injectors market are:

In December 2025, Enable Injections, Inc. announced that its EMPAVELI Injector, based on the enFuse on‑body delivery system, received regulatory approval from the Saudi Food and Drug Authority (SFDA) under the country’s medical device authorization framework—a key step enabling legal sale and distribution of this large‑volume subcutaneous injection device in the Kingdom of Saudi Arabia.

In January 2026, Enable Injections announced a US$ 30 million investment from Sanofi aimed at accelerating manufacturing capabilities for its enFuse wearable drug delivery platform, strengthening production readiness for global and GCC launches.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - GCC Wearable Injectors Market

Gerresheimer AG

Becton Dickinson and Co

West Pharmaceutical Services Inc

Ypsomed Holding AG

Insulet Corp

Enable Injections

CeQur SA

Amgen Inc

LTS LOHMANN Therapie-Systeme AG

CCBio

Frequently Asked Questions

How big is the GCC Wearable Injectors Market?

The GCC Wearable Injectors Market is valued at US$ 7.4 Million in 2025, it is projected to reach US$ 14.8 Million by 2033.

What is the CAGR for GCC Wearable Injectors Market by (2026 - 2033)?

As per our report GCC Wearable Injectors Market, the market size is valued at US$ 7.4 Million in 2025, projecting it to reach US$ 14.8 Million by 2033. This translates to a CAGR of approximately 9.1% during the forecast period.

What segments are covered in this report?

The GCC Wearable Injectors Market report typically cover these key segments-

Application (Cancer, Autoimmune Disorders, Hormonal Disorders, Pain Management, Other Applications)

What is the historic period, base year, and forecast period taken for GCC Wearable Injectors Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the GCC Wearable Injectors Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in GCC Wearable Injectors Market?

The GCC Wearable Injectors Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Gerresheimer AG

Becton Dickinson and Co

West Pharmaceutical Services Inc

Ypsomed Holding AG

Insulet Corp

Enable Injections

CeQur SA

Amgen Inc

LTS LOHMANN Therapie-Systeme AG

CCBio

Who should buy this report?

The GCC Wearable Injectors Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the GCC Wearable Injectors Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For GCC Wearable Injectors Market

Get Free Sample For GCC Wearable Injectors Market