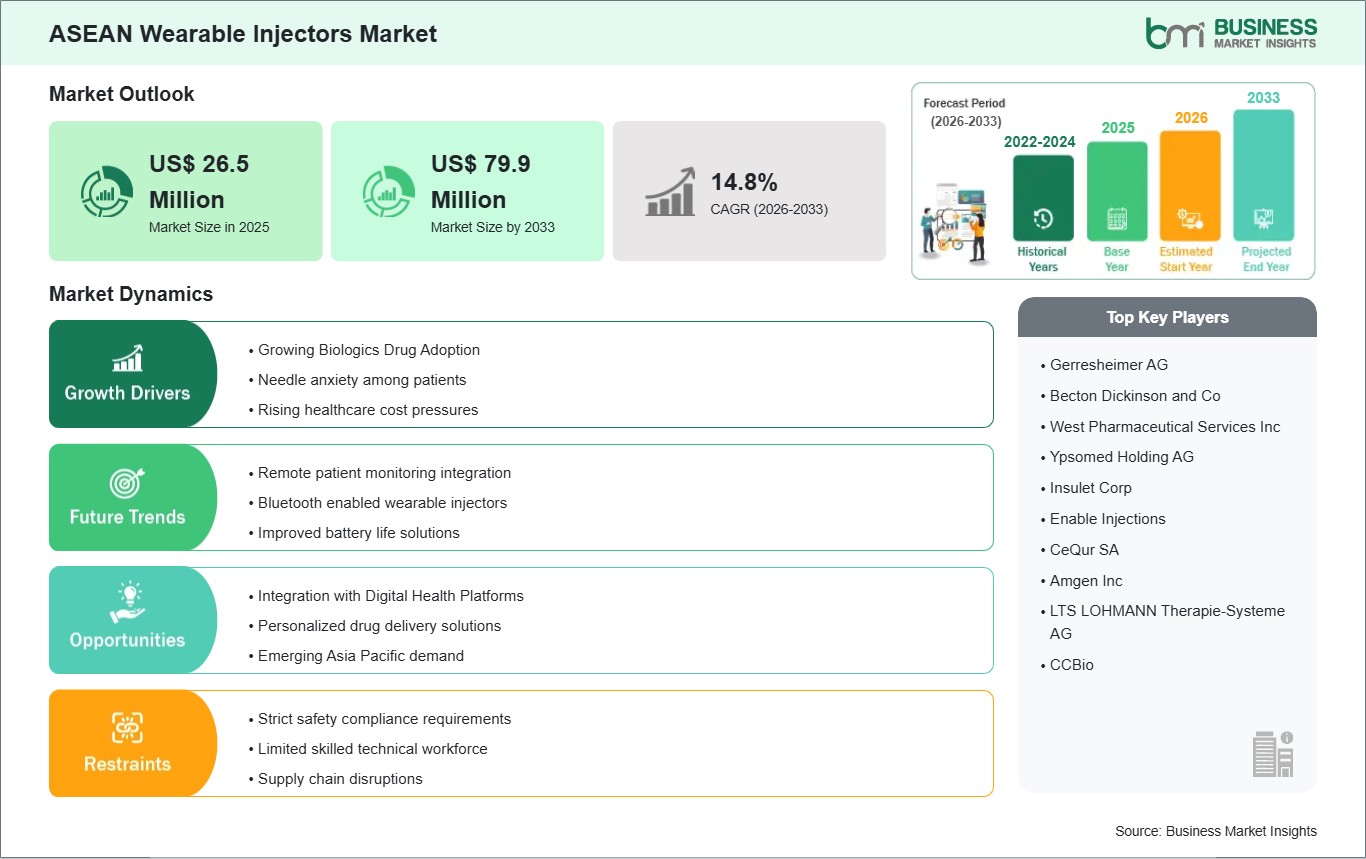

The ASEAN Wearable Injectors Market size is expected to reach US$ 79.9 million by 2033 from US$ 26.5 million in 2025. The market is estimated to record a CAGR of 14.8% from 2026 to 2033.

Executive Summary and ASEAN Wearable Injectors Market Analysis:

Wearable injectors are experiencing accelerated adoption in the ASEAN region as healthcare systems are transitioning toward patient-centric care and decentralized drug delivery models. The increasing prevalence of chronic diseases such as diabetes, autoimmune disorders, and oncology conditions is creating demand for innovative administration solutions that reduce hospital visits and improve adherence. Wearable injectors, offering controlled subcutaneous or intradermal delivery of high-volume therapies, are well-positioned to address these needs, particularly in urban healthcare hubs like Singapore, Bangkok, and Kuala Lumpur. Market dynamics are shaped by both multinational device manufacturers and emerging local medical technology firms, with competition driven by innovation in ergonomics, extended wear time, and digital connectivity. Integration of smart features, including wireless monitoring and dosing reminders, is enhancing patient engagement while enabling healthcare providers to remotely track treatment adherence. Regulatory frameworks across ASEAN countries are heterogeneous, with Singapore and Malaysia exhibiting more streamlined approval processes compared to Indonesia and the Philippines, where multi-tiered regulatory pathways require strategic navigation. Distribution models are evolving, with private hospital chains, specialty clinics, and pharmacy-led channels increasingly facilitating access to wearable injectors. Strategic partnerships between global manufacturers and regional distributors are critical to expand reach, while education campaigns targeted at physicians and patients play a central role in adoption. Affordability remains a key constraint, particularly in emerging ASEAN markets where out-of-pocket healthcare expenditure is high. Nonetheless, growing investment in home-based care infrastructure and rising awareness of self-administration convenience are expected to propel adoption, making wearable injectors a transformative component in the region’s evolving therapeutic landscape.

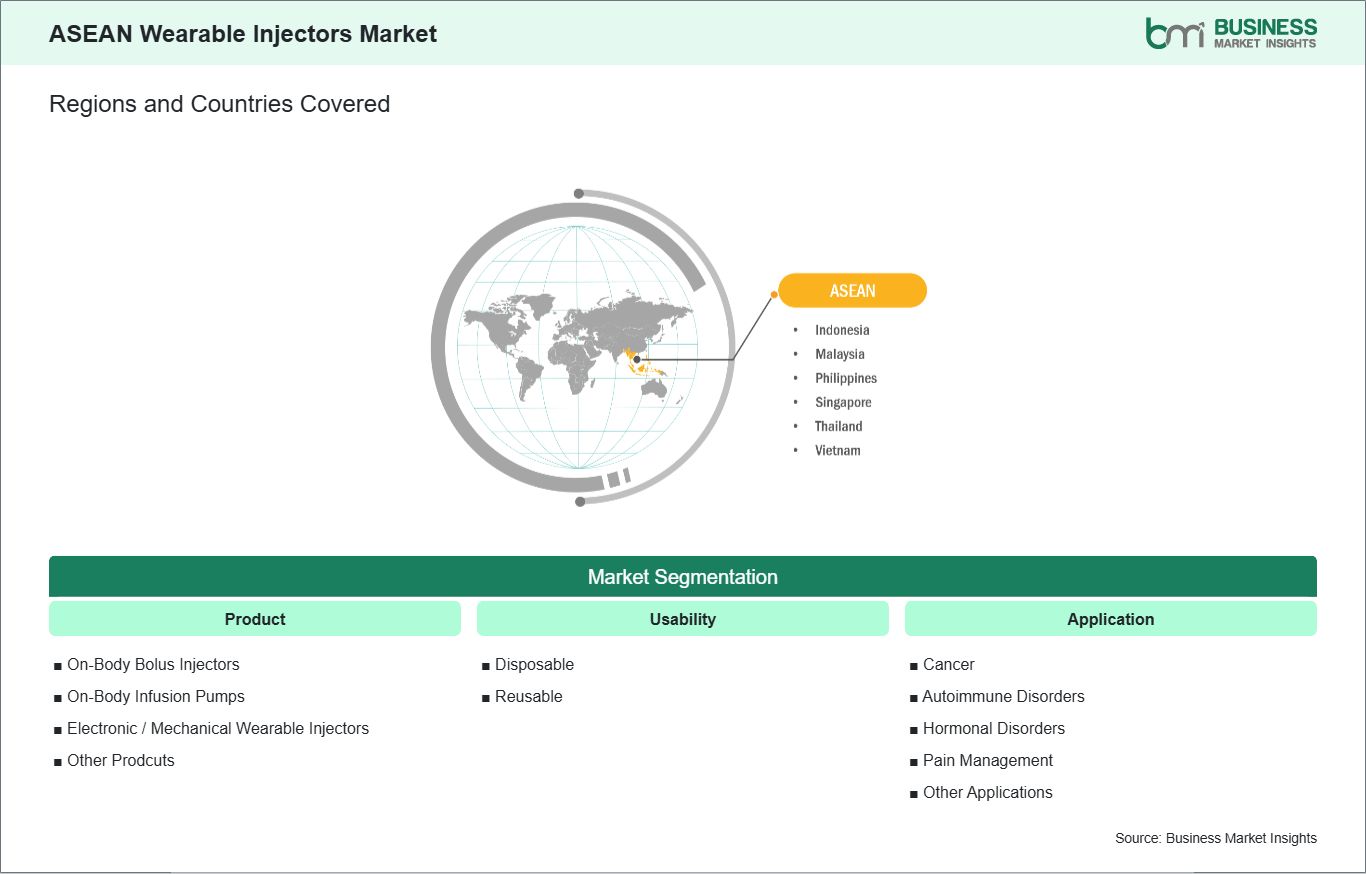

Key segments that contributed to the derivation of the ASEAN wearable injectors market analysis are product, usability, and application.

By product, the wearable injectors market is segmented into on-body bolus injectors, on-body infusion pumps, electronic / mechanical wearable injectors, and others. The on-body bolus injectors segment dominated the market in 2025.

Based on usability, the wearable injectors market is categorized into disposable and reusable. The disposable segment dominated the market in 2025.

In terms of application, the market is classified into cancer, autoimmune disorders, hormonal disorders, pain management, and other applications. The autoimmune disorders segment dominated the market in 2025.

ASEAN Wearable Injectors Market Drivers and Opportunities:

Growing Biologics Drug Adoption

The ASEAN region is witnessing a marked shift in how medicines are being developed, prescribed, and administered, with biologic therapies gaining prominence across multiple therapeutic areas. Healthcare systems in countries such as Singapore, Thailand, Malaysia, and Vietnam are actively incorporating biologics into treatment regimens for conditions that were once managed primarily with conventional small‑molecule drugs. This trend is prompting pharmaceutical companies and healthcare providers to explore delivery solutions that can keep pace with the unique requirements of large‑molecule medications, strengthening the case for wearable injectors that are designed to handle complex formulations with precision and reliability. Biologics are increasingly seen as essential tools for addressing chronic and immune‑mediated diseases in ASEAN. Healthcare stakeholders are expanding formularies and treatment protocols to include newer protein‑based therapies, reflecting broader acceptance of these advanced modalities. This has stimulated interest from medical device developers and drug delivery innovators seeking to offer solutions that improve patient convenience and access to biologics outside traditional clinical environments. Wearable injectors, with their capacity for controlled subcutaneous delivery and reduced dependency on frequent clinic visits, are positioned to play a strategic role in this evolving treatment landscape. Regional regulatory bodies and health authorities are also adapting to frameworks to better accommodate biologics and associated delivery technologies. Harmonised guidelines across ASEAN member states are encouraging more efficient local registration pathways for biosimilars and originator biologics, fostering a more predictable environment for market entry and scale‑up. These regulatory developments dovetail with broader efforts to modernize healthcare delivery, incentivizing manufacturers to align product portfolios with regional needs and enabling healthcare providers to offer patients a wider suite of therapeutic options supported by advanced wearable injection systems.

Integration with Digital Health Platforms

The ASEAN healthcare ecosystem is rapidly embracing digital transformation, driven by national strategies that prioritize interoperability, telemedicine expansion, and patient engagement technologies. Governments and private sector partners are building frameworks that support connected health architectures, including electronic health records, remote patient monitoring platforms, and mobile health applications. This digital momentum creates fertile ground for wearable injectors that can integrate with broader health information systems, enabling data‑driven care coordination and improved adherence to therapy regimens. As digital health adoption grows, stakeholders are increasingly focused on solutions that can capture and transmit patient‑level device data securely and in real time. Wearable injectors with embedded connectivity features become more than just drug delivery devices; they serve as nodes within an expanding digital care continuum. Integrating wearable injectors with digital platforms helps clinicians monitor adherence, verify dosing history, and adjust care plans without requiring frequent face‑to‑face visits. This is especially relevant for chronic care management and follow‑up, where continuous feedback loops between patients and providers can enhance outcomes and foster more personalised care journeys. Digital health strategies across ASEAN also promote cross‑platform interoperability and standardised health data exchange, enabling connected devices to work seamlessly with national and private sector systems. This regional emphasis on unified digital health frameworks supports the evolution of wearable injection technologies from isolated tools to integrated assets within clinical workflows and patient homecare protocols. As digital maturity increases across the association, adoption of smart wearable injectors is likely to be catalyzed by the value these devices bring in bridging physical therapy delivery with remote monitoring and analytics.

ASEAN Wearable Injectors Market Size and Share Analysis:

The ASEAN Wearable Injectors Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, usability, and application, offering insights into their contribution to overall market performance.

By product, the on-body bolus injectors subsegment dominated the market in 2025, driven by increasing preference for advanced, high‑volume drug delivery systems that offer precise dosing and ease of use for chronic therapies.

Based on usability, the disposable subsegment dominated the market in 2025, driven by the demand for cost‑effective, single‑use devices that reduce contamination risk and simplify patient self‑administration.

In terms of application, the autoimmune disorders subsegment dominated the market in 2025, driven by the rising prevalence of conditions like rheumatoid arthritis and psoriasis in the region, boosting demand for frequent biologic injections.

Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam

Market leaders and key company profiles

Gerresheimer AG

Becton Dickinson and Co

West Pharmaceutical Services Inc

Ypsomed Holding AG

Insulet Corp

Enable Injections

CeQur SA

Amgen Inc

LTS LOHMANN Therapie-Systeme AG

CCBio

Get more information on this report

ASEAN Wearable Injectors Market Report Coverage and Deliverables:

The "ASEAN Wearable Injectors Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

ASEAN Wearable Injectors Market size and forecast at regional and country levels for all segments covered under the scope

ASEAN Wearable Injectors Market trends, as well as drivers, restraints, and opportunities

ASEAN Wearable Injectors Market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the ASEAN Wearable Injectors Market

Detailed company profiles, including SWOT analysis

The geographical scope of the ASEAN Wearable Injectors Market report is divided into Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam. Indonesia held the largest share in 2025.

Within the ASEAN wearable injectors market, Indonesia emerges as the dominant country, driven by its large population, rising prevalence of chronic diseases such as diabetes and autoimmune conditions, and expanding private healthcare sector. Adoption is concentrated in major urban centers like Jakarta, Surabaya, and Bandung, where specialty clinics and private hospitals are increasingly incorporating wearable injectors into patient care programs. Growing awareness among patients about the convenience of self-administration and improved treatment adherence is further fueling demand, making Indonesia a strategic hub for device manufacturers targeting Southeast Asia. Thailand represents a secondary growth market, supported by urban hospitals and specialty care facilities in Bangkok, Chiang Mai, and Phuket. Government initiatives promoting home-based healthcare and integration of wearable drug delivery devices into chronic care programs are creating favorable adoption conditions. Additionally, digital health initiatives enabling remote monitoring and patient follow-up are enhancing the relevance of wearable injectors in the Thai healthcare ecosystem. Malaysia is experiencing steady adoption, particularly in Kuala Lumpur and Penang, where private hospitals and specialty clinics are increasingly leveraging wearable injectors for high-volume biologic therapies. Patient convenience, coupled with gradual integration with mobile health platforms for adherence monitoring, is driving adoption, though cost and reimbursement limitations remain key constraints for wider use. Egypt-level markets were not included in ASEAN, so focusing on Algeria is not relevant here; instead, the fourth focus country in ASEAN is the Philippines, where adoption is emerging but concentrated in urban centers such as Manila and Cebu. Uptake is supported by private hospital chains and high-income patient segments, although fragmented healthcare infrastructure and limited insurance coverage restrict broader penetration. Overall, Indonesia dominates the ASEAN wearable injector market, while Thailand, Malaysia, and the Philippines represent complementary markets with differentiated adoption drivers. Tailored strategies addressing regulatory compliance, clinician training, patient education, and affordability will be critical for companies aiming to capitalize on the diverse opportunities across the region.

Get more information on this report

ASEAN Wearable Injectors Market Research Report Guidance:

The report includes qualitative and quantitative data in the ASEAN Wearable Injectors Market across product, usability, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the ASEAN Wearable Injectors Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the ASEAN Wearable Injectors Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the ASEAN Wearable Injectors Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover ASEAN Wearable Injectors Market segments by product, usability, application, and geography across Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the ASEAN Wearable Injectors Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

ASEAN Wearable Injectors Market News and Key Development:

The ASEAN Wearable Injectors Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the ASEAN wearable injectors market are:

In May 2024, Enable Injections expanded its strategic partnership with Roche, granting Roche a worldwide, exclusive license to develop and commercialize combination products using Enable’s enFuse wearable drug delivery technology, boosting applications of wearable injectors with Roche’s molecules.

In January 2026, ten23 health and BD announced a strategic manufacturing partnership to support commercialization and supply chain readiness of the BD Libertas Wearable Injector, offering integrated CDMO services to speed development and market entry.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

The List of Companies - ASEAN Wearable Injectors Market

Gerresheimer AG

Becton Dickinson and Co

West Pharmaceutical Services Inc

Ypsomed Holding AG

Insulet Corp

Enable Injections

CeQur SA

Amgen Inc

LTS LOHMANN Therapie-Systeme AG

CCBio

Frequently Asked Questions

How big is the ASEAN Wearable Injectors Market?

The ASEAN Wearable Injectors Market is valued at US$ 26.5 Million in 2025, it is projected to reach US$ 79.9 Million by 2033.

What is the CAGR for ASEAN Wearable Injectors Market by (2026 - 2033)?

As per our report ASEAN Wearable Injectors Market, the market size is valued at US$ 26.5 Million in 2025, projecting it to reach US$ 79.9 Million by 2033. This translates to a CAGR of approximately 14.8% during the forecast period.

What segments are covered in this report?

The ASEAN Wearable Injectors Market report typically cover these key segments-

Application (Cancer, Autoimmune Disorders, Hormonal Disorders, Pain Management, Other Applications)

What is the historic period, base year, and forecast period taken for ASEAN Wearable Injectors Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the ASEAN Wearable Injectors Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in ASEAN Wearable Injectors Market?

The ASEAN Wearable Injectors Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Gerresheimer AG

Becton Dickinson and Co

West Pharmaceutical Services Inc

Ypsomed Holding AG

Insulet Corp

Enable Injections

CeQur SA

Amgen Inc

LTS LOHMANN Therapie-Systeme AG

CCBio

Who should buy this report?

The ASEAN Wearable Injectors Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the ASEAN Wearable Injectors Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For ASEAN Wearable Injectors Market

Get Free Sample For ASEAN Wearable Injectors Market