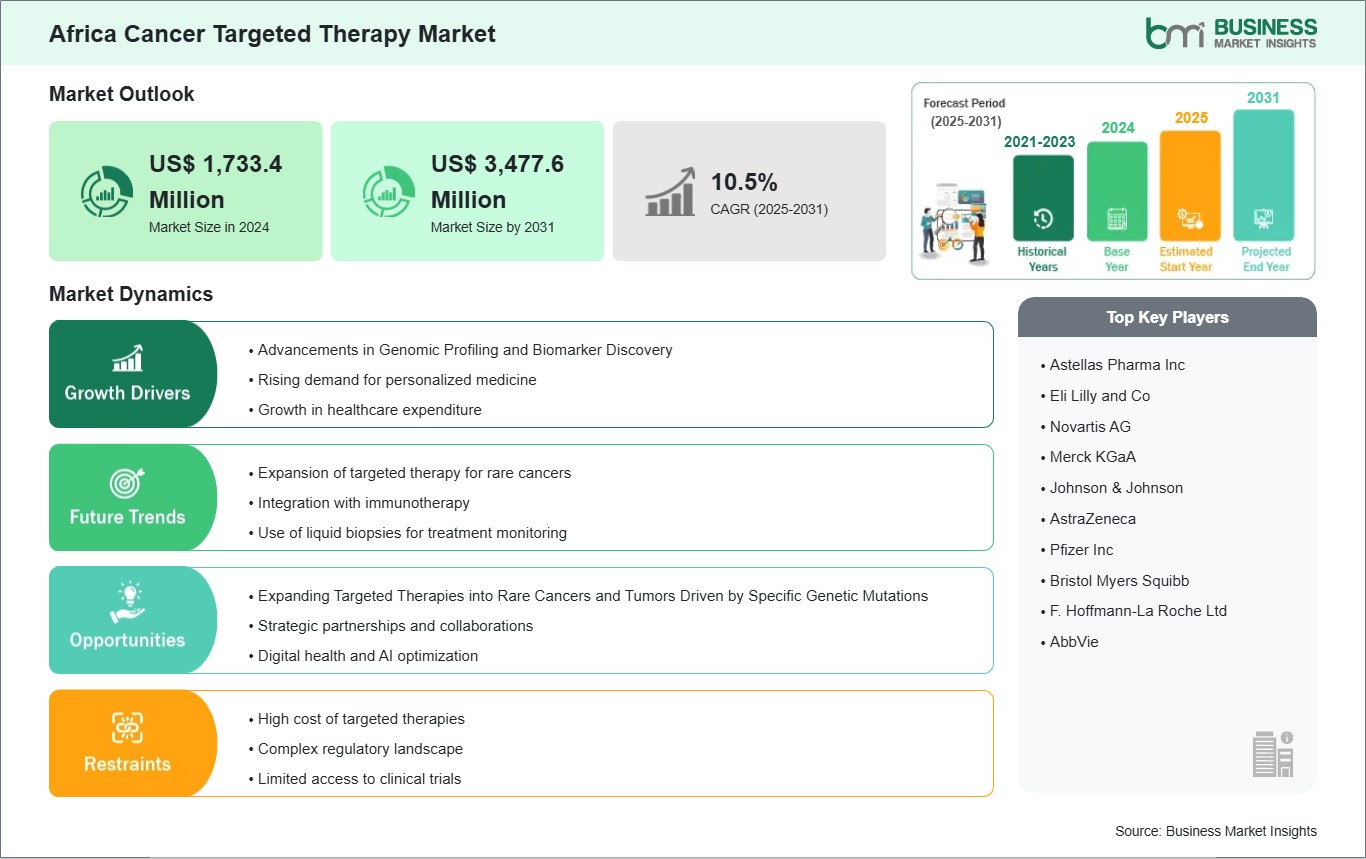

The Africa Cancer Targeted Therapy Market size is expected to reach US$ 3,477.6 million by 2031 from US$ 1,733.4 million in 2024. The market is estimated to record a CAGR of 10.5% from 2025 to 2031.

Executive Summary and Africa Cancer Targeted Therapy Market Analysis:

The Africa cancer targeted therapy market is characterized by a dynamic interplay of evolving clinical protocols, emerging payer frameworks, and strategic investment shifts. Over the past decade, healthcare systems across Africa have transitioned from largely symptom-driven oncology care to more precision-focused treatment pathways, driven by growing access to diagnostic capabilities and an expanding oncology workforce. This has spurred demand for targeted therapies that offer improved efficacy and reduced toxicity compared to conventional chemotherapy. Key market drivers include increasing cancer incidence due to aging populations, urbanization, and lifestyle-related risk factors, alongside expanding public-private partnerships aimed at strengthening oncology infrastructure. At the same time, the market faces notable barriers, including fragmented healthcare delivery systems, limited reimbursement coverage, and disparities in diagnostic testing availability. Market participants are responding by forming strategic alliances with local healthcare providers, launching patient access programs, and optimizing supply chain logistics to overcome distribution bottlenecks.

Competitive dynamics are intensifying as multinational biopharma companies expand their footprint through licensing agreements and localized manufacturing initiatives, while regional players focus on biosimilar development and portfolio diversification. Regulatory environments are gradually becoming more favorable, with some countries adopting expedited review pathways for oncology drugs and fostering collaborative frameworks for clinical trial participation. Overall, the market is shifting toward value-based care models where treatment decisions increasingly depend on biomarker testing, cost-effectiveness assessments, and real-world evidence. This creates opportunities for companies that can integrate diagnostic services with therapy offerings and develop scalable access models that address affordability and patient adherence.

Africa Cancer Targeted Therapy Market - Strategic Insights:

Get more information on this report

Africa Cancer Targeted Therapy Market Segmentation Analysis:

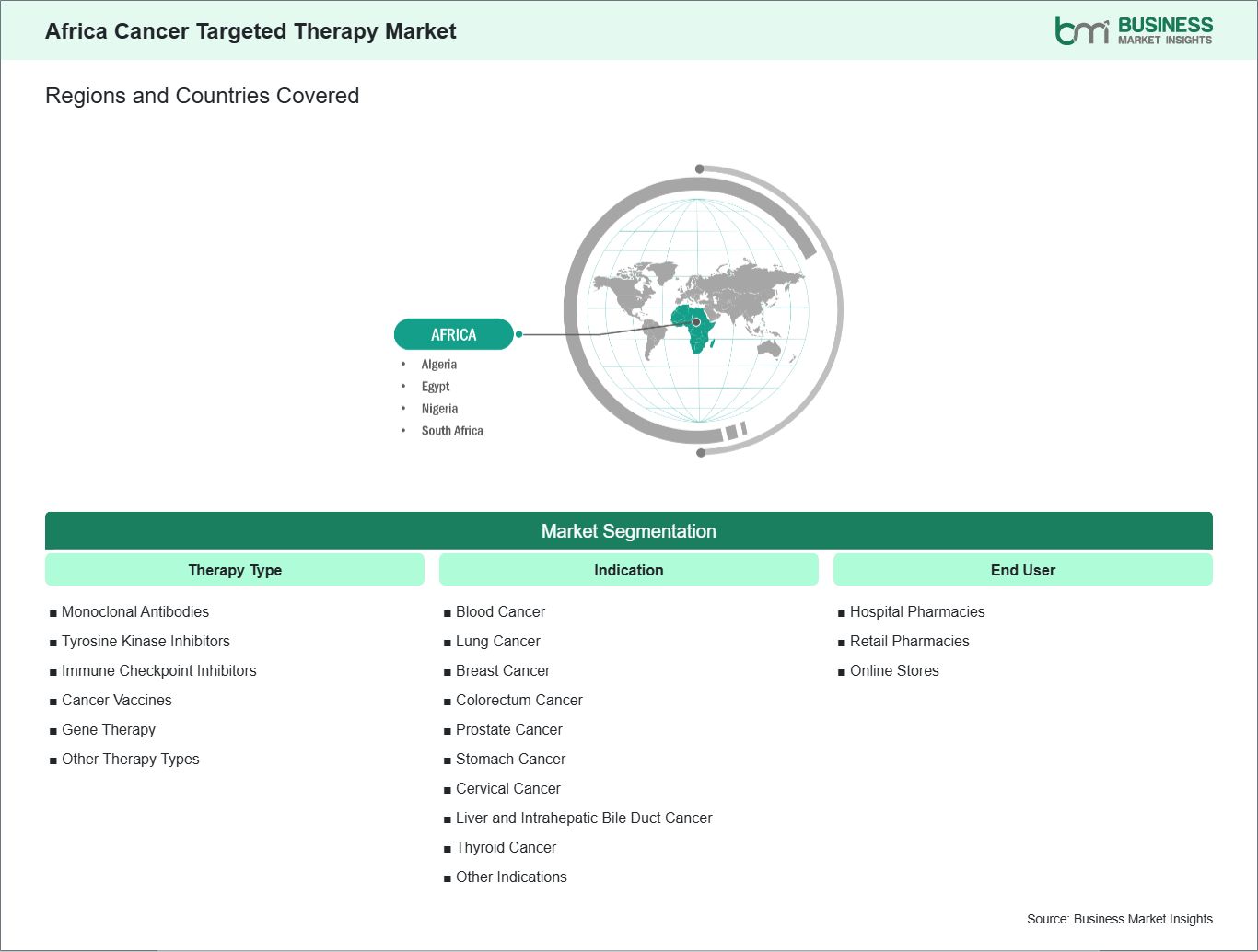

Key segments that contributed to the derivation of the Africa Cancer Targeted Therapy market analysis are therapy type, indication, and distribution channel.

By therapy type, the cancer targeted therapy market is segmented into monoclonal antibodies, tyrosine kinase inhibitors, immune checkpoint inhibitors, cancer vaccines, gene therapy, and others. The monoclonal antibodies segment dominated the market in 2024.

Based on indication, the cancer targeted therapy market is segmented into blood cancer, lung cancer, breast cancer, colorectum cancer, prostate cancer, stomach cancer, cervical cancer, liver and intrahepatic bile duct cancer, thyroid cancer, and other indications. The lung cancer segment dominated the market in 2024.

In terms of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online stores. The hospital pharmacies segment dominated the market in 2024.

Africa Cancer Targeted Therapy Market Drivers and Opportunities:

Advancements in Genomic Profiling and Biomarker Discovery

Advancements in genomic profiling and biomarker discovery have become key drivers of the global cancer targeted therapy market. The widespread adoption of next-generation sequencing (NGS), whole-exome sequencing, and liquid biopsy technologies has enabled clinicians to identify precise genetic alterations—such as EGFR, ALK, RET, BRAF, FGFR, and PIK3CA mutations—that directly influence tumor behavior and treatment response. This molecular-level understanding has shifted oncology away from a one-size-fits-all chemotherapy approach toward precision medicine, where therapies are selected based on an individual patient's tumor genomics. Improved biomarker discovery has significantly increased drug development efficiency and regulatory success rates. Pharmaceutical companies can now design highly selective targeted therapies and antibody–drug conjugates (ADCs) that act on well-validated molecular targets, improving efficacy while reducing systemic toxicity. Biomarkers also enable better patient stratification in clinical trials, leading to smaller, faster, and more successful studies. Regulatory agencies increasingly require companion diagnostics alongside targeted therapies, further strengthening the commercial ecosystem around genomic testing.

Liquid biopsy innovations—which allow detection of circulating tumor DNA (ctDNA)—have expanded the use of targeted therapies beyond initial diagnosis into disease monitoring, minimal residual disease detection, and treatment resistance tracking. These innovations have increased therapy duration and lifecycle value for targeted drugs. Additionally, real-world genomic databases and AI-driven analytics are accelerating biomarker validation and uncovering novel targets across rare and hard-to-treat cancers. As healthcare systems increasingly reimburse genomic testing and precision diagnostics, adoption rates continue to rise globally. Collectively, these advancements are expanding eligible patient populations, improving clinical outcomes, and driving sustained growth in the market.

Expanding Targeted Therapies into Rare Cancers and Tumors Driven by Specific Genetic Mutations

The expansion of targeted therapies into rare cancers and tumors driven by specific genetic mutations represents a major opportunity. Traditionally, rare cancers have faced limited treatment options due to small patient populations, high development costs, and low commercial attractiveness. However, advances in genomic profiling have demonstrated that many rare tumors harbor actionable genetic alterations that are shared across multiple cancer types, enabling a shift toward mutation-driven treatment strategies.

Tumor-agnostic drug development has played a critical role in this transformation. Targeted therapies addressing biomarkers such as NTRK fusions, RET rearrangements, BRAF mutations, and FGFR alterations have gained approvals across diverse and rare malignancies. This approach allows pharmaceutical companies to expand indications for a single therapy across multiple low-incidence cancers, significantly increasing market potential. Supportive regulatory frameworks—including orphan drug designation, accelerated approval pathways, and extended market exclusivity—further enhance the commercial viability of developing therapies for rare cancers.

From a clinical perspective, targeted therapies often deliver superior efficacy and tolerability compared to conventional chemotherapy in rare genetically driven tumors. Broader adoption of next-generation sequencing and comprehensive molecular testing has also improved the identification of rare mutations, increasing the eligible patient population. Innovative clinical trial designs, such as basket and umbrella trials, have reduced development timelines and costs.

Africa Cancer Targeted Therapy Market Size and Share Analysis:

The Africa Cancer Targeted Therapy market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within therapy type, indication, and distribution channel, offering insights into their contribution to overall market performance.

By therapy type, the monoclonal antibodies subsegment dominated the market in 2024, driven by their high clinical efficacy, strong adoption of immuno-oncology and targeted biologics, and a robust pipeline supported by regulatory approvals and combination therapy use.

Based on indication, the lung cancer subsegment dominated the market in 2024, driven by the high global disease burden, rising smoking- and pollution-related risk factors, and the availability of multiple approved targeted and immunotherapy options addressing key genetic mutations.

By distribution channel, the hospital pharmacies subsegment dominated the market in 2024, driven by the centralized administration of complex oncology therapies, greater access to specialized oncology care, and hospitals serving as primary sites for cancer diagnosis, treatment initiation, and monitoring.

Africa Cancer Targeted Therapy Market Report Highlights:

Report Attribute

Details

Market size in 2024

US$ 1,733.4 Million

Market Size by 2031

US$ 3,477.6 Million

CAGR (2025 - 2031)

10.5%

Historical Data

2021-2023

Forecast period

2025-2031

Segments Covered

By Therapy Type

Monoclonal Antibodies

Tyrosine Kinase Inhibitors

Immune Checkpoint Inhibitors

Cancer Vaccines

Gene Therapy

Other Therapy Types

By Indication

Blood Cancer

Lung Cancer

Breast Cancer

Colorectum Cancer

Prostate Cancer

Stomach Cancer

Cervical Cancer

Liver and Intrahepatic Bile Duct Cancer

Thyroid Cancer

Other Indications

By End User

Hospital Pharmacies

Retail Pharmacies

Online Stores

Regions and Countries Covered

Africa

Egypt, South Africa, Nigeria, and Algeria

Market leaders and key company profiles

Astellas Pharma Inc

Eli Lilly and Co

Novartis AG

Merck KGaA

Johnson & Johnson

AstraZeneca

Pfizer Inc

Bristol Myers Squibb

F. Hoffmann-La Roche Ltd

AbbVie

Get more information on this report

Africa Cancer Targeted Therapy Market Report Coverage and Deliverables:

The "Africa Cancer Targeted Therapy Market Size and Forecast (2021–2031)" report provides a detailed analysis of the market covering below areas:

Africa Cancer Targeted Therapy market size and forecast at regional and country levels for key segments covered under the scope

Africa Cancer Targeted Therapy market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Africa Cancer Targeted Therapy market analysis covering key trends, regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Africa Cancer Targeted Therapy market

Detailed company profiles, including SWOT analysis

Africa Cancer Targeted Therapy Market Geographic Insights:

The geographical scope of the Africa Cancer Targeted Therapy market report is divided into Egypt, South Africa, Nigeria, and Algeria. South Africa held the largest share in 2024.

Country-level dynamics in Africa’s cancer targeted therapy market reveal substantial variation in adoption, access, and investment intensity. South Africa remains the most mature market, driven by a relatively advanced private healthcare sector, established oncology networks, and greater access to diagnostic services. The country’s market is shaped by sophisticated payer systems and higher per-capita healthcare spending, which supports the use of high-cost targeted agents. In contrast, North African markets such as Egypt and Morocco are witnessing rapid growth due to expanding public oncology centers, increased local manufacturing capabilities, and supportive government initiatives that prioritize cancer care modernization. These countries are also becoming regional hubs for clinical research and trials, enhancing early access to novel targeted therapies.

In East Africa, Kenya and Tanzania are emerging as important growth markets, primarily driven by expanding private hospitals, international partnerships, and improving diagnostic infrastructure. However, access remains uneven, with urban centers accounting for most of the market demand. West African countries, including Nigeria and Ghana, present a mixed picture: large patient populations and rising cancer incidence create significant demand, yet market expansion is constrained by fragmented reimbursement systems and limited diagnostic coverage.

In Central Africa, market growth is slower, largely due to infrastructural limitations and constrained healthcare spending. Across the continent, differences in regulatory frameworks impact time-to-market and product availability. Some countries are increasingly adopting expedited approval pathways for oncology therapies, while others maintain lengthy review processes that delay access. Additionally, variations in pricing policies, import tariffs, and distribution channels influence market competitiveness. Companies targeting Africa must therefore tailor strategies to each country’s healthcare maturity, focusing on localized partnerships, flexible financing models, and scalable diagnostic solutions to drive adoption.

Get more information on this report

Africa Cancer Targeted Therapy Market Research Report Guidance:

The report includes qualitative and quantitative data in the Africa Cancer Targeted Therapy market across therapy type, indication, distribution channel, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Africa Cancer Targeted Therapy market.

Chapter 3 includes the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Africa Cancer Targeted Therapy market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Africa Cancer Targeted Therapy market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 11 cover Africa Cancer Targeted Therapy market segments by therapy type, indication, distribution channel, and geography across Egypt, South Africa, Nigeria, and Algeria. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Cancer Targeted Therapy market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Africa Cancer Targeted Therapy Market News and Key Development:

The Africa Cancer Targeted Therapy market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Africa cancer targeted therapy market are:

In February 2025, Yemaachi Biotechnology partnered with Roche to launch The African Cancer Atlas (TACA), a genomic and clinical database of up to 7,500 African cancer patients aimed at driving precision oncology research and identifying novel biomarkers relevant to targeted therapies across the continent. This initiative addresses the severe underrepresentation of African genomic data in cancer research and will support the development of targeted treatments tailored to African populations.

In November 2024, Biopharmaceutical company CStone Pharmaceuticals entered a strategic commercial collaboration with Pharmalink to license and commercialize its anti-PD-L1 targeted therapy sugemalimab in South Africa and the Middle East and North Africa (MENA) region. The deal expands access to this immuno-oncology agent for metastatic non-small cell lung cancer in significant African markets.

Key Sources Referred:

World Health Organization (WHO)World Heart Federation (WHF)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Africa Cancer Targeted Therapy Market?

The Africa Cancer Targeted Therapy Market is valued at US$ 1,733.4 Million in 2024, it is projected to reach US$ 3,477.6 Million by 2031.

What is the CAGR for Africa Cancer Targeted Therapy Market by (2025 - 2031)?

As per our report Africa Cancer Targeted Therapy Market, the market size is valued at US$ 1,733.4 Million in 2024, projecting it to reach US$ 3,477.6 Million by 2031. This translates to a CAGR of approximately 10.5% during the forecast period.

What segments are covered in this report?

The Africa Cancer Targeted Therapy Market report typically cover these key segments-

Therapy Type (Monoclonal Antibodies, Tyrosine Kinase Inhibitors, Immune Checkpoint Inhibitors, Cancer Vaccines, Gene Therapy, Other Therapy Types)

Indication (Blood Cancer, Lung Cancer, Breast Cancer, Colorectum Cancer, Prostate Cancer, Stomach Cancer, Cervical Cancer, Liver and Intrahepatic Bile Duct Cancer, Thyroid Cancer, Other Indications)

End User (Hospital Pharmacies, Retail Pharmacies, Online Stores)

What is the historic period, base year, and forecast period taken for Africa Cancer Targeted Therapy Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Africa Cancer Targeted Therapy Market report:

Historic Period : 2021-2023

Base Year : 2024

Forecast Period : 2025-2031

Who are the major players in Africa Cancer Targeted Therapy Market?

The Africa Cancer Targeted Therapy Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Astellas Pharma Inc

Eli Lilly and Co

Novartis AG

Merck KGaA

Johnson & Johnson

AstraZeneca

Pfizer Inc

Bristol Myers Squibb

F. Hoffmann-La Roche Ltd

AbbVie

Who should buy this report?

The Africa Cancer Targeted Therapy Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Africa Cancer Targeted Therapy Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Africa Cancer Targeted Therapy Market

Get Free Sample For Africa Cancer Targeted Therapy Market