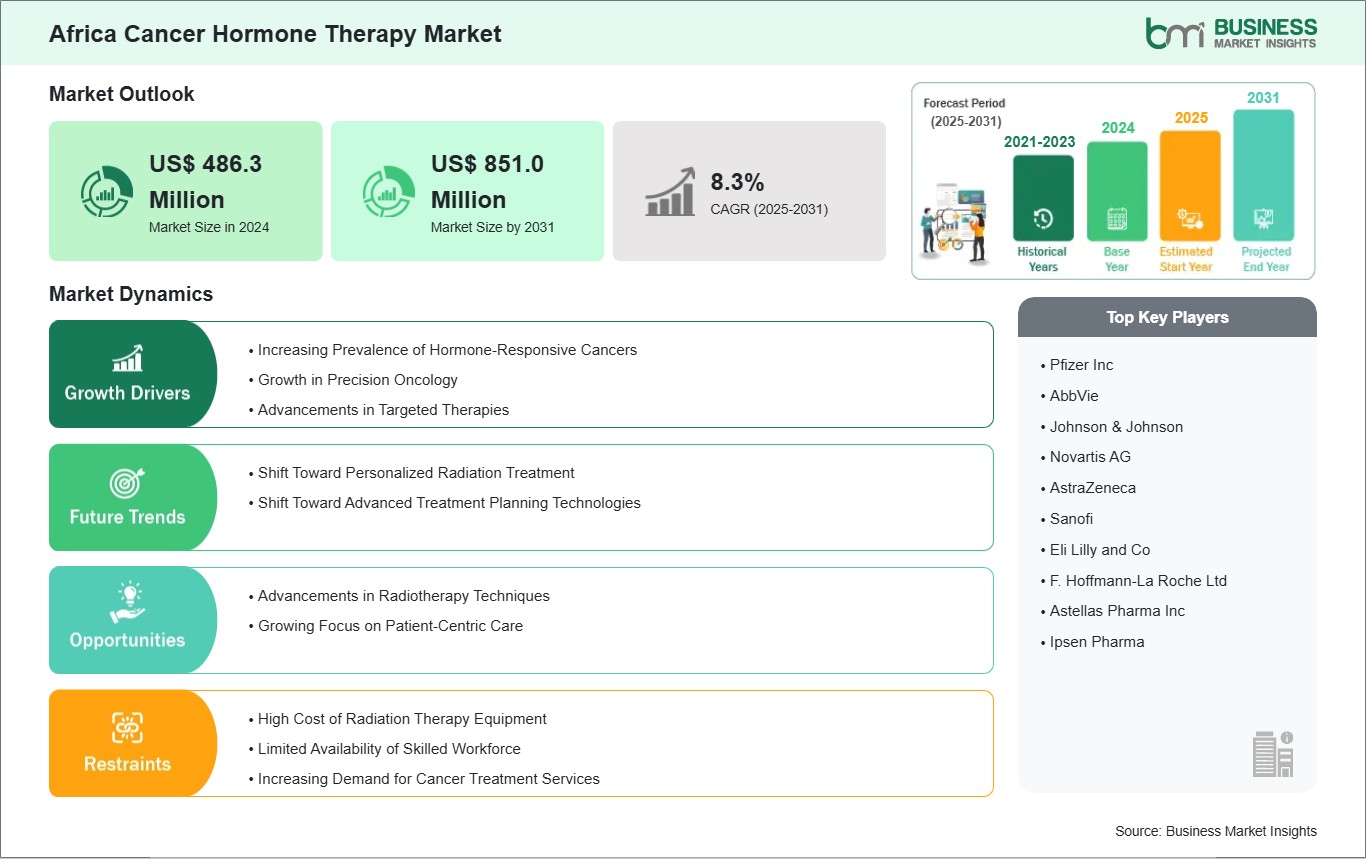

The Africa cancer hormone therapy market size is expected to reach US$ 851.0 million by 2031 from US$ 486.3 million in 2024. The market is estimated to record a CAGR of 8.3% from 2025 to 2031.

Executive Summary and Africa Cancer Hormone Therapy Market Analysis:

Hormone therapy plays an important role in the management of hormone-sensitive cancers such as prostate and certain breast cancers, which are diagnosed across the region due to lifestyle transitions, aging populations, and better detection in urban centers. The market is driven by the expanding availability of systemic cancer treatments in tertiary hospitals, rising physician familiarity with endocrine-based therapies, and a shift toward less invasive treatment options compared with conventional chemotherapy. Urbanization and the expansion of private healthcare providers have supported the adoption of hormone therapy in select African countries. However, market growth remains constrained by limited access to specialized oncology services in many parts of the continent, delayed diagnosis, and disparities between urban and rural healthcare delivery. Supply chain challenges and affordability issues restrict widespread adoption, making hormone therapy largely concentrated in more developed healthcare markets within Africa rather than evenly distributed across the region.

Africa Cancer Hormone Therapy Market - Strategic Insights:

Get more information on this report

Africa Cancer Hormone Therapy Market Segmentation Analysis:

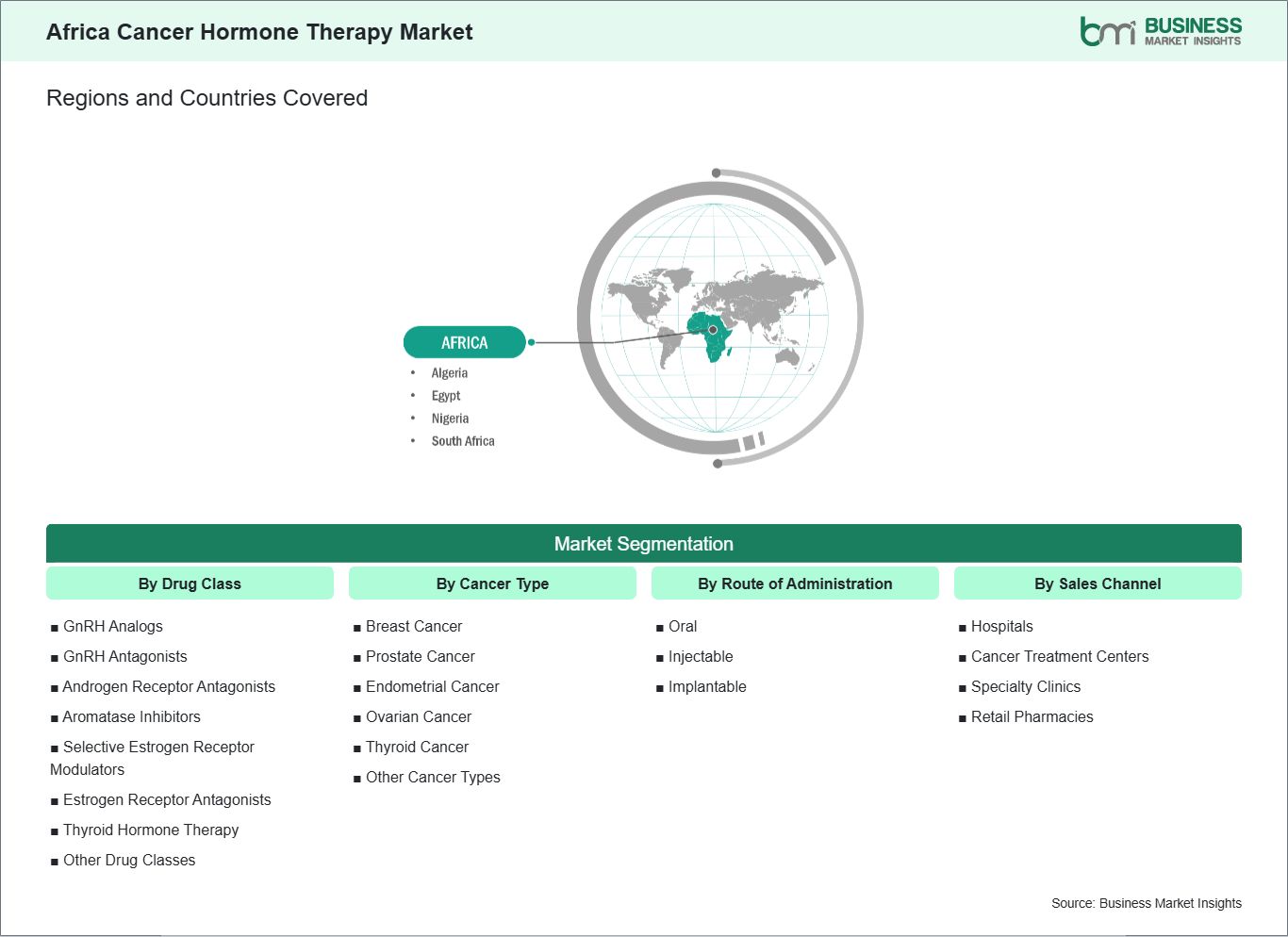

Key segments that contributed to the derivation of the Africa cancer hormone therapy market analysis are drug class, cancer type, route of administration, and sales channel.

By drug class, the cancer hormone therapy market is segmented into GnRH analogs, GnRH antagonists, androgen receptor antagonists, aromatase inhibitors, selective estrogen receptor modulators, estrogen receptor antagonists, thyroid hormone therapy, and others. The GnRH analogs segment dominated the market in 2024.

By cancer type, the cancer hormone therapy market is segmented into breast cancer, prostate cancer, endometrial cancer, ovarian cancer, thyroid cancer, and others. The breast cancer segment dominated the market in 2024.

By route of administration, the cancer hormone therapy is segmented into oral, injectable, and implantable. The oral segment dominated the market in 2024.

By sales channel, the cancer hormone therapy market is segmented into hospitals, cancer treatment centers, specialty clinics, and retail pharmacies. The hospitals segment dominated the market in 2024.

Africa Cancer Hormone Therapy Market Drivers and Opportunities:

Increasing Prevalence of Hormone-Responsive Cancers

Across Africa, the prevalence of hormone-responsive cancers is rising as demographic shifts, urbanization, and lifestyle changes intersect with improving diagnostic awareness. Breast cancer is now the most commonly diagnosed cancer among women in many countries, including South Africa, Nigeria, Kenya, and Morocco, with a significant proportion being hormone receptor–positive. Prostate cancer incidence is increasing across Sub-Saharan Africa, particularly in Southern and West Africa, driven by population aging and greater use of PSA testing in urban centers. Although overall incidence rates remain lower than in Western regions, late presentation and growing survivor populations are expanding the need for sustained hormone therapy.

Epidemiologic transitions are amplifying risk factors relevant to endocrine-driven malignancies. Rising obesity rates, reduced physical activity, and dietary changes are linked to estrogen-mediated breast cancer risk in urban populations, while longer life expectancy increases cumulative prostate cancer burden. In North Africa, countries such as Egypt and Tunisia report growing breast cancer prevalence with improving pathology services enabling hormone receptor testing. As more tumors are accurately classified, eligibility for endocrine therapy is increasing, expanding the addressable patient base for hormone treatments.

Health system constraints shape how hormone therapy demand materializes. In African settings, limited radiotherapy and chemotherapy capacity elevate the importance of oral hormone therapies as accessible, relatively affordable treatment options. Public sector oncology services in South Africa and selected North African countries use tamoxifen, aromatase inhibitors, and androgen-deprivation therapies as backbone treatments. As national cancer control plans prioritize essential medicines lists and early detection, hormone therapy continues to become a cornerstone of cancer management across diverse resource settings.

Rising Adoption of Combination Regimens

Combination regimens involving hormone therapy are emerging gradually across Africa, with adoption strongly correlated to health system capacity and reimbursement structures. In middle-income markets such as South Africa, Egypt, and Algeria, endocrine therapies are combined with targeted agents for hormone receptor–positive breast cancer, particularly in private-sector and academic hospitals. While access to CDK4/6 inhibitors and newer androgen receptor inhibitors remains uneven, their inclusion in treatment guidelines signals a shift toward more comprehensive regimens where feasible.

In prostate cancer, androgen-deprivation therapy remains the foundation of care, with limited but growing use of combination approaches in metastatic disease. South Africa leads the region in incorporating next-generation hormonal agents alongside ADT, while pilot programs and donor-supported initiatives in East and West Africa are expanding access to improved systemic therapies. Even where advanced agents are unavailable, sequential use of different hormone therapies reflects an incremental move toward more sophisticated treatment strategies.

Policy reforms and international partnerships are key enablers of combination therapy uptake. WHO essential medicines guidance, pooled procurement mechanisms, and NGO-supported access programs are improving the availability of traditional and newer endocrine agents. Training collaborations and regional oncology networks are also strengthening clinician familiarity with combination protocols. As infrastructure, reimbursement, and diagnostic capacity improve, Africa’s market is expected to evolve from monotherapy-dominant use toward broader adoption of combination regimens, anchored by hormone therapy as the treatment backbone.

Africa Cancer Hormone Therapy Market Size and Share Analysis:

The Africa cancer hormone therapy market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report further examines subsegments categorized within drug class, cancer type, route of administration, and sales channel, highlighting their respective contributions to overall market performance.

By drug class, the GnRH analogs subsegment dominated the market in 2024. Their proven efficacy in hormone-dependent cancers, widespread clinical adoption, established safety profile, and ability to effectively suppress gonadotropin release make them a cornerstone of endocrine-based cancer therapies.

Per cancer type, the breast cancer subsegment dominated the market in 2024, driven by the high global prevalence of breast cancer, increasing awareness and screening programs, strong reliance on hormone-based treatments, and continuous advancements in targeted and combination therapies.

By route of administration, the oral subsegment dominated the market in 2024. Oral therapies are preferred due to their ease of administration, improved patient compliance, convenience for long-term treatment, reduced need for hospital visits, and growing availability of effective oral oncology drugs.

Per sales channel, the hospitals subsegment dominated the market in 2024. Hospitals remain the primary distribution channel as they offer comprehensive cancer care, access to specialized oncology pharmacists, advanced treatment infrastructure, and integrated diagnostic and therapeutic services, ensuring efficient delivery of cancer medications.

Africa Cancer Hormone Therapy Market Report Highlights:

Report Attribute

Details

Market size in 2024

US$ 486.3 Million

Market Size by 2031

US$ 851.0 Million

CAGR (2025 - 2031)

8.3%

Historical Data

2021-2023

Forecast period

2025-2031

Segments Covered

By Drug Class

GnRH Analogs

GnRH Antagonists

Androgen Receptor Antagonists

Aromatase Inhibitors

Selective Estrogen Receptor Modulators

Estrogen Receptor Antagonists

Thyroid Hormone Therapy

Other Drug Classes

By Cancer Type

Breast Cancer

Prostate Cancer

Endometrial Cancer

Ovarian Cancer

Thyroid Cancer

Other Cancer Types

By Route of Administration

Oral

Injectable

Implantable

By Sales Channel

Hospitals

Cancer Treatment Centers

Specialty Clinics

Retail Pharmacies

Regions and Countries Covered

Africa

Egypt, South Africa, Nigeria, Algeria

Market leaders and key company profiles

Pfizer Inc

AbbVie

Johnson & Johnson

Novartis AG

AstraZeneca

Sanofi

Eli Lilly and Co

F. Hoffmann-La Roche Ltd

Astellas Pharma Inc

Ipsen Pharma

Get more information on this report

Africa Cancer Hormone Therapy Market Report Coverage and Deliverables:

The "Africa Cancer Hormone Therapy Market Size and Forecast (2021–2031)" report provides a detailed analysis of the market covering below areas:

Africa Cancer Hormone Therapy market size and forecast at regional and country levels for all the key market segments covered under the scope

Africa Cancer Hormone Therapy market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Africa Cancer Hormone Therapy market analysis covering key market trends, regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Africa Cancer Hormone Therapy market

Detailed company profiles, including SWOT analysis

Africa Cancer Hormone Therapy Market Geographic Insights:

The geographical scope of the Africa Cancer Hormone Therapy market report is divided into: Nigeria, Egypt, South Africa, and Algeria. South Africa held the largest share in 2024.

South Africa dominates the market due to its advanced healthcare system and established oncology treatment framework. The country has a stronger concentration of specialized cancer care facilities, including academic hospitals and private oncology centers that routinely incorporate hormone therapy into treatment protocols for prostate and breast cancer. Clinical practice reflects greater awareness of hormone-responsive cancers, with endocrinological approaches used as first-line or long-term management strategies. The presence of trained oncologists, access to diagnostic services, and a structured referral system support the consistent use of hormone therapies across public and private healthcare sectors. Private healthcare providers offer broader access to newer therapeutic options and long-term disease management. Despite its leadership position, disparities remain within the country, as patients in rural or under-resourced areas face challenges in accessing timely diagnosis and sustained hormone therapy. South Africa continues to set clinical standards for hormone-based cancer treatment in Africa, influencing treatment practices across neighboring countries.

Get more information on this report

Africa Cancer Hormone Therapy Market Research Report Guidance:

The report includes qualitative and quantitative data in the Africa cancer hormone therapy market across drug class, cancer type, route of administration, sales channel, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Africa Cancer Hormone Therapy market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Africa Cancer Hormone Therapy market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Africa Cancer Hormone Therapy market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 11 cover the African Cancer Hormone Therapy market segments by drug class, cancer type, route of administration, sales channel, and geography across Nigeria, Egypt, South Africa, and Algeria. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Africa Cancer Hormone Therapy market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Africa Cancer Hormone Therapy Market News and Key Development:

The Africa Cancer Hormone Therapy market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Africa cancer hormone therapy market are:

In January 2026, The Pfizer Foundation announced that it would expand its Action & Impact: A Cancer Care Initiative with a new three‑year, US$ 10 million investment to improve access to timely breast cancer diagnosis, treatment, and care in Kenya and Ethiopia, supporting community‑ and country‑led efforts through partnerships with AMPATH and Innovations in Healthcare with CHAI — building on prior work in Rwanda, Ghana, and Tanzania to address critical gaps in oncology care across sub‑Saharan Africa.

In January 2025, the Pfizer Foundation announced that it would progress a three‑year US$ 15 million initiative to improve breast cancer care in Rwanda, Ghana, and Tanzania by providing grant funding to Jhpiego and Partners In Health to scale community‑ and country‑led efforts addressing barriers to diagnosis and treatment of breast cancer across sub‑Saharan Africa.

Key Sources Referred:

The World BankWorld Health Organization (WHO)Center for Disease Control and Prevention (CDC)American Association for Cancer Research (AACR)National Cancer Institute (NCI)American Society of Clinical Oncology (ASCO)European Society for Medical Oncology (ESMO)Company WebsitesCompany Annual ReportsCompany Investor Presentations

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Africa Cancer Hormone Therapy Market?

The Africa Cancer Hormone Therapy Market is valued at US$ 486.3 Million in 2024, it is projected to reach US$ 851.0 Million by 2031.

What is the CAGR for Africa Cancer Hormone Therapy Market by (2025 - 2031)?

As per our report Africa Cancer Hormone Therapy Market, the market size is valued at US$ 486.3 Million in 2024, projecting it to reach US$ 851.0 Million by 2031. This translates to a CAGR of approximately 8.3% during the forecast period.

What segments are covered in this report?

The Africa Cancer Hormone Therapy Market report typically cover these key segments-

Drug Class (GnRH Analogs, GnRH Antagonists, Androgen Receptor Antagonists, Aromatase Inhibitors, Selective Estrogen Receptor Modulators, Estrogen Receptor Antagonists, Thyroid Hormone Therapy, Other Drug Classes)

Cancer Type (Breast Cancer, Prostate Cancer, Endometrial Cancer, Ovarian Cancer, Thyroid Cancer, Other Cancer Types)

Route of Administration (Oral, Injectable, Implantable)

Sales Channel (Hospitals, Cancer Treatment Centers, Specialty Clinics, Retail Pharmacies)

What is the historic period, base year, and forecast period taken for Africa Cancer Hormone Therapy Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Africa Cancer Hormone Therapy Market report:

Historic Period : 2021-2023

Base Year : 2024

Forecast Period : 2025-2031

Who are the major players in Africa Cancer Hormone Therapy Market?

The Africa Cancer Hormone Therapy Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Pfizer Inc

AbbVie

Johnson & Johnson

Novartis AG

AstraZeneca

Sanofi

Eli Lilly and Co

F. Hoffmann-La Roche Ltd

Astellas Pharma Inc

Ipsen Pharma

Who should buy this report?

The Africa Cancer Hormone Therapy Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Africa Cancer Hormone Therapy Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Africa Cancer Hormone Therapy Market

Get Free Sample For Africa Cancer Hormone Therapy Market