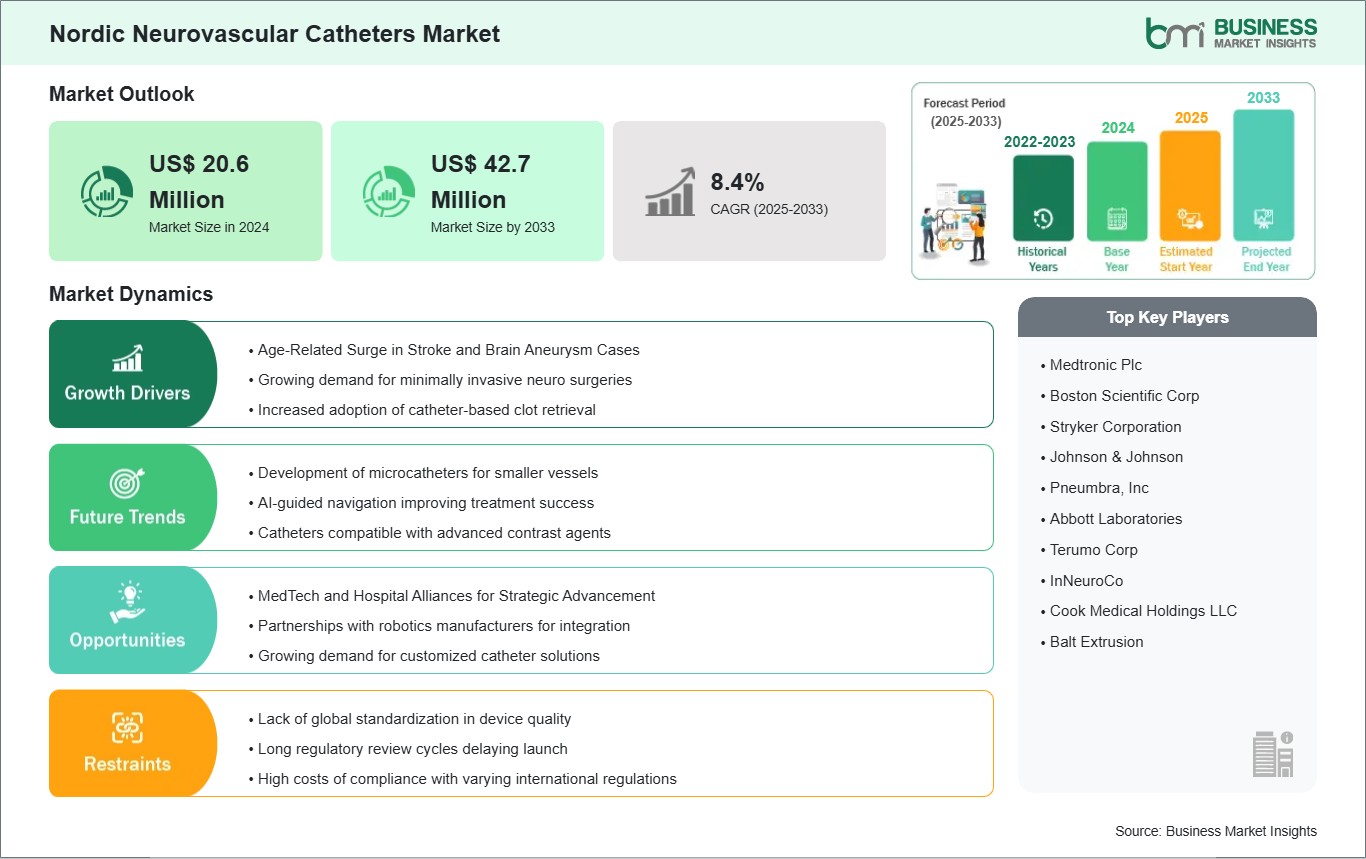

The Nordic Neurovascular Catheters market size is expected to reach US$ 42.7 million by 2033 from US$ 20.6 million in 2024. The market is estimated to record a CAGR of 8.4% from 2025 to 2033.

Executive Summary and Nordic Neurovascular Catheters Market Analysis:

Sweden, Norway, Denmark, and Finland exhibit strong healthcare infrastructure, extensive diagnostic imaging coverage, and established referral networks for acute stroke care, which facilitate rapid adoption of neurovascular technologies.

Stroke is a leading cause of morbidity and mortality across the Nordics, and mechanical thrombectomy has become a standard of care for eligible patients with large vessel occlusions. This procedural increase drives demand for thrombectomy and aspiration catheters capable of navigating complex cerebral vasculature. Early detection of cerebral aneurysms through advanced imaging has increased the volume of coil embolization and flow diversion procedures, elevating demand for specialized microcatheters.

Hospitals and dedicated neuro interventional centers represent the largest end user segment, bolstered by state‑of‑the‑art angiography suites in major university hospitals (e.g., Karolinska, Rigshospitalet, Oslo University Hospital, Helsinki University Hospital). Coated catheters are gaining traction due to infection control priorities. Multi‑lumen designs support simultaneous therapies in emergency and intensive care settings. Competitive dynamics in the region include global MedTech leaders (such as Terumo, Medtronic, Stryker, and Penumbra) collaborating with distributors and clinical networks to expand procedural training and device access. The market reflects a mature healthcare environment with increasing procedural volumes, strong reimbursement support, and growing clinician familiarity with advanced neurovascular catheter systems — positioning the region for stable growth.

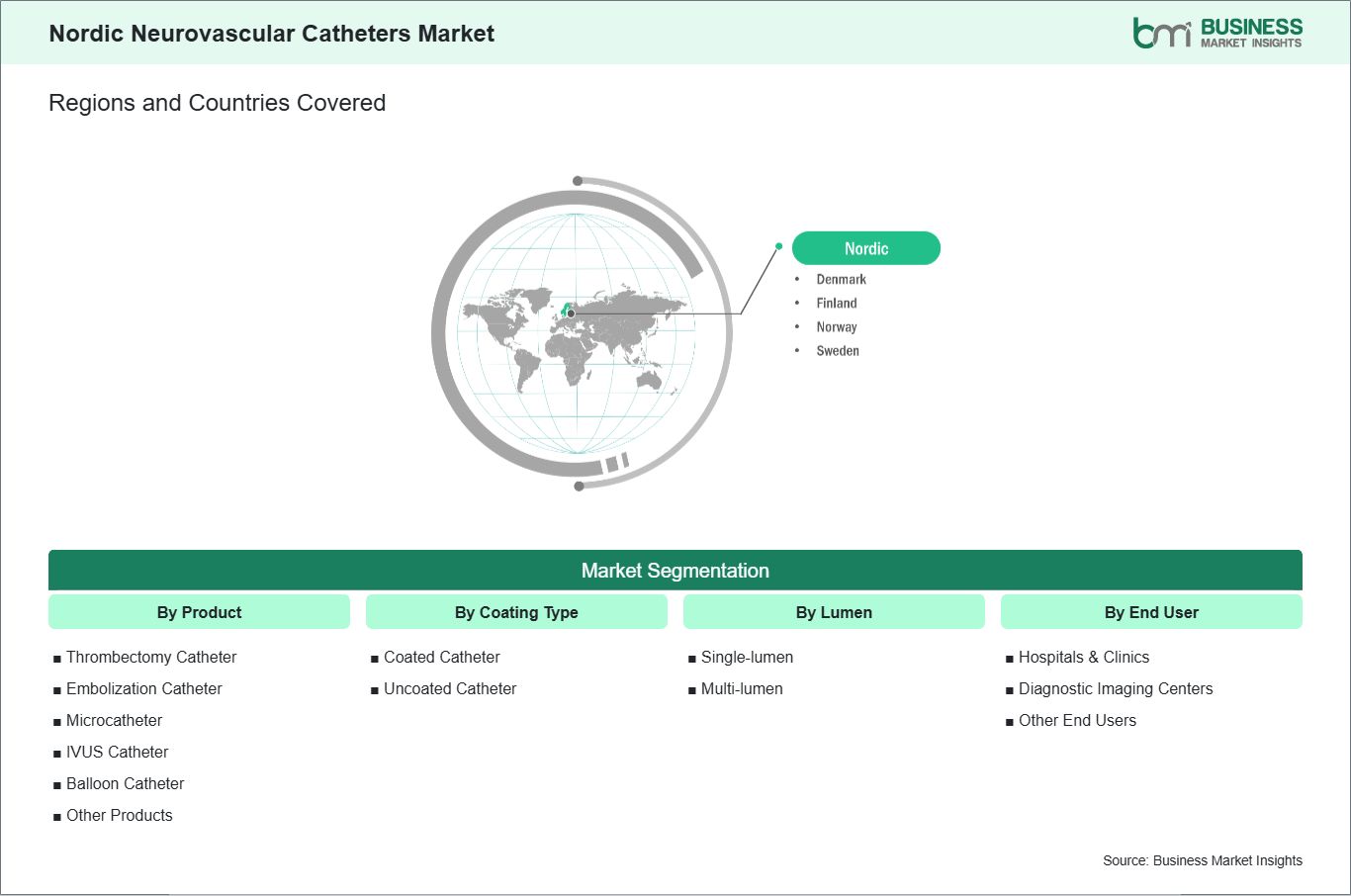

Key segments that contributed to the derivation of the Nordic Neurovascular Catheters market analysis are product, coating type, lumen, and end user.

By product, the neurovascular catheters market is segmented into thrombectomy catheter, embolization catheter, microcatheter, IVUS catheter, balloon catheter, and others. The thrombectomy catheter segment dominated the market in 2024.

Per coating type, the neurovascular catheters market is bifurcated into coated catheters, uncoated catheters. The coated catheters segment dominated the market in 2024.

Based on lumen, the market is divided into single-lumen and multi-lumen. The multi-lumen segment dominated the market in 2024.

By end user, the market is segmented into hospitals and clinics, diagnostic imaging Centers, and others. The hospitals and clinics segment dominated the market in 2024.

Nordic Neurovascular Catheters Market Drivers and Opportunities:

Age-Related Surge in Stroke and Brain Aneurysm Cases

Stroke remains one of the leading causes of death and long‑term disability in Europe, with ischemic strokes accounting for the majority of cases. Neurovascular catheter‑based mechanical thrombectomy has gained clinical acceptance as a standard of care for large vessel occlusion strokes, enabling rapid recanalization and improved functional outcomes. High levels of diagnostic imaging accessibility mean more patients are identified early and referred for thrombectomy, boosting utilization of aspiration and delivery catheters.

Cerebral aneurysms are detected through routine use of CT angiography (CTA) and magnetic resonance angiography (MRA) in tertiary hospitals. Endovascular aneurysm treatments such as coil embolization and flow diversion rely on microcatheters and embolization catheter systems for precise device delivery. These procedures are performed in comprehensive stroke and neurovascular centers located in capital cities, where neurointerventional expertise and hybrid angiography suites are available. The aging demographics in the region — combined with high rates of vascular risk factors such as hypertension and atrial fibrillation — contribute to growing procedural volumes. The increasing burden of neurovascular diseases, enhanced imaging capabilities, and broader procedural eligibility criteria are driving sustained demand for neurovascular catheters in healthcare systems, supporting market growth.

MedTech and Hospital Alliances for Strategic Advancement

Nordic hospital systems and academic centers are increasingly partnering with global medical device manufacturers to gain access to advanced catheter technologies, clinical education, and procedural support tailored to regional clinical workflows. These collaborations help accelerate the adoption of novel devices while enhancing procedural outcomes.

Long‑term supply agreements and clinical research partnerships enable MedTech firms to engage with interventional neurologists and radiologists to better understand procedural challenges unique to Nordic patient populations. Insights from these collaborations support the refinement of device design — for example, improving catheter trackability, flexibility, and precision in navigating tortuous cerebral anatomy — increasing clinical adoption. Hospitals benefit from early access to next‑generation technologies, structured training programs, and on‑site support during complex procedures.

Joint clinical studies conducted with academic hospitals generate real‑world evidence that can support regulatory submissions and inclusion in clinical guidelines. Hospitals participating in such trials become reference centers, promoting wider acceptance of advanced neurovascular catheter systems within regional healthcare networks. Additionally, educational collaborations and simulation training enhance physician proficiency in catheter‑based stroke and aneurysm interventions, increasing procedural volumes.

From a commercial perspective, partnerships with national hospital networks and stroke care initiatives provide MedTech firms with market penetration and stable revenue streams. In a region emphasizing quality of care and minimally invasive interventions, strategic collaborations between device manufacturers and hospitals will remain pivotal in expanding access to neurovascular catheter technologies and sustaining long-term market growth.

Nordic Neurovascular Catheters Market Size and Share Analysis:

The Nordic neurovascular catheters market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report further examines subsegments categorized within product, coating type, lumen, and end user, offering insights into their contribution to overall market performance.

By product, the thrombectomy catheter subsegment dominated the market in 2024, driven by the widespread use in routine IV therapy and emergency care across hospitals and clinics.

Based on coating type, the coated catheters subsegment dominated the market in 2024, driven by infection prevention initiatives and demand for biocompatible devices in Nordic healthcare systems.

Per lumen, multi-lumen subsegment dominated the market in 2024, driven by the efficiency needs in administering multiple therapies simultaneously in critical care settings.

By end user, hospitals and clinics subsegment dominated the market in 2024, driven by government investment in healthcare infrastructure and expansion of private medical facilities across the Nordic.

Nordic Neurovascular Catheters Market Report Coverage and Deliverables:

The "Nordic Neurovascular Catheters Market Size and Forecast (2025–2033)" report provides a detailed analysis of the market covering below areas:

Nordic Neurovascular Catheters market size and forecast at regional and country levels for all the key market segments covered under the scope

Nordic Neurovascular Catheters market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Nordic Neurovascular Catheters market analysis covering key market trends, regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Nordic Neurovascular Catheters market

Detailed company profiles, including SWOT analysis

The geographical scope of the Nordic Neurovascular Catheters market report is divided into: Sweden, Denmark, Norway, and Finland. Sweden held the largest share in 2024.

The Nordic neurovascular catheters market comprises Sweden, Norway, Denmark, Finland, and Iceland. Sweden is the largest market in the region, benefiting from strong healthcare investment, a high density of certified stroke centers, and widespread adoption of advanced interventional workflows in major hospitals such as Karolinska University Hospital. Norway demonstrates growth through comprehensive stroke care programs, with Medtronic, Stryker, and other device players represented in major tertiary centers.

Denmark continues to expand neurovascular capabilities, especially in Copenhagen and Aarhus, where high procedural volumes for mechanical thrombectomy and coil embolization support catheter adoption. Finland emphasizes integrated stroke networks and advanced imaging access, particularly in Helsinki and Tampere, where neurovascular procedures are performed. Iceland is a smaller market but shows rising procedural adoption in its main tertiary hospital, with catheter workflows embedded into acute care pathways.

Hospitals and specialized neuro interventional centers dominate device adoption due to centralized procedural capabilities, strong reimbursement support, and clinician expertise. Regional collaborations with global MedTech firms help facilitate training, evidence generation, and structured product rollouts, fostering market growth across healthcare systems.

Get more information on this report

Nordic Neurovascular Catheters Market Research Report Guidance:

The report includes qualitative and quantitative data in the Nordic Neurovascular Catheters market across product, coating type, lumen, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Nordic Neurovascular Catheters market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Nordic Neurovascular Catheters market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Nordic Neurovascular Catheters market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover the Nordic Neurovascular Catheters market segments by product, coating type, lumen, end user, and geography across Sweden, Denmark, Norway, and Finland. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Nordic Neurovascular Catheters market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Nordic Neurovascular Catheters Market News and Key Development:

The Nordic Neurovascular Catheters market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Nordic neurovascular catheters market are:

In January 2026, Boston Scientific Corporation revealed a definitive deal to acquire Penumbra, Inc. for approximately US$ 14.5 billion, expanding its neurovascular portfolio — including thrombectomy and aspiration catheters — that are used extensively in Nordic hospitals for stroke and neurovascular procedures.

In June 2024, Penumbra, Inc. announced the commercial launch of its BMX81 and BMX96 neurovascular access catheter systems in Europe, enhancing neurovascular procedural options for stroke care and aneurysm management. These devices, compatible with a range of access techniques, support catheter‑based interventions offered in Nordic hospitals and comprehensive stroke centers.

Key Sources Referred:

World Health Organization (WHO)World Heart Federation (WHF)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Nordic Neurovascular Catheters Market?

The Nordic Neurovascular Catheters Market is valued at US$ 20.6 Million in 2024, it is projected to reach US$ 42.7 Million by 2033.

What is the CAGR for Nordic Neurovascular Catheters Market by (2025 - 2033)?

As per our report Nordic Neurovascular Catheters Market, the market size is valued at US$ 20.6 Million in 2024, projecting it to reach US$ 42.7 Million by 2033. This translates to a CAGR of approximately 8.4% during the forecast period.

What segments are covered in this report?

The Nordic Neurovascular Catheters Market report typically cover these key segments-

End User (Hospitals & Clinics, Diagnostic Imaging Centers, Other End Users)

What is the historic period, base year, and forecast period taken for Nordic Neurovascular Catheters Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Nordic Neurovascular Catheters Market report:

Historic Period : 2022-2023

Base Year : 2024

Forecast Period : 2025-2033

Who are the major players in Nordic Neurovascular Catheters Market?

The Nordic Neurovascular Catheters Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic Plc

Boston Scientific Corp

Stryker Corporation

Johnson & Johnson

Pneumbra, Inc

Abbott Laboratories

Terumo Corp

InNeuroCo

Cook Medical Holdings LLC

Balt Extrusion

Who should buy this report?

The Nordic Neurovascular Catheters Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Nordic Neurovascular Catheters Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Nordic Neurovascular Catheters Market

Get Free Sample For Nordic Neurovascular Catheters Market