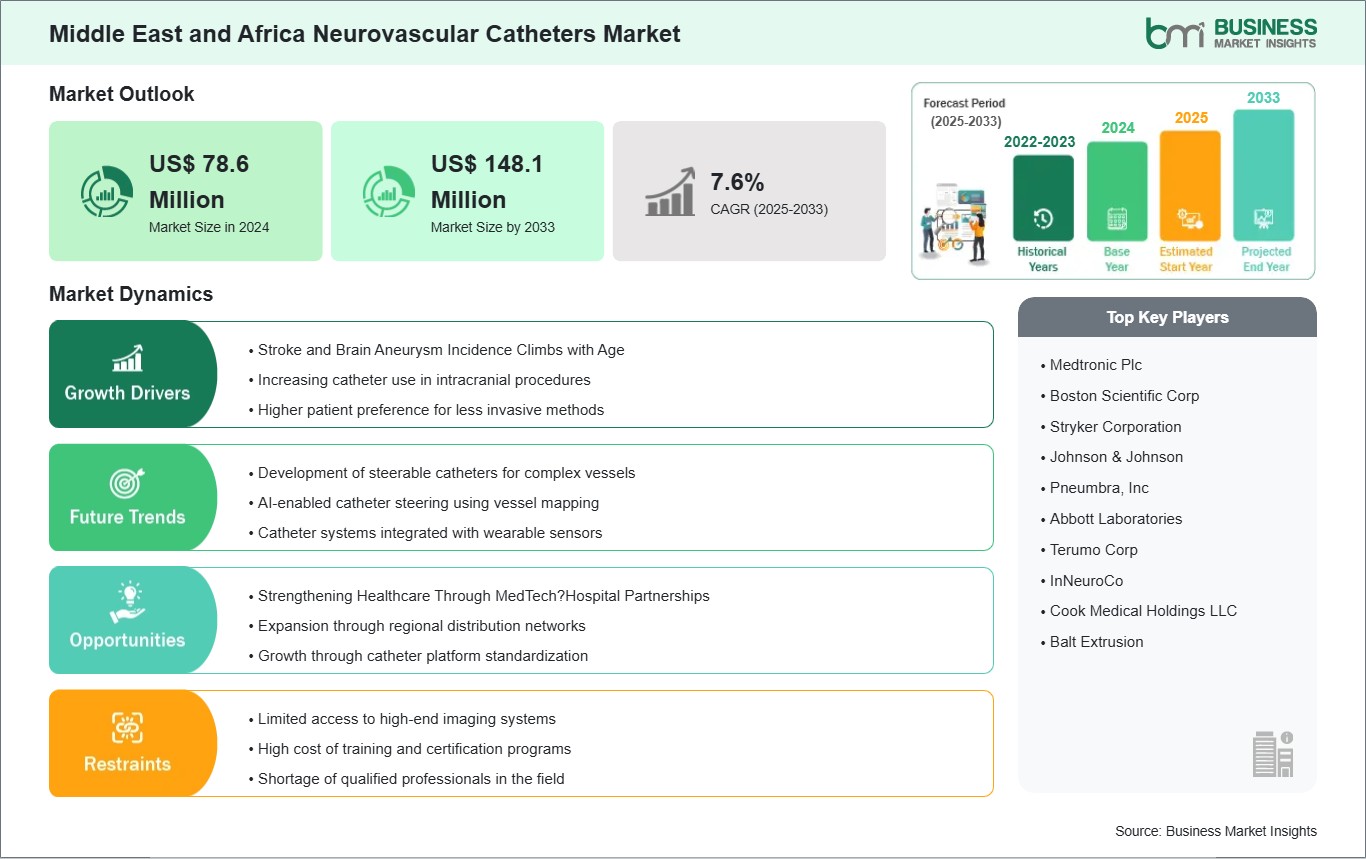

The Middle East and Africa Neurovascular Catheters market size is expected to reach US$ 148.1 million by 2033 from US$ 78.6 million in 2024. The market is estimated to record a CAGR of 7.6% from 2025 to 2033.

Executive Summary and Middle East and Africa Neurovascular Catheters Market Analysis:

Saudi Arabia, UAE, and South Africa lead regional growth due to well-developed hospital infrastructure, government initiatives to improve stroke care, and investment in neuro-interventional suites. In North Africa, countries such as Egypt and Morocco are witnessing growing procedural volumes as urban hospitals upgrade imaging capabilities and stroke management protocols. Stroke is a leading cause of death in the region, and the prevalence of ischemic stroke has been rising due to aging populations and increasing prevalence of hypertension, diabetes, and obesity. Catheter-based interventions, such as mechanical thrombectomy for large vessel occlusions and endovascular coil embolization for cerebral aneurysms, are becoming standard care in tertiary hospitals, fueling demand for thrombectomy and microcatheter systems.

Advancements in hospital infrastructure, including hybrid angiography labs and modern intensive care units, have supported the adoption of coated and multi-lumen catheters, particularly in critical care settings. Government healthcare programs and public-private partnerships in GCC countries have facilitated procurement and clinician training, accelerating catheter adoption. Across MEA, hospitals and clinics dominate as end users, but diagnostic imaging centers and specialized stroke units are gradually integrating interventional catheter procedures.

Collaborations between MedTech companies and hospitals, along with regional clinical trials, have bolstered market growth by improving access to advanced devices, building physician expertise, and supporting real-world evidence generation.

Middle East and Africa Neurovascular Catheters Market - Strategic Insights:

Get more information on this report

Middle East and Africa Neurovascular Catheters Market Segmentation Analysis:

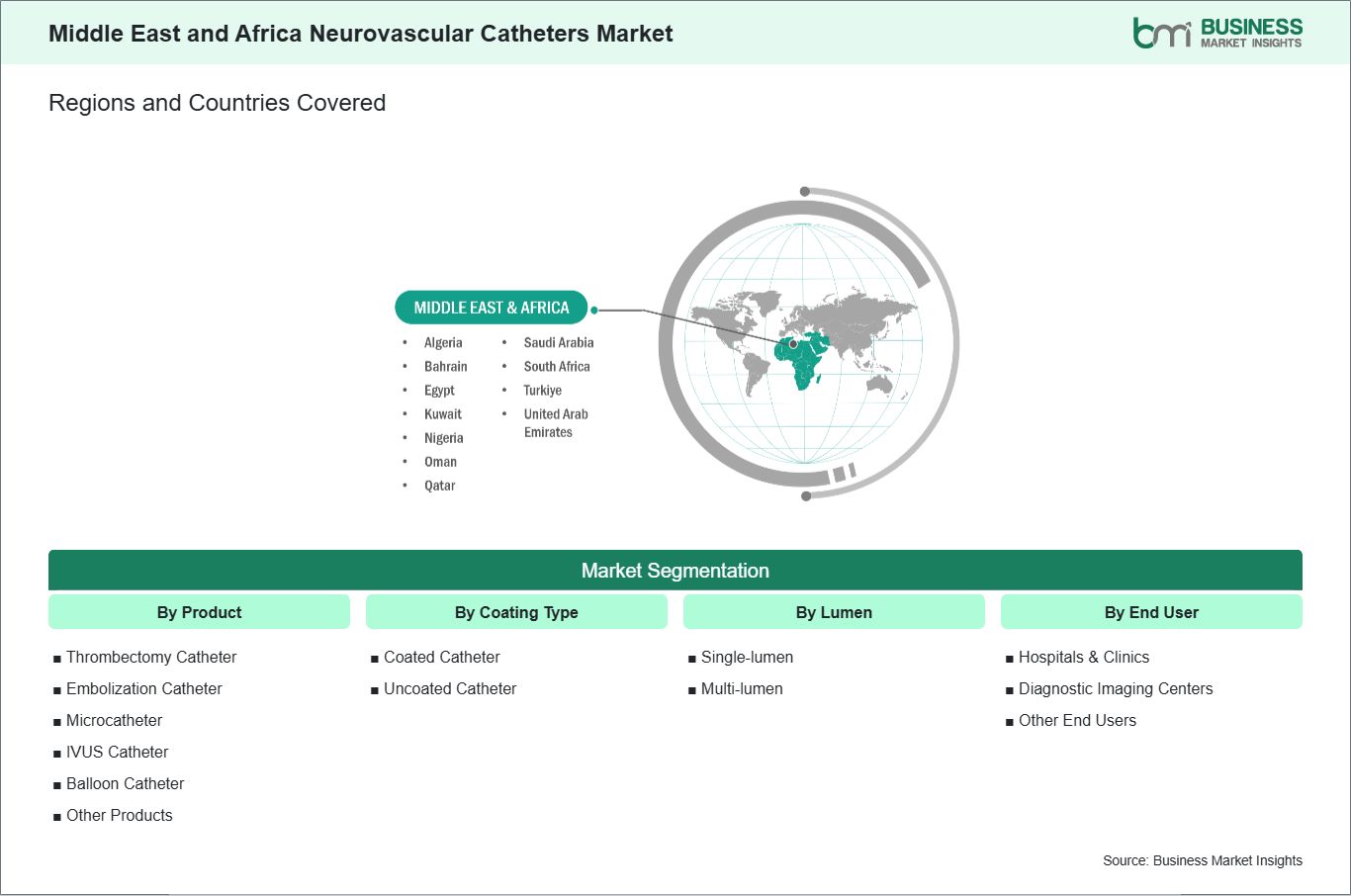

Key segments that contributed to the derivation of the Middle East and Africa Neurovascular Catheters market analysis are product, coating type, lumen, and end user.

By product, the neurovascular catheters market is segmented into thrombectomy catheter, embolization catheter, microcatheter, IVUS catheter, balloon catheter, and others. The thrombectomy catheter segment dominated the market in 2024.

Per coating type, the neurovascular catheters market is bifurcated into coated catheters and uncoated catheters. The coated catheters segment dominated the market in 2024.

Based on lumen, the market is divided into single-lumen and multi-lumen. The multi-lumen segment dominated the market in 2024.

By end user, the market is segmented into hospitals and clinics, diagnostic imaging Centers, and others. The hospitals and clinics segment dominated the market in 2024.

Middle East and Africa Neurovascular Catheters Market Drivers and Opportunities:

Stroke and Brain Aneurysm Incidence Climbs with Age

Stroke remains a leading cause of mortality and long-term disability across the region, with ischemic strokes accounting for the majority of cases. Mechanical thrombectomy is used as a primary treatment for large vessel occlusions, elevating demand for thrombectomy catheters capable of navigating complex cerebral vasculature and restoring perfusion.

Cerebral aneurysms are diagnosed due to improved access to CT angiography and MRI in urban tertiary hospitals, leading to higher volumes of coil embolization and flow diversion procedures. Microcatheters and embolization catheters are essential for precise device delivery and successful endovascular interventions. Coated catheters are gaining popularity in tertiary care settings where infection control is a priority. Multi-lumen catheters are being adopted in ICUs to facilitate simultaneous administration of fluids, medications, and contrast agents.

Public awareness campaigns and increasing healthcare spending in GCC countries and parts of North Africa have contributed to early detection and intervention, expanding the patient base for neurovascular catheter procedures. Rising procedural volumes, combined with technological advancement and infrastructure investment, are driving sustained demand for neurovascular catheters across the region.

Strengthening Healthcare Through MedTech–Hospital Partnerships

Hospitals rely on collaborations to access advanced catheter technologies, procedural training, and device support, particularly in regions where neuro-interventional expertise is developing.

MedTech firms benefit by gaining insights into regional clinical needs, procedural workflows, and local healthcare requirements, enabling the development of catheters optimized for anatomical and procedural challenges prevalent in patients. Co-development initiatives, long-term supply agreements, and structured physician training programs accelerate product adoption and build procedural confidence. Hospitals gain early access to next-generation devices, hands-on training, and technical support, enhancing patient outcomes and procedural efficiency. Clinical collaborations and research initiatives reinforce adoption by generating real-world evidence that supports guideline inclusion, reimbursement approval, and market acceptance. Hospitals participating in trials become reference centers, promoting the wider adoption of neurovascular catheter systems in neighboring countries.

Commercially, partnerships with prominent hospital networks, stroke centers, and healthcare authorities provide MedTech firms with reliable revenue streams and expanded market reach. These collaborations are impactful in countries such as Saudi Arabia, the UAE, and Egypt, where hospital modernization and stroke center expansion are high priorities. As healthcare systems emphasize minimally invasive, value-based care, strategic collaborations remain central to increasing access to neurovascular catheters and sustaining market growth.

Middle East and Africa Neurovascular Catheters Market Size and Share Analysis:

The Middle East and Africa neurovascular catheters market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report further examines subsegments categorized within product, coating type, lumen, and end user, offering insights into their contribution to overall market performance.

By product, the thrombectomy catheter subsegment dominated the market in 2024, driven by mechanical thrombectomy adoption for acute stroke cases.

Per coating type, the coated catheters subsegment dominated the market in 2024, driven by an infection prevention focus on modern hospitals.

Based on lumen, the multi-lumen subsegment dominated the market in 2024, driven by the rising demand for simultaneous therapy administration in the ICU and stroke interventions.

By end user, hospitals and clinics subsegment dominated the market in 2024, driven by strong investment in neuro-interventional facilities and procedural capacity.

Middle East and Africa Neurovascular Catheters Market Report Highlights:

Report Attribute

Details

Market size in 2024

US$ 78.6 Million

Market Size by 2033

US$ 148.1 Million

CAGR (2025 - 2033)

7.6%

Historical Data

2022-2023

Forecast period

2025-2033

Segments Covered

By Product

Thrombectomy Catheter

Embolization Catheter

Microcatheter

IVUS Catheter

Balloon Catheter

Other Products

By Coating Type

Coated Catheter

Uncoated Catheter

By Lumen

Single-lumen

Multi-lumen

By End User

Hospitals & Clinics

Diagnostic Imaging Centers

Other End Users

Regions and Countries Covered

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Medtronic Plc

Boston Scientific Corp

Stryker Corporation

Johnson & Johnson

Pneumbra, Inc

Abbott Laboratories

Terumo Corp

InNeuroCo

Cook Medical Holdings LLC

Balt Extrusion

Get more information on this report

Middle East and Africa Neurovascular Catheters Market Report Coverage and Deliverables:

The "Middle East and Africa Neurovascular Catheters Market Size and Forecast (2025–2033)" report provides a detailed analysis of the market covering below areas:

Middle East and Africa Neurovascular Catheters market size and forecast at regional and country levels for all the key market segments covered under the scope

Middle East and Africa Neurovascular Catheters market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Middle East and Africa Neurovascular Catheters market analysis covering key market trends, regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Middle East and Africa Neurovascular Catheters market

Detailed company profiles, including SWOT analysis

Middle East and Africa Neurovascular Catheters Market Geographic Insights:

The geographical scope of the Middle East and Africa Neurovascular Catheters market report is divided into: Turkiye, the UAE, Saudi Arabia, Bahrain, Oman, Egypt, South Africa and Africa, Algeria, Nigeria, Kuwait, and Qatar. Turkiye held the largest share in 2024.

The MEA neurovascular catheters market varies widely across countries due to differences in infrastructure, healthcare investment, and procedural capacity. Turkiye and Saudi Arabia are large markets, driven by modern hospitals, dedicated stroke centers, and widespread adoption of catheter-based interventions. Urban centers such as Riyadh and Jeddah lead in procedural volumes and infrastructure development.

The UAE follows closely, with well-established tertiary care facilities, advanced imaging capabilities, and strong private healthcare participation. Hospitals are early adopters of coated and multi-lumen catheters in stroke and aneurysm procedures. Egypt represents a high-potential market in North Africa, with expanding hospital infrastructure and increasing access to neuro-interventional procedures in Cairo and Alexandria. Hospitals are investing in hybrid angiography suites and stroke units to improve procedural outcomes. South Africa and other Sub-Saharan countries are witnessing the gradual adoption of advanced catheters, largely in private hospital networks and urban centers. Differences in healthcare funding, infrastructure, and clinician expertise affect regional adoption, but rising stroke incidence, aging populations, and healthcare modernization initiatives continue to drive demand across MEA. Hospitals and clinics remain the dominant end users, while diagnostic imaging centers and tertiary care hospitals are emerging as secondary adopters.

Get more information on this report

Middle East and Africa Neurovascular Catheters Market Research Report Guidance:

The report includes qualitative and quantitative data in the Middle East and Africa Neurovascular Catheters market across product, coating type, lumen, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Middle East and Africa Neurovascular Catheters market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Middle East and Africa Neurovascular Catheters market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Middle East and Africa Neurovascular Catheters market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover the Middle East and Africa Neurovascular Catheters market segments by product, coating type, lumen, end user, and geography across Turkiye, the UAE, Saudi Arabia, Bahrain, Oman, Egypt, South Africa and Africa, Algeria, Nigeria, Kuwait, and Qatar. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Middle East and Africa Neurovascular Catheters market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Middle East and Africa Neurovascular Catheters Market News and Key Development:

The Middle East and Africa Neurovascular Catheters market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Middle East and Africa neurovascular catheters market are:

In November 2025, Vesalio announced FDA 510(k) clearance for its latest aspiration devices intended for peripheral and neurovascular thrombectomy applications, broadening the range of thrombectomy solutions available to clinicians, including those treating MEA patient populations.

In February 2025, Johnson & Johnson MedTech introduced the CEREGLIDE 92 Catheter System, a next‑generation large‑lumen neurovascular catheter system designed to enhance access and delivery during acute ischemic stroke interventions — a platform now influencing treatment standards in advanced MEA hospitals.

Key Sources Referred:

World Health Organization (WHO)World Heart Federation (WHF)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Middle East and Africa Neurovascular Catheters Market?

The Middle East and Africa Neurovascular Catheters Market is valued at US$ 78.6 Million in 2024, it is projected to reach US$ 148.1 Million by 2033.

What is the CAGR for Middle East and Africa Neurovascular Catheters Market by (2025 - 2033)?

As per our report Middle East and Africa Neurovascular Catheters Market, the market size is valued at US$ 78.6 Million in 2024, projecting it to reach US$ 148.1 Million by 2033. This translates to a CAGR of approximately 7.6% during the forecast period.

What segments are covered in this report?

The Middle East and Africa Neurovascular Catheters Market report typically cover these key segments-

End User (Hospitals & Clinics, Diagnostic Imaging Centers, Other End Users)

What is the historic period, base year, and forecast period taken for Middle East and Africa Neurovascular Catheters Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East and Africa Neurovascular Catheters Market report:

Historic Period : 2022-2023

Base Year : 2024

Forecast Period : 2025-2033

Who are the major players in Middle East and Africa Neurovascular Catheters Market?

The Middle East and Africa Neurovascular Catheters Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic Plc

Boston Scientific Corp

Stryker Corporation

Johnson & Johnson

Pneumbra, Inc

Abbott Laboratories

Terumo Corp

InNeuroCo

Cook Medical Holdings LLC

Balt Extrusion

Who should buy this report?

The Middle East and Africa Neurovascular Catheters Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Middle East and Africa Neurovascular Catheters Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Middle East and Africa Neurovascular Catheters Market

Get Free Sample For Middle East and Africa Neurovascular Catheters Market