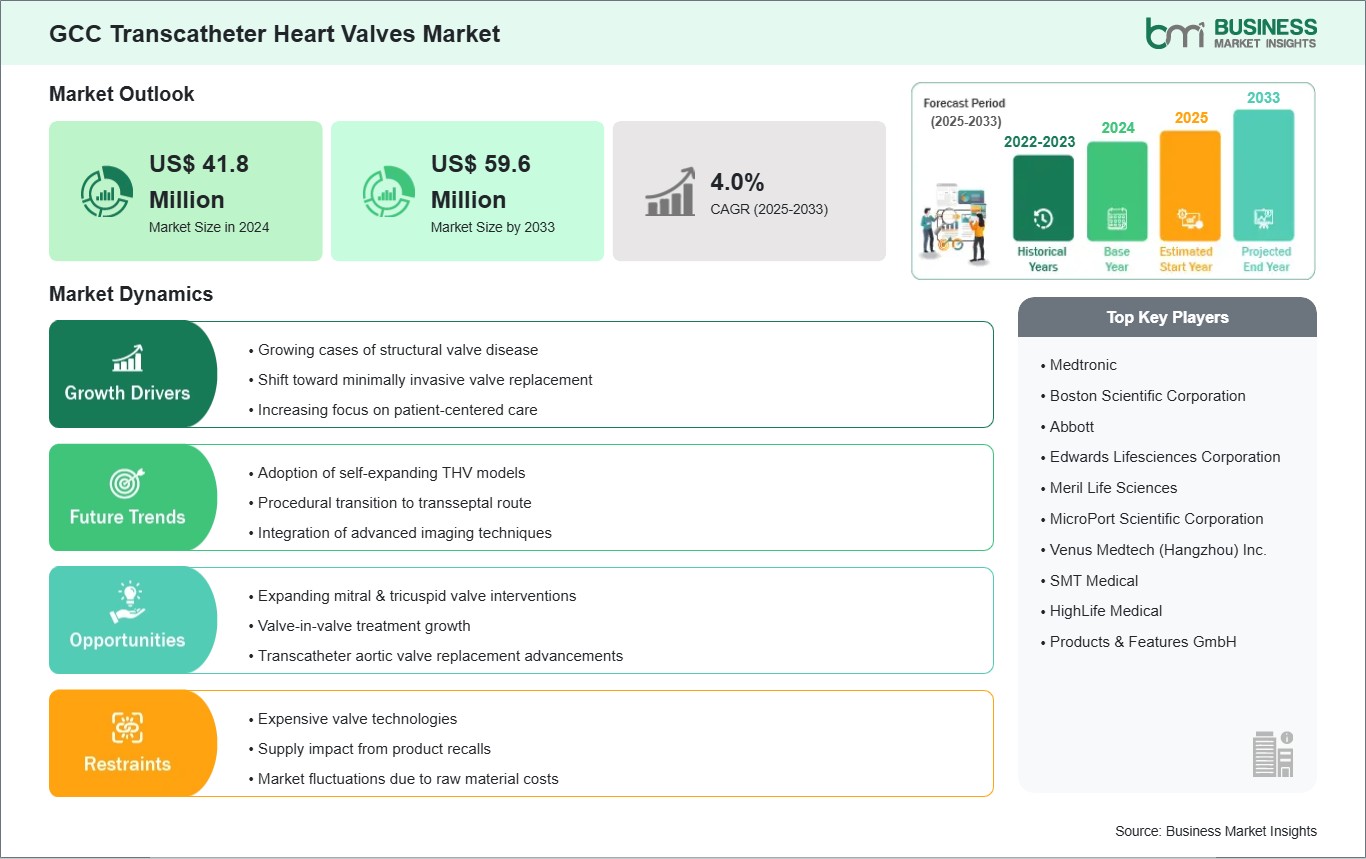

Growing cases of structural valve disease

In the GCC region, valvular heart disease is recognized as a growing health concern, especially among the aging population and individuals with lifestyle-related risk factors such as obesity, diabetes, and hypertension. While traditionally rheumatic heart disease was less common than in some other regions, the rise of non-communicable diseases is contributing to more cases of aortic and mitral valve dysfunction. Hospitals in major cities such as Riyadh, Dubai, and Doha are reporting higher numbers of patients requiring advanced valve interventions.

The region's healthcare systems are highly developed but concentrated in urban centers, meaning access to traditional open-heart surgery is sometimes limited for patients in smaller towns. Transcatheter heart valves offer a minimally invasive alternative, reducing hospital stay and surgical risks, which is especially important for older or high-risk patients. Well-equipped cardiac centers, specialist training programs, and growing clinical confidence in catheter-based procedures support the adoption of these therapies.

Government initiatives across the GCC are also helping drive adoption. Health authorities are supporting state-of-the-art cardiac care, including public and private partnerships that enhance access to advanced interventions. Awareness campaigns and early screening programs are improving diagnosis, leading to timely referrals. These factors make the rising prevalence of valvular heart disease a key driver of transcatheter heart valve adoption in the GCC market.

Expanding mitral & tricuspid valve interventions

Historically, transcatheter procedures in the GCC focused primarily on aortic valve disease, but there is increasing attention on mitral and tricuspid valve disorders. Advanced imaging technologies and growing expertise among cardiologists in major cardiac centers are enabling earlier detection and assessment of these complex valve conditions. As physicians gain confidence in performing these procedures, hospitals are gradually expanding their offerings to include mitral and tricuspid transcatheter interventions, creating a significant market opportunity.

Many patients with mitral and tricuspid valve dysfunction are elderly or have multiple comorbidities, making conventional surgery less viable. Minimally invasive transcatheter therapies allow these patients to receive effective treatment with reduced risk and faster recovery. Cardiac centers in Dubai, Abu Dhabi, Riyadh, and Doha are performing these procedures, often supported by multidisciplinary heart teams and regional referral networks.

For medical device companies, this represents a promising opportunity to grow their presence in the GCC market. Providing training, clinical support, and procedural guidance can help hospitals expand their expertise and patient volume. As more clinicians and patients become aware of the benefits, mitral and tricuspid valve applications are poised to become an important segment of the region's transcatheter heart valve market.